MTTR - Matterport's Inability To Scale Explained

2023-07-14 14:01:12 ET

Summary

- In this article, we discuss why MTTR remains depressed and couldn't scale growth despite growing adoption, strategic acquisitions, and strategic partnerships.

- Matterport's inability to scale stems from its linear revenue model and self-competition, evident from the discrepancy between its 75% CAGR adoption growth and 13.5% CAGR revenue growth.

- We believe that cloud revenue and monetizing end-users are key to scaling revenue growth and capturing the value it provides to the market.

Introduction

Gone are the days when Matterport's ( MTTR ) share price was supported by the SPAC's $10 NAV. This "feature" had capped MTTR's downside while retaining full upside potential. In our previous coverage , we gave Matterport price targets between $18 - $90 on the basis that it can capture 1%-5% of its targeted addressable market. The MTTR share price front ran expectations to hit as high as $37.60 before the market crash due to the 2022 inflation-interest rate fiasco.

Today, MTTR is declined over 90% of its all-time high. Not only did MTTR fail to meet its 2022 revenue guidance, but we believe MTTR also lost another major investment value proposition - the potential of getting acquired by tech giants. So we'll be re-examining our initial thesis for MTTR after 2 years since our last coverage.

In addition, the digital twin landscape has changed dramatically with competition coming from different levels of the spatial computing software stack, namely Unity ( U ). So is MTTR overvalued despite its 90% decline from ATH? How is MTTR positioned in the market today? That's what we also want to find out in this article.

Re-examining Past Thesis

1. Proven Concept Without Ability To Scale

We gave MTTR credit for proving market demand for digital twins and virtual space management, but we can't say the same for its ability to scale. We believe the problem lies in its inability to effectively monetize its adoption.

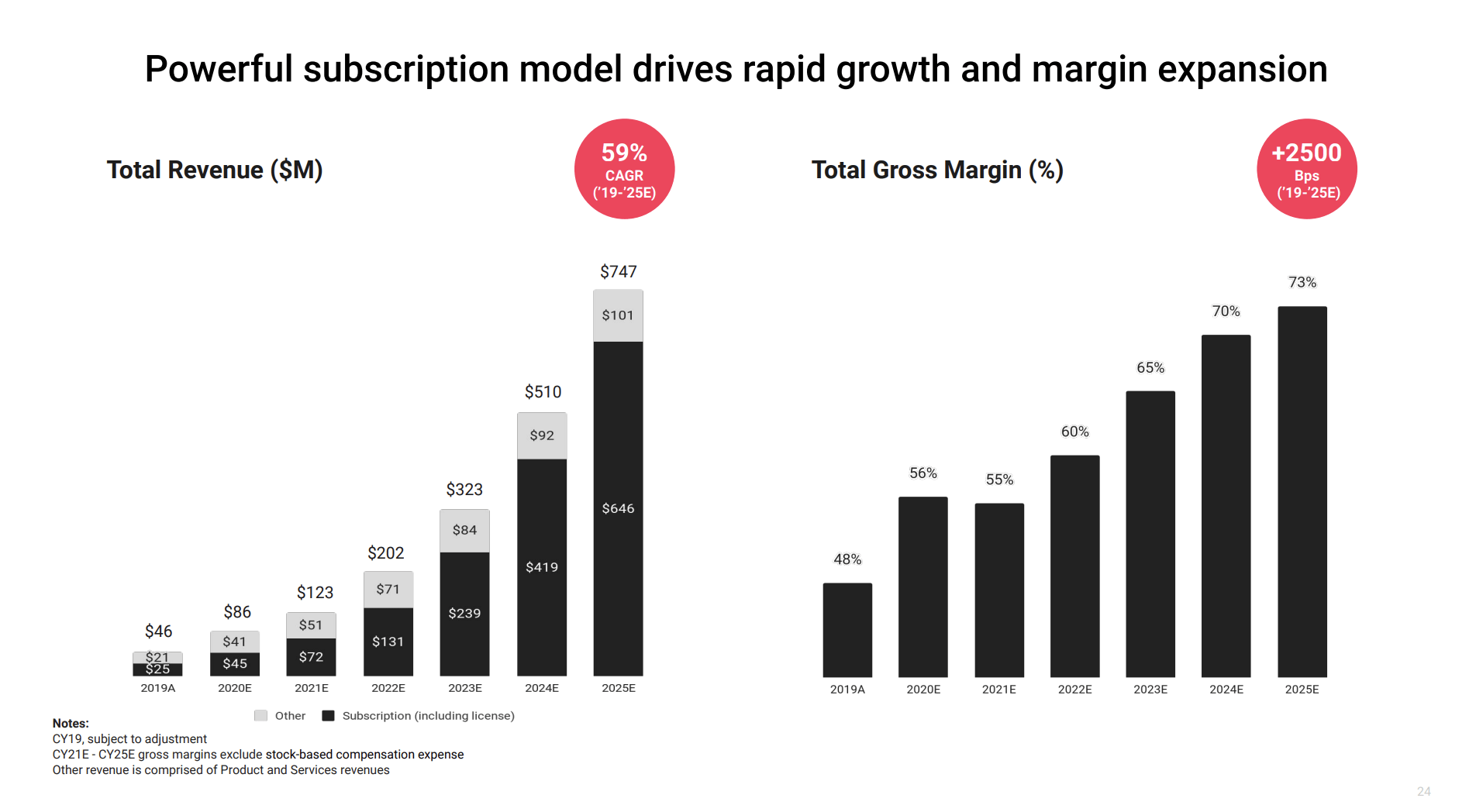

In our previous coverage, we stated that MTTR guided a 59% revenue CAGR growth through 2025. MTTR has indeed met this expectation in terms of adoption, but not revenue.

Since June 2021, MTTR's subscribers increased from 250k to 770k , space under management grew from 4.4mil to 10mil, sqft in the database grew from 10bil sqft to 30bil sqft. This represents a 75% CAGR in terms of adoption.

However, MTTR couldn't translate adoption into revenue. During the same period, MTTR's quarterly revenue only grew 13.5% CAGR (from $29.5mil in 2021Q2 to $38mil in 2023Q1).

We believe we can explain MTTR's inability to scale revenue.

Failure to Capture Lucrative Revenue Source: Usage Revenue

MTTR's revenue model is split into 3 segments: Subscription, Licensing, and Products (hardware). The problem with this revenue model is that the relationship between revenue growth to adoption growth is very linear.

- For every unit of active space under management, MTTR earns a fixed rate (about $0.4 to $0.9 per active space based on its subscription plans ).

- For every product sale, MTTR earns a fixed revenue for every sale of its camera (such as the Pro 3).

This revenue model omitted the most lucrative part of the business - Usage.

Unity, a major competitor in the digital twin domain, also has subscription revenue. But subscription revenue only represents a third of its total revenue . The majority of its revenue is derived from "Usage". Both Unity and MTTR have subscription revenue, but Unity can further monetize its products and services through ads and cloud services.

In this sense, the relationship between Unity's revenue growth and adoption growth is non-linear. This is because a digital twin asset created by 1 developer can serve unlimited end users and Unity can monetize these end users as well.

This is the same for cloud services. Digital twin developers on Unity's platform are required to create and render their models on the cloud before running them on the device. A single developer could create an unlimited number of models. The more models are created, the more revenue Unity can accrue.

Self-Competition

Product sales contribute about $9mil in revenue every quarter without growth since 2021Q2 ($9.244mil in 2021Q2 vs $9.4mil in 2023Q1). This stagnating growth can be explained through self-competition.

A new set of MTTR camera hardware cost around $2,500 (Pro 2) to $5,995 (Pro 3). This is a double-edged sword. On one hand, this represents a substantial earnings potential (a quarter of MTTR's revenue is product sales). On the other hand, this also slows adoption.

To increase adoption, MTTR launched an app for the iPhone to utilize its LiDAR sensor to capture spaces in 2021. Now that phones are becoming more advanced, justifying a $6000 investment in hardware for capturing 3D spaces could become harder to justify.

From another perspective, MTTR's app is competing against its Pro camera. With the launch of Apple Vision Pro, which also has a high capability to capture spaces in 3D, the demand for MTTR's specialized hardware could dwindle.

Therefore, although advancement in third-party devices (such as the iPhone and Vision Pro) could increase MTTR's adoption, this adoption could come at the expense of product revenue.

2. A Less Attractive Acquisition Target

In our previous coverage, aside from exponential adoption, our bullish thesis was also built on the possibility of getting acquired by large tech giants. We were hoping MTTR to be acquired at high valuations similar to how ironSource , Weta , Ziva , and SpeedTree are acquired by Unity to complete its RT3D development platform.

However, platforms like Unity and Epic Games' Unreal Engine already have their digital twin solutions. Unity even guided investors that its digital twin will be one of its growth drivers to hit $1bn EBITDA by 2024.

In addition, MTTR's digital twin is very niche. MTTR's digital twin only focuses on real estate. In comparison, Unity's digital twins solution is being applied to a wider range of applications including architectural, manufacturing, automotive, airports, and other applications.

Moreover, MTTR's digital twin feature might trail behind other digital twin solutions. For instance, a feature of Unity's digital is the ability to simulate in real-time . Based on MTTR's product demonstration , it doesn't seem that MTTR has this unique feature.

These factors make MTTR less likely to be acquired at high valuations.

Valuations

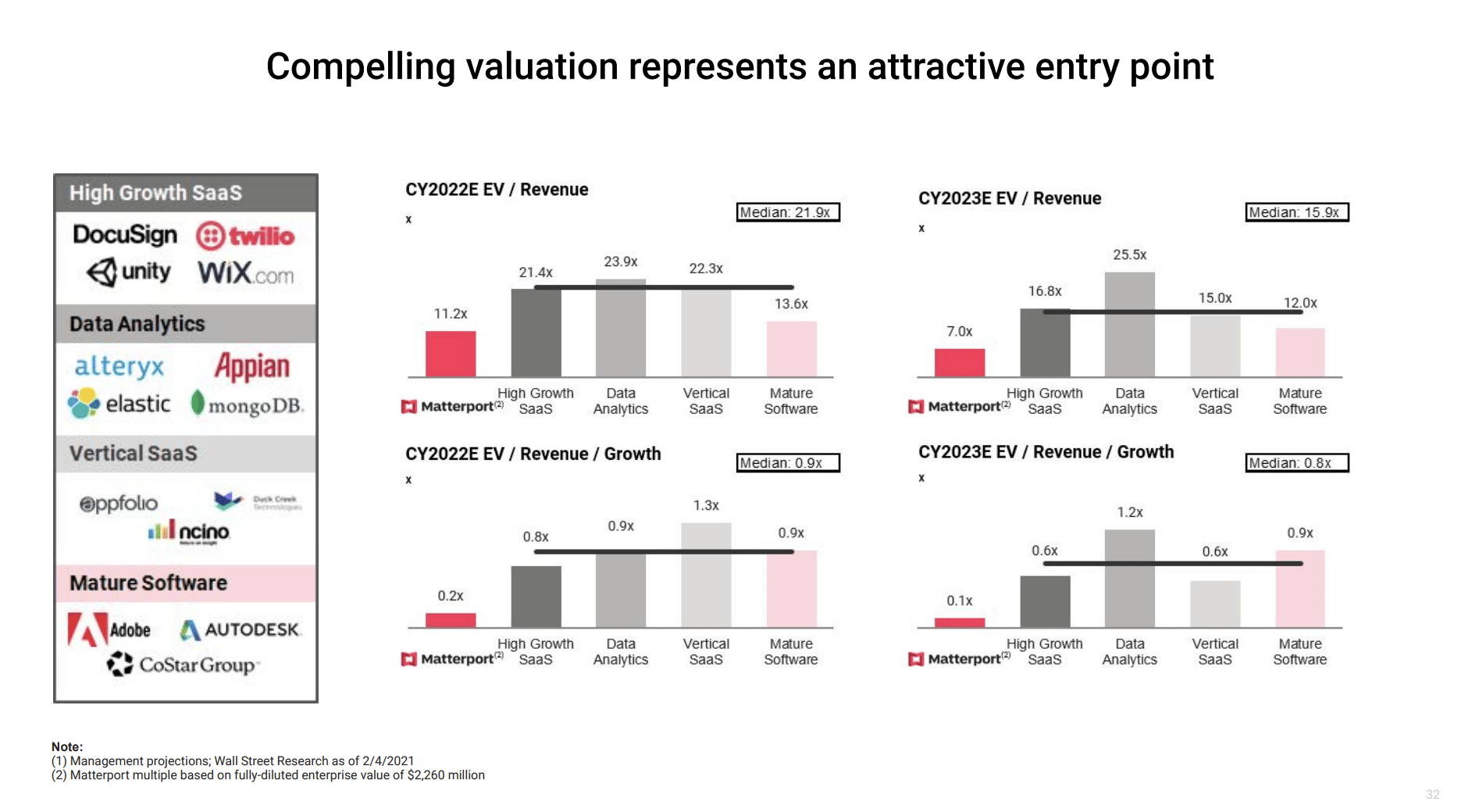

Before MTTR's merger with Gores Holdings (the SPAC), MTTR suggested that DocuSign ( DOCU ) and Twilio ( TWLO ) are suitable comps as MTTR classifies itself as "high-growth Saas" together with DOCU and TWLO. On average, both DOCU and TWLO are also growing at a similar pace as MTTR, about grew about 13% YOY.

Comps used by MTTR (Matterport)

{kind=link}

DOCU and TWLO are currently trading at 3.8x and 3.2x 2023Q1 annualized revenue, while MTTR is trading at 5.6x 2023Q1 annualized revenue. This is one sign that MTTR is more overvalued than comps.

The other sign that MTTR is currently overvalued is referenced from MTTR's guidance. MTTR previously justified its $2.90bn valuation by guiding a 59% CAGR through 2025. MTTR now only trades at a third of its initial valuation, which priced MTTR at about 20% CAGR growth rate. But since MTTR is only growing at 13.5% CAGR, MTTR is also overvalued by its standards.

MTTR's Guidance Before Going Public (Matterport)

{kind=link}

Verdict and Final Remark

We now know why MTTR's adoption growth failed to translate into meaningful revenue growth. We now also know why MTTR's share price remains depressed, despite strategic acquisitions ( VHT Studios and Enview ) and strategic partnerships (such as Equinox and Compusoluciones ).

Fortunately, the current market forces could be advantageous to MTTR. The cooling inflation and the spatial computing hype could see rotation specifically to VR stocks such as MTTR.

Despite our pessimistic view on MTTR, this is not over for MTTR. MTTR can still be a viable investment in the future if MTTR can find more ways to capture the value it provides for its customers and end-users. Until then, We'll choose Unity over MTTR due to Unity's more synergistic revenue model, product offerings, and position in the spatial computing software stack.

For further details see:

Matterport's Inability To Scale Explained