MATW - Matthews International: Downsides Corroborated By Economics And Valuations

2023-10-26 22:11:50 ET

Summary

- Matthews International is a potentially cheap offering in the diversified support services industry.

- The company operates in the memorialization business, industrial technologies, and brand solutions segments.

- The company's economics and potential for growth are lacking, supporting a hold across all investment horizons.

Investment Briefing

A broad selloff across global equity markets has opened the funding window to run money across a more selective investment profile. This includes sub-specialty and niche sectors, including the diversified support services industry.

After a sharp consolidation off its August '23 highs, Matthews International ( MATW ) has entered the fore as a potentially cheap company with interesting economics in situ. The company has been around since 1850, specializing in the memorialization business, but has diversified its scope to industrial tech and brand solutions.

Of the company's 3 segments:

- The memorialization business deals with memorials—caskets, cremation-related products, and so forth, all for the cemetery and funeral home industries.

- The industrial technologies segment creates energy storage solutions, product ID, and warehouse automation technologies for order fulfillment.

- Lastly, the SGK brand solutions segment is in the brand management business, with offerings like printing plates, imaging services and design services predominantly for the consumer goods and retail industries.

Whilst the company's long-standing, deep customer networks and diversified scope of operations are appealing, on closer examination, the economics to form a mid to long-term investment compounder are lacking in my opinion. In that vein, my recommendations are the following, based on various investor time horizons:

Fundamental/economic bias:

(i). Short-term (coming 12 months): Potential value, with earnings multiples compressed, balanced by high relative pre-tax margins.

(ii). Mid-term (1–3 years): Sales + earnings growth flat, little support for mid-term capital gains,

(iii). Long-term (3 years+): Business returns flat, divesting capital (not investing for growth), dividend yield not attractive.

Technical bias:

Neutral across all respective time frames.

The company will report its full-year fiscal '23 earnings into the coming weeks/months, and will require a mammoth effort to attract demand at these current prices. On the bounce of probabilities, my estimate is that it won't surprise to the upside vs. the market's and consensus' expectations. Net-net, I rate MATW a hold at this stage.

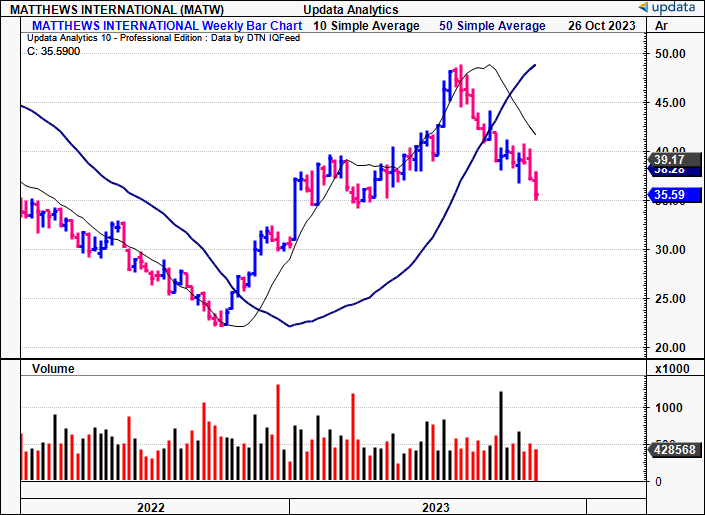

Figure 1. MATW long-term price evolution, now trading below 50DMA and 200DMA as of last 8 weeks continuous.

{kind=link}

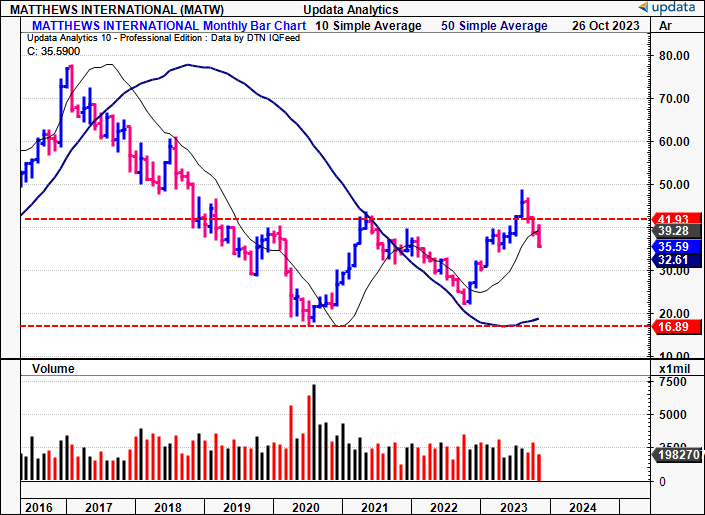

Figure 2. MATW monthly returns, trading within range since 2018, unable to break + hold $41-$42 despite 3x tests in this time frame.

{kind=link}

Critical investment facts supporting hold thesis

1. Macroeconomic backdrop

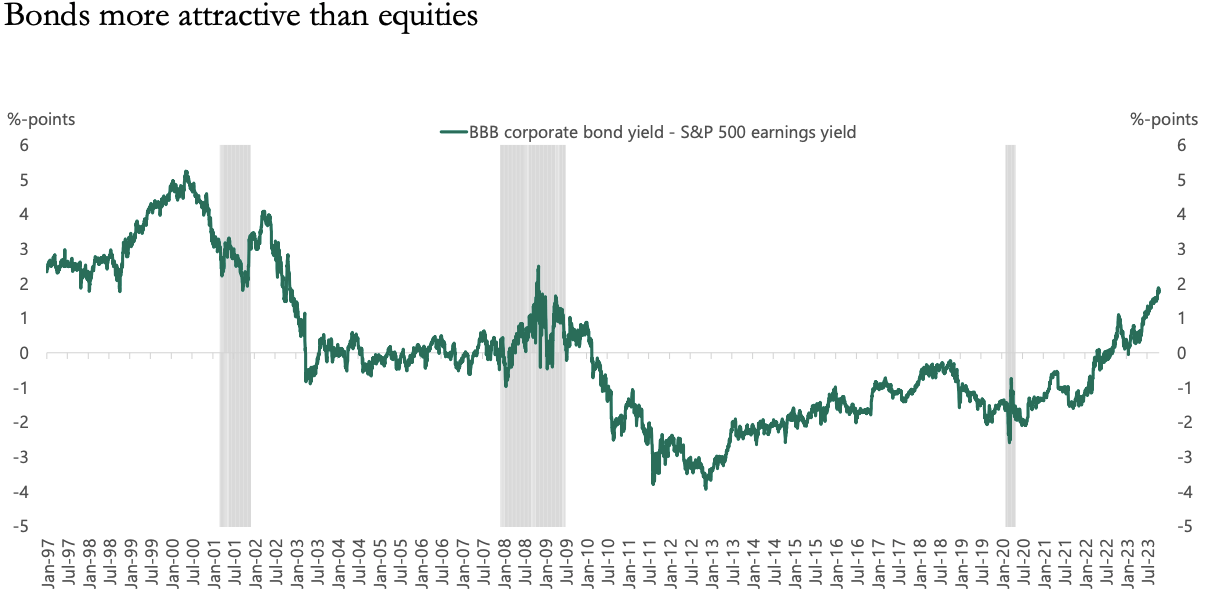

The investment landscape has shifted immensely in '22–'23 and a new value paradigm has emerged. Or, you could say, re-emerged. Fixed rates along the duration curve in both Treasuries/Governments and high-yield corporates have set a high hurdle for equities moving forward. Only the highest-return businesses with exceptional economics are likely to be rewarded without the liquidity support of quantitative easing ("QE") and other Fed liquidity programs.

A recent set of slides from Apollo Global Management makes a compelling case for investing in bonds—particularly high-yield corporate issues. As you can see in Figure 3, Apollo suggests that bonds are currently "more attractive" at the BBB rating, when factoring in yields on the notes less the S&P 500 earnings yield.

Figure 3.

{kind=link}

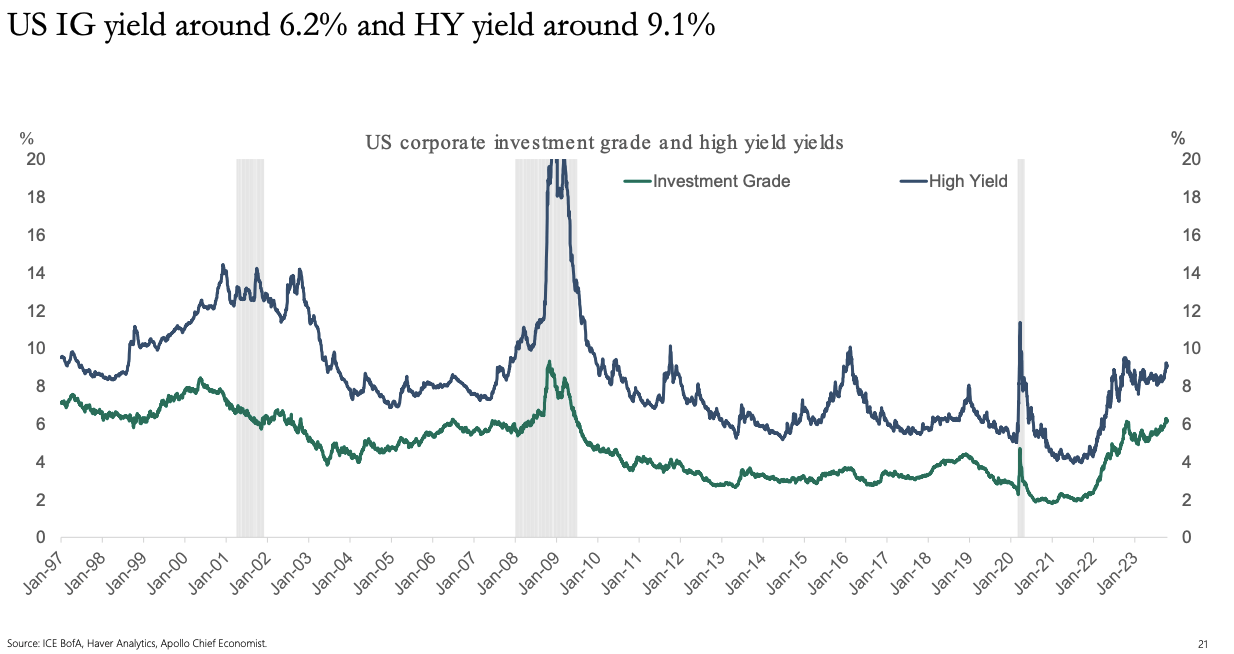

Not to mention, US investment grade and high-yield corporate issues are offering 6% and 9% average starting yields at the time of publication. This is an attractive proposition, given (1) the fact these bonds are statistically cheap, so you're getting a high yield on cost, and (2), if/when yields these issues begin to compress again, you're positioned to capture a return on the bond's pricing as well.

As mentioned, the bar for equities has been set tremendously high going forward.

Figure 4.

{kind=link}

2. Price implied expectations

With the bar set so high for equities vs. the last decade, the market's discounting mechanism is far more 'compressive'. Companies really need to show us something exceptional by way of business economics for market's to discount future performance to continuously higher levels.

In that vein, the market's expectations for MATW includes the following:

(i). Trading at ~$35.60/share at 13x forward earnings implies the market expects $2.74/share in forward earnings, a 5% YoY decrease. It expects $94mm in pre-tax earnings with the same logic ($1.9Bn EV / 20.03x = 94) and ~$1.88Bn in sales, 23% and 7% YoY growth respectively. Consensus expects it to grow earnings by ~6% from '23–'25, which is reasonable to extend as a forecast out to '28.

(ii). It also trades at 1.3x EV/invested capital, a small market value on its investments. MATW's TTM returns on capital employed into the business are 4.9%, and the market forecasts 3.8% ROIC going forward (1/1.3x4.9%) = 3.8%). It expects MATW to reinvest 16% of pre-tax earnings or $21-$22mm on this. The market is therefore forecasting MATW to compound its intrinsic value at just 0.6% over the coming 12 months (ROICxRI).

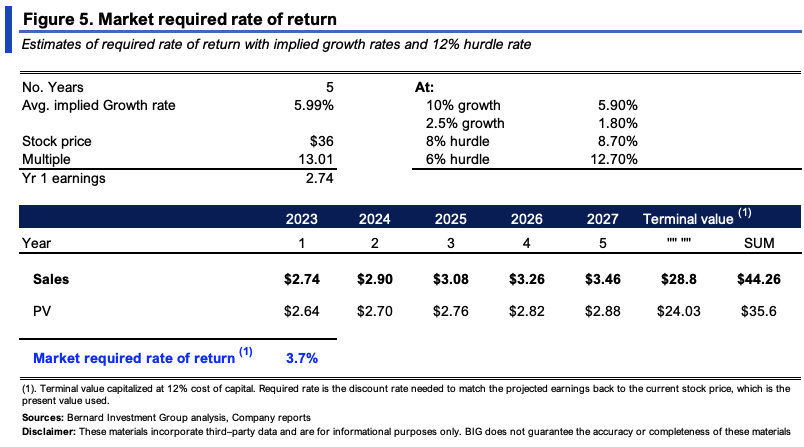

(iii). Given the combination of 1) predictable cash flows (due to its maturity) and 2) the embedded growth of intrinsic value, the market requires just 3.7% return for compensation of the perceived risk, ranging from 1.8–12.7% based on various scenarios seen in Figure 5.

In this vein, the bar has been set reasonably low for MATW in the coming 12 months. Its next set of numbers is therefore critical to either support or negate this view.

{kind=link}

3. Bias from economic value created + on offer

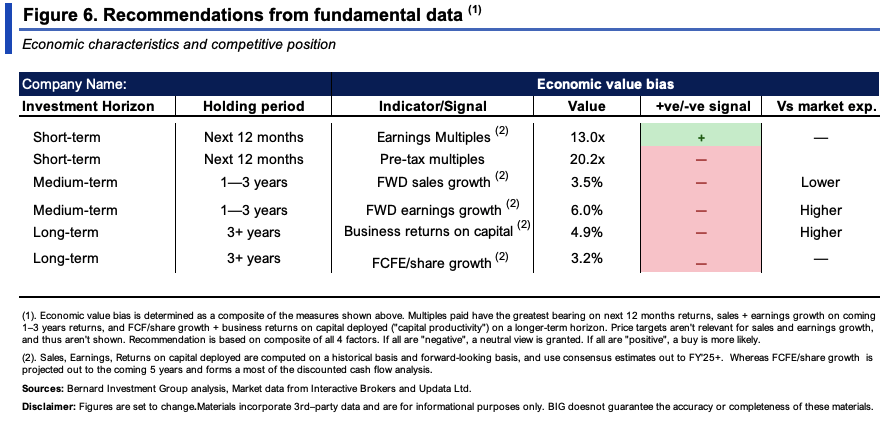

On inspection, there is a lack of support to buy MATW across all time horizons, as seen in Figure 6.

Critically, the following factors illustrate this reasoning:

- In the short-term, the compressed earnings multiples may offer scope for a repricing in the next 12 months. This is balanced by the fact MATW sells at 20x forward EBIT, ~40% premium to the sector.

- Projected forward sales growth is below market expectations, and low on absolute terms. Earnings growth is also low in absolute terms, reducing the scope for medium-term capital appreciation (1-3 years).

- Over the long-term, the prospect of compounding its FCF/share and return high rates on capital deployed is also low.

{kind=link}

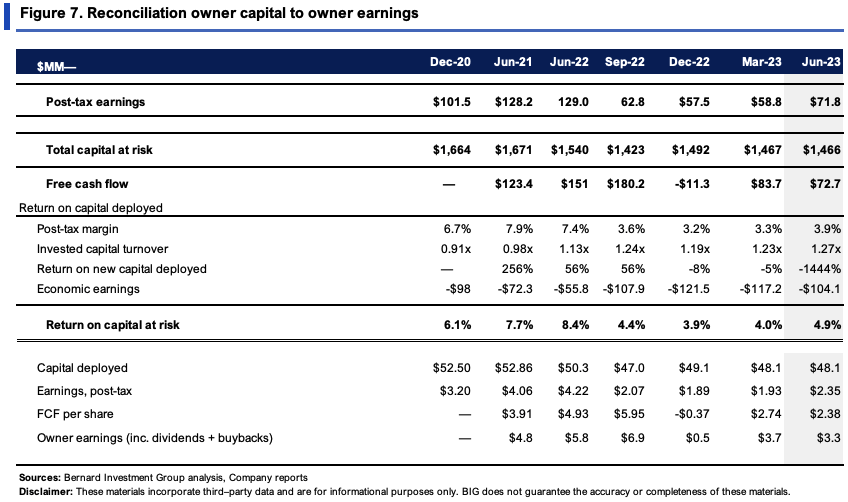

The economic reasons for no multiple growth, flat financials and poor business returns are abundantly clear in Figure 7.

One, this is a low-margin, low capital turnover business. Unit margins have compressed to <4%, whereas turnover of unit capital (aggregated across all 3 business lines) is ~1.2–1.3x, not nearly enough to overcome the marginal pressures.

Two, MATW has divested ~$4.44/share of capital invested into operations, likely as it isn't profitable enough to maintain this capital intensity. After-tax earnings produced on this capital are still flat on 2-year range at $2.35/share in the TTM.

Three, FCF/share has been lumpy and declining, the same when including all dividends paid up as owner earnings. This reflects the low business returns, which require more earnings/cash flows to be reinvested to maintain MATW's competitive position, slowing growth investment, profit growth, and dividend increases.

Four, based on the lagging business returns, the company has produced an economic loss of $910mm ($831mm inc. dividends), when placing a 12% threshold return on its earnings (12% reflects long term market averages).

{kind=link}

4. Technicals support fundamental bias

Trading of MATW's equity stock has been distributed across a wide range of values in the last 3 quarters (i.e., Q1–Q3 in CY 2023). Critically, time at price has begun to concentrate around the $32–$35 level. This is telling, for two reasons:

(1). The lower pocket of usage has not yet completed a full distribution; instead has been filling the segment shown in Figure 8.

(2). Critically, my view is that the market will continue to fill this region in order to complete the distribution before deciding on its next moves. This supports a neutral view, with little conviction of a repricing to the upside.

Figure 8.

Data: Updata

As seen in Figure 9, the overall distribution of time at price is fairly uniform, with little skew. The 'zero' skewness supports the notion of little directional returns, instead, for MATW to continue trading sideways.

Figure 9.

Data: Updata

In that vein, it's unsurprising to see further downside targets to the $33/share region, based on a daily time frame that looks to the coming weeks. The point and figure studies below have eyed key levels well recently, thereby adding weight to their validity.

Figure 10.

Data: Updata

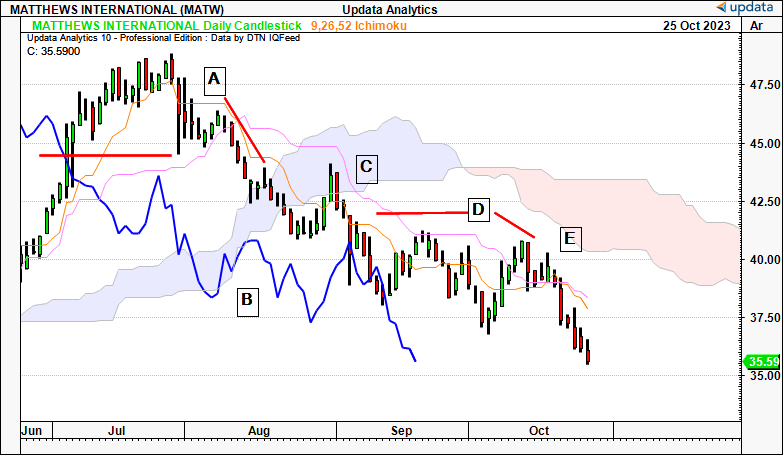

Trend action is equally as important here and the following insights are critically relevant:

- On the daily cloud chart, looking to the coming weeks, we have a large reversal that took place in July at point A, taking out the marabuzo line of a large bullish candle from June. The height of this level could not be retaken. We then saw an evening star formation that crossed the key level, as the price line crossed into the cloud, indicating more downside to come.

- We then crossed beneath the cloud base at point B, a bearish signal.

- Then at point C we had a test back into the cloud with no lagging line support, and a shooting star with subsequent downsides saw bears recapture the market.

- It then descended lower in a 3 wave descent at point D, characterized by 2x dark cloud formations with the arrows shown.

- Finally, at point E we had another shooting star with a confirmatory subsequent bearish candle just last week, continuing the downtrend.

Figure 11.

{kind=link}

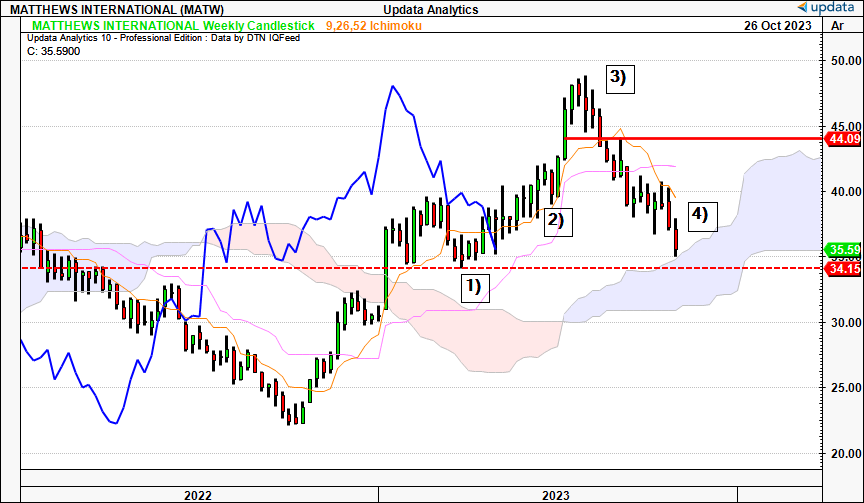

On the weekly, 4 points standout in this analysis:

- A sharp pullback in early '23 that tested the marabuzo line at 1) of the bullish candle in first week of January. That it didn't break this level was key, and saw a sharp rally to point 2.

- At point 2), a large hammer with bullish follow through into the next week saw bullish trend continue.

- Point 3) was the reversal, with a climax top and 2 weeks later the marabuzo line of the large green candle shown was broken. This was clear signal of a reversal in trend.

- We are now at point 4), currently testing the cloud top. A further descent would see us push into this zone, and a cross at ~$30 would clearly support a hold rating.

Figure 12.

{kind=link}

Valuation and conclusion

Relative valuations are balanced, as mentioned earlier, reducing the scope for an attractive entry for the next 12 months. The current 2.6% dividend yield isn't enough to bolster the total return.

To summarize the valuation debate, consider the following:

(1). The market's implied expectations are low on the company, illustrating its selloff in recent times,

(2). Forward sales + earnings growth are projected to be flat, reducing 1-3 year returns,

(3). Based on this analysis, Business returns + FCF growth is the same.

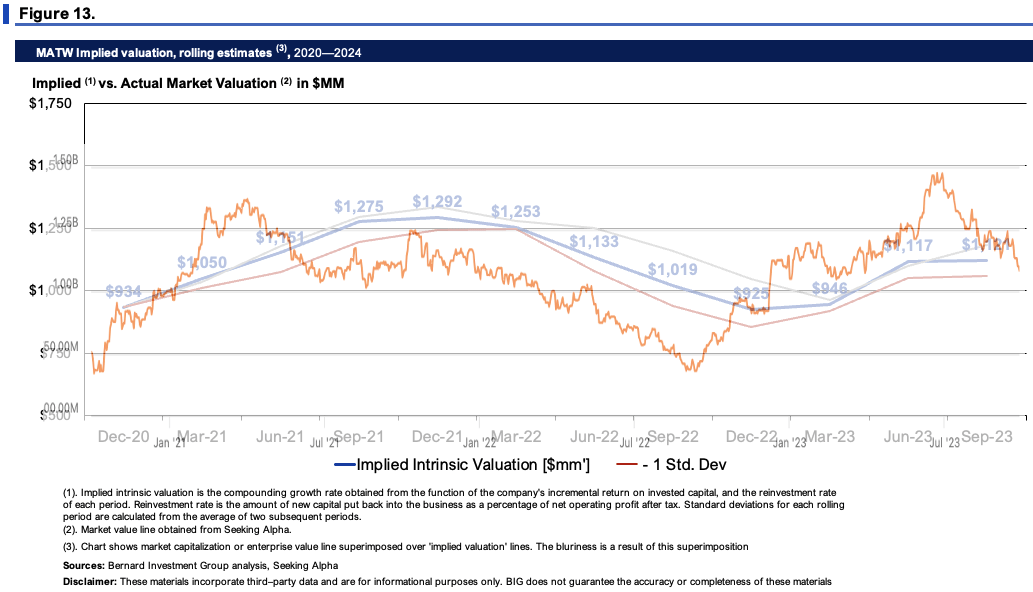

Therefore I see little evidence to suggest a change in expectations and/or that the market has priced MATW incorrectly. In fact, in Figure 13, it shows the market has been an accurate judge of its fair value, compounding MATW's intrinsic value at the function of its ROIC and reinvestment rates.

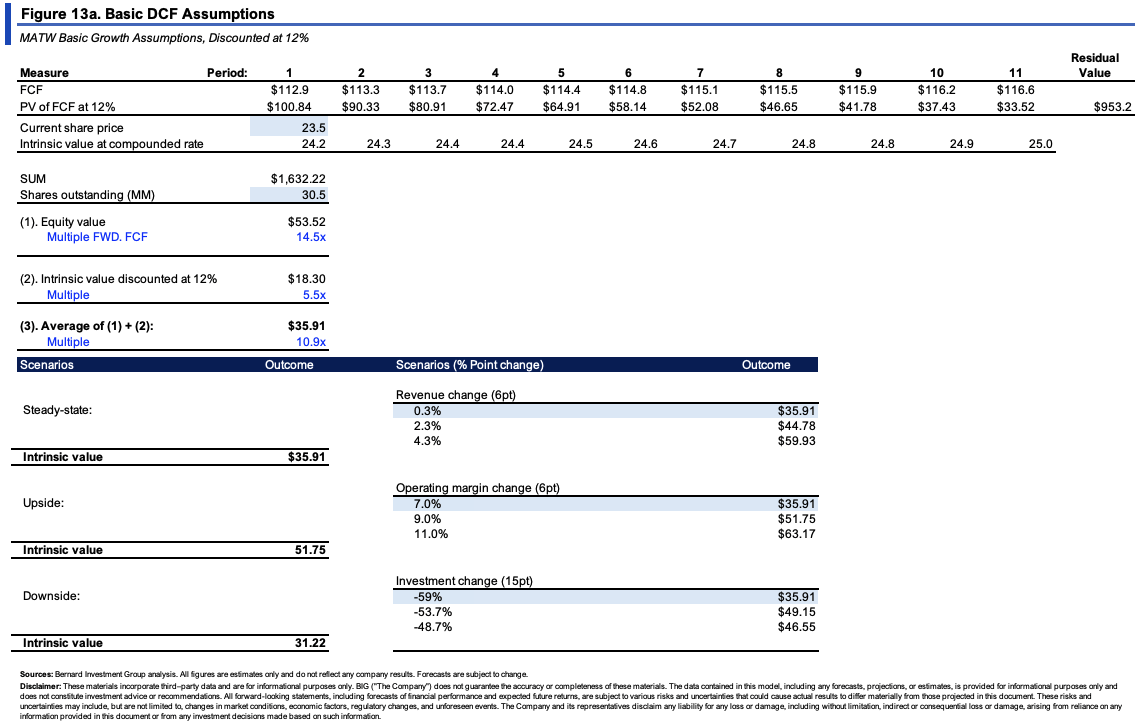

Further, projecting the company's FCFs out to FY'28 at its steady state of operations, then discounting back at our 12% threshold margin, implies the company is fairly valued at ~$35–$36/share in line with where it currently trades (Figure 13a).

{kind=link}

{kind=link}

In short, MATW's diversified offering and deep customer networks aren't well supported by robust economics or potential catalysts to see it trade higher over time. A hold rating is the most probable rating on this company across all time frames, including fundamental and technical data. Net-net, I rate MATW a hold at $35–$36/share.

For further details see:

Matthews International: Downsides Corroborated By Economics And Valuations