MATW - Matthews International: Profit Scaling Limited By Labor Costs

2023-11-03 10:18:48 ET

Summary

- Matthews International has benefited from business development in the energy solutions sector.

- The energy solutions business has seen strong order book growth and is expected to achieve around 40% sales growth for the fiscal year as they liquidate backlog.

- Cost actions are now possible to improve the performance of acquisitions and contribute to the bottom line, leading to a potential earnings bump in that segment.

- The continued underlying value that is supported by the activist agenda and deleveraging means there's still upside from these prices over the next 2-3 year horizon.

Matthews International (MATW) was one of our best picks in 2022-2023. In particular, it benefited from substantial business development, primarily the R+S and Olbrich acquisitions as well as associated massive order increases for energy solutions. Things look good, but there have been latent pressures from labor arrangements that should loosen and provide a deferred bump to profits in the coming quarters. On the retraced prices, MATW is pretty interesting again.

Quarterly Breakdown

Let's take a look at some of the results.

{kind=link}

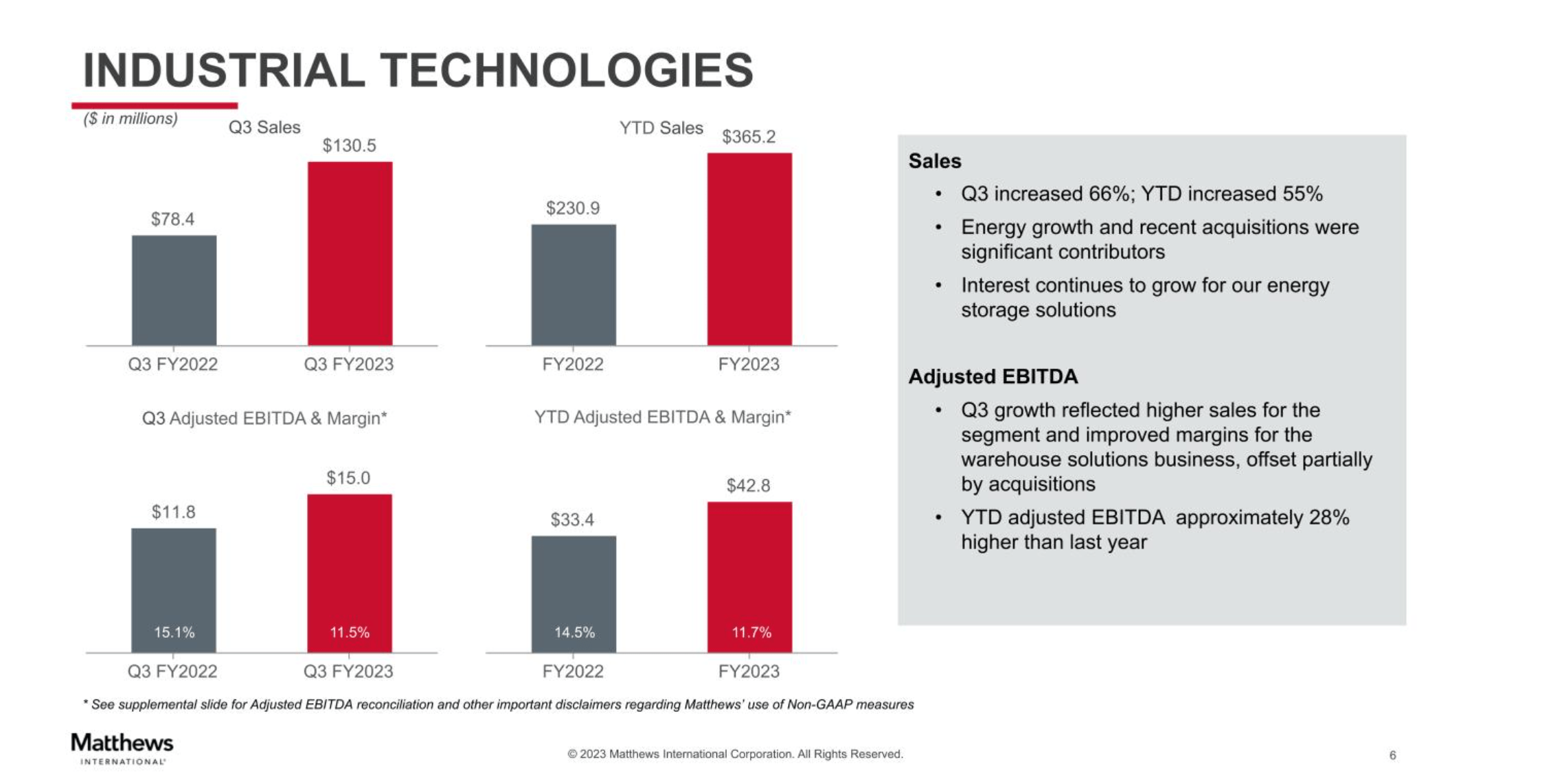

The most important is the industrial technologies segment which is home to the energy solutions business which has been responsible for a lot of orders and for the secular story.

We are continuing to make progress in fulfilling the over $200 million of energy orders announced earlier this year.

These recent orders are being converted gradually into sales, with expectations to convert about half the orderbook and to achieve around 40% sales growth in energy solutions for the FY. Total industrial technologies growth is around 66% as of Q3, but the aforementioned orders came in after the inorganic effects and underline that the segment is seeing strong, secular and underlying growth.

Importantly, EBITDA grew much less than sales for industrial technologies resulting in margin compression. Management addresses this:

Beginning this quarter, cost actions will be taken over the next 12 to 18 months that will improve the performance of these acquisitions and contribute directly to the bottom line. We have been prevented from taking action earlier due to the labor contracts in place at the time of our acquisition, but those contracts have now expired.

Joe Bartolacci, CEO

A latent earnings bump should come as these cost controls are implemented.

{kind=link}

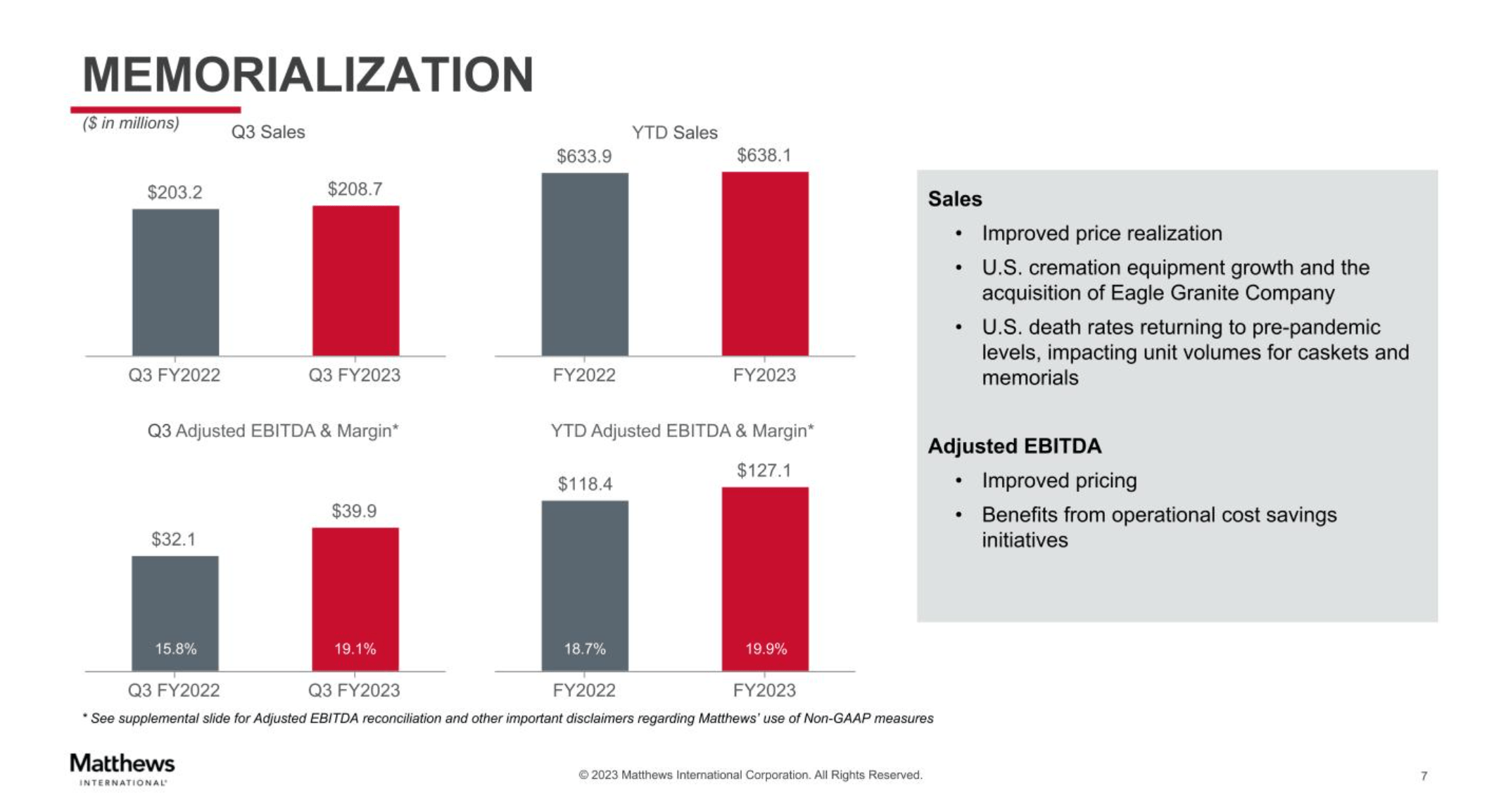

Memorialization is another interesting segment. Margin improvement is happening as pricing actions come through and commodity deflation occurs. The business was suffering a bit due to higher metal costs for memorial plaques and other materials such as lumber. With all these costs substantially receding as the first sign of deflationary pressures in the economy, the resilient underlying business continues to step forward in sales on these higher unit margins.

{kind=link}

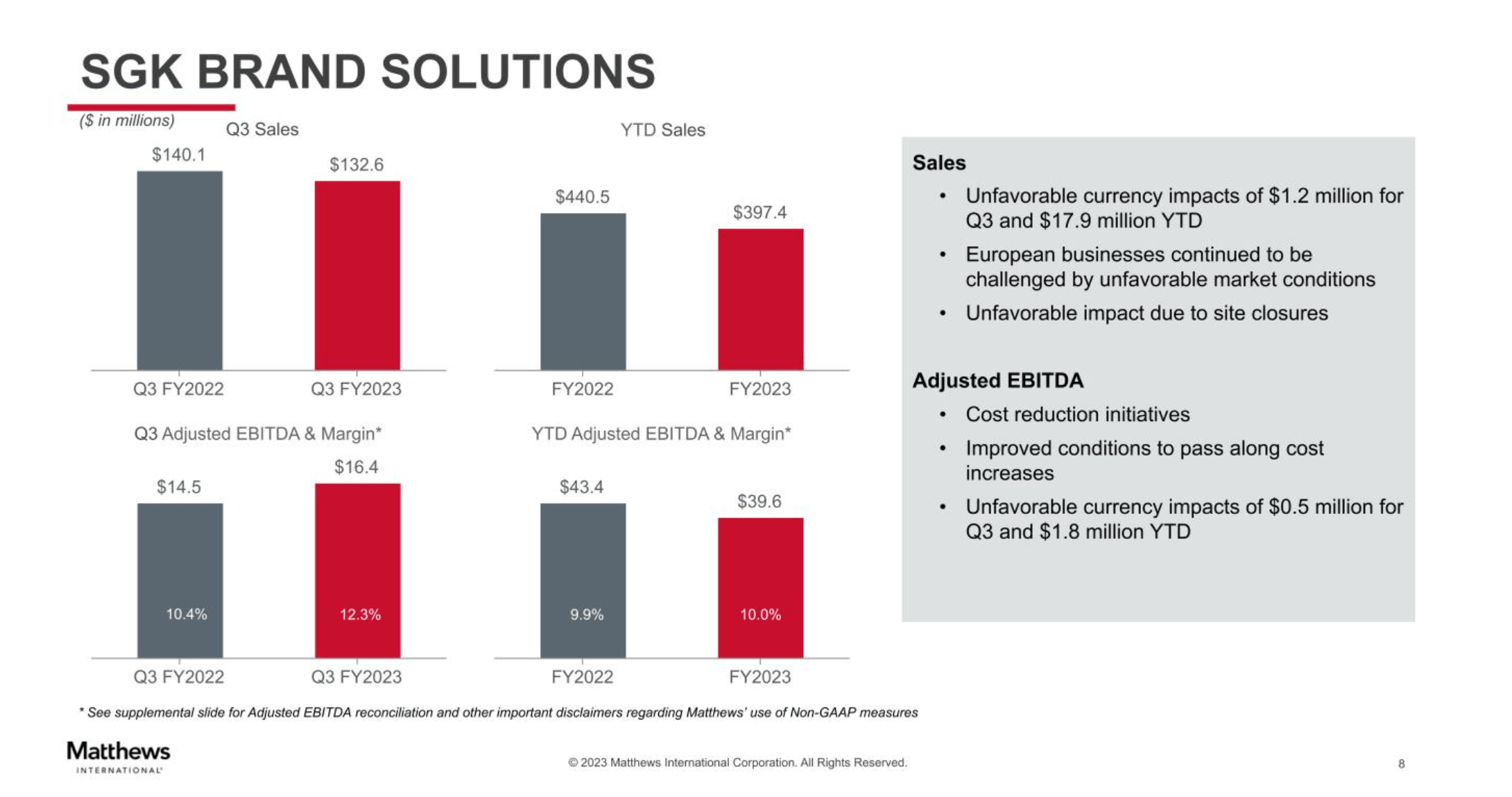

SGK continues to be a pretty uninteresting business, hampered by substantial European exposure that is hitting results in the form of FX, as well as issues such as labor tightness and general customer reticence for making these discretionary spends.

Bottom Line

It's important to remember where the activist interest in this business comes from, which is that there could be a lot of sponsor interest in memorialization, and a potential exit from SGK to invest in the more promising areas including industrial tech. Below is our updated SoTP from our initial valuation, where we have pared down multiples to be conservative due to the higher cost of capital environment.

Valuation (VTS)

We think that with the next printer product that they are coming out within industrial tech, as well as secular growth in energy solutions, EBITDA growth should be possible.

The issue is that net income is under pressure from higher interest rates. MATW has pretty high leverage, and ultimately the growth is beginning to contribute to a deleveraging story more than the SoTP play, especially since the sponsor environment to absorb assets like SGK or memorialization is not going to be favorable. It is still a buy as they deleverage over this downcycle in deal-making.

{kind=link}

For further details see:

Matthews International: Profit Scaling Limited By Labor Costs