MATW - Matthews Is A Backlog Story Now

Summary

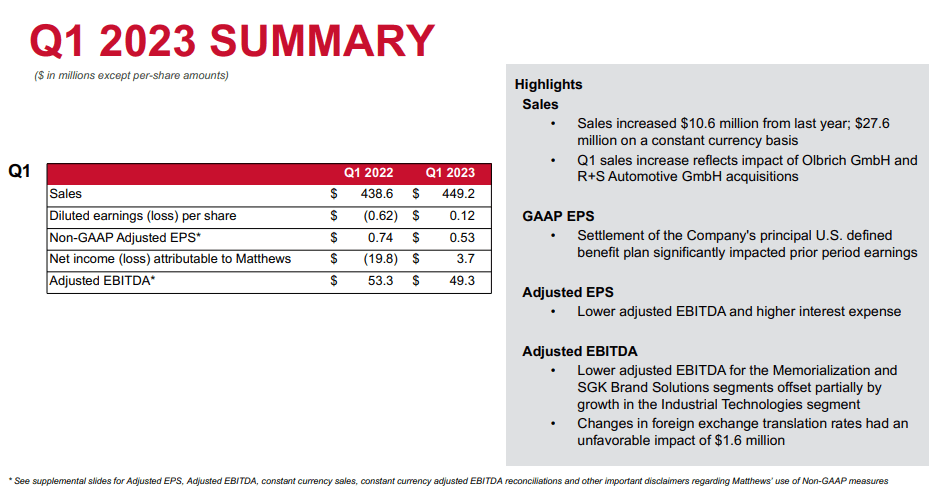

- The Q1 2023 results show give and take from a deflationary commodity environment but also lower death rates from the attenuation of the coronavirus.

- Industrial technologies are mostly seeing growth from consolidation effects, but what matters is that the segment has now created huge backlogs of $200 million.

- The bet on the renewable and EV thesis by Matthews is already bearing fruit, and it is clear that this market in fact exists and will be a growth area.

- Matthews continues to be a strong buy.

Published on the Value Lab 1/27/23

Matthews International (MATW) just reported its earnings. With very pronounced recent appreciation of the MATW stock, the earnings look pretty muted - but that's because MATW proved itself to markets with order backlog. The renewable thesis continues to be very strong, and where markets may have been unsure or unaware of the exposure MATW's had, that is now changing. Moreover, there is the possibility of activism helping out realisation of segments within the company. SGK would be worth getting rid of, as it's a segment we never liked, but the casket business could command a great multiple on private markets too when sponsor activity eventually recovers. While the latter point needs some of the market parameters to normalise, the renewable thesis is market agnostic. MATW has put our portfolio ahead of markets YTD already by 8%, and continues to deserve a strong buy rating.

Quick Q1 Note

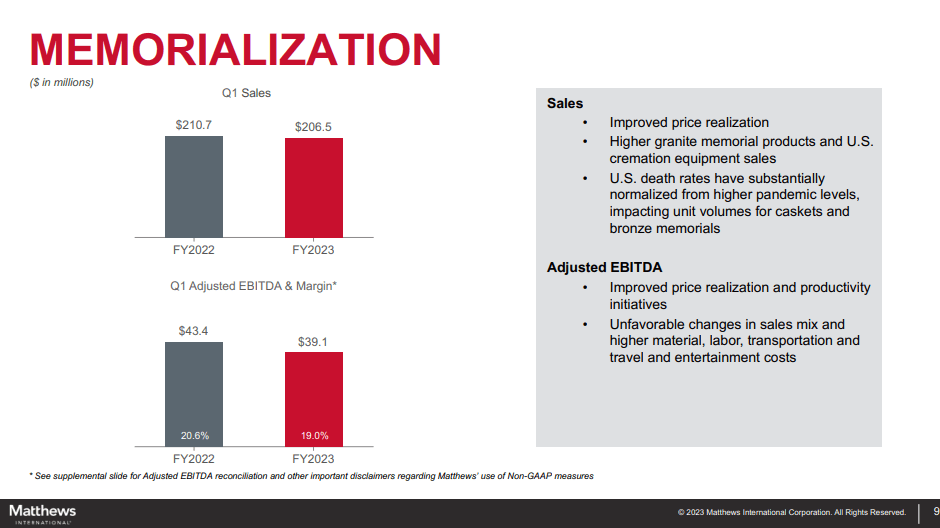

The Q1 presentation shows some pretty good stability. Memorialisation, which includes the sale of incinerators for crematoriums , caskets and plaques and urns for memorialisation, is the majority of the EBITDA and sales representation for MATW. The segment saw slight sales pressures as death rates fall in the US as the coronavirus attenuates, but EBITDA declines with no demonstration of operating leverage to the downside thanks to mitigating factors like deflation of commodity prices, in particular lumber, copper and other metals. In other words, the segment remains very stable YoY.

{kind=link}

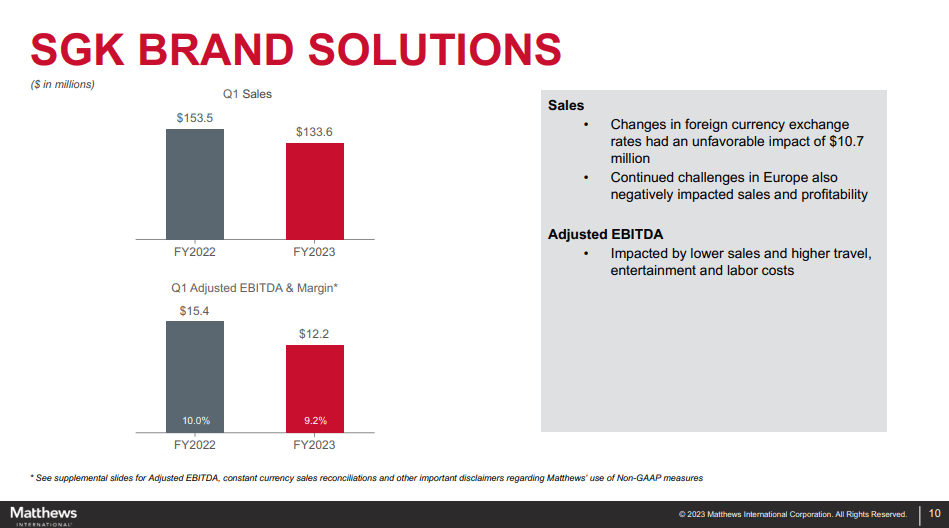

SGK Brand Solutions, which is basically a marketing and printing consulting company with some industrial expertise, is not doing well at all as the pool of money dedicated to marketing spending falls on economic concerns and more conservative discretionary spending by corporates.

{kind=link}

The segment that is the most important element of the story is the industrial technologies segment. The emerging opportunity is the calendering machines that they sell, which can be used to flatten out plates in Li-ion battery production for EVs, to increase the battery performance. While calendering machines have been around for ages, this is an important new application. The growth in sales and EBITDA is not from demand from these new markets yet, it's all just consolidation effects for now as the company acquired two European businesses that would consolidate their offering for EV purposes. In reality, this segment would have given a very flat performance too, and overall results would have looked worse due to the SGK fall-off.

{kind=link}

While investors may be concerned that an imminent and compelling EV thesis is not bearing fruit, it in fact is - but it just hasn't been booked as sales yet. At the beginning of January, the company confirmed massive orders from its industrial technologies segment of $200 million , which is almost 20% of the company's market cap in order value. This is only the beginning, and it proved to markets that MATW was going to be a beneficiary of the EV push - the stock went up more than 10% over the next couple of days. Other positives are that this segment has been harangued by a relatively weak Euro. As exchange rates stabilise or normalise, this growing part of the mix should also benefit from an additional FX push.

Bottom Line

One of the themes for 2023 that we are talking about at the Value Lab is the return of sponsor activity. Sponsor activity has halved in 2022 as LevFin markets were shut, and everyone got a lot more conservative so as not to make more mistakes for pretty unhappy PE fund shareholders who saw their money sunk at the highest rates ever at the market peak in 2021. MATW will be a beneficiary of the return of PE, as they have assets within memorialisation that could command a great multiple if leveraged financing becomes possible again. Memorialisation has very stable cash flows, even if ARPUs are falling with higher cremation rates, and the demographic picture in the US is so good for death care that it even offsets declining ARPUs. SGK may also be saleable in 2023, which would be nice since the business has always been a little iffy in terms of moats, and too pro-cyclical in our books. Still, a recovering economy in 2023 will also see EBITDA contribution return from SGK.

On top of the clear EV thesis that will produce a lot of growth and scale economics for MATW's industrial business, we think cash flows are poised to grow rapidly and to see a lot of realised value for shareholders. The company is still relatively early in its upside push, and we continue to hold shares.

For further details see:

Matthews Is A Backlog Story Now