MNESP - MAV: Municipal Bonds At A Deep Discount

Summary

- MAV's latest discount is pushing near 11%, providing a great sale price for municipal bond exposure.

- Most interest rate hikes should be behind us, so muni bonds should stabilize from here; in fact, as risk-free yields decline, we've seen big rallies from bond funds.

- MAV is designed to invest in muni bonds that are exempt from regular federal income taxes; however, they do this through exposure to some lower-rated debt.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was published to members of the CEF/ETF Income Laboratory on February 4th, 2023.

Pioneer Municipal High Income Advantage Trust ( MAV ) provides investors with exposure to municipal bonds. They look to invest in muni bonds that are going to be exempt from regular federal income taxes. However, instead of investing in all investment-grade muni bonds, they take a "high" yield approach and invest in some holdings below investment grade.

All U.S. states are currently rated investment-grade, even Illinois and New Jersey, but these are the two lowest rated. That means this fund provides exposure outside of just the general obligation state debt that other muni bond funds will contain. Instead, they'll also be invested in revenue bonds that are issued by various projects.

The fund currently trades at a deep discount, and interest rates should be stabilizing. Going forward, that puts the fund in a great position.

The Basics

- 1-Year Z-score: -1.37

- Discount: -12.65%

- Distribution Yield: 5.12%

- Expense Ratio: 1.31%

- Leverage: 39.1%

- Managed Assets: $357.9 million

- Structure: Perpetual

MAV's investment objective is "to pursue high current income exempt from regular federal income tax, with capital appreciation as a secondary objective." To achieve this, the fund "invests in a professionally managed portfolio of municipal securities from across the United States." As mentioned, this includes below-investment grade muni debt to achieve higher relative yields.

The fund is highly leveraged, as are the majority of muni CEFs. The fund's total expense ratio is 2.84% when including those interest rate expenses. They deleveraged a bit in the last year by redeeming about $20 million of their preferred shares.

As of September 30, 2022, the Fund has outstanding 1,600 Variable Rate MuniFund Term Preferred Shares Series 2021 (“series 2021 VMTP Shares” or “VMTP Shares”). The Fund issued 1,600 VMTP Shares on February 16, 2018 and 200 VMTP Shares on February 16, 2021, and redeemed 200 VMTP Shares on September 29, 2022.

They then reduced it by another $20 million after the reporting period on November 22nd, 2022. At this point, they still have $140 million in Variable Rate MuniFund Term Preferred Shares outstanding.

Performance - Interest Rate Hit But Looks Better Now

In the last year, MAV indicated that investments in the high-yield portion of their portfolio lagged behind their investment-grade counterparts. They called out specific areas that performed poorly in their last semi-annual report .

High-yield municipals lagged their investment-grade counterparts during the period, due in part to negative performance from credit-sensitive sectors, including housing bonds, pollution control revenue ((PCR)) bonds, industrial development revenue ((IDR)) bonds, hospital bonds, tobacco master settlement agreement ((MSA)) bonds, and bonds issued by the Commonwealth of Puerto Rico.

Along with credit risks in these types of names, the primary hit for the fund overall was interest rates. Muni bond funds carry some of the highest maturities, and that translates into high durations on their portfolio. The effective duration for MAV was last shown at 8.35 years at the end of 2022. That means that, in theory, for every 1% increase in interest rates, the underlying portfolio should fall 8.35%. With the Fed rapidly increasing interest rates through 2022, this fund and most other muni funds saw a swift collapse.

However, as yields have started to ease back substantially - despite the Fed still increasing interest rates - we've seen that MAV has been able to come off the lows significantly.

Ycharts

For some comparisons in the last year, we can also take a look at some non-leveraged ETFs to see how they've done. That can provide some context to see if MAV was providing returns as expected.

I've included iShares National Muni Bond ETF ( MUB ). This is a high-quality, passive muni bond fund. However, they carry a portfolio with lower maturity and durations. I've also included the BlackRock High Yield Muni Income Bond ETF ( HYMU ). This is an actively managed ETF that includes a lot of similarities with MAV in where they can invest, except it doesn't employ leverage.

We can see that MAV and HYMU appeared to correlate more closely than MUB. This is expected since their portfolios are similarly invested in some below-investment-grade muni debt. Additionally, MAV had underperformed significantly through some of the lowest periods. That's also expected due to the leverage they employ. When it was rebounding, we can see that they were able to close the gap too.

Ycharts

HYMU was only incepted in 2021. So we don't have a long-term history that we can look back on. However, we can look over the last ten years between MAV and MUB.

MAV has outperformed on a total NAV return basis despite the significant hit it took this year. With interest rates stabilizing now, going forward, MAV should once again be able to outperform.

Ycharts

Again worth reiterating that these aren't similar muni funds, despite both being muni funds. This is to highlight their differences and how it worked for MAV during good times but also against the fund during bad times.

One thing that stands out above is how much the total share price of MAV had underperformed. This is because it might seem surprising, but this fund traded at quite a lofty premium ten years ago.

Now that the fund is trading at a deep discount, that's an even better chance that MAV could outperform going forward.

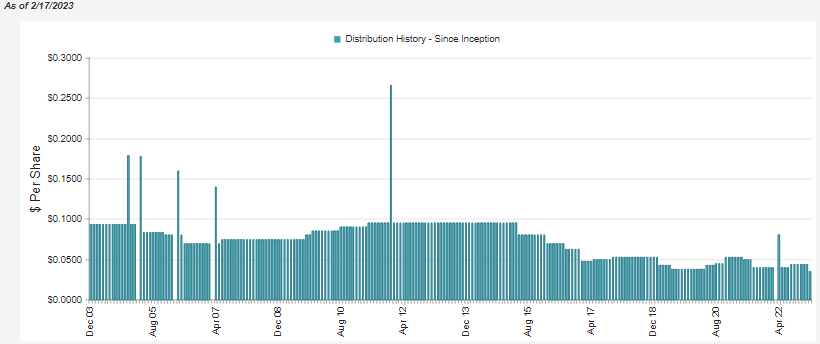

Distribution - Lacking Coverage Led To A Cut

While performance is important, most investors holding onto MAV are probably looking at the income it can produce or the distribution. Many muni funds cut their distributions in 2022 due to the rising leverage costs. MAV actually increased its distribution last year.

{kind=link}

However, since then, they cut their distribution by 21.6% to $0.0345 per month. This is more in line with what we've seen from other muni funds, which now have a lower payout than a year ago.

The latest distribution yield of 5.12% is fairly attractive, especially when one calculates their taxable equivalent yield, as that'll juice it further. The fund's NAV distribution rate is 4.48%.

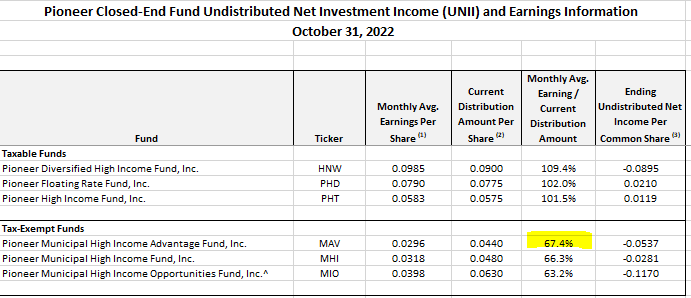

In looking back at the coverage, it seems quite clear why a distribution cut was necessary. The latest report showed that MAV's distribution coverage for the last three months was 67.4%.

{kind=link}

So it didn't appear that they could avoid the same fate as other funds seeing their net investment income decline. Yet, they chose to raise their distribution anyway, perhaps in an attempt to reduce the fund's discount. Since yields were rising, it could also be that they wanted to remain competitive with other risk-free yields.

Q Did the Fund’s distributions** to shareholders change during the six-month period ended August 31, 2022?

A Yes, in a rising interest-rate environment, the Fund’s monthly distribution rate rose from $0.04000 cents per share/per month at the beginning of the period, to $0.04400 cents per share/per month as of September 30, 2022, with the increase occurring in August. Please note that the Fund has drawn on accumulated net investment income in paying the Fund's distributions in recent periods, and these reserves may be depleted over time.

That isn't necessarily bad. However, one needs to be aware they weren't covering their distribution from income generated in the underlying portfolio with the types of coverage we see. Over time that could have eroded the fund's capital and made it harder to generate income on a reduced capital base. With cutting, this will be less of a concern.

The three-month report can be less reliable due to being shorter time frame. However, a lack of coverage seems to be fairly consistent with this fund. Net investment income coverage in the last semi-annual report was nearly 87%.

MAV Semi-Annual Report (Pioneer)

Year-over-year, the fund's interest expense went from $785k to $1,820,325 million. The actual total investment income stayed relatively flat, from $8,617,610 to $8,546,397.

Therefore, the largest hit to the fund's NII coverage came directly from higher interest rate costs. That confirms that despite the three-month UNII report above being for a fairly short period, that coverage would have declined regardless. With reduced leverage from redeeming their preferred shares, we know that income generation can take another hit from that.

Again this reflects why the cut was necessary. Going forward, at an annualized $0.414 distribution against 23,914,439 shares outstanding, it would come to an annual payout of $9,900,578. Given the last report showing $5,158,529 for six months, the NII coverage would work out to 104%.

That being said, we know that by reducing leverage since the report and that their preferred leverage costs are still rising a bit, the NII going forward should be lower. After the distribution cut, it will still give us much better coverage numbers than what we saw in their latest UNII report.

All that being said, for tax purposes, they are providing exactly what their goal is. That would be tax-exempt income distributions to shareholders.

The tax character of current year distributions payable will be determined at the end of the current taxable year. The tax character of distributions paid during the year ended March 31, 2022 was as follows:

MAV Distribution Tax Classification (Pioneer)

The bulk of the was being characterized as tax-exempt income. A fairly small portion was considered to be ordinary income. As a muni fund that is invested in many different states, some of the distributions could qualify for tax-free status from the state you reside too.

MAV's Portfolio

Above, we noted that the fund's effective duration of 8.35 years is high, but that is quite normal for muni funds. This is due to the high maturities that municipalities can generally get away with. The higher the quality of the offering, generally, the longer the maturity will be granted.

MAV Portfolio Stats (Pioneer)

Looking at the maturity breakdown more closely, the largest allocation is to the 20+ bucket. This reflects why the average life of the underlying portfolio is over 20 years, as listed above.

MAV Maturity Breakdown (Pioneer)

In total, the portfolio carries 143 positions. For a bond fund, that is a fairly low number of holdings. The largest sectors to make up this fund are listed as hospitals and then tobacco.

MAV Top Sector Allocations (Pioneer)

A bit of a paradox of exposure at first glance. However, this is through tobacco settlement financing , where the bonds are backed by tobacco revenue from lawsuits.

Looking at the quality distribution, we can see that the fund isn't invested all in below-investment-grade munis or those not rated. There is still a fairly significant allocation to higher-rated debt.

In total, 38.91% of the portfolio would be considered to be invested in investment-grade bonds. Then they have 27.86% in below-investment-grade or junk-rated debt. That leaves us with the remainder in the not rated category.

MAV Credit Quality (Pioneer)

The top ten in the portfolio shows the top two positions at a fairly large weight. As mentioned above, 143 holdings aren't that many for a bond fund. That is no matter what category of fixed-income bond fund either. They generally have several hundred, into the thousands, of holdings spread across a diverse basket of positions. Each holding sometimes represents less than 1% of any weighting, even the largest holding.

In below investment grade type of holdings, one would generally find some comfort in the broad diversification of hundreds of holdings. Therefore, MAV could be considered a relatively concentrated muni bond fund and even somewhat riskier.

MAV Top Ten Holdings (Pioneer)

Conclusion

Seeing the fund increase its payout last year seems counterintuitive when we saw most other muni funds cut their distributions. However, that lack of distribution coverage was rectified more recently with a big distribution cut to make it more in line with peers.

Additionally, the fund carries some high-yield or below-investment-grade exposure in a relatively narrowly focused portfolio compared to peers.

All that being said, MAV is trading at a tempting discount, and interest rates should stabilize. At the very least, the rapid pace of increase is coming to a halt with the latest 25 basis point increase. We've already seen the violent snapback from the lows as the 10 Year Treasury Yield started to recede. Subsequently, now we see the decline again as yields rise once again based on getting strong economic data and the PPI hotter than expected.

That should continue to bode well for municipal CEFs such as MAV. Their leverage costs should quit rising, and their underlying portfolio should quit dropping. The fund also has been offering a distribution largely classified as tax-exempt for federal tax purposes, which is exactly their goal.

For further details see:

MAV: Municipal Bonds At A Deep Discount