MXCT - MaxCyte May Benefit From Potential Gene Therapy Approval

2023-11-27 08:00:00 ET

Summary

- MaxCyte is a pick-and-shovel play on cell editing technology, but may capture a royalty stream from successful products.

- Vertex's potential candidate approval in the U.S. could prove a decisive catalyst ultimately validating MaxCyte's approach and business model.

- If MaxCyte's partners see commercial success, MaxCyte could be valued at multiples of its current price on potential royalties.

- However, there is almost total downside risk too, should the technology fail.

MaxCyte ( MXCT ) is an attractive 'picks and shovels' play on cell and gene editing innovation. This is because they are considered to have industry-leading technology that is broadly used, and their contracts enable "low single digits" royalty payments in the event of commercial launches at partner pharmaceutical firms.

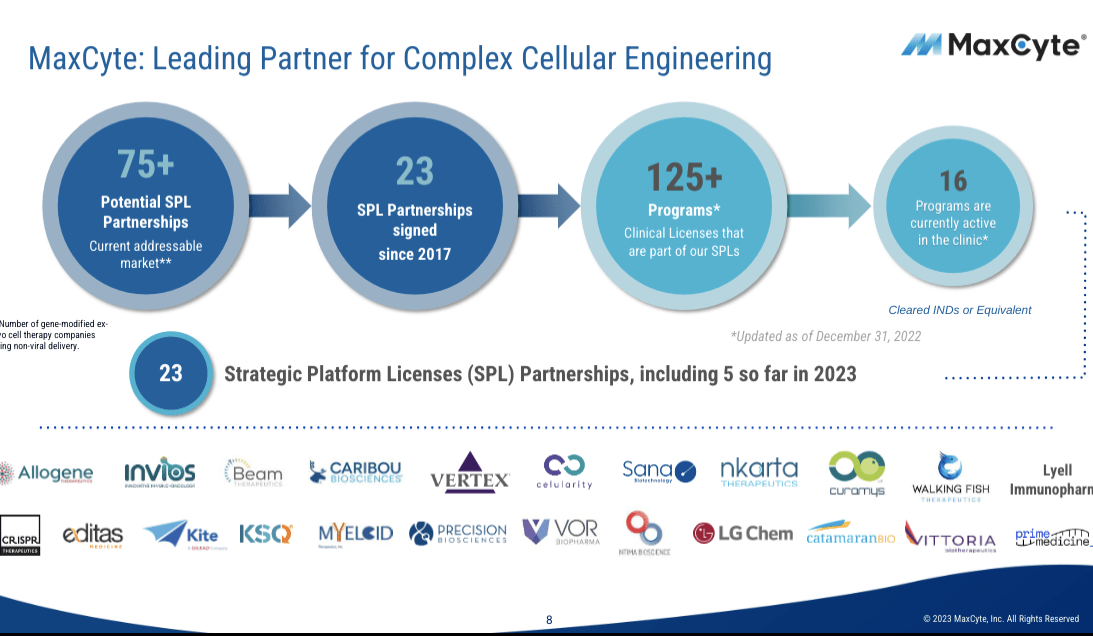

These royalty-share agreements or as the company terms it a Strategic Platform License (SPL) apply to 23 companies currently.

Vertex (VRTX), which is a MaxCyte partner, just had its first gene-editing therapy approved (via conditional marketing approval) in the UK. Assuming U.S. approval follows that could be lucrative for MaxCyte and help to validate their business model.

Potential FDA Approval On December 8

The potential approval may come on December 8 (the Prescription Drug User Fee Act action date ) for Vertex's gene therapy offering (Exa-Cel) for sickle cell disease. This may then be followed by a potential approval for a second gene therapy for Vertex on March 30 2024 addressing beta thalassemia.

The FDA may broadly agree on the benefits of these therapies, but the main questions might surround potential long-term side effects. These may require further study. Vertex has proposed an ongoing 15-year study to monitor for any potential side effects. Of course, given that gene therapies are a relatively new innovation, longer-term impacts are harder to gauge than for treatments with a longer track record. However, the FDA has already approved a number of therapies that involve gene editing, such as many CAR T therapies for cancer and a gene editing therapy for beta thalassemia already, so this is not quite the watershed moment it might appear.

Partnership Value

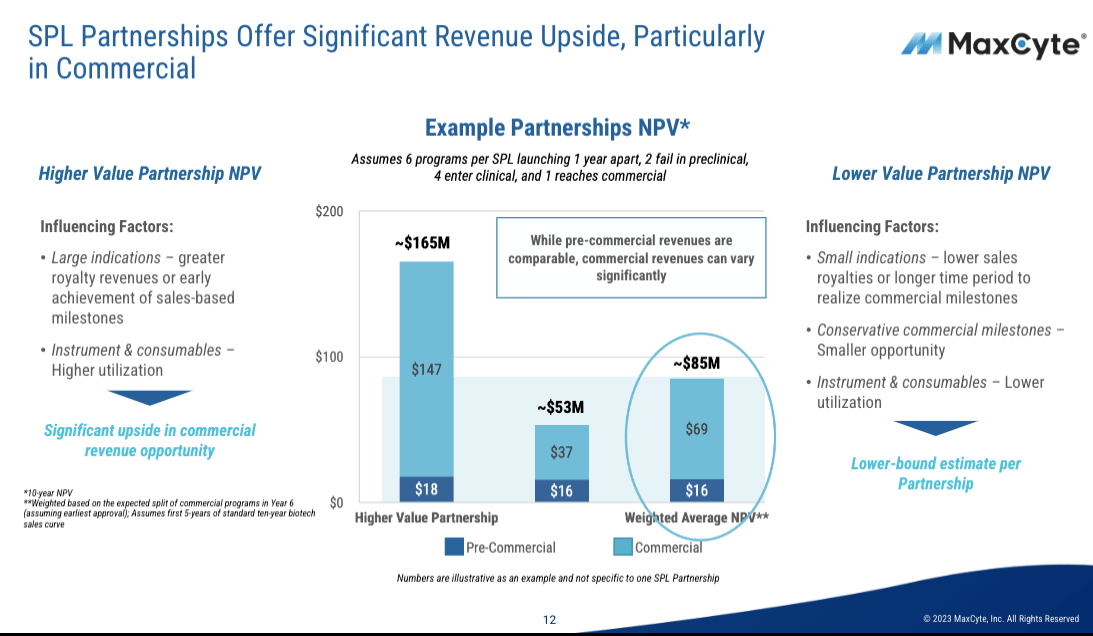

The key to the investment case is the value of the range of valuable partnerships that MaxCyte has. This is slide 12 of MaxCyte's investor deck, where they quantify the expected value of a typical partnership at $85M on a net present value basis.

NPV of Partnership (MaxCyte Investor Presentation)

{kind=link}

Next, note that they have 23 of these partnerships and that includes Vertex Pharmaceuticals and CRISPR (the companies that, working in partnership, recently received U.K. approval and have an upcoming FDA decision on December 8). Their partners also include many other leading gene therapy companies.

MaxCyte Partnerships (MaxCyte Investor Presentation)

{kind=link}

Of course, we need to test management's assumptions, but simplistically 23 partnerships with an NPV of $85M for each is just under $2 billion of value. That compares to a market cap of approximately $450M today, and a lower enterprise value of $270M due to MaxCyte's cash position without any material debt (note: $16M of operating leases as of Dec 2022), though the company is currently burning approximately $20M-$40M of cash depending on whether you're looking at past year's results or 2023's run rate which is trending higher.

SPL Terms

Regarding the SPL license terms, obviously, these can vary on a partnership by partnership, basis, but we have the following nuggets (from the company's investor deck - slide 10):

- "Multiple 7-figure milestones" related to approval

- "Low single-digit percentage of sales" during the commercial phase.

SPL Valuation

| Component |

| Value |

| Probability of event |

| Pre-clinical milestones |

| $10M |

| 100% |

| Approval milestone |

| $6M |

| 10% |

| Commercial royalties |

| $30M |

| 10% |

Key Assumptions of the above analysis:

- Per-clinical milestones can be inferred from historical data. In 2022, they earned $2M per program ($40M/18 programs), I assume that persists over 5 years per program for a value of $10M per SPL.

- Approval milestones are based on management's statement of multiple 7-figure milestones per approval. I assume 3 x $2M payments.

- Commercial royalties assume a therapy launches at $100M and then grows 20% a year to hit $300M in years 7-10. That's discounted back at 10% a year, and I assume they earn a 2.5% royalty on those sales.

Lastly, note they estimate an average of 6 candidates per SPL. So we get the following, assuming that the chance of a therapy candidate successfully launching is around 10% from the start to end of the regulatory process, according to industry approval base rates, for example, see here for a Congressional Budget Office study .

| Component |

| Probability |

| Number of events |

| Event value |

| Expected value |

| Pre-clinical milestones (per program) |

| 100% |

| 1 |

| $10M |

| $10M |

| Approval milestone (per candidate) |

| 10% |

| 6 |

| $6M |

| $3.6M |

| Commercial royalties (per candidate) |

| 10% |

| 6 |

| $30M |

| $18M |

| Expected value per SPL (sum of above values) |

| $31.6M |

Obviously, the above numbers are very broad estimates, but per the slide above. Management gives an SPL value with ranges of $53M to $165M and an average value of $85M. My estimate of just over $30M is not too divergent from that considering how many assumptions are involved.

If we again recall that they have 23 of these partnerships, then at $30M per partnership, then the value is $690M, still well in excess of the current market capitalization. Also, if Vertex does ultimately receive U.S. approval, as seems reasonably likely given the U.K.'s approval, then that may increase the expected value of the portfolio overall.

Private Market Valuation Is Encouraging

In 2021, Vertex acquired an additional 10% stake in CRISPRs two initial gene therapy candidates at a cost of $900M-$1,100M. Now, we don't know what MaxCyte's royalty share is precisely, but if it's 2.5% then that's 1/4 of the 10% value that Vertex acquired, suggesting a private market valuation of $225M-$275M.

Now, it's highly likely that the Vertex SPL may be among the more valuable SPLs today as it could be within weeks of approval for a potentially very valuable market, and other SPLs may not reach the commercial stage, but Vertex's value may be in excess of what MaxCyte estimate for even what they call a "higher yielding partnership". It's also possible, of course, that Vertex overpaid for the 10% stake. Nonetheless, with a market cap today of around $400M, just the value of the Vertex SPL alone may account for half of MaxCyte's value when they have 22 other partnerships, though of course, all are further away from commercialization.

Another way to think about potential SPL value is that CRISPR (Vertex's partner) has a market capitalization of $5.6B today. Of course, that value doesn't rest on two therapies alone, since CRISPR has a broad range of clinical programs , but their 40% stake in those therapies might account for at least 50% of the firm's value today. Hence if $2.7B is the value of 40% of these therapies, then a ~2.5% stake is perhaps worth around $170M. It's unlikely all of MaxCyte's SPLs would be this valuable, but it does not seem a stretch to say an average SPL is worth tens of millions.

Lastly, we can potentially size the SPL in a bottom-up manner. If there are 30,000 patients eligible for Vertex/CRISPR's sickle cell disease treatment at a cost of $1 million per treatment, that would suggest an addressable market of $30 billion, 2.5% of which is $750M. Of course, a major issue will be who can afford a $1 million treatment which would bring down revenues compared to the addressable market considerably. However, similarly very valuable gene therapies have been priced in the $0.5M-$3.5M range in the U.S ..

Five SPLs Added in 2023

We should also consider that MaxCyte has added around 3-4 SPLs per year over recent years, if that trend continues, then those additional SPLs would be adding potentially $100M-$350M of value per year. Though, of course, at some point, they will have saturated the market and run out of major additional firms to partner with, or have to move onto the second-tier players with less potential. Management estimated that the addressable market for gene and cell editing-related SPLs is around 75 firms.

They have been marking progress in 2023. As recently as August 2023, MaxCyte added an SPL with Prime Medicine . The pace of new SPLs does not appear to be slowing down. Vittoria also signed an SPL in July 2023 as did Lyell and Walking Fish signed in May and Catamaran Bio in January . This pace of SPL additions is a positive if they are the SPLs are as valuable as management estimates. The pace of additions in 2023, also implies that there may be further SPLs to come.

Valuation

We can therefore think of MaxCyte as a portfolio of these SPLs with more optimistic and pessimistic parameters for each, I assume 104M shares outstanding and that they burn through their current cash pile, but incur no debt, the value then is simply the value of each SPL multiplied by the number of SPLs divided by the 104M share count:

| Number of SPLs at steady state |

| Low SPL Value ($30M) |

| Management Base SPL Value ($85M) |

| Management High SPL Value ($165M) |

| 23 |

| $7 |

| $19 |

| $37 |

| 30 (7 more SPLs added) |

| $9 |

| $25 |

| $48 |

| 40 (17 more SPLs added) |

| $12 |

| $33 |

| $64 |

| 50 (penetration of 2/3 of management's estimated addressable SPL market) |

| $14 |

| $41 |

| $79 |

It therefore seems that MaxCyte may be inexpensive today at a $4.5 share price. It is somewhat strange to see all the scenarios above point to the upside, but it appears a reasonable assumption that they will add more SPLs over time, given they added 5 in 2023 so far, and valuing SPLs at $30M-$165M appears to triangulate with various valuation approaches, albeit, we'll know more once commercial success is achieved.

Risks

- Virtually all the value of MaxCyte comes from management disclosures currently, especially with regard to potential commercial royalties. These cannot be rigorously independently tested, though the transaction between Vertex and CRISPR in 2021 gives one data point. My attempt to recreate the estimates relies itself on high-level management disclosures regarding the contracts in question and is itself speculative requiring long-term estimates of potential revenue streams. Therefore, if any statement proves to be incorrect (due to the future differing from the model's assumptions), the valuation could be similarly misstated.

- MaxCyte's SPL programs are not truly independent. A lot rides on the overall success of cell therapy, gene therapy, and related technologies. If something pivot to the technology fails, then all of MaxCyte's SPLs may be virtually worthless. That said, MaxCyte is well diversified across a range of therapies and implementation methods, but the key reliance on cell and gene editing can't be diversified away.

- MaxCyte is a long-duration asset, even in the best case, most royalty payments would be 5+ years out and later, in most cases given the significant timelines for therapy development, FDA approval, and commercial launch.

- MaxCyte is currently well-regarded and viewed as an industry-leading firm, if that changes, the stock will perform poorly. It also relies on suppliers for key pieces of its offering, and it may be able to capture more value over time at the expense of MaxCyte.

Conclusion

MaxCyte is an interesting, if speculative idea, that may attract further interest depending on the trajectory of Vertex and CRISPR's gene-editing therapies, which could help validate or disprove the promise of the technology. I am also encouraged that management and the board, own a relatively material holding of shares at around 6%.

If Vertex performs well, then MaxCyte may be reappraised by the market as holding the keys to a technology that shows a lot of promise, and MaxCyte would essentially collect a small royalty on a meaningful portion of the sector's sales, albeit on a medium-term view.

There is certainly downside risk, if something goes wrong with the overall technology, or the SPL model fails contractually or in some other way, then MaxCyte may be essentially worthless. This scenario appears possible, but unlikely.

However, if things trend well then MaxCyte, could eventually be worth multiples of its current value as the number of partnerships increases with each worth tens of millions, and perhaps hundreds of millions in the best cases.

Vertex's potential therapy approval for sickle cell disease and subsequent sales (on which MaxCyte would likely receive a royalty) may create a tailwind for MaxCyte going forward in validating the overall SPL model and hence increasing the valuation of the company.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

MaxCyte May Benefit From Potential Gene Therapy Approval