MAXN - Maxeon: Strong Technology But Challenging Financials

2023-11-03 08:34:29 ET

Summary

- Maxeon Solar Technologies has leading solar technology but faces near-term headwinds that warrant caution.

- The company operates on thin margins and a heavy debt burden, making profitability elusive.

- Recent slowdown in financial results and disputes with major customer SunPower add to the uncertainty.

Investment Thesis

While Maxeon Solar Technologies possesses industry-leading solar technology resulting from decades of R&D and patents, the company's debt profile and lack of profitability since its 2020 spin-off are concerning. Heavy debt load and negative cash flow heighten financial risks, especially amid recent demand slowdowns acknowledged by management.

While long-term growth prospects remain strong given global energy transition tailwinds, caution seems prudent until Maxeon makes headway on cash flow, deleveraging, and stabilizing demand trends. Until then, MAXN appears fairly valued, even at its lower end of historical multiples. I rate MAXN a hold until financial sustainability improves, as these challenges currently outweigh its impressive technology and market opportunity.

Maxeon's Competitive Edge

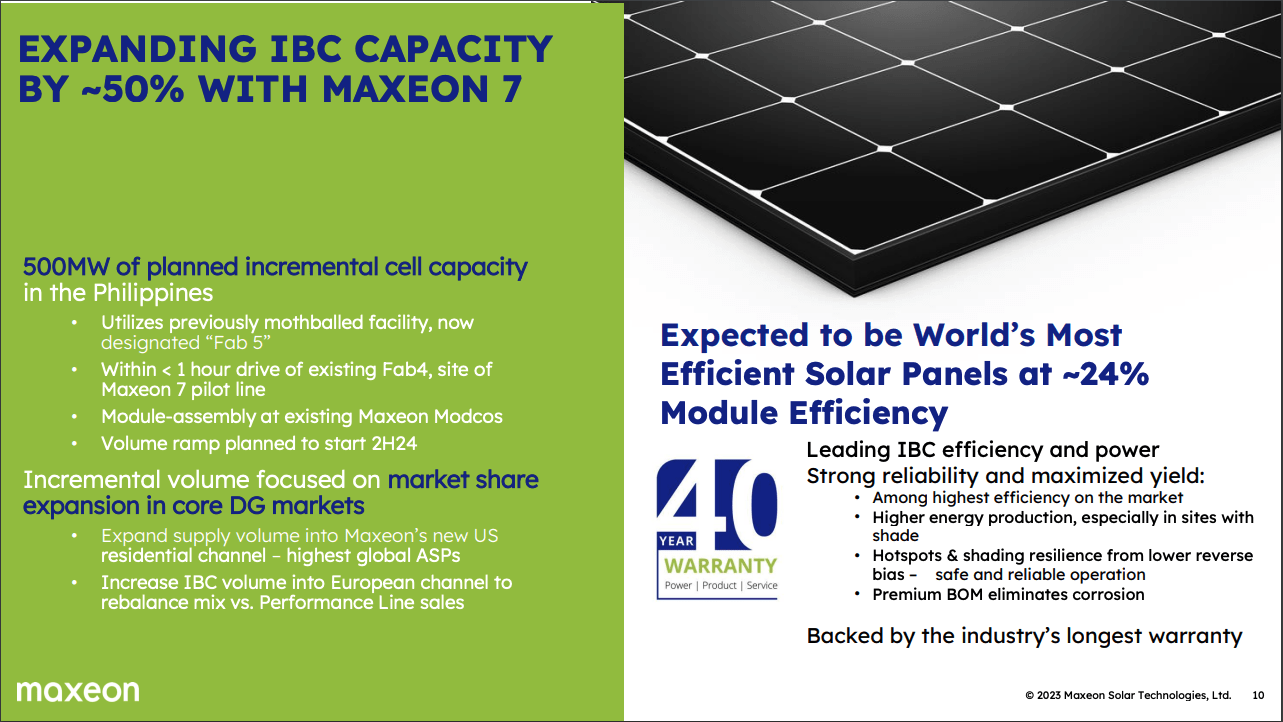

Maxeon Solar Technologies possesses a competitive edge stemming from its proprietary interdigitated back contact (IBC) cell technology, used in its premium SunPower line of solar panels.

IBC technology enables high module efficiency of up to 24% and lower degradation rates of just 0.2% per year, compared to the industry average of 0.5-0.7% annually. This results in Maxeon's panels producing 20% more energy over 25 years for a given rooftop area compared to conventional panels. Maxeon also offers a 40-year warranty on certain products, the longest in the industry.

{kind=link}

In addition to the Maxeon line, the company sells lower-cost Performance line panels utilizing more conventional shingled cell technology targeted at utility-scale projects. This diversified product portfolio provides exposure to both distributed generation (residential/commercial rooftops) and utility-scale markets. Maxeon's technology leadership has been built over 35+ years of R&D and patents.

Margins and Debt Profile Maxeon operates on thin gross margins under 20%, and has only recently posted positive GMs. The company has yet to produce positive net income since becoming a standalone company after being spun off from SunPower in 2020. In fiscal year 2022, Maxeon posted a net loss of $267 million. While gross margins have expanded from previous negative levels and there's positive adjusted EBITDA, consistent net profitability remains elusive.

Maxeon

The balance sheet is also heavily leveraged, with $200 million in convertible debt due in 2025 and new $275 million notes payable to TZE due in 2027. Unlevered cash flows are negative $54m over the trailing twelve months. This high debt load and negative cash flow heighten risks around Maxeon's unproven path to profitability if business slows.

Seeking Alpha

Recent Slowdown in Topline

Weaker demand has transpired in recent quarters, acknowledged by Maxeon management. On the Q2 2023 earnings call , CEO Mulligan stated “we experienced an unexpectedly rapid change in the market demand environment late in Q2” that impacted volumes and revenue. He cited softening in European residential demand and inventory buildup. CFO Kai Strohbecke noted lower sequential margin expectations for Q3 and beyond.

Maxeon is also apparently in a dispute with major customer SunPower , which it relies on for significant volume as a legacy relationship from when Maxeon was part of SunPower. The nature of the disputes is uncertain but presents an overhang until resolved given the dependence.

Potential Upside Catalysts

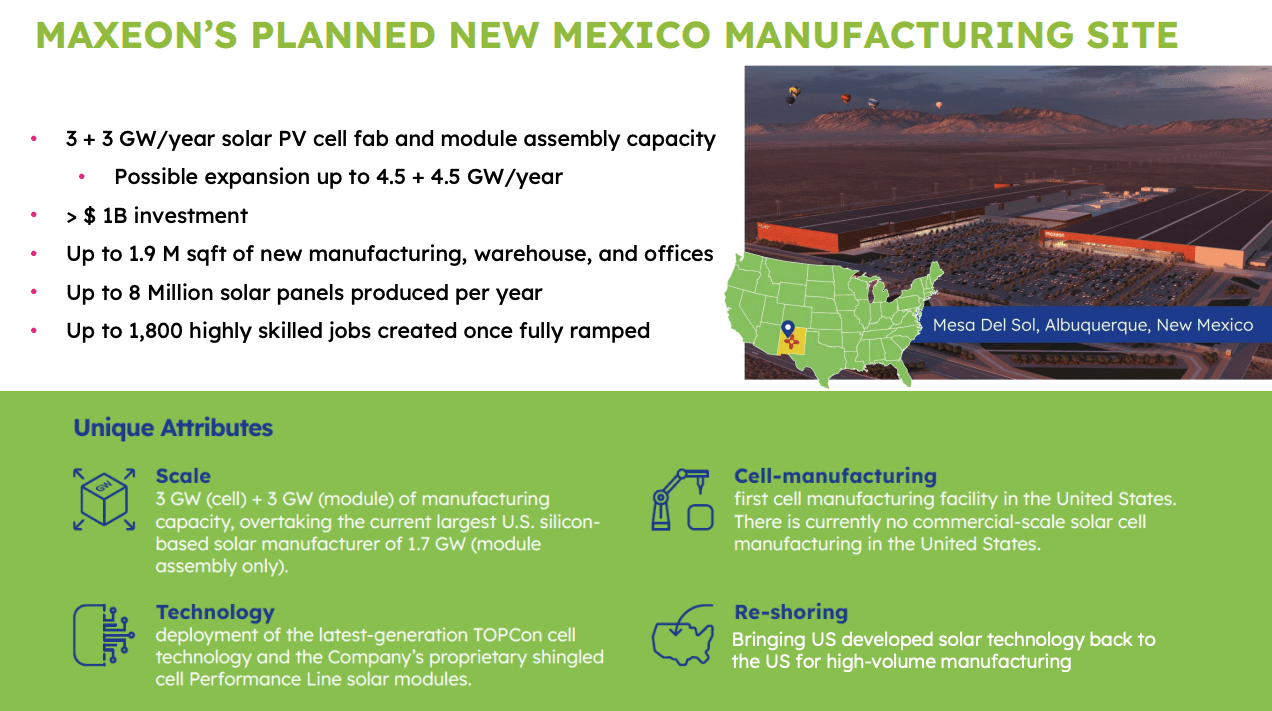

Despite current headwinds, Maxeon has potential upside catalysts that could smoothen things out over time. The company is making major investments to increase manufacturing capacity, including plans for a large U.S. factory targeting both utility-scale and distributed generation markets. This factory aims to capitalize on U.S. incentives and bring more production stateside.

{kind=link}

Additionally, Maxeon is preparing to ramp up production of its new Maxeon 7 panels, which feature upgraded IBC cell technology for even higher efficiency and lower costs. If these capacity expansions and new products scale successfully, they should drive revenue growth and margin expansion over the next several years.

Maxeon's long-term growth prospects also remain strong, as the company is well positioned to capitalize on booming global demand for solar energy. The global energy transition should provide tailwinds for premium solar technologies like Maxeon's.

Risk Profile

Maxeon faces substantial downside risks that could impede its path to profitable growth and result in further share price declines.

Prolonged slowdown in global distributed generation demand would negatively impact Maxeon's core residential market. The company has yet to reach sustainable profitability and positive operating cash flow since its spin-off, and failure to achieve these milestones presents significant risk.

Deterioration of the relationship with major customer SunPower, which Maxeon relies on for significant volume from a legacy tie, would also be detrimental. Execution missteps in the company's major factory capacity expansion plans could hamper growth.

Competitive pressures from low-cost Asian solar manufacturers may weigh on margins. Maxeon also faces financing uncertainty for its planned U.S. factory without firm approval for a Department of Energy loan.

Macroeconomic weakness leading to reduced solar demand would provide further headwinds. If one or more of these risks materialize in the near to medium term, it will likely impede Maxeon's path to profitable growth and result in further downside for the stock from current levels.

Attractive Valuation

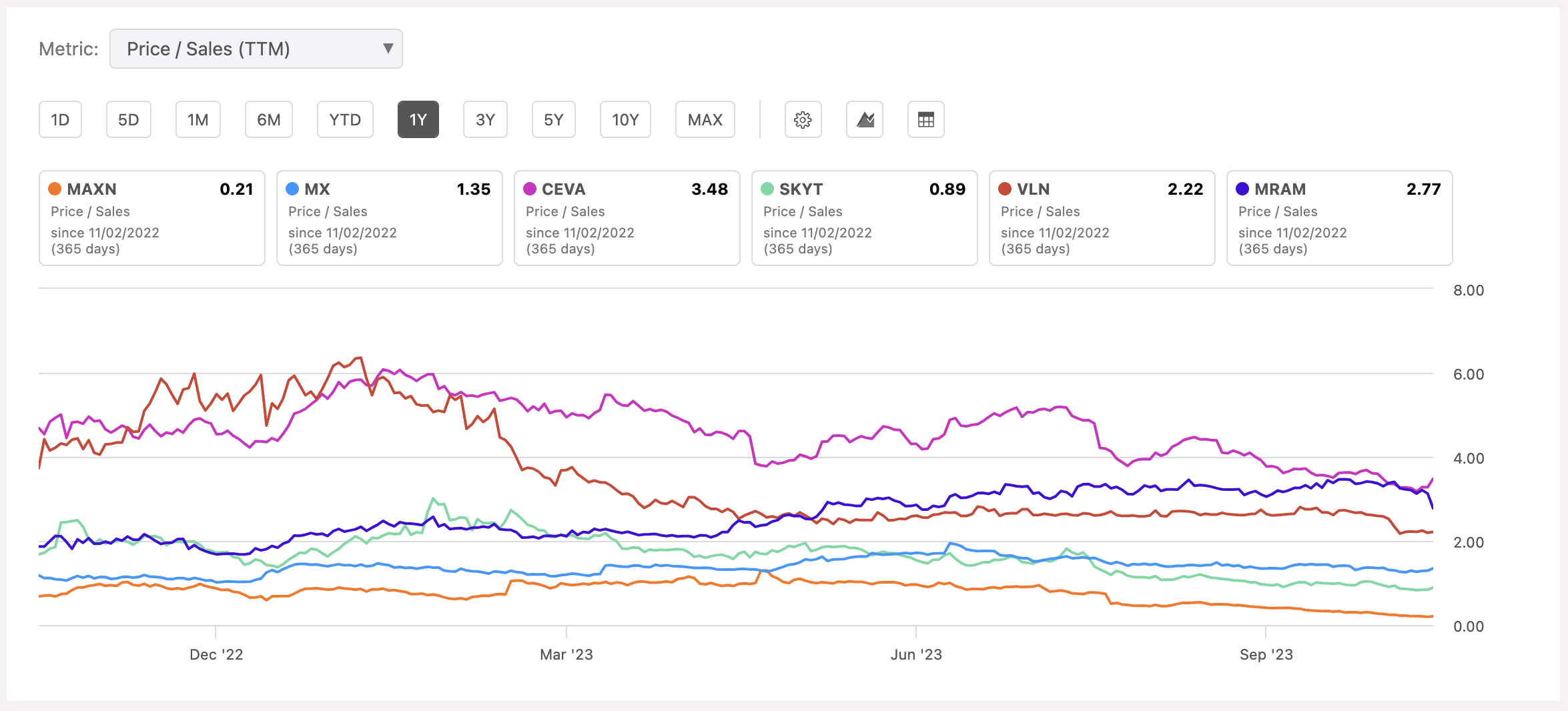

With the recent drawdown in the stock, MAXN is currently valued at a meager 0.21x Price/Sales on a trailing basis. This is way lower than the company's peers that trade over 1x. A lot of the bad news seems to have been priced in already, but catching a falling knife here doesn't seem the most prudent thing to do until margins expand and there's a clear path to sustainability. My view is that the stock seems fairly valued based on current financials. I would reconsider Maxeon for upside on signs of stabilization, resumed growth, execution on upcoming projects, and progress toward sustained profitability and positive cash flow. But more clarity is needed first.

{kind=link}

Conclusion

Maxeon Solar boasts impressive solar technology, but near-term headwinds outweigh its long-term potential currently. I rate MAXN a Hold due to uncertain profitability, high leverage, and demand slowdowns. While the long-term growth story is intact, caution seems prudent until headwinds stabilize. The stock appears fairly valued today, but clarity on financial sustainability is still needed to justify upside.

For further details see:

Maxeon: Strong Technology But Challenging Financials