EBGEF - May's 5 Dividend Growth Stocks With 6.08%+ Yields

2023-05-18 14:56:20 ET

Summary

- May started off on a bit of a sour note, with the broader indexes giving up some of their gains.

- Declining prices have helped push up dividend yields across the board as share prices fall.

- This month there was a heavy focus on energy names as five different names screened highly on the list; we touch on three of them today.

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on May 4th, 2023.

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines; they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all returned back into your pocket from that point forward.

Inflation has remained sticky, and that has pushed the Fed to hike rates aggressively. However, as banks have also been starting to fail now, we may have seen the last of the rate hikes for now. From here, it is widely expected that the Fed will pause. The Fed itself has indicated as much, but it hasn't indicated that there will be cuts anytime soon. That's something the market is starting to anticipate, though.

With inflation coming back down, they have some room to be able to pause here. However, inflation is still admittedly quite high and well above the Fed's 2% target.

YCharts

All of this being said, it's important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. These are September's five dividend growth stocks that might be worthwhile for a deeper exploration. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth, and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt, and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue, and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 538 stocks at this time from the 540 listed last month. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

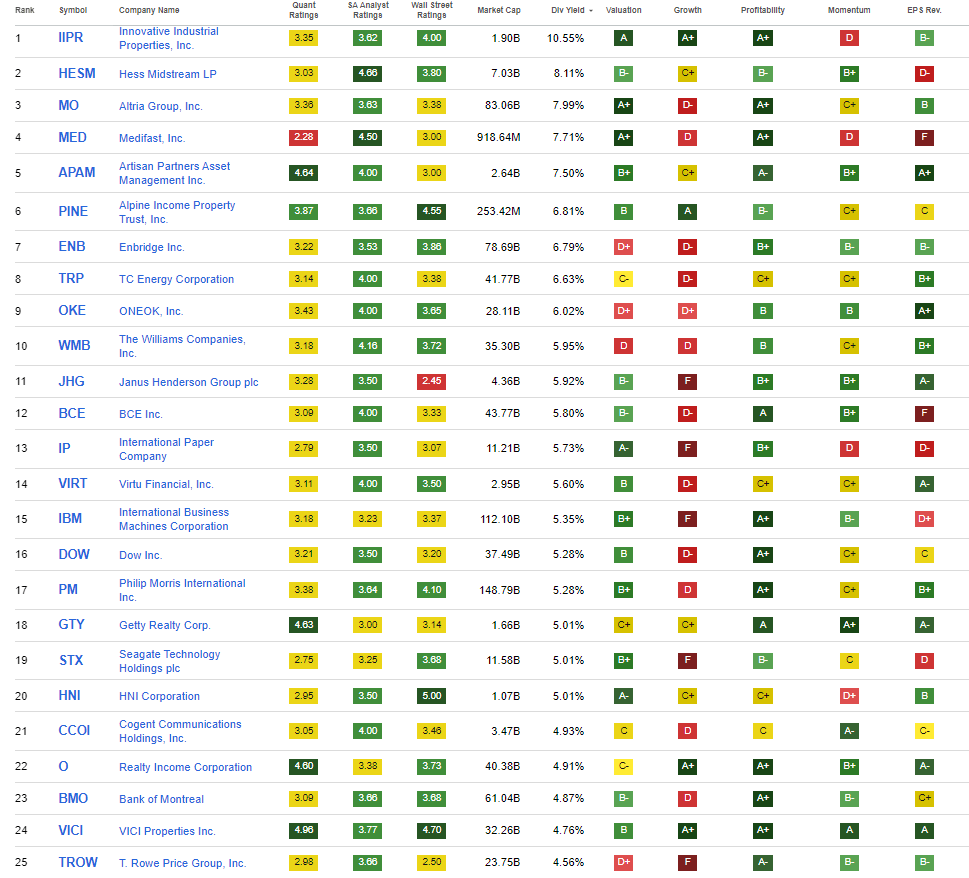

I will share the top 25 that showed up as of 05/04/2023.

{kind=link}

We recently discussed Innovative Industrial Properties ( IIPR ), Alpine Income Property Trust ( PINE ), Enbridge ( ENB ), and TC Energy Corporation ( TRP ). So we will wait another month or two before giving those an update.

That leaves us with Hess Midstream ( HESM ), Altria ( MO ), Medifast ( MED ), ONEOK ( OKE ), and The Williams Companies ( WMB ). Perhaps the most interesting thing to note right away is that this leaves us with three energy plays to touch on this month. Not only that, but ENB and TRC screened highly too.

Oil and natural gas prices have been under pressure, which is likely playing a role in this outcome. If share prices decline, the yields on these types of names will start to become more attractive. Dividend safety grades from Seeking Alpha's quants seem to be becoming better as well in this category. This was often an area where the screener would be generally negative and rate the safety quite low, even if they had tons of cash flow coming in to support the payout. There is a heavy emphasis on EPS metrics, which aren't necessarily the best metrics for midstream companies. Thus, why the companies often point out adjusted EBITDA and distributable cash flow more prominently as they are more appropriate.

Admittedly, the energy sector isn't my favorite, and I keep an overall low allocation to energy. In general, it's just too volatile of a sector for me. With that being said, these are also all names we've touched on before, so we can take an updated look at how they might be doing.

Hess Midstream 8.35% Yield

The last time we touched on HESM was in January 2023. They describe themselves as a "fee-based, growth-oriented midstream company that owns, operates, and develops a diverse set of midstream assets to provide services to Hess and third-party customers."

An important distinction is that HESM is a midstream C-Corp for tax purposes, which means a 1099 and no K-1. Some investors find the additional paperwork of a K-1 off-putting. Although, I think investors should make investment decisions on fundamentals and not because of a tax form. Still, that should open up HESM to a wider investor audience.

HESM might not have the longest history, but with their short history, they've been able to provide an attractive growing dividend. In fact, since 2017, they've been growing their dividend every single quarter. That includes the latest that was good for a 2.7% boost.

HESM Dividend History (Seeking Alpha)

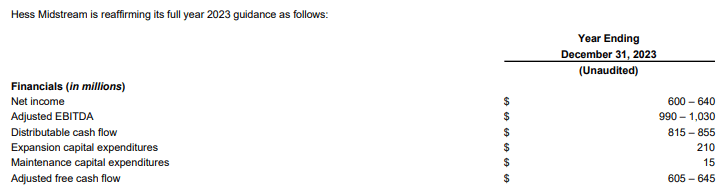

They posted their first-quarter results recently on April 26th, 2023. That showed adjusted EBITDA at $239 million and distributable cash flow at $196.6 million, and adjusted free cash flow was $142.2 million. Year-over-year, this was actually a decline on all three metrics.

However, their guidance for 2023, if achieved, would show at least some growth from 2022. Adjusted EBITDA for 2022 came in at $982.9 million with a distributable cash flow of $835.2 million.

{kind=link}

85% of their revenues are fixed-fee, which should give them good visibility into these metrics. However, energy is a volatile area of the market, and we've seen oil and natural gas prices both coming down. Shares of HESM are down around 4.36% on a YTD basis. So overall, they've still been holding up fairly well.

Altria Group 8.08% Yield

MO recently posted its results, and they mostly met EPS estimates, but revenue fell short. They had a small decline year-over-year in revenue, which isn't necessarily great given they are mostly expected to post flat revenue going forward by analysts. Where they earn some higher EPS growth estimates is from the pricing power they have.

However, the company is still dealing with declining cigarette sales, which isn't anything new. In a recent news post , it was noted that smoking rates in the U.S. have just reached their lowest level in around 60 years. So seeing the decline in cigarettes below isn't anything too shocking.

MO Cigarettes Sold in Latest Quarter (Altria)

They've been continuing to try to venture into other business categories, but that's been met with limited success. The latest is another attempt into the vaping segment of the market with NJOY Holdings . This was after their Juul investment went up in vapor.

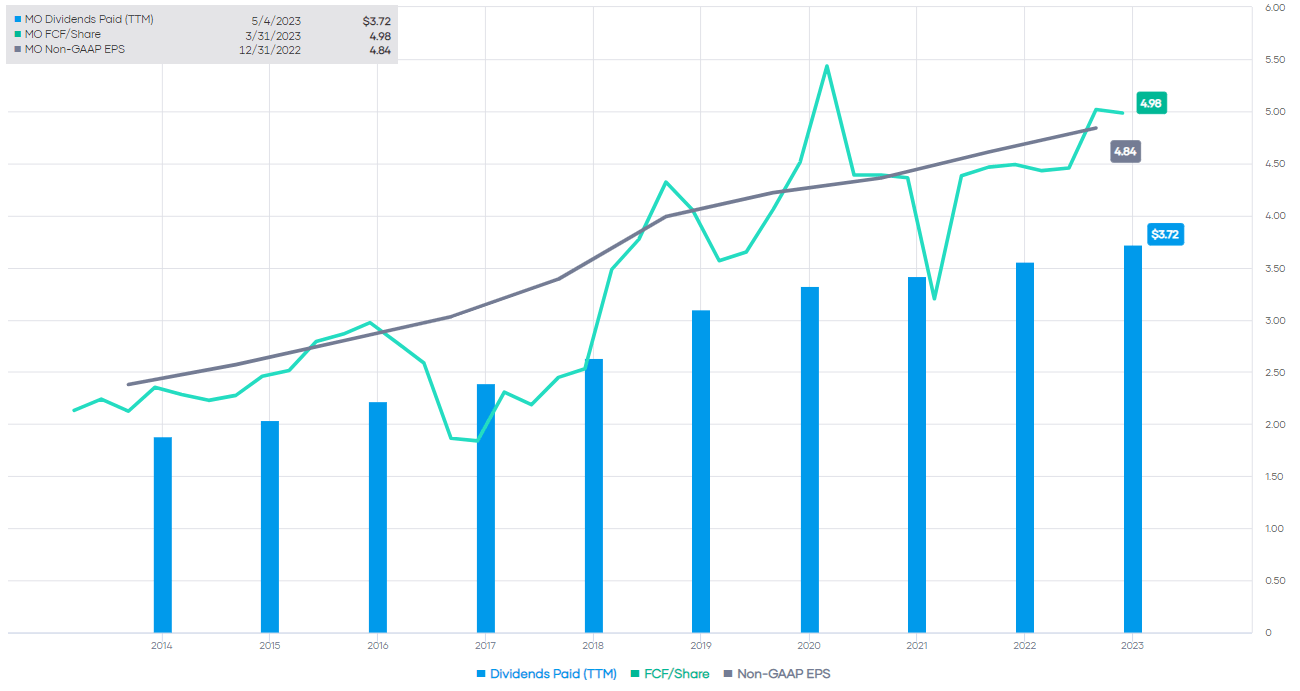

Still, the main draw to MO continues to be its growing dividend. Despite the headwinds to their business, they've been able to grow this dividend on the back of growing earnings and free cash flow. This trend of expected earnings growth going forward bodes well with this trend continuing.

{kind=link}

Medifast 7.75% Yield

MED is a bit of a unique company. It isn't a name that would often screen as a higher-yielding position. However, due to a rapidly declining share price with losses of nearly 55% in the last year, the yield has been pushed up.

This is a company in the consumer staples sector operating in the personal care products industry. Basically, the complete opposite of MO above. They describe themselves as "the global company behind one of the fastest-growing health and wellness communicative, OPTAVIA."

It may be hard to see visually, but with the latest dividend announcement, they did increase it pushing it up to $1.65 from $1.64. That worked out to just a 0.6% increase, and that means they've certainly cooled down the growth they had been showing.

MED Dividend History (Seeking Alpha)

If we look at the expected earnings from this company, though, one can see why the rapid dividend increase came to a halt. In fact, the way that earnings are expected to fall off a cliff, one might be more surprised they didn't freeze the dividend where it was. To be fair, they experienced perhaps what was an unwarranted amount of earnings growth in the prior years too. This is more of a normalizing after seeing what appeared to be a tailwind during the Covid pandemic come to an end.

MED Earnings History and Future Estimates (Portfolio Visualizer)

{kind=link}

Given the trajectory of their earnings, it would appear the dividend is covered. However, there is much less room here if we don't see them return back to earnings growth.

The Williams Companies 6.18% Yield

WMB last showed up on our screening piece back in July 2022. WMB " owns and operates energy infrastructure that safely and reliably delivers the natural gas that is used every day to affordably heat our homes, cook our food, and generate our electricity." This is another C-Corp, so investors can expect a 1099 and no K-1.

Their dividend history is quite volatile compared to other energy plays that one can find. However, they have been growing the dividend at a steady clip for several years now. That's why I believe that still makes them a fine fit for this article.

WMB Dividend History (Seeking Alpha)

With their latest earnings, they boasted a substantial increase in adjusted EBITDA, a large jump in adjusted EPS, and a sizable boost in Available Funds from operations. On an AFFO basis, dividend coverage went from 2.3x to 2.65x.

WMB Financial Results (Williams Companies)

These sorts of strong metrics are conducive to being able to grow the dividend even further in the future. Or, at the very least, the current coverage shows that even a substantial slowdown in their business should mean they have more than enough cushion before the dividend is threatened.

Even better, they highlighted that their balance sheet is strong with no significant near-term debt maturities. They carry an investment grade rating of BBB. That's allowed them a weighted average fixed rate for their debt of 4.81% with a weighted average maturity of 11.4 years. Despite these sorts of strengths, shares are down around 9.27% on a YTD basis.

ONEOK 6.08% Yield

Since the original publication to our members, OKE has announced they intend to acquire Magellan Midstream ( MMP ). That is likely to alter the forward projections heavily, and shares of OKE dropped meaningfully after the announcement.

OKE is another natural gas energy play, which we last took a look at in February 2023. They have a natural gas liquids segment or NGL, natural gas gathering and processing segment and natural gas pipelines segment. OKE is a C-Corp so that once again means no K-1.

Similar to HESM, they've been able to deliver a solid and growing distribution to investors. However, OKE has an even longer history, which some investors would likely find more appealing.

OKE Dividend History (Seeking Alpha)

At the same time, the yield is lower, and they aren't as aggressive in raising more recently. In fact, after the pandemic in 2020, they froze their dividend at the same $0.935 for an extended period of time. Only a couple of quarters ago did they start to raise the payout once again. At the same time, they've been able to grow their adjusted EBITDA at a fairly healthy clip.

OKE Adjusted EBITDA Growth (ONEOK)

If they can continue to keep up the momentum, investors could expect even more dividend growth in the future. In fact, they noted on their last earnings call that with a debt reduction, they now have more flexibility for dividend increases going forward, too.

Our priorities haven't changed at all. Our first priority is to find very high return projects that we can grow our business. Our debt reduction has kind of achieved the goals that we were looking for and that does create our flexibility for further dividend increases and potentially even stock buybacks over time. But that is our list of priorities, and as I said, high return growth projects that they're at the top of the list and that's a good segue into West Texas LP.

One thing we noted in our prior update was the fact that it seemed to be trading at a fairly cheap level. At least according to where it had been trading in the last decade on an EV/EBITDA basis, it's been trading below its average. Since our update, the valuation has actually declined further as the market price slipped.

YCharts

A good reminder that just because something is cheap doesn't mean it can't get cheaper. On the other hand, it still appears to be a fairly attractive time to consider entering into shares for a long-term investor. Despite the fixed-rate fee-based business of these sorts of energy companies, the declines we saw from OKE as well as HESM and WMB, still highlight their susceptibility to being volatile in terms of their share prices. At the same time, energy remains essential for a functioning society.

For further details see:

May's 5 Dividend Growth Stocks With 6.08%+ Yields