MEC - Mayville Engineering: Slowing Demand Expected In All 5 Primary End Markets

2023-12-23 10:12:22 ET

Summary

- Mayville Engineering's capital spending is expected to decrease, leading to improved free cash flow and potential for internal investments and acquisitions.

- The recent acquisition of MSA has contributed to sales growth, and the company's internal value-creating framework is driving organic growth and cost savings.

- Technical resistance and uncertainty in the commercial vehicle and construction segments may impact Mayville's stock performance and future earnings revisions.

Intro

We wrote about Mayville Engineering Company, Inc. ( MEC ) in September of this year when we reaffirmed our 'Hold' position in the stock. The company at the time was on the back of consecutive quarterly earnings misses, followed by a further bottom-line miss in Mayville's recently reported third-quarter numbers. Although Mayville's profitability remained under pressure (which we believed the technicals were pricing in at the time), shares have still managed to rally approximately 30% over the past 14+ weeks. The question now is whether a new bullish long-term trend has begun in Mayville or if those repeated earnings misses will adversely affect how the stock trades going forward.

Improvements Happening

What Mayville certainly has going for it is the fact that capital spending should continue to wind down due to the Hazel Park facility finally being completed. $3.5 million was used for capital expenditure purposes in Q3 this year as opposed to $12.5 million in the same period of 12 months prior. This means free cash flow came in at a much improved $16.1 million in Q3 this year as opposed to a mere $5.2 million in Q3 of fiscal 2022. Free cash flow is the most important metric in investing bar none and a key valuation driver. Furthermore, given as mentioned Mayville's constrained profitability (where margins remain tight), growing free cash flow means internal organic investments as well as acquisitions can be accelerated over time. The company's 2026 annual free-cash-flow target in this respect comes in at a much improved $70 million.

The recent MSA purchase for example gives an insight into how smart aligned acquisitions can contribute quickly to Mayville's financials. MSA (Mid-States Aluminum) aided in growing Q3 sales by over 16%. Furthermore, Mayville's internal value-creating framework (MBX) is tailored to drive organic growth as much as possible. What I like about MBX is the company's relentless pursuit of measuring and improving commercial excellence (Kaizen's continuous improvement model). On this point, the 100 MBX lean events that were realized by the end of Q3 are bound to result in significant cost savings for Mayville in the long run.

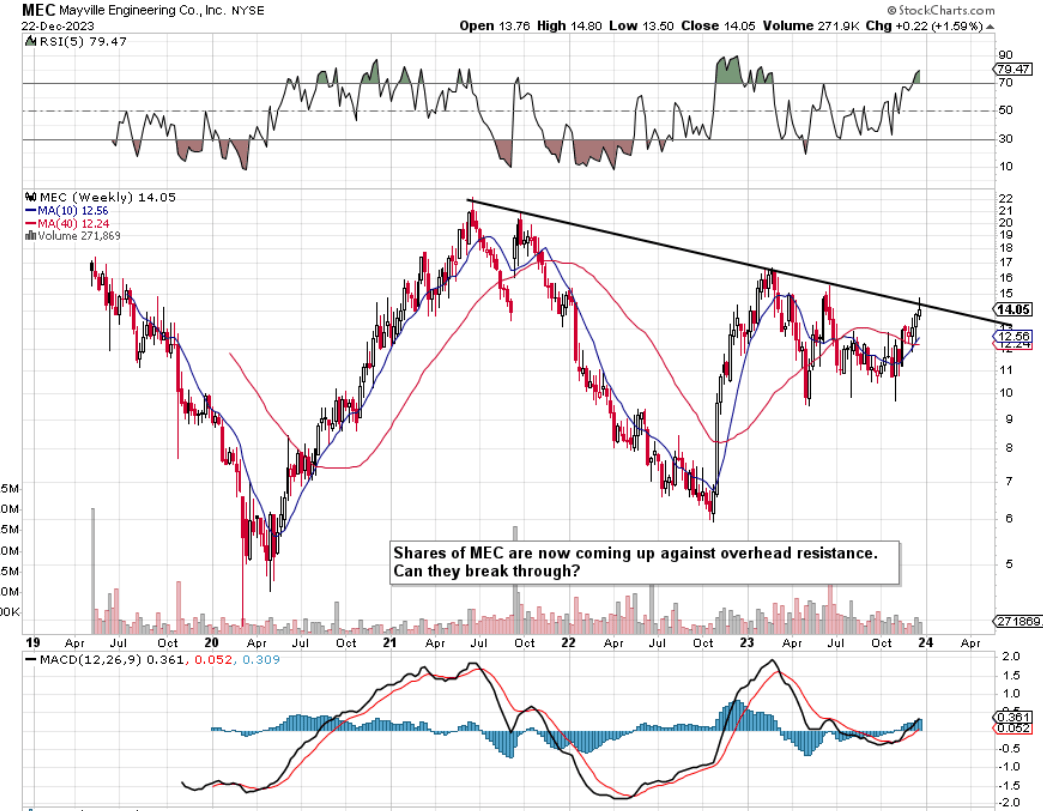

Technical Resistance

However, after delving through Mayville's technicals & forward-looking fundamentals, we have decided to stand pat on our 'Hold' rating for the time being. As we see below on Mayville's intermediate chart, shares are now coming up against overhead resistance which makes us believe that the current rally will come to a halt for now.

{kind=link}

Growth Uncertainty In Multiple Markets

On the fundamental side, although revenues of Mayville's commercial vehicle segment grew by over 6% in Q3, the CEO's comments below on the recent earnings call concerning forward-looking demand trend were revealing. Remember, this segment constitutes roughly 40% of Mayville's trailing 12-month sales. Therefore, sustained weakness in Mayville's commercial vehicle segment would certainly affect the share price if a prolonged slowdown was expected by the market.

Customer demand requirements continue to indicate slowing demand going into the end of the year and 2024, as the industry navigates regulatory changes as well as a general slowing in economic activity. Currently, ACT Research forecasts the Class 8 vehicle production to increase 6.6% year-over-year in 2023 to 336,000 units. The current projection indicates that build rates will slow during the fourth quarter and decline by nearly 4% on a year-over-year basis. For 2024, ACT projections reflect a deeper softening in demand through the middle of the year with current production estimates reflecting an 18.5% decline for the full year 2024. Furthermore, we are currently experiencing volume disruptions associated with the United Auto Workers strike with one of our customers. This has impacted our volumes for their products so far during the fourth quarter and will continue to do so until an agreement is reached

The 'Construction & Access' segment is just as open as the commercial vehicle segment to economic activity in that prevailing conditions will govern the level of demand. Although the market seems to be pricing in interest rate cuts in 2024, this does not necessarily mean that the residential housing market will see improved levels of construction. Interest rate cuts many times take place because of reduced economic activity. Furthermore, the risk here is that if the Fed adopts an accelerated dovish stance in 2024 (in response to an economic contraction), then inflation could easily remain inflated if not grow once more (which would not be good for this segment). Construction & Access makes up almost a fifth of Mayville's trailing sales so it also remains a crucial segment for the company.

Mayville's 'Power Sports' segment continues to grow from strength to strength but issues linger regarding dealer inventory levels. Agriculture & Military reported growing sales in Q3 but doubts (concerning forward-looking growth models) also remain.

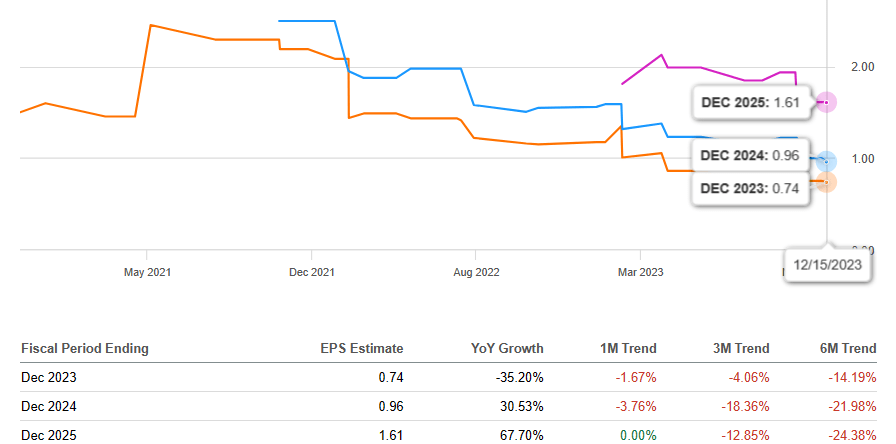

Therefore, when one ties everything together, it becomes understandable why forward-looking earnings revisions have deteriorated in recent times as we see below. The bottom-line estimate for fiscal 2024 has been revised down by almost 4% already over the past 30 days.

{kind=link}

Conclusion

Therefore, to sum up, although Mayville Engineering is expected to meaningfully grow over the next few years, forward-looking demand trends have resulted in decreasing EPS revisions in recent months. With free cash flow now beginning to come on stream for the company, it will be interesting to see how effectively management allocates capital going forward. Let's see what Q4 numbers bring. We look forward to continued coverage.

For further details see:

Mayville Engineering: Slowing Demand Expected In All 5 Primary End Markets