MZDAF - Mazda: Journey Into The Electric Vehicle Era

2023-09-27 12:36:59 ET

Summary

- Mazda's financial development has been modest, driven by design philosophy, quality innovation, and technology, but its lack of scale and brand value limits market share gains against the leading players.

- Mazda's shift toward EVs has been slow and now will likely rely on Toyota for support to accomplish this successfully.

- Mazda's share price has underperformed due to mild financial performance, but it currently offers value with a high FCF yield.

Investment thesis

Our current investment thesis is:

- Mazda's financial development in the last decade has been modest, driven by its KODO design philosophy, quality innovation, and Skyactiv technology. Its lack of scale and brand value relative to the major automotive players has restricted its ability to expand beyond its current level.

- Mazda's development toward an EV fleet has been slow, now relying on Toyota to support the company's aggressive catch-up phase in the coming 5 years. We are concerned by Mazda's lost ground but believe broadly that the partnership with Toyota should protect the company.

- Although we believe the coming 5 years will be tough, Mazda is currently operating with an FCF yield of 14% and a deep discount to its historical average and peer group, implying value.

Company description

Mazda Motor ( MZDAY ) Corporation is a Japanese automaker known for producing a range of vehicles, including cars and SUVs. The company emphasizes innovation and driving dynamics in its products.

Share price

Mazda's share price performance has been underwhelming, losing value since 2010. This is a reflection of its mild financial performance during this period, struggling in the face of high competition.

Financial analysis

{kind=link}

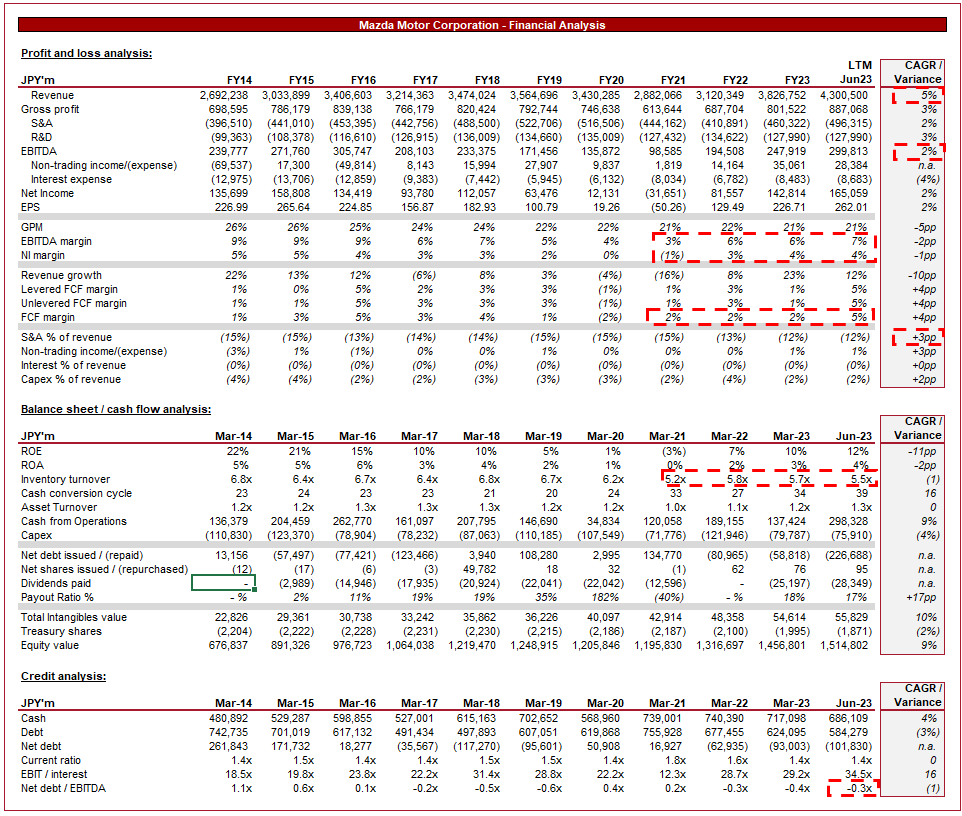

Presented above is Mazda's financial performance in the last decade.

Revenue & Commercial Factors

Mazda's revenue has grown at a modest 5% during the last 10 years, with broadly consistent growth, although noting 2 periods (excl. the pandemic) of negative growth.

Business Model

Mazda has a reputation for emphasizing design, engineering, and driving dynamics in its vehicles. The company strives to provide vehicles that offer an enjoyable driving experience and stand out in terms of aesthetics. The company operates in the affordable to mid-range segment, similar to many of its Japanese peers.

The company prides itself on its unique approach to engineering and design, referred to as KODO, which is described as the " depiction of potential energy in stationary forms " The inspiration for this was the stance of an animal waiting to pounce. This design approach has won several awards and is distinctive within the industry, allowing Mazda to differentiate itself. We believe this has been a key contributor to growth in the early part of the decade (in particular), allowing for brand development in Western nations as consumers seek Japanese manufacturing with a hint of fun.

Mazda has developed its proprietary Skyactiv Technology, which focuses on improving fuel efficiency, engine performance, and overall vehicle dynamics. This technology platform is aimed at enhancing the driving experience while also addressing environmental concerns. Reviews of Skyactiv have generally been positive, with good reliability and an enjoyable driving experience as key observations.

Both KODO and Skyactiv are supported by the wider "Zoom-Zoom" marketing, emphasizing driving pleasure, responsiveness, and a connection between the driver and the vehicle. We believe Mazda has done a fantastic job of gaining market share globally through effective marketing, underpinned by deep expertise.

Mazda's vehicle lineup includes a mix of sedans, SUVs, crossovers, and sporty models. This diversity allows the company to target different market segments and cater to varying consumer preferences. This is critical to generating economies of scale and brand development within this highly competitive industry.

Mazda operates in various global markets, including North America (36% of FY22 revenue), Europe (14%), Japan (15%), China (8%), and other markets. This global footprint has helped the brand develop, reaching a wide customer base and reducing concertation to specific markets.

Mazda has shown a willingness to work with other automakers to achieve joint improvements, similar to other partnerships agreed upon by competitors (Renault ( RNSDF )/Nissan ( NSANY )/Mitsubishi ( MMTOF ) being the most famous of which). Most recently, Mazda partnered with Toyota ( TM ), to collaborate on technology development, manufacturing efficiencies, and shared platforms to expand the former's footprint into the US. Toyota has taken a 5% stake in Mazda to cement this marriage.

Electric transition

The shift toward electric vehicles has been a gradual one for Mazda, with the business having been broadly focused on expanding its ICE-powered product range. Similar to its Japanese peers, the company has been less aggressive than the Europeans.

This said, Management has committed over $10bn to investment in EVs, with a number of models expected in the lead-up to 2030. The issue is that this is a technological race, not one of purely utilizing existing competencies. Consumers care about range, function, performance, etc., all of which rely on battery and powertrain technology. This means the business is likely to lean heavily on Toyota for further technology (which ironically has faced criticism for neglecting EV investment).

We do not think Mazda is in trouble yet but it is concerning that further progress has not been made.

Competitive Positioning

We believe Mazda's key competitive advantages are:

- Brand Perception. Mazda's unique approach to design and driving dynamics has allowed the business to perform well following its divorce from Ford.

- Market Trends. Consumer preferences have shifted toward SUVs and crossovers, impacting sales of traditional sedans. Mazda's ability to adapt to this has been extremely impressive, with a range of SUVs in varying sizes and price brackets. These are generally well-reviewed.

- Expertise and reach. Mazda has developed a strong brand globally, through innovation and operational efficiency.

- Toyota. Having one of the largest automakers in the world as a partner and shareholder is a major advantage for Mazda. The success of its innovation will be somewhat limited because of this, knowing Toyota is there to support it.

The automotive sector has reached a point of saturation, with slower growth in demand for new vehicles and a relatively fixed hierarchy of brands. Improvements and mistakes will only partially impact Mazda's position, so long as it is broadly moving in line with the industry as a whole.

Mazda faces competition from other affordable/mid-market automakers such as VW ( VWAGY ), GM ( GM ), Ford ( F ), Toyota ( TM ), Honda ( HMC ), Subaru ( FUJHF ), and Stellantis ( STLA ), among others.

Economic & External Consideration

Current macro conditions are posing challenges for the automotive sector (and the wider global economy as a whole), mainly due to high inflation and elevated interest rates, which are leading to decreased consumer spending, particularly on significant commitments. Consequently, the ability to finance a new purchase, or willingness to, is reduced.

In its most recent quarter, Mazda posted a +32% increase in volume relative to the prior year, driven in large part by North America and Europe. Further, this quarter is broadly in line with the prior quarter (302k v. 322k), implying robust demand. LTM revenue growth of +12% reflects the impact on Mazda's topline.

The industry's resilience in terms of demand is a consequence of the lingering impact of the pandemic. Following an extended period of supply constraints owing to the semiconductor industry, consumer demand continues to unwind as availability improves. Further, we believe this is evidence of the general economic resilience in major economies, as evidenced by the lack of a recession despite the economic indicators. Finally, positive pricing action has been taken following the supply issues.

Margins

Mazda operates with slim margins, with an EBITDA-M of 7% and a NIM of 4%. This is a reflection of the company's aggressive pricing strategy and size, reducing its ability to achieve substantial economies of scale in line with the majors.

Margins are ticking up in the LTM period but this will likely slow, restricting the company's ability to move beyond an EBITDA-M of 7-8%, as economic conditions weigh on demand. Inventory turnover is not clearly suggestive of a slowdown but remains below its pre-pandemic level, restricting cash flows partially.

Balance sheet & Cash Flows

Although Mazda has a mild FCF margin, the business is positioned well to allocate capital to investors. It is investing consistently in R&D/Capex at a reasonable level while having a net cash position. Even as spending increases as part of the EV transition, the lack of material debt servicing means healthy excess FCF will remain. Despite this, returns have been below the company's potential, as Management has conservatively deleveraged and allowed cash to accumulate. This is seen among many Japanese companies and contributes to reduced ROE.

Industry analysis

Automotive industry (Seeking Alpha)

Presented above is a comparison of Mazda's growth and profitability to the average of its industry, as defined by Seeking Alpha (16 companies).

Mazda underperforms its peer group, which primarily includes the largest traditional automakers, as well as several of the new EV players.

Mazda's growth has materially trailed in the industry in recent years, primarily due to the ability of the majors to price aggressively on the back of supply constraints. As the demand for Mazda cars is less high, it has not been afforded a proportionate effect.

Further, its margins are also lacking, although appreciating that at an FCF level, this gap materially shrinks. This is a reflection of both its competitive position and scale.

Valuation

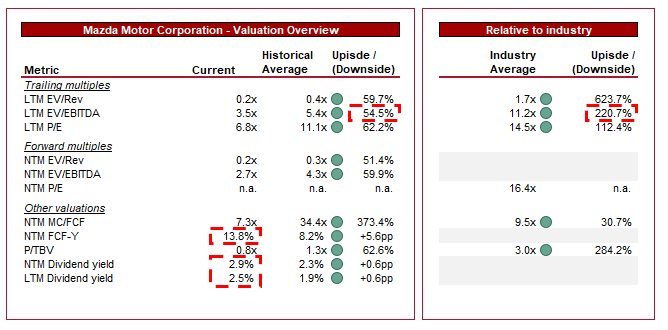

{kind=link}

Mazda is currently trading at 3.5x LTM EBITDA and 2.7x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is likely warranted, given the mild revenue growth, lack of margin improvement, and lack of EV development sufficient to safeguard its future. The latter point is our largest concern, as its slim margins need to be offset by growth at the higher end of LSDs.

Further, a discount to its peer group is equally warranted, reflecting its subpar financial performance and weaker brand in key automotive industries. Given the degree of discount, the relative view is not a reasonable metric for assessing fair value.

Based on this, Mazda looks undervalued, primarily due to the size of the discount relative to its historical average, which is inherently conservative. The company is trading at an over 100% discount to its peers on an EBITDA basis and over 50% on an FCF basis, underpinning this view. This represents an FCF yield of 14% (although appreciating that investors are not necessarily seeing this in the form of excess distributions). Following the recent share price appreciation, we would conservatively suggest an additional 20-25% upside, allowing for a (potentially conservative) 25-30% discount to account for medium-term risks associated with the EV transition.

Final thoughts

Mazda's approach to the automotive industry is respectable, with a highly regarded design philosophy and strong marketing to sell price-conscious consumers on the enjoyment of its cars. We suspect the company continues to perform in line with historically achieved in the years to come, continuing to lag behind its much larger peers.

The key consideration is whether the company is sufficiently progressing toward the EV future. We do not believe so. This will act as a drag on the company's share price and financial performance until the likely outcome is known.

However, with an FCF yield of 14% and support from Toyota, we believe the risk-to-reward profile is currently attractive.

For further details see:

Mazda: Journey Into The Electric Vehicle Era