MZDAF - Mazda Motor Corporation: Beneficiary Of The Depreciating Yen

2023-07-10 09:49:16 ET

Summary

- The strong jobs data in the US spells somewhat of a doom for the Yen, at least for now, as rates are going to have to continue to come up.

- While this could eventually be an issue for the leverage-driven automotive space, Mazda will likely benefit in a fundamental way.

- Pent-up demand continues, and the only really weak area is China. The depreciated Yen keeps vertically integrated production in Japan cheap.

- Mazda can achieve a wedge by building products in Yen and selling them to a meaningful extent in other currencies.

- Also, Mazda expects a recovery in China in 2024 and seems confident in unit growth in other geographies too despite macro conditions in the West due to volume recoveries after Shanghai issues.

Mazda Motor Corporation ( MZDAY ) is a great automotive pick to follow in the current environment, as it benefits from some smart moves to premiumise, some recent launches, recovery in volumes due to idiosyncratic supply issues, and most importantly a depreciating Yen. The key thing to know about Mazda is that a depreciating Yen doesn't create just a technical effect that could only benefit Yen denominated accounts, even the US listed units, listed in dollars, could continue to benefit as the depreciating Yen has a fundamental impact on the profit profile of the company since it is manufactured with Japanese parts and sold in foreign markets. This argument is true for many other Japanese automotive players as well and is an important backstop for the Japanese stock market, which is overwhelmingly automotive-exposed. While Mazda is a holistically correct pick, we still think there are other European automotive players with a more pronounced margin of safety, even if Mazda flows best with the changes we are seeing in the current market.

FY Results

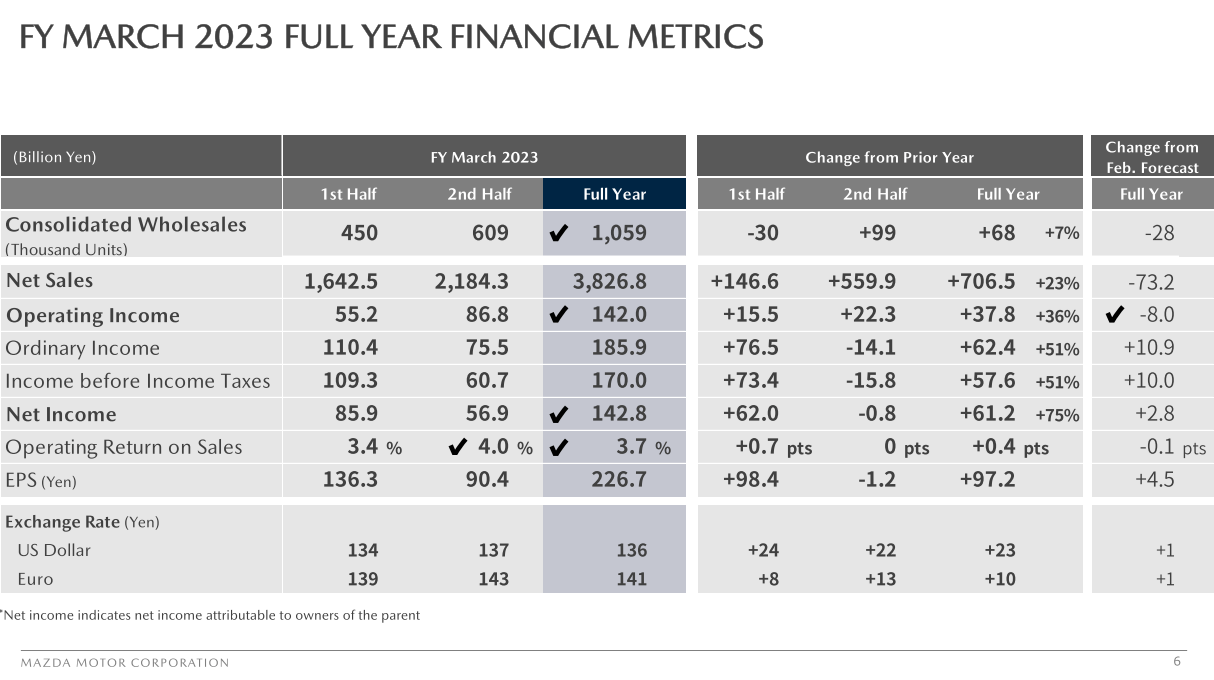

The units are up nicely by 11% as the company recovers from issues that hit volumes in Shanghai, causing general production delays. China is down 50%, but that is to be expected given their credit and COVID-zero situation that affected much of the year. The sales were up more than volumes, as the company is benefiting both from recent price action, but also from the fact that it has been premiumising over the last half-decade, and its ASPs are coming up.

Actual Metrics 2023 (FY 2023 Pres) Forecast (FY 2023 Pres)

{kind=link}

{kind=link}

The operating profit grew further as operating leverage kicked in, helped by the CX-90 release recently in North America, which is Mazda's most profitable market, as well as from FX effects, which are central to the story.

Since Mazdas are manufactured using many Japanese parts, and in factories that are furnished meaningfully by Japanese industrial providers, a weaker Yen, which is the denomination of much of their cost structure, is helpful when the Yen is a much smaller proportion of their sales portfolio. The US market is very important for Mazda's profit and growth plans, and what seems to be a well-received launch of the CX-90 is important.

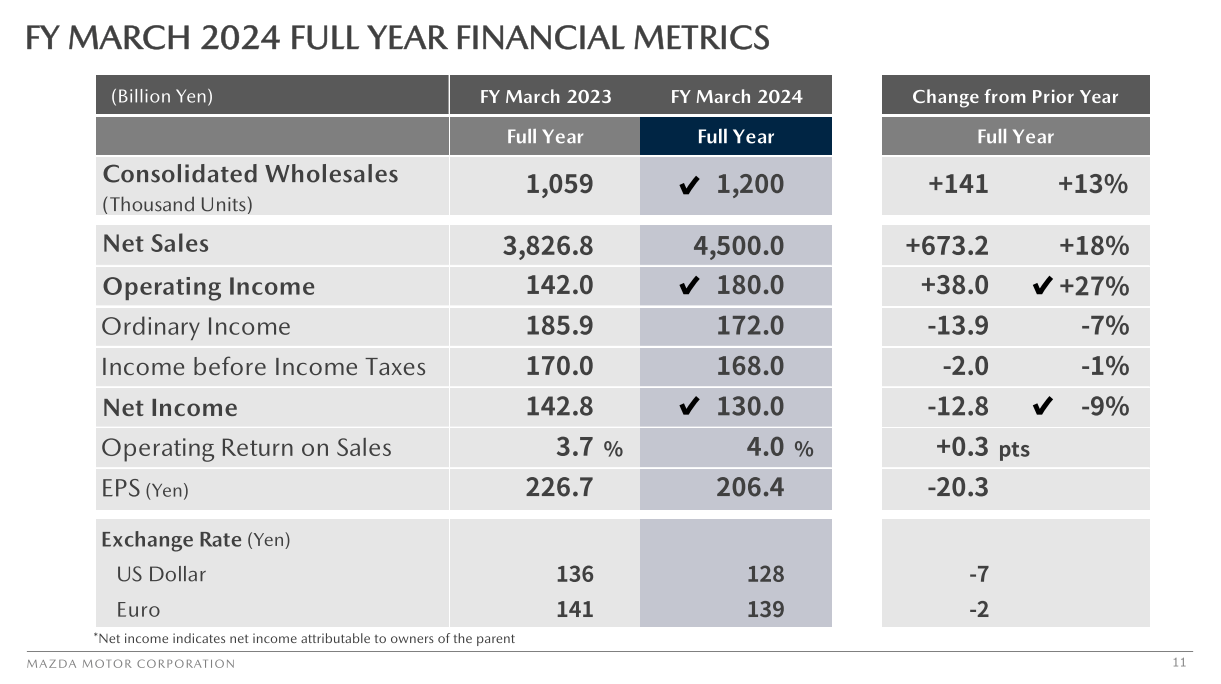

The Yen is likely to continue to depreciate on strong jobs data . Jobs data are being affected by two structural forces: they lag the health of the economy, and they are also currently being affected by pretty low levels of labour participation, which still has a negative impact on the overall labour supply. We are worried about a recession, but we think the setup lends itself to more interest rate hikes and more belligerent labour figures until something gives. Mazda forecasts a Yen appreciation in 2024 which would be to their detriment, but we think that this will not happen yet and that Mazda will benefit for another year from a weak Yen. In other words, we think results will be a bit stronger than expected from the FX side, and also given the strong forecasts for units, especially in a rebounding China.

Bottom Line

While Mazda has been executing well, including doing things on the marketing and sales side to improve gross margins and drive down some of the overheads in addition to benefiting from economies of scale, volumes are the main source of concern for us. The Yen may be reliably weaker than the USD for the time being, but pent-up demand in automotive will have to be exhausted at some point, and it's unclear if new cars financed by leverage are going to get bought at higher rates than before. While the ability to compete on price thanks to a Yen denominated cost structure helps, as well as the fact that Mazda was especially impacted by Shanghai lockdowns and has those lost volumes to recover, macro is a concern for us. Some analysts think that Q2 will be the last quarter before a plateau. Higher rates plus higher car prices are a dangerous combination for leveraged durables demand. Nonetheless, a large balance of Toyota Motor ( TM ) shares as well as net cash balances make the company cheap at an EV/EBITDA TTM of 2.8x. While compelling, we still think a more aggressive margin of safety can be found in Volkswagen ( VWAGY ) and its brands after the recent Porsche IPO and the potential value in its other luxury segments like Lamborghini considering Ferrari's ( RACE ) valuation. However, we choose to not take positions in automotive for the time being.

For further details see:

Mazda Motor Corporation: Beneficiary Of The Depreciating Yen