MZDAF - Mazda Motor: Pay Attention To China And Electrification

2024-01-02 10:25:44 ET

Summary

- The key negatives for Mazda Motor Corporation are the headwinds associated with the weak Chinese economy, and expectations of substantial electrification-related investments.

- The negatives are priced in to a large extent, as Mazda Motor stock is trading at a mid-single digit P/E multiple and a low-single digit EV/EBITDA ratio.

- I award a Hold rating to Mazda Motor Corporation, after taking into account China's economic prospects, the company's electrification transition, and the stock's valuation.

Elevator Pitch

I rate Mazda Motor Corporation ( MZDAF , MZDAY ) [7261:JP] stock as a Hold.

Mazda Motor should be able to command a higher valuation multiple in the future, when the Chinese economy shows signs of recovery and the company is at the later stages of the electrification transition journey. In the very near term, electrification investments are expected to weigh on MZDAY's earnings, while the sales outlook for the company's Chinese and Southeast Asian businesses is poor. As such, Mazda Motor warrants a Hold rating now, even though its valuations aren't demanding.

Investors should know that Mazda Motor's shares are traded on both the OTC (Over-The-Counter) market and in Japan. The three-month average daily trading values for Mazda Motor's Japan-listed shares and OTC shares were $60 million and $0.5 million, respectively as per S&P Capital IQ data. Readers can deal in Mazda Motors' relatively more liquid shares listed on the Tokyo Stock Exchange with U.S. brokerages such as Interactive Brokers.

Company Description

In its integrated report , Mazda Motor refers to itself as a company engaged in the "manufacture and sales of passenger cars and commercial vehicles." The company is headquartered in Japan and has been established since 1920.

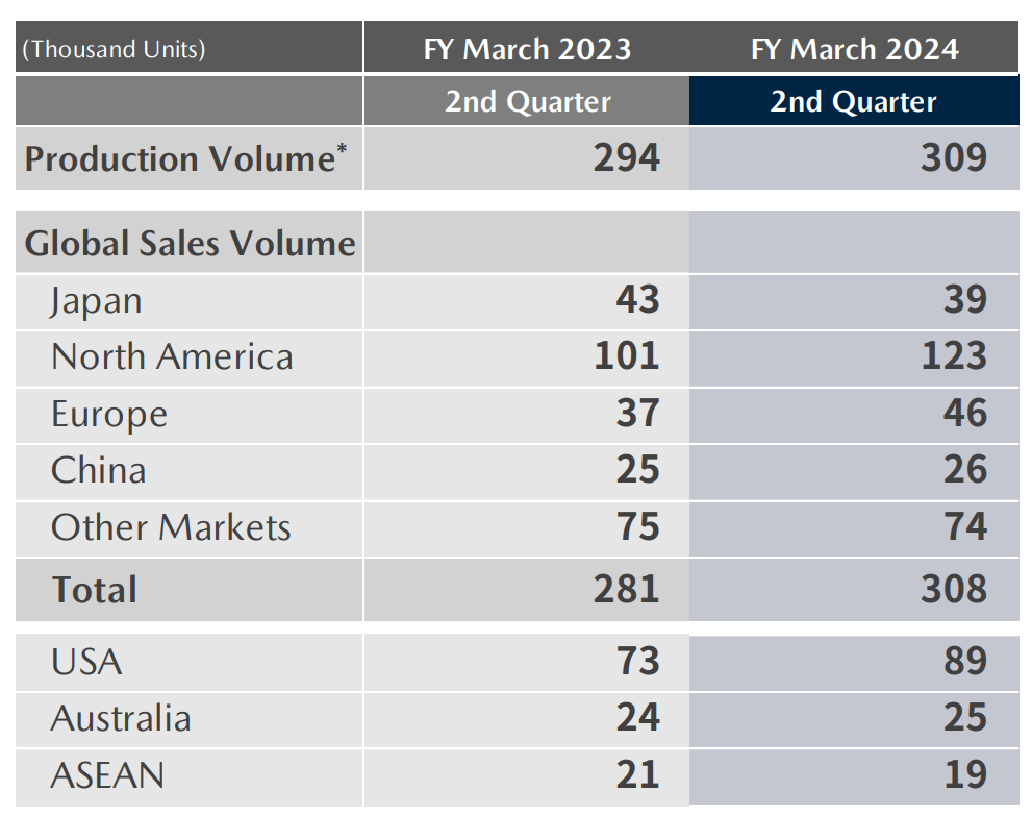

Mazda Motor's Sales Volume Mix By Market

{kind=link}

As highlighted in its Q2 FY 2024 (YE March 31, 2024) results presentation , MZDAY's market shares for the automotive markets in Australia, Japan, North America, Europe, and China were 7.9%, 3.7%, 2.3%, 1.1%, and 0.3%, respectively, for 1H FY 2024.

Weak Chinese Economy Is A Key Headwind For Mazda Motor

China's economy remains weak, and this is expected to have a negative impact on Mazda Motor's sales performance in the short term.

A January 1, 2024, Seeking Alpha News article noted that "China's Manufacturing PMI (Purchasing Managers' Index)" declined for the third consecutive month in December 2023 and also fell short of expectations. The lackluster economic outlook for the Chinese market helps to explain why Mazda Motor cut its full-year fiscal 2024 sales volume forecast for its China business by -34% in November 2023 (the prior projection was made in May 2023) as detailed in the chart presented below.

Mazda Motor's Full-Year FY 2024 Sales Volume Guidance

{kind=link}

MZDAY is expecting a modest single-digit (or +8% to be exact) sales volume growth for the Chinese market in FY 2024. At the company's Q2 FY 2024 analyst briefing Q&A session, Mazda Motor also guided that "demand in China is expected to remain flat from this fiscal year (FY 2024) to next fiscal year (FY 2025) due to the current uncertain economic situation."

Notably, the challenging automotive market in Mainland China has prompted Chinese automakers to accelerate their expansion plans in foreign markets such as ASEAN (Association of Southeast Asian Nations). Nikkei Asia published a commentary piece on December 1, 2023, highlighting that "more Chinese electric vehicle makers are heading into Southeast Asia," which it referred to as the "2nd China EV wave." Automotive companies from China such as Changan Automobile and Guangzhou Automobile Group ( GNZUF , GNZUY ) are following in the footsteps of their Chinese peer and early mover, BYD Company Limited ( BYDDF , BYDDY ), which boasts the biggest share of EV sales in Southeast Asia.

In other words, Mazda Motor is facing more intense competition from Chinese automotive companies in the ASEAN or Southeast Asia region. Therefore, it is easy to understand why MZDAY is guiding for a -10% contraction in sales volume for the Southeast Asia market in FY 2024.

To sum things up, the continued weakness associated with the Chinese economy translates into a slower pace of sales growth in the Mainland China automotive market and greater competition in the ASEAN market for Mazda Motor.

Electrification Investments Could Potentially Be A Drag On MZDAY's Profitability

Mazda Motor's EBITDA and EBIT are projected to decline by CAGRs of -0.6% and -0.4%, respectively, for the FY 2024-2027 time frame as per S&P Capital IQ's consensus data. Expectations of increased investments in electrification-related initiatives could provide an explanation for the company poor operating profit growth outlook.

In the company's 2023 Integrated Report published in late December last year, MZDAY outlined its long-term plans relating to electrification as detailed in the chart presented below.

Mazda Motor's Electrification Transition Plan

{kind=link}

In its Q2 FY 2024 results presentation slides, Mazda Motor disclosed that it had recently "established the Electrification Business Division," and also "appointed an officer in charge of electrification promotion" to "accelerate our efforts."

Based on the corporate disclosures highlighted above, it is highly probable that MZDAY will allocate a substantial amount of investments to support its electrification plans in the coming years. This is reflected in the sell-side analysts' estimates of Mazda Motor's future profit margins. In specific terms, Mazda Motor's pre-tax profit margin is forecasted to narrow from 6.0% in FY 2024 to 5.5% for FY 2027.

In a nutshell, even though the electrification transition is a necessary long-term strategic pivot, MZDAY will have to bear with short-term pain in the form of weaker profitability driven by electrification-related investments.

Closing Thoughts

Mazda Motor's valuations are depressed, but this is justified considering the negative effects of China's economic weakness and the drag on the company's profitability resulting from the electrification transition. As per S&P Capital IQ data, the market is currently valuing Mazda Motor at consensus forward FY 2024 P/E, EV/EBITDA, and EV/FCF valuation metrics of 5.0 times, 1.8 times, and 3.3 times, respectively. China's economy might recover in time to come and MZDAY's electrification investments could pay off in the long run, but these are medium to long-term catalysts. Mazda Motor Corporation deserves a Hold rating taking into account its current valuation and its unfavorable short-term outlook.

For further details see:

Mazda Motor: Pay Attention To China And Electrification