MZDAF - Mazda: Worrying Talk About Price Competition In China

2023-04-11 07:30:00 ET

Summary

- Mazda has the general issue that the Yen risks taking a recovery and hurting Mazda margins.

- With credit tightening being a concern now that banking is more fragile, automotive stocks seem generally risky.

- Finally, while China is reopening, there seems to be specific issues around this geography around price competition to revive the market.

- Incremental earnings growth seems unlikely, and we'd be wary despite the very low multiples.

Published on the Value Lab 04/08/23

Mazda ( OTCPK:MZDAY ) has had a pretty good YTD run in line with the catch-up game being played by Japanese markets behind the initial rally in the US. There have been several positive catalysts for the year, including continuing sales growth in non Yen-denominated markets, that have boosted returns. We also posited that a China reopening would be good. However, our view has changed, not only in light of the banking fragility and its likely impact on automotive, but also details on the success of the China reopening. Mazda stock is ridiculously cheap, but even so it is a pass.

Key FY Observations

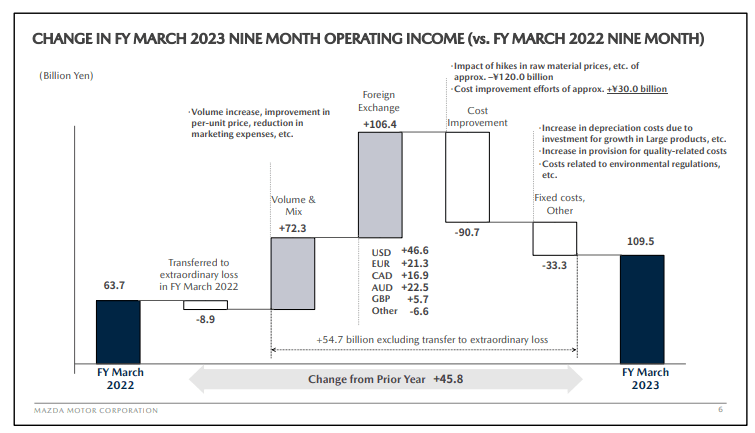

The operating income waterfall does a lot to summarize the FY 2023, and while the results end up being pretty backward looking with much having happened after the close of period, it is helpful to go through.

{kind=link}

Key positive forces have been FX. Mazda is Yen denominated, and with substantial Yen depreciation of around 20% relative to the dollar as the differentials in rates materialized in 2022, foreign market contribution ended up being massive in Yen terms. Moreover, a disproportionate amount of Mazda's costs are in Yen , so the impact in truly creating margin, not just technical growth coming from Yen depreciation, played a role in a positive result in 2022.

In addition to the FX effects, there was simply pretty good growth in North American and European markets in terms of car deliveries in 2022 thanks in part to loosening supply chain bottlenecks.

{kind=link}

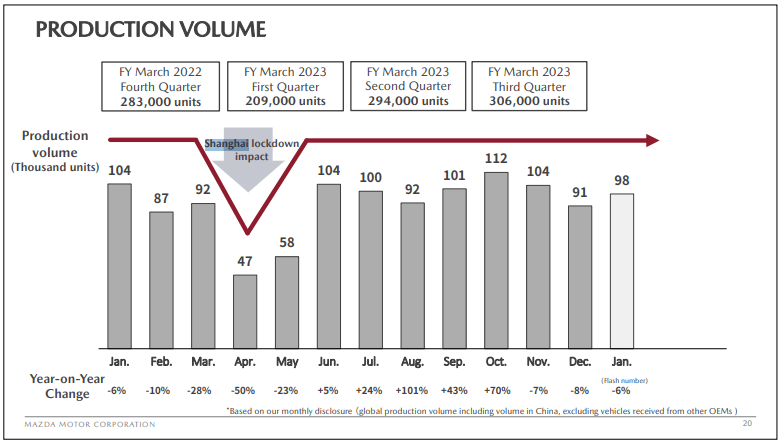

On the negative side there were lockdowns in Shanghai that created meaningful volume hits and torpedoed China results by more than 40%.

Our Outlook

China has since ended COVID-zero policies so more fiascos around lockdowns are unlikely, even if the recovery is jagged in China. There are other issues though. With the evident banking fragilities, we think that credit-dependent consumer durables markets including cars are going to start taking a hit, especially as pent-up demand around the semiconductor shortages in 2022 dissipates. We are already seeing some deceleration in North America in April compared to March . Comp effects aren't material here, and remember that NA is a huge market.

{kind=link}

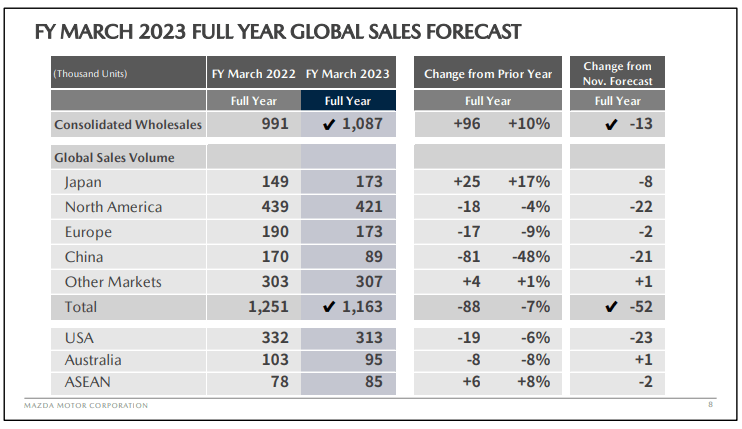

The secondary issue is around China. While nothing can be worse than 2022 for the Chinese exposure, the return to normalcy is coming at a price. Automotive manufacturers are engaging in price competition in this market. Since much of the current issues in China are related to the credit situation there, which was tanked by the real estate market, this is a pretty good data point for the deflationary effects we could worry about in the West if the inflation from credit withdrawal starts to look much more severe. Since China is an important market, a slightly gimped return to normal in this market is not a great thing.

Finally, we have a view on the Yen. While Japanese monetary policy has stayed entirely accommodative, and won't become restrictive in absolute terms, with the entry of Ueda we do expect some reversal in the Yen as while the Yen will still yield marginally, it will yield materially better than it currently does under what will likely be a more hawkish BoJ regime.

Bottom Line

Mazda is cheap as dirt at a <5x PE TTM. While we think the combination of smaller than expected benefits from a China reopening, a reversal of the depreciated Yen catalyst, and general issues in Western markets around credit availability for auto loans, which are huge in financing demand, will lead to declines in earnings, we don't think they'll be enough to render the current multiple overvalued. We should also point out that Mazda is about as cheap as Volkswagen ( OTCPK:VWAGY ) whose Porsche IPO is not being considered in their assets. Mazda is very cheap - but we decided that with enough opportunities in the markets, we can get other stocks similarly cheap that don't have the economic currents against us, even if only temporarily. We just don't need to take a chance on this one in terms of the timing of total returns.

For further details see:

Mazda: Worrying Talk About Price Competition In China