MBI - MBIA: Don't See Any Value Here

2023-09-28 21:52:15 ET

Summary

- MBIA Inc.'s share price has been volatile, and the company's historical performance and ongoing legal battle in Puerto Rico are concerning.

- MBI provides financial payment insurance and manages risk through diversification.

- The company's recent income shows rising concerns, and the ongoing challenge in the PREPA case is impacting operations. Valuation is not favorable, and there are significant risks associated with Puerto Rico obligations. A sell rating is recommended.

Introduction

MBIA Inc. ( MBI ) is engaged in the insurance industry where it serves a variety of different customers and clients through its operational and extensive offerings as well. Looking at the last 12 months for the company, the share price has been very volatile. In early March, the share price tumbled quickly following their earnings release. It seems though that the company was caught up in some of the turmoil of the banking industry, which sent shockwaves through the markets. The share price tumbled quickly, even if MBI managed to beat both the top and bottom lines for the quarter. I remain however quite concerned about the company's historical performance and the ongoing battle with the Supreme Court in Puerto Rico is worrying me that MBI will deliver a lackluster performance over the coming years. This results in me issuing a sell for MBI. Besides, the company has a negative bottom line, which is only adding to the sell case currently.

Company Structure

MBI has built its business around providing financial payment insurance. The fundamental concept is that clients seeking to secure financial payments, such as those from bond issuers, can pay MBI a premium. In return, if the issuer defaults on its payment obligations, MBI commits to fulfill those obligations on behalf of the client.

To manage risk effectively, MBI employs a strategy of diversification. This entails spreading its coverage across numerous issuers, industries, and geographic regions. By doing so, MBI aims to mitigate the impact of any individual issuer's default. In essence, the premiums it receives for covering these diverse payment streams help offset potential losses arising from isolated defaults.

{kind=link}

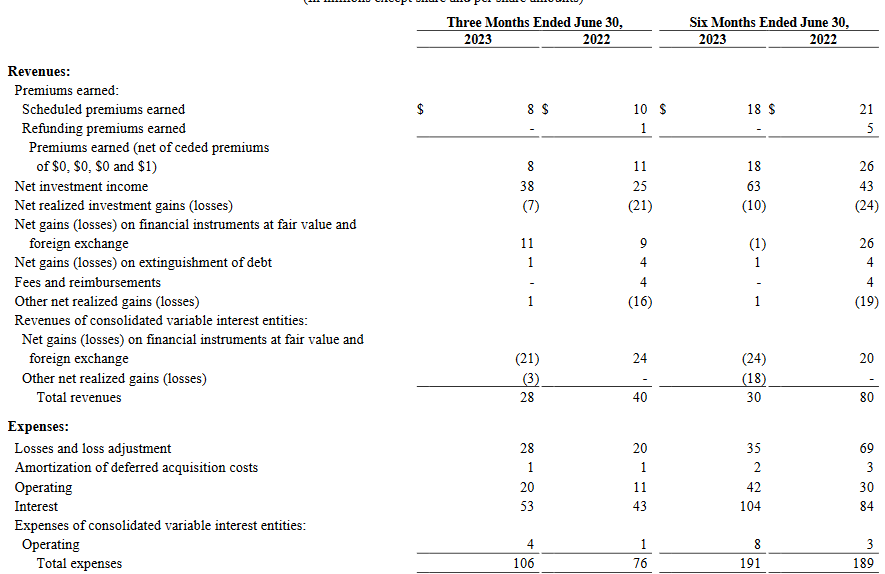

Looking at the recent income report from the company, I think it displays rising concerns as the operating expenses are increasing quite quickly. In the last quarter, it landed at $106 million and ultimately led to a negative EPS result of $0.45. This was also a significant miss on expectations of $0.35. The results didn't have a massive impact on the share price, it has only slightly declined following the last report. I think the market is anticipating the worst and MBI will continue to trade quite irrationally.

The financials of the company have seen some decent improvements over the last 6 months. The cash position for example has grown to over $200 million, up from $50 million on December 31, 2022. I think this is moving MBIA into a more conservative financial position, as it should hopefully lend them some more flexibility as well. Looking at the debts of the company, they have seen a slight increase to $2.5 billion. Given that MBIA has a market cap of under $400 million, that is a substantial amount of debt given the size of the business. I would imagine that if interest keeps rising, it will be weighing heavily on the earnings potential of the business. The interest expenses have already risen quite sharply to $176 million in the last 12 months. All in all, I think there are some good improvements on the balance sheet, however, it's overshadowed by the large amount of debts the company holds.

Earnings Transcript

Let's get some further insight from the management of MBI as well as the current situation they are in. The CEO of the business Bill Fallon had some good comments that I think are worth including here.

-

“While we await the filing of PREPA’s third plan of adjustment, we continue our efforts to deliver shareholder value in other areas, including by reducing expenses, monitoring the run-off of our insurance portfolios, and repurchasing shares”.

It seems that MBI is still in a weird spot where the ongoing challenge in the PREPA case is putting a toll on the operations. This lackluster progress I think further adds to the dullness of investing in MBI right now. The company is caught up in the legal dispute in Puerto Rico and can't fully focus on expanding instead.

-

“As noted earlier, we remain hopeful that PREPA will resolve sooner rather than later. Following the insurance claims payments made by National on July 1st of this year, its remaining exposure to PREPA is $610 million of gross par insured”.

The company is dependent on positive news about PREPA. When the news comes out it does feel like a coinflip though on how the share price will react. The market can be irrational sometimes and taking a bet on that is discouraging I think. Negating unnecessary risk I think is reasonable in times like these, making me stay away from MBI right now.

Valuation & Comparison

From a valuation view, MBI doesn't offer anything significant right now I think. The company had a negative bottom line, and the last time it had positive earnings was in 2015. Furthermore, the company has managed to gather up a debt position of $3.4 billion which is going to weigh heavily on the capital allocations strategy. Little shareholder value seems likely and if the bottom line does get raised quickly the likelihood of share dilution is further increased.

{kind=link}

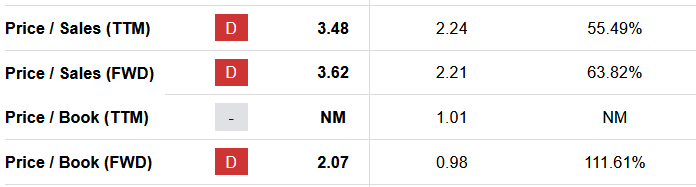

Looking at the p/s tough for MBI it stands at 3.87 right now on a FWD basis. That is a premium of 69% to the sector median. With the uncertainty revolving around the company right now, it looks even more expensive and I think the market is not properly accounting for these risks.

Looking at a peer like Universal Insurance Holdings Inc ( UVE ) I think it looks far more appealing on the surface. UVE has a positive bottom line and a strong dividend yield of over 4% as well. Looking at the p/s of UVE it sits significantly below that of MBIA at under 0.32. The p/b is 1.23 on an FWD basis, perhaps higher than the sector median, but in comparison to MBIA, it still exhibits a good discount and more favorable investment.

Risk Associated

MBI faces significant risks associated with its obligations related to Puerto Rico. Specifically, there are four major issues, including General Obligation Bonds, PBA, PRHTA, and PREPA, which are currently undergoing bankruptcy-like processes governed by Title III of the Puerto Rico Oversight, Management, and Economic Stability Act (PROMESA).

However, there is a significant risk that negotiations may falter or reach an impasse. In such a scenario, MBI could face challenges in fulfilling its contractual guarantee payments while potentially being unable to recover a substantial portion of them. Even if the negotiation process proceeds positively, it may extend over several years, leading to a substantial reduction in investor returns. This prolonged timeline can add uncertainty and complexity to MBI's financial outlook, requiring careful monitoring and risk management strategies to navigate potential challenges effectively. The share price seems to have peaked back in early 2022 and has been heading downward ever since. I fear that this trend will likely continue as the disputes that the company has is seeing little progress. For shareholders in MBI, I think it's better to get out and look for better opportunities elsewhere right now in the market. Sitting and bag-holding shares here seem unnecessary and leave potential ROI on the table still.

Investor Takeaway

MBI has had a consistently negative bottom line and with a large debt position, I am skeptical about the actual value that investors can get here. There are also no significant tailwinds or catalysts that I could see viable for raising the margins for the business. The growth seems limited and I would rather stay away, resulting in a sell rating.

For further details see:

MBIA: Don't See Any Value Here