MBI - MBIA Inc. Soars On Massive Shareholder Payout

2023-12-10 09:00:00 ET

Summary

- Shares of MBIA Inc. surged 81.8% after the announcement of a large inflow of capital and a one-time distribution to shareholders.

- The company's financial performance has been declining, but its net assets and potential distributions suggest further upside.

- MBIA Inc. received approval for a $550 million dividend, with $409 million to be paid as a special dividend to common shareholders.

Absent a buyout or merger scenario, it is incredibly rare to see shares of a company nearly double in the course of a single day. I have seen it in the pharmaceutical industry when a company gets a drug approved. But beyond that, such a movement higher is almost unheard of. Lo and behold, on December 8th, shares of MBIA Inc. ( MBI ) skyrocketed, closing up 81.8%. This surge in price was driven not by some buyout development or some major discovery. Rather, it was driven by news that the company is going to receive a large inflow of capital, much of which will be used toward paying a large one-time distribution to shareholders. When you look at the recent financial performance of the business, the picture looks anything but great. But when you dig a bit deeper and see just how much safety there is in its net assets, and you consider management's recent rhetoric regarding distributions, it's likely that further upside exists from here.

A big development for a small firm

Before I get into the newest details regarding MBIA Inc., it would be helpful to discuss a little bit about the company and what it does. This is a truly complex business and multiple articles could be written about various facets of it. So my objective here is to be brief but precise. According to the management team at the business, the firm owns multiple operating subsidiaries that provide financial guarantee insurance policies to investors. In short, its insurance policies are meant to cover losses in the event that a municipal or other issuer defaults on the debt that it makes available to the investment community. This can mean the interest that would be payable, the principal that would be payable, or even both, in the event of a default.

I don't think that it would be incorrect to say that the enterprise is largely inactive these days. What I mean by that is that, as opposed to writing new policies, the business seems really dedicated toward ensuring that existing policies are honored and that any potential capital above that is ultimately returned to shareholders. For instance, its largest subsidiary, National Public Finance Guarantee Corporation, has not written any new financial guarantee policies since 2017. Its primary business is instead centered around providing ‘ongoing surveillance, including remediation activity where warranted, of its existing insured portfolio’ of gross par value outstanding. As time goes on, that number has been on the decline. As of the end of the most recent quarter , it stood at $29.1 billion. At the end of last year , meanwhile, it was $31.7 billion. Another subsidiary, MBIA Corp, has $2.9 billion outstanding, which is down from the $3.4 billion the company had at the end of last year.

{kind=link}

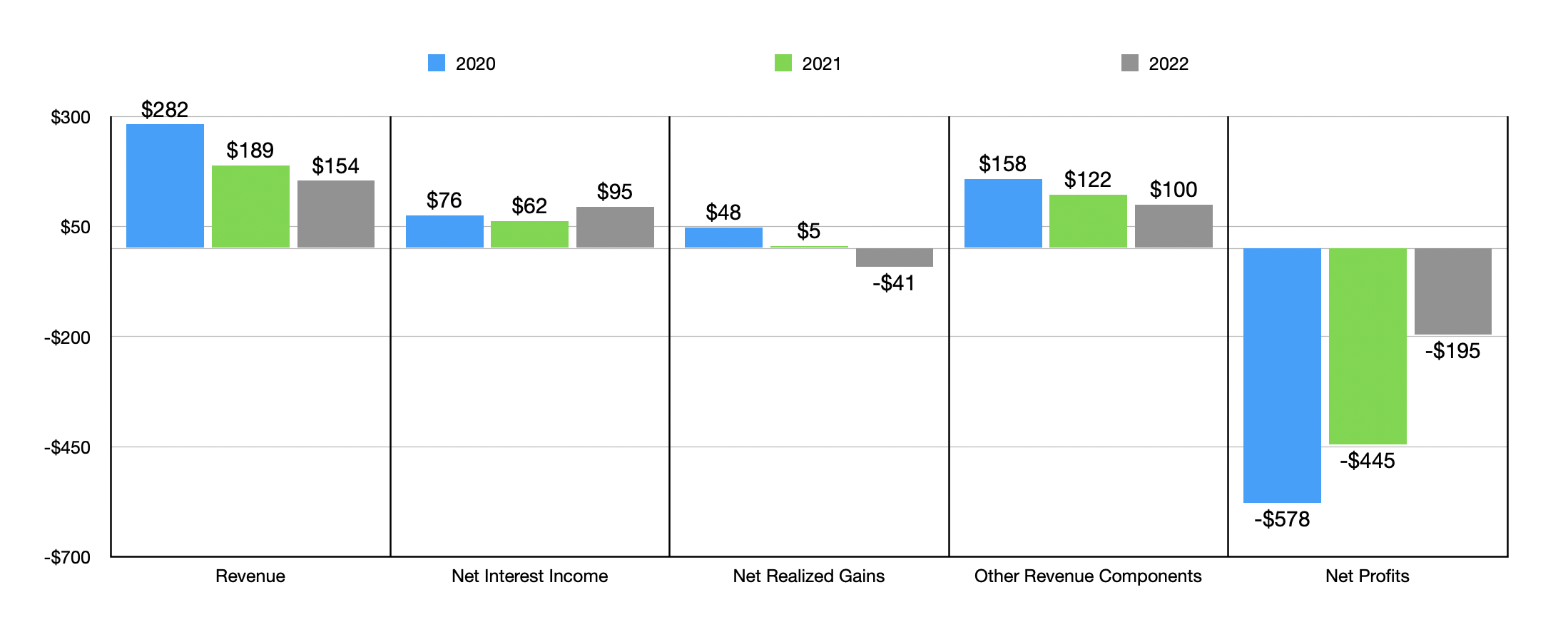

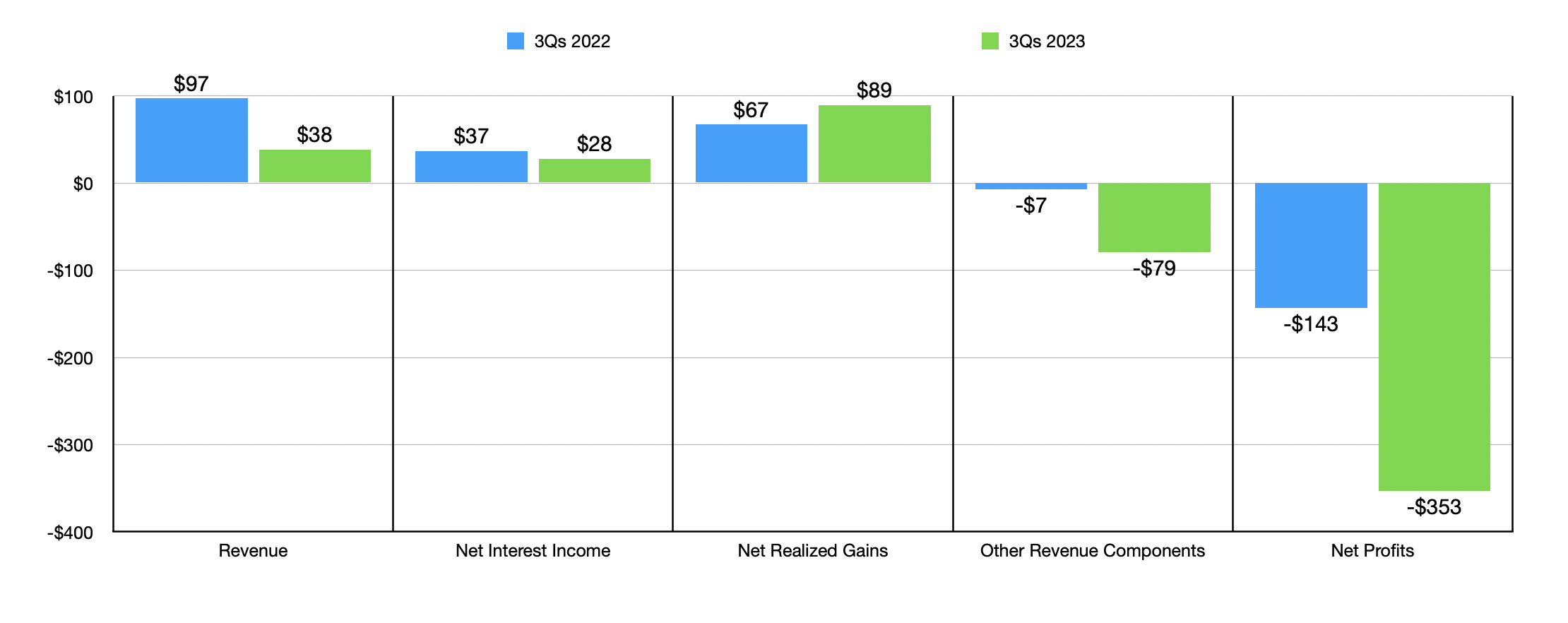

If you were to look at the picture of the business from a revenue and profit perspective, your initial inclination would be to run for the hills. From 2020 to 2022, total revenue for the enterprise declined from $282 million to $154 million. There are various pieces that go into the revenue picture, with the most significant being net interest income. In the chart above, you can see a breakdown of a couple of these. Over the same window of time, net profits did improve, with the company going from a net loss of $578 million to a loss of $195 million. As you can see in the chart below, financial performance for the first nine months of this year has worsened considerably compared to what it was at the same time last year. Revenue and profits have taken a hard turn lower.

{kind=link}

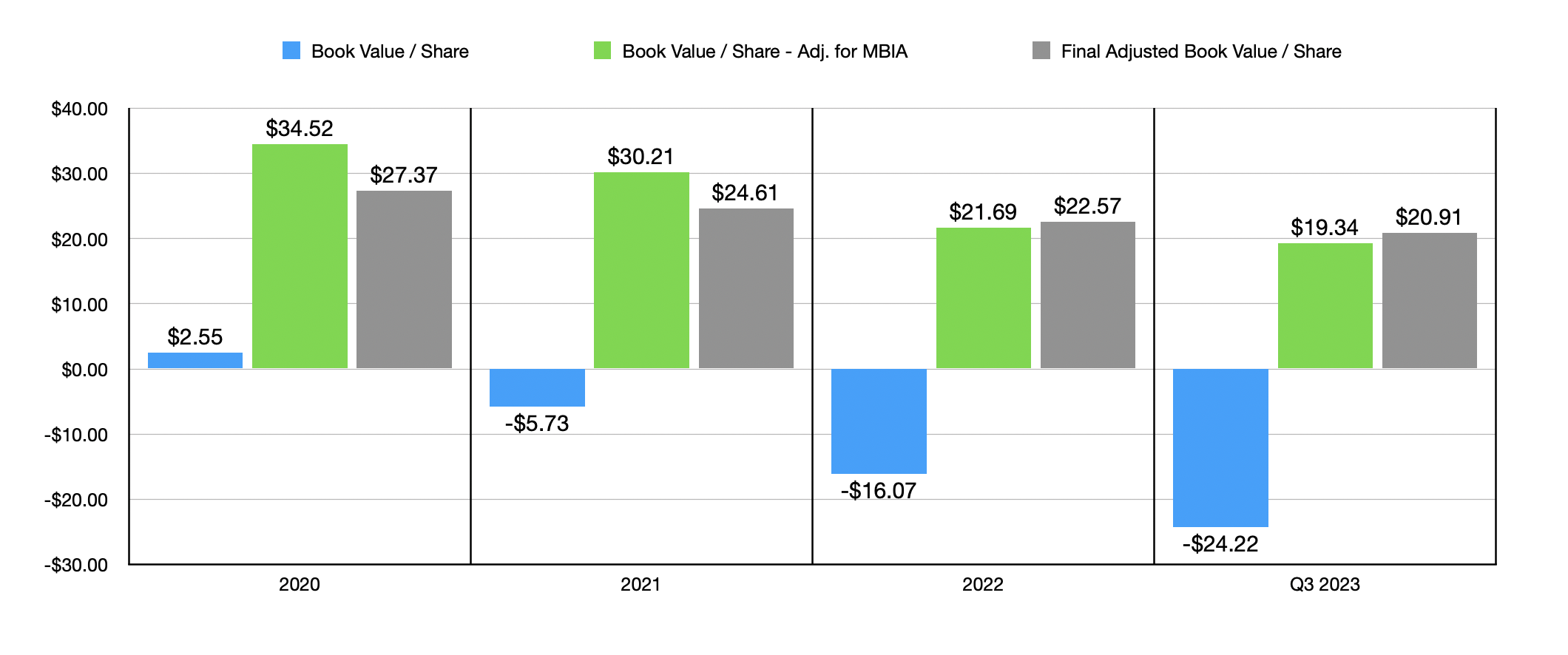

But this is where it's important to dig as deep as you possibly can. Because even when you think that you might have reached the bottom of the well, you can still go further. As an example, when I first looked at these numbers, I thought that there might be some attractive asset value at play. But as of the most recent quarter, the company had a book value of equity that was negative to the tune of $1.23 billion. That translates to a book value per share that is negative in the amount of $24.22. And that number has also been worsening over time. Back in 2020, for instance, book value per share was positive in the amount of $2.55. By the end of 2022, it had turned negative in the amount of $16.07.

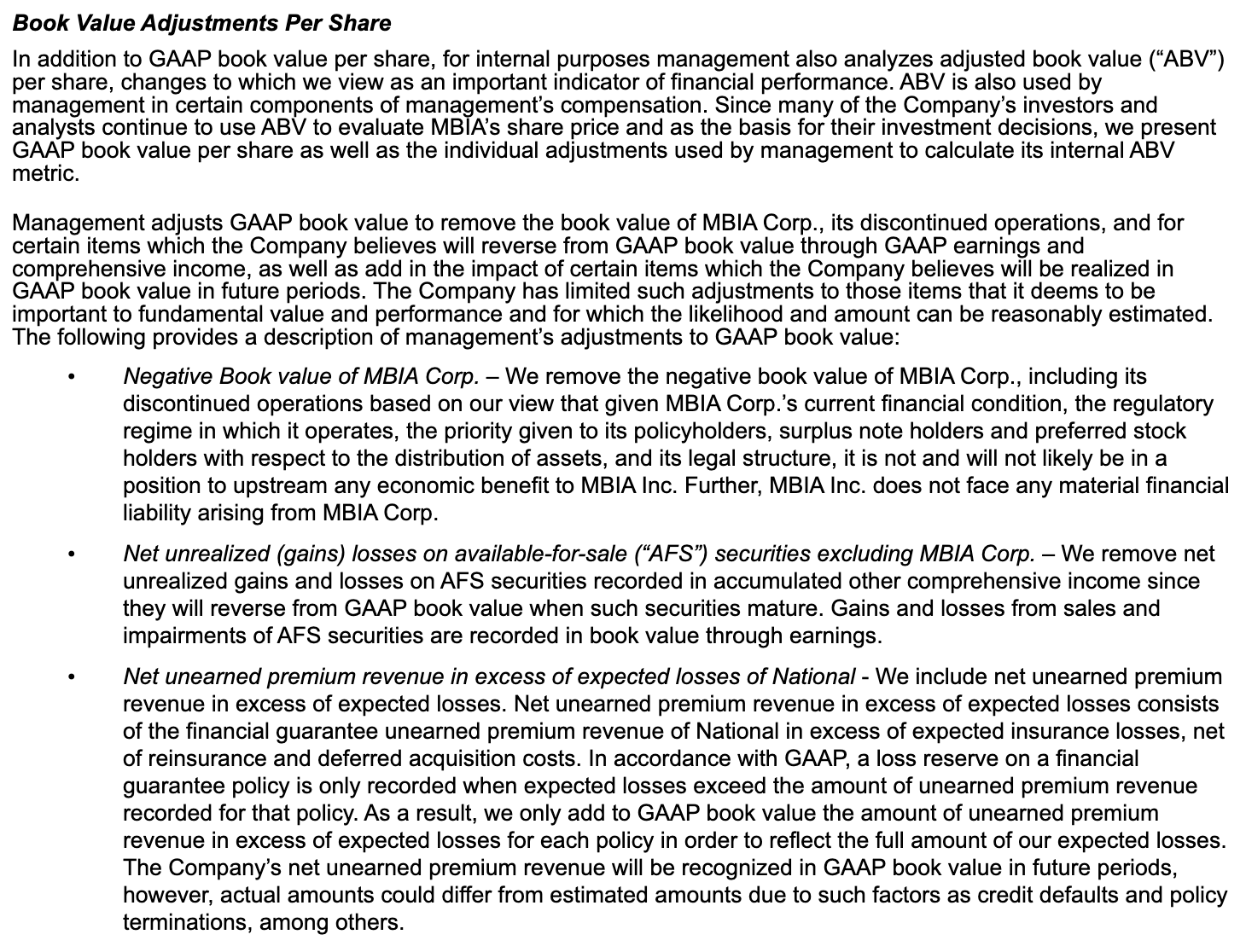

{kind=link}

Clearly, the general trend for the business does not look positive at all. But if you continue to dig beyond that, you find that certain adjustments to the firm's book value of equity are appropriate. Most notably, you can justifiably remove the negative book value of a subsidiary called MBIA Corp. This is because, based on its current financial condition and the regulatory system in which it operates, the parent company would not face any material liabilities associated with that entity. If we remove that from the equation, the firm suddenly has a positive book value of equity of $19.34. To put this in perspective, even after shares skyrocketed on December 8th, they were still trading at $13.42. There are a couple of other adjustments that can be made as well. And when you do that, you end up with a positive book value per share for the enterprise as a whole of $20.91.

{kind=link}

Make no mistake. It is true that as time goes on, the book value of equity, even on an adjusted basis, continues to worsen for the business. The adjusted figure was $27.37 per share back at the end of 2020. But again, you can't expect much more than this from an enterprise that is only managing existing operations instead of emphasizing growth opportunities. Where the opportunity for additional value comes into play is in the distributions that the company can receive over time. And that is precisely what the news released on December 7th covers.

According to the management team at MBIA Inc., the New York Department of Financial Services approved an extraordinary dividend to be paid to MBIA Inc. by the National Public Finance Guarantee Corporation in the amount of $550 million. This is in addition to $97.245 million that was paid out last month. In response to this, MBIA Inc. has decided to allocate $409 million of this, working out to $8 per share, to be paid in the form of a special dividend to common shareholders who are of record as of December 18th. What's really exciting about this is that, up to the cost basis for individual investors, all distributions will be tax-free returns of capital. Anything beyond that point will be taxed at the capital gains rate.

Management intends to use the rest of the cash between the two distributions it has received for general corporate purposes and, potentially, some minor debt reduction. In all, it should have about $238.2 million of additional cash at its disposal thanks to this development. Realistically, shares of MBIA Inc. will decline to some extent once this distribution is paid. It wouldn't be surprising to see shares drop by the full $8. However, when we consider the significant book value per share that the company has, it does still appear as though the enterprise is undervalued.

I would be remiss if I did not mention one other issue that the company does have that is still unresolved. This involves its exposure to Puerto Rico. Odds are if you have followed MBIA Inc to any meaningful extent, you know a great deal about the troubles that it has had there. So I will spare the details. Instead, I will focus only on its final material exposure to the territory, which would be the Puerto Rico Electric Power Authority, also known as PREPA. Back on January 1st of this year, PREPA defaulted on scheduled debt service for National Public Finance Guarantee Corporation. In July of this year, it defaulted on additional liabilities. This all followed a move back in March of 2022 in which PREPA terminated a pending restructuring support agreement that was originally entered into in the middle of 2019.

By the end of 2022, MBIA Inc. found itself on the hook for as much as $945 million of gross debt service associated with PREPA. That number has since dropped to $808 million because of payments that MBIA Inc. has made good on. It seems like we won't have any further material updates on this until early March of next year. But investors should understand that this does materially increase the risk to shareholders.

Takeaway

Clearly, the news of a special dividend that was not expected was well received by shareholders of MBIA Inc. The stock would not have popped up otherwise. After the payment is made, I would expect shares to pull back a good amount. But this doesn't make the company a bad investment. When you really dig deep and come to understand its inner workings, it does seem to offer some nice upside potential. But at the end of the day, this is one of those high risk/high reward prospects that investors should not tread into carelessly. Keeping in mind how speculative it is, I am going to rate it a soft ‘buy’. But I would definitely discourage anybody who has a low tolerance for risk to even consider shares at this time.

For further details see:

MBIA Inc. Soars On Massive Shareholder Payout