MKC - McCormick: Bubble Valuations Have Not Deflated But The Thyme Is Cumin

2023-03-16 09:16:01 ET

Summary

- McCormick has been underperforming the consumer staples sector in the last year.

- The former high flyer has been weighed down by poor results.

- We take a first look at this company and dissect the valuation.

McCormick & Company, Incorporated ( MKC ) describes itself as "end-to-end flavor". We do not disagree.

{kind=link}

MKC is a global leader in all things flavor, operating in around 170 countries and territories. The company manufactures, markets and distributes products across the spectrum to customers in the food industry.

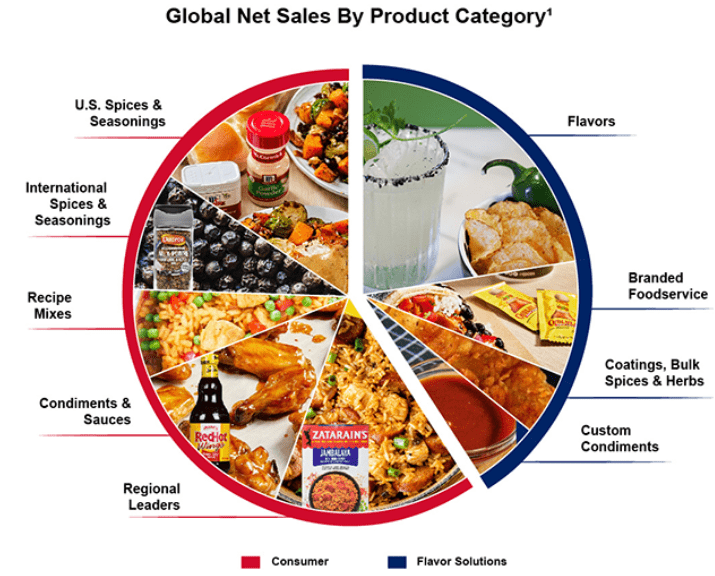

Its Consumer segment includes popular brands like the eponymous "McCormick", "Frank's RedHot", and "Club House", along with ethnic and regional brands like "Thai Kitchen", and "Simply Asia" among others. And this is just a little taste (pun intended) from the North American market. More than half of the Consumer segment comprises sales of spices, seasoning, condiments and sauces, with MKC even occupying the global leader position for the first two categories. Customers for this segment include retailers of all shapes and forms including grocery stores, warehouse clubs, discount and drug stores. They also supply to wholesalers and private label items, aka, store brands.

{kind=link}

The flavor segment comprises multinational food manufacturers and food service customers. They cover the market for customized flavors solutions for the products noted in the above picture. MKC does not stop at meeting product needs, they also assist in sensory testing, culinary research, food safety and flavor application.

{kind=link}

Chocolate has trumped spices in the last three years. Christopher Columbus would have been flummoxed and so are we.

Today we will review the numbers and see if the relatively sane price action makes this a buy for us.

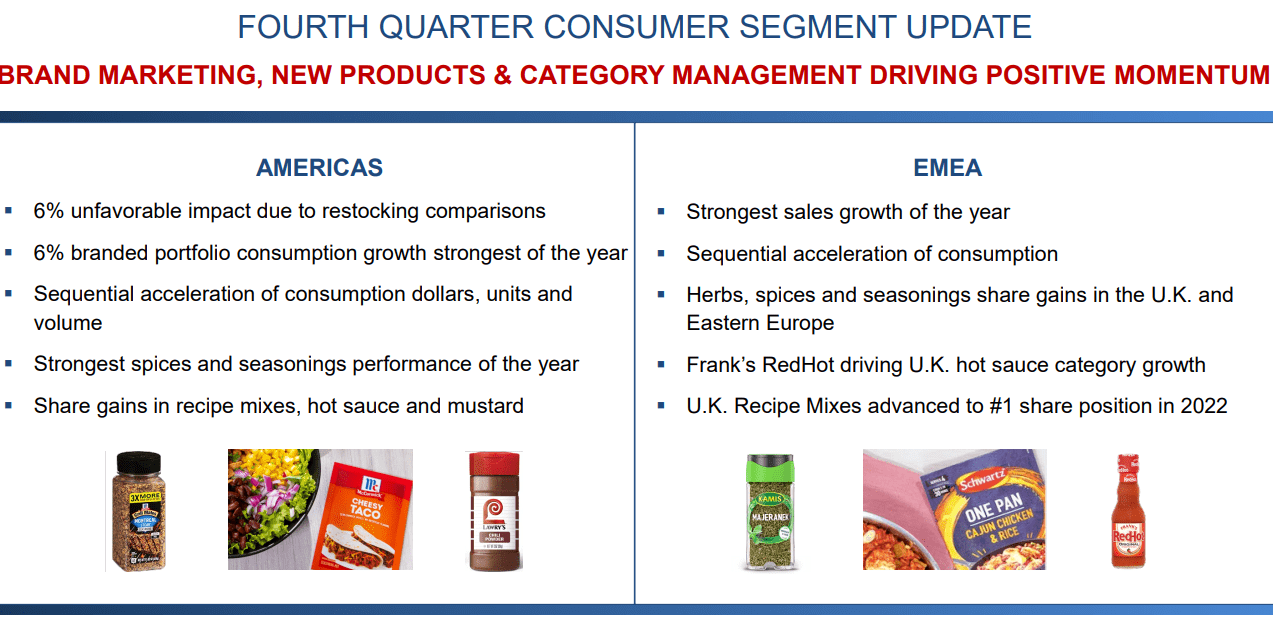

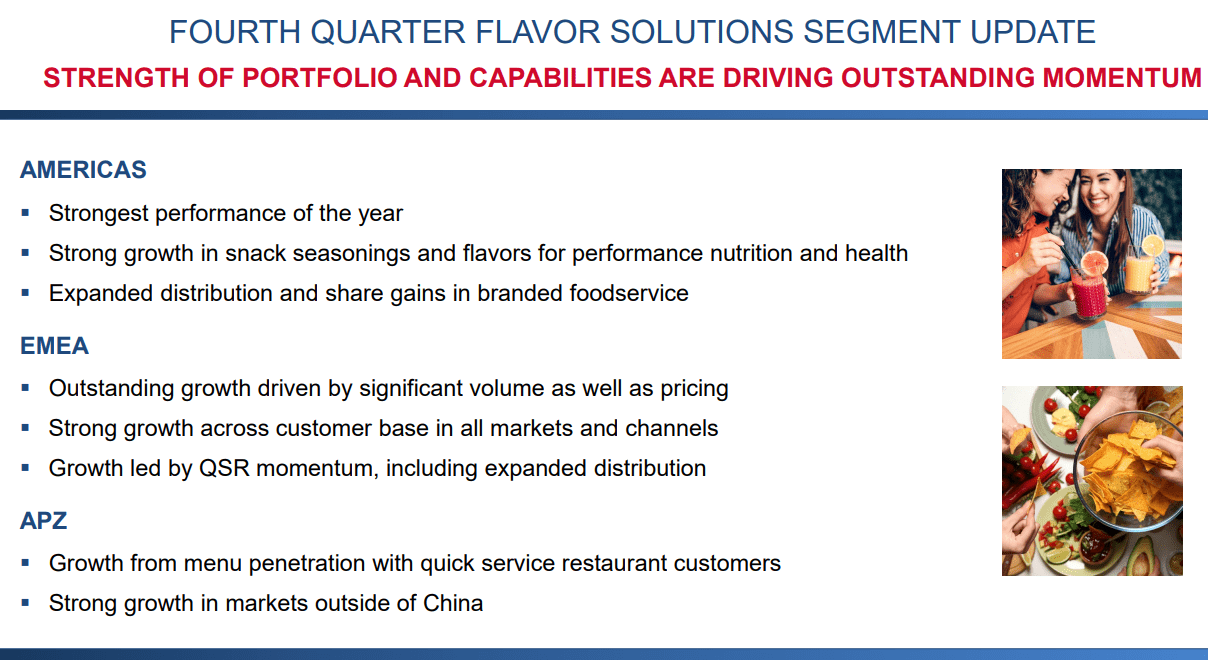

Q4-2022

The most recent results were quite an unmitigated disaster as MKC missed earnings estimates by a whopping 14 cents a share. Revenues came in short as well and dropped $80 million under estimates. But the earnings picture was the one that got bulls reaching for the ginger.

{kind=link}

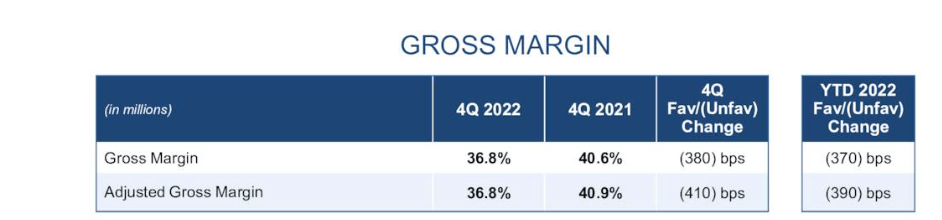

Adjusted gross margins were walloped and similar to Hormel ( HRL ), the company lost a lot of ground despite raising prices.

Q4-2022 Presentation

The company is expecting a 6% sales growth in the year ahead. Based on how they have been raising prices, we will venture to guess that this is all a price effect with volumes coming in flat. That theory is also seen in the expectations that adjusted operating income will be up double digits.

Valuation & Outlook

If you looked at the 30% drop from the highs last year, you would expect that this consumer staples company has probably become cheap.

Unfortunately such was the mania of 2020 and 2021 that 30% declines barely dented the valuation metrics. MKC still trades at about 28X earnings estimates for the fiscal year ended November 2023.

{kind=link}

For that multiple you will be the recipient of a mind blowing 1.45% earnings growth year over year. We will add this earnings growth was made feasible primarily by MKC missing November 2022 earnings estimates by mile. Now to be fair to MKC bulls, the stock does tend to trade expensive and P/E ratios have trended above 30 on more than 1 occasion.

So perhaps one could argue that it is not as expensive as it looks. But checking on other metrics is not very comforting either. On a price to sales basis, the company is still near 3.0X.

Here 2.0X ratios look more appropriate for the long run and the upper end of our comfort zone, assuming MKC can continue delivering good margins, would be 2.25X. Finally, on an EV to EBITDA ratio MKC looks almost comically expensive for a company poised to grow so slowly over the next 12 months.

The key question here is whether the growth for the next 12 months is an aberration or is it the path the company will see for the foreseeable future. Well, over the last decade, sales have grown at about 5% a year, a good deal of that coming from price increases.

In a tough recessionary environment, which we see dead ahead, it is hard to imagine MKC maintaining pricing power versus "generics". On offset here is the fact that MKC is the leading private-label spice and seasoning producer. In other words, some "generics" and store brand business will come its way. It does supply Dollar General and Family Dollar stores currently and we think this makes the business a little more resilient. But this potential move from MKC's brands to private label will likely keep pressure on margins and at 28X earnings we are really reaching here. In fact, should we see another few earnings estimates misses down the line, we would not rule out a solid contraction to 20X earnings. That is hardly farfetched considering that the company has traded below that on two occasions. in the last 15 years. On both occasions, interest rates were far lower.

Verdict

MKC is a solid consumer staples story but one which we think is in the process of deflating. Well, the stock valuation is going to deflate more, not the company. In fact, extremes of valuation in one direction tend to create extremes in the other direction. We would not be surprised to see this at even a 16X earnings multiple in 3-4 years. That would be a very unpleasant journey even discounting above average growth rates for the company. At present the stock looks oversold and perhaps you get a bounce here. Longer term, we don't see this as an ideal buy point. We think we will get that though within the next 12 months and it likely will be at least 30% lower. We rate this as a Sell.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

McCormick: Bubble Valuations Have Not Deflated, But The Thyme Is Cumin