MKC:CC - McCormick & Company: Too Spicy Currently On Financial Weakness

2023-12-21 22:32:39 ET

Summary

- MKC has grown well during the last decade (+5% CAGR), owing to global expansion and periodic acquisitions to enhance its business.

- The company is built on brand enhancement and marketing superiority, underpinned by product development and outspending its peers. This has been successful and gives it a defensible position in key.

- MKC’s recent performance has been disappointing, although it may be on the up. Margins are down, and growth is purely price-driven.

- MKC performs well relative to its peers. The company is tracking well in terms of growth despite its substantial scale, while generating significantly superior margins. We see a continuation of this as management targets operational improvements.

- MKC’s valuation has slipped, but we are still not sold. We would like to see operational improvements achieved and deleveraging, as well as a discount to its historical NTM FCF yield.

Investment thesis

Our current investment thesis is:

- MKC is a quality business but the timing is not correct in our view. The business has developed well during the last decade but several decisions were made that now leave the company in a weaker position than it otherwise would be. Interest payments are rising fast and restricting its ability to take advantage of the current market conditions (e.g. cash acquisitions). This is not a medium-term issue, Management has already deleveraged considerably in the YTD period and will likely only need to do a little more. This said, investors should not bear the timing cost of this.

- Further, the company’s recent financial performance has slumped, primarily reflected in its margins, although the top line is price-driven with volume also weak. Again, we do not see these as medium-term issues but will likely take 1-3 quarters to unwind.

Company description

McCormick & Co. ( MKC ) is a global leader in flavor, producing and distributing spices, seasoning mixes, condiments, and other flavorful products to the entire food industry, including retail outlets, food manufacturers, and foodservice businesses.

Share price

MKC’s share price performance has been moderate during the last decade, returning over 100% to shareholders inclusive of distributions, although has lagged behind the wider market. This is a reflection of positive financial development but a recent pull-back.

Financial analysis

{kind=link}

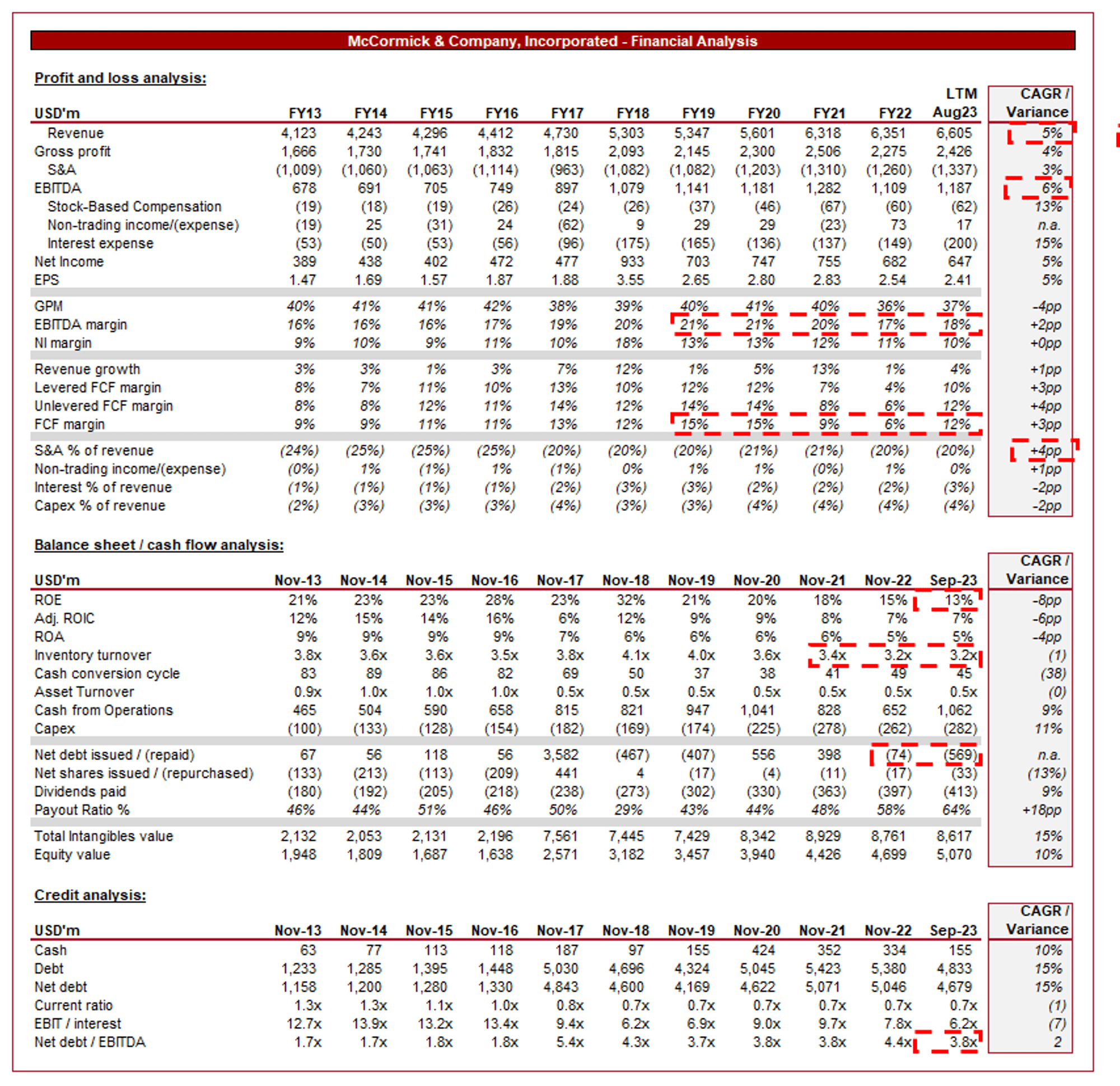

Presented above are MKC's financial results.

Revenue & Commercial Factors

MKC’s revenue has grown well for a mature business, with a CAGR of +5% into the LTM. Growth has been consistent and supported by M&A, with only three periods of ~1% growth. EBITDA has exceeded this rate, with a CAGR of +6%.

Business Model

MKC offers a wide range of products, from spices and herbs to sauces, marinades, and condiments. MKC has established a range of trusted brands in these industries. Its brands are associated with quality, authenticity, and superior flavors, contributing to consistently recurring purchases that appeal to a broad customer base.

MKC has a presence in over 150 countries, leveraging its deep expertise in production and brand building to tap into new markets worldwide. It can cost-effectively adapt its products to suit local tastes, broadening its revenue growth potential.

MKC has a strong distribution network that ensures its products are readily available to consumers through a number of leading outlets. Its strong brand development allows it to be a leading option for consumers, with distributors playing into this (positive cycle) by giving it preferential terms (such as shelf space, access to more stores, etc.). Its products are distributed through grocery stores, supermarkets, e-commerce platforms, and foodservice channels, maximizing its market reach.

MKC has strategically acquired companies that complement its product offerings and/or expand its market reach / distribution potential. These acquisitions have enhanced its portfolio and often led to synergies and cost efficiencies. We would like to see this strategy continue ( although noting that a detailed discussion of capital allocation will follow ), as it can support organic growth and improve the company’s runway.

MKC has seen reasonable growth in recent years, with market share gains in a number of sub-segments and geographies. We attribute its growth and market share gains to the following factors (which should all have forward influences):

- Health and Wellness Trends - Consumers are increasingly prioritizing health and wellness, driven by social pressures and increased awareness of health issues. MKC has adapted its offerings with reduced sodium, sugar, and artificial additives. Further, this has the potential to more broadly drive increased cooking and thus demand for spices.

- Changing Food Habits - Impacted by the pandemic, working from home, ease of access to recipes (YouTube, etc.), and the above point (among others), we are seeing greater interest in cooking, and global cuisines in particular. This will strongly underpin demand for spices and condiments.

- Global Expansion - MKC’s expansion into emerging markets, where the middle class is growing and consumer spending is increasing, has opened up new avenues for sales. As an example, the company is currently expanding its presence in Mexico to much success. Further, the company is also improving its distribution/channel approach to further gain market share, such as targeting the discount channels in the UK and France, again to success.

- Brand Building - MKC's consistent quality and innovation are underpinned by superior marketing and effective customer acquisition. Many of the segments it operates within are commoditized and so differentiation and justifications for premium pricing will come from its brand. Recently, the company has launched a Schwartz range in partnership with Nadiya Hussain, who is a celebrity chef in the UK. Although this sounds like just another campaign, we see this as a shrewd decision. Nadiya resonates extremely well with the working class in the UK, an untapped and under-targeted segment by premium brands. Other examples include holiday-based marketing, product line expansion, and greater merchandising.

Margins

{kind=link}

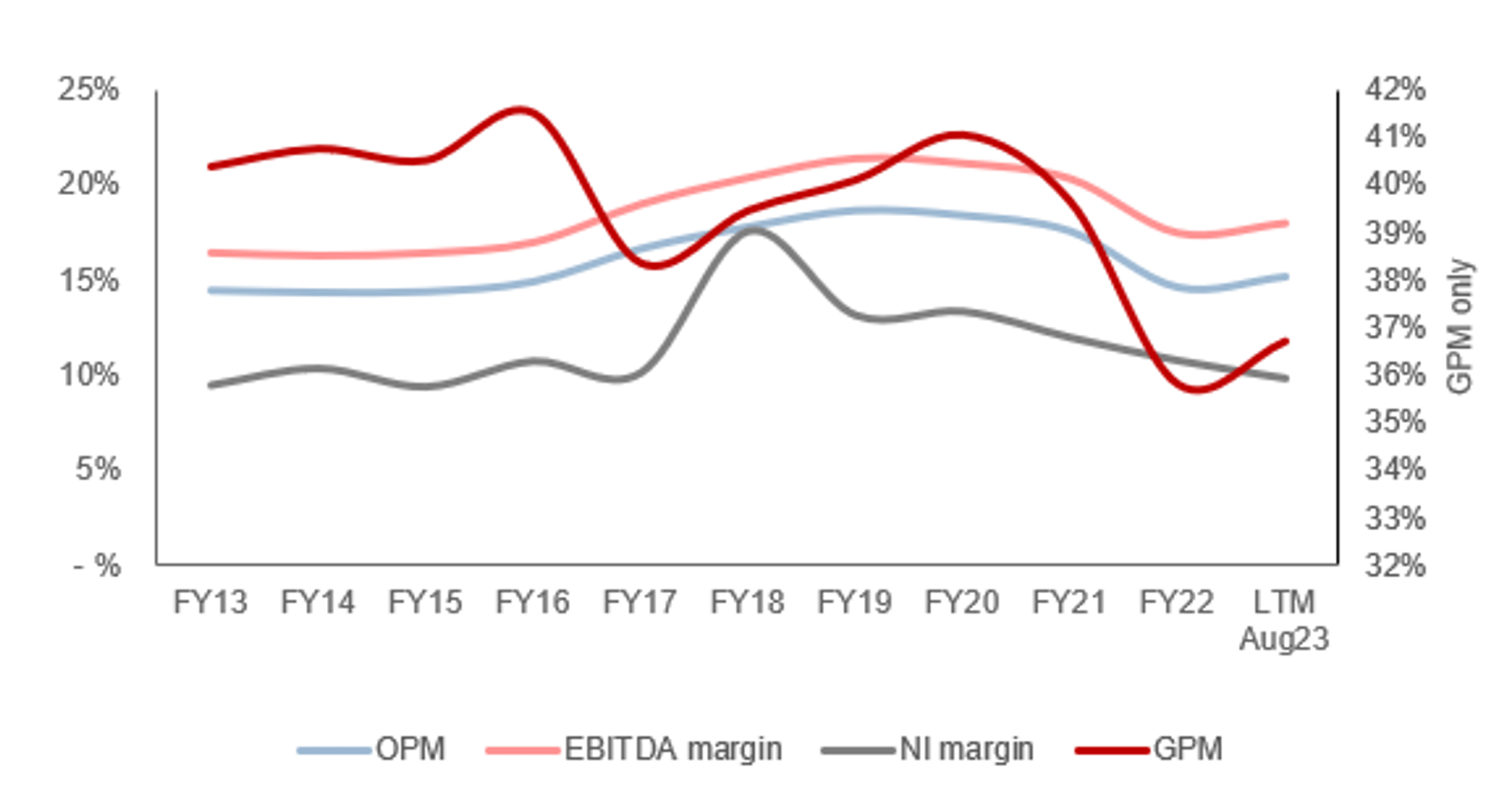

MKC’s margins had developed well during the last decade, with improvement principally at an operating cost level, with S&A spending declining as a % of revenue (-4ppts) offset by a decline in GPM. This is a reflection of operating cost leverage as the company has grown in scale globally, although competition and a degree of M&A dilution have contributed to the GPM slide.

Broadly, we are positive about the development of margins, although the post-FY22 performance has been poor. The company has seen a material decline in EBITDA-M, owing to the wider macroeconomic environment. MKC’s inability to offset this reflects a degree of cyclicality.

We suspect margins will normalize at their pre-pandemic level, although this will not be immediately won back.

Quarterly results

MKC’s performance has followed on from FY22 in its muted nature, with top-line revenue growth of (2.0)%, +2.8%, +8.0%, and +5.6% in its most recent four quarters. In conjunction with this, margins have improved and appear to have stabilized.

MKC’s weakness is a reflection of several wider factors, all of which are linked to the macroeconomic/geopolitical environment. The company chose to wholly exit Russia and divest its Kitchen Basics, contributing to a ~2% impact on revenue at the start of the year. Further, the business has seen weakness in China due to the impact of the various additional lockdowns in FY22, which is only now beginning to unwind. Finally, MKC is currently executing on operational improvements, including investment in sales staff compensation.

More overarchingly, the business is feeling the impact of economic conditions. With elevated inflation and interest rates, consumers are experiencing a squeeze on financials as living costs rise. This is contributing to greater hesitancy from retailers with stock levels, as well as many consumers trading down. Finally, this has contributed to supply chain issues, including rising disruption and labor costs.

Many of the issues MKC is facing have now subsided, with the biggest issue now being the economic environment. As a food business, the company benefits from inelasticity, and so the impact should be relatively less. This said, it should be appreciated that many of MKC’s products are “commoditized”, such as generic spices, and so the ease of trading down is higher. We suspect MKC can begin an upward trajectory from here, potentially having reached its “bottom”.

Key takeaways from its most recent quarter are:

- Sales growth of 6% reflects price realization following sub-par progress in FY22, as well as improvements in underlying volume.

- Management is seeing sustained demand and good progress toward its growth strategies across its Consumer and Flavor Solutions segments, reinforcing the strength of its competitive advantages.

- The only weakness experienced has been in its Consumer segment in APAC, where the pace of China's economic recovery has been slower than anticipated. Consideration must be given to whether this is the “new normal” for China, as Covid-19 can no longer be blamed.

- Further, margin improvement has been achieved through continued recovery of cost inflation, as well as cost savings from its various operational programs.

- Management has reaffirmed its sales and operating profit outlook, and also increased its adjusted EPS outlook.

Balance sheet & Cash Flows

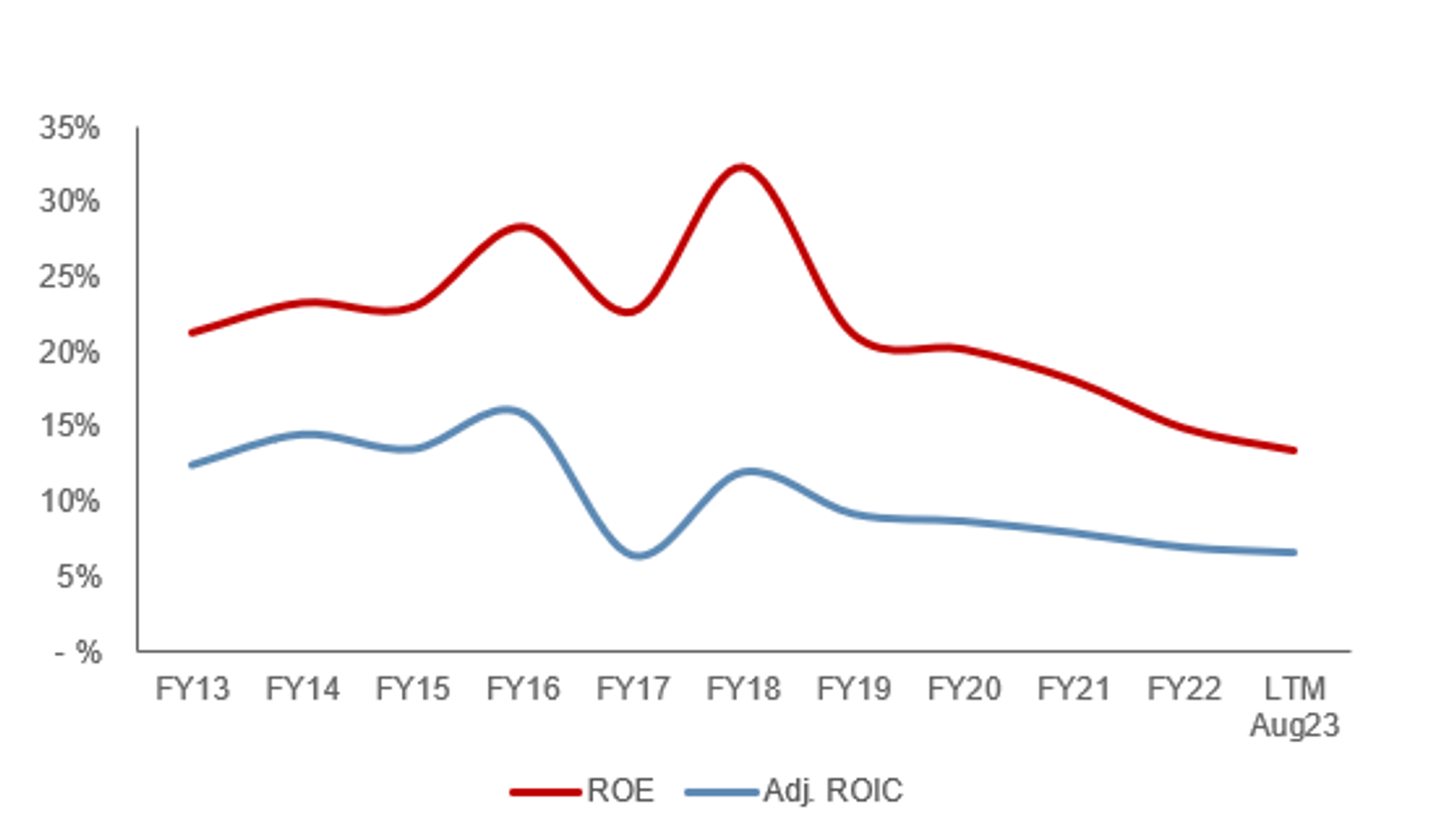

Management has aggressively allocated capital during the last decade. Debt has been laddered to fund distributions while maintaining its M&A strategy. At a ND/EBITDA ratio of 3.8x and interest comprising 3% of revenue, we consider the company at a reasonable maximum.

We are generally against the use of debt to fund distributions, particularly when it’s this aggressive, due to the risks associated with a change in environment. With rates rising and demand weakening, the company has been hit on two sides. The fear is that opportunities will potentially be missed due to financing constraints, as well as the potential for distributions to slow if growth cannot sufficiently bring its debt ratio down.

The company’s allocation of shareholder capital appears weaker in recent years. Margins have slid since FY18 and even once an upward trajectory returns sustainably, they may not necessarily immediately return to this level.

We would like to see a refocus on maximizing returns reducing the aggressiveness of capital allocation.

{kind=link}

Outlook

{kind=link}

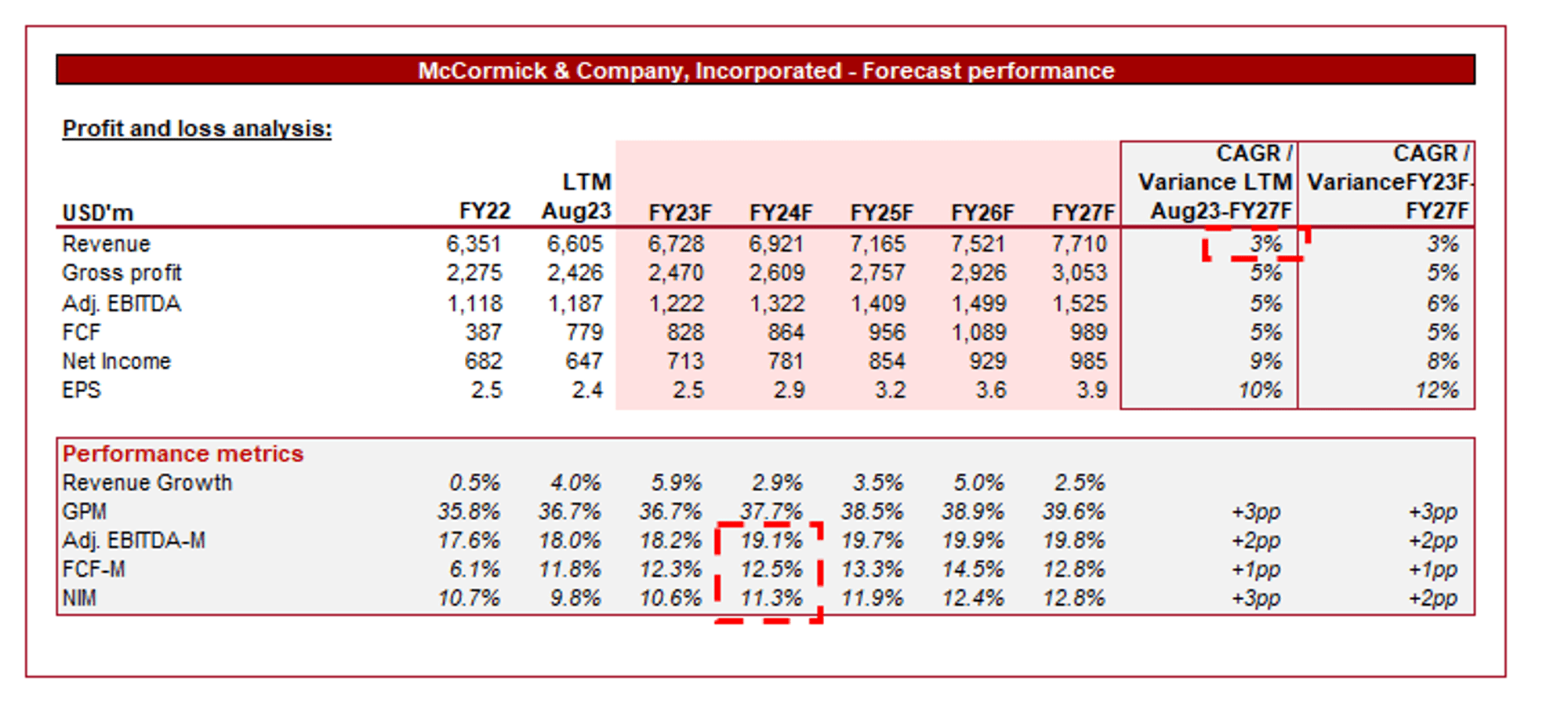

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a slight step-down in growth, with a CAGR of +3%. In conjunction with this, margins are expected to sequentially improve toward FY21/FY18 levels, although with a noticeably lower NIM.

We consider these assumptions to be broadly reasonable. With leverage constraints, the business will likely rely on organic top-line growth, which will begin to slow as inflationary price increases subside. As a mature business, LSD growth is expected. With the focus now switching to operational improvement, we see margin appreciation toward prior peak levels.

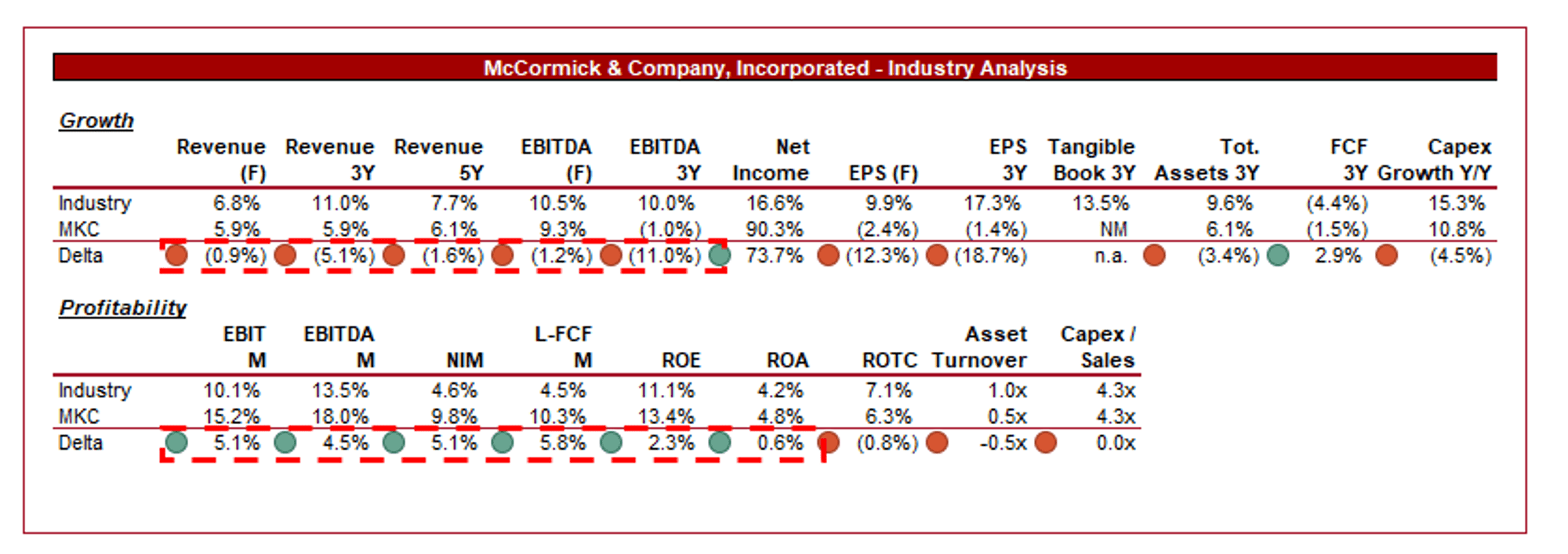

Industry analysis

{kind=link}

Presented above is a comparison of MKC's growth and profitability to the average of its industry, as defined by Seeking Alpha (41 companies).

MKC performs well relative to its peers. The company is lacking in revenue growth, although not materially so at a 5Y level. This is a reflection of its maturity and scale, restricting absolute gains relative to smaller peers. Assuming regular M&A returns in the coming years, we suspect MKC can broadly track its peers at a small delta.

The company’s strength is in its margins, with a significant delta to its peers and further room to improve in the coming 12-24 months. This is a reflection of its strong competitive position and scale, allowing for superior returns despite the growth delta.

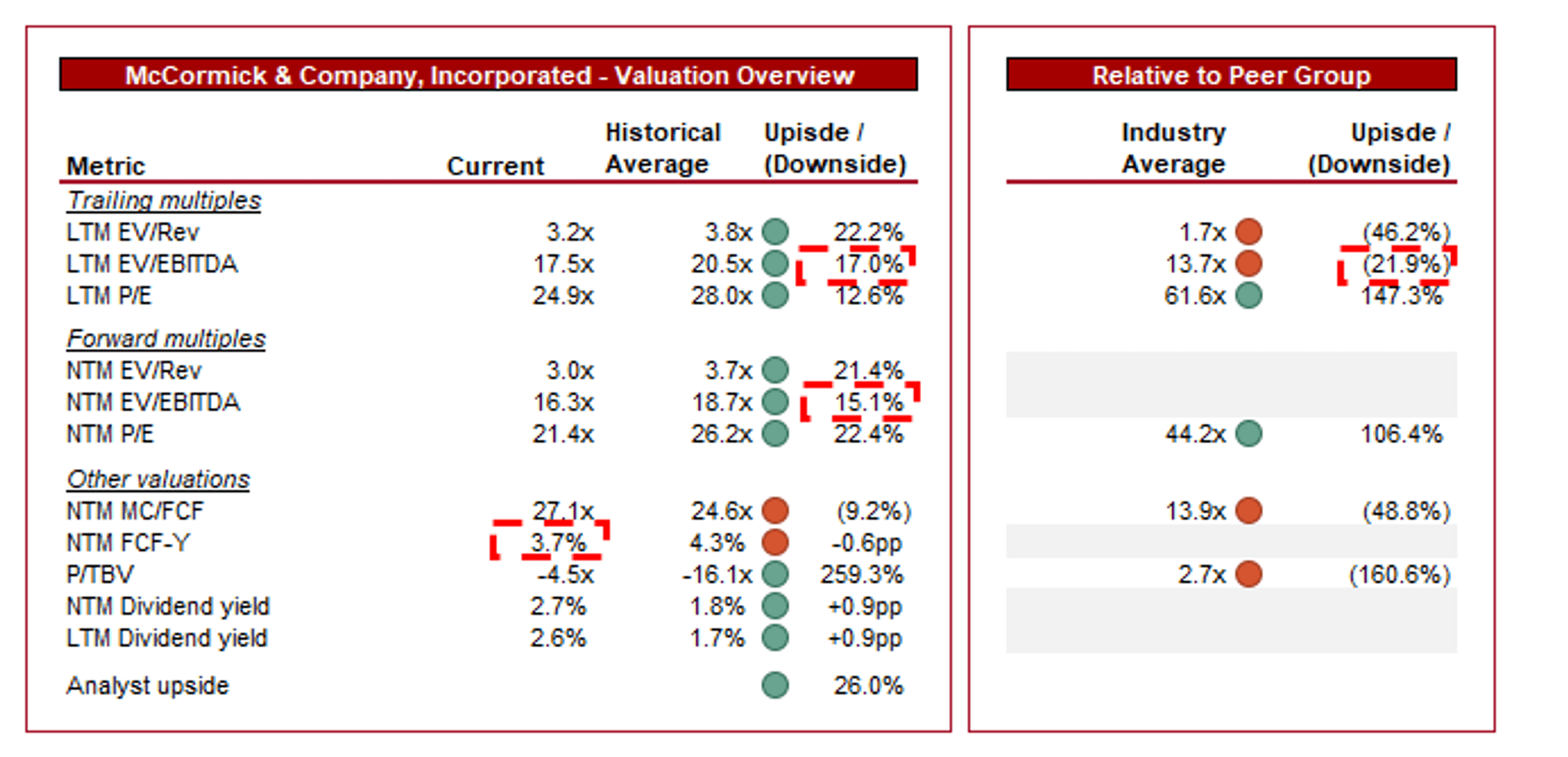

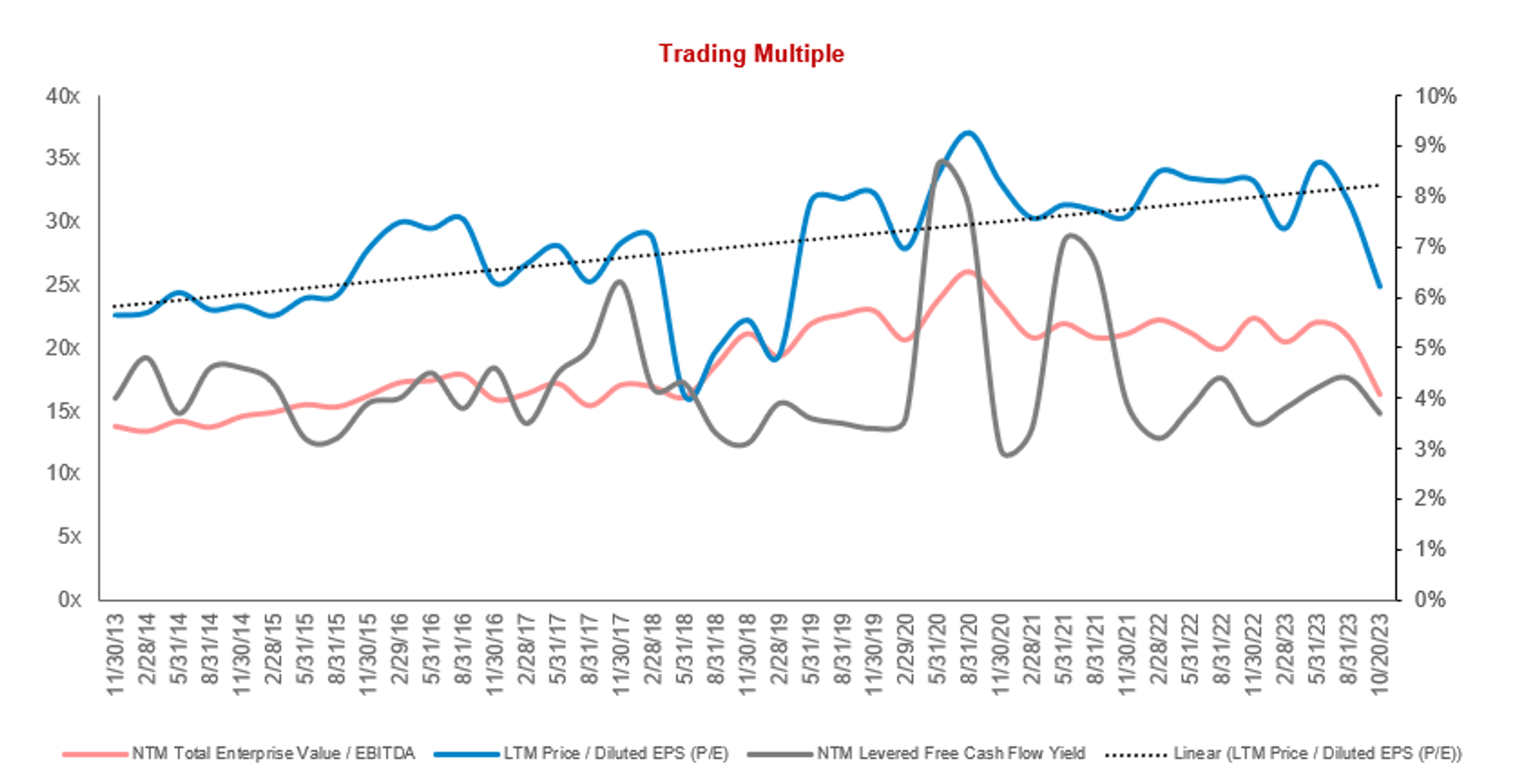

Valuation

{kind=link}

MKC is currently trading at 18x LTM EBITDA and 16x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, owing to the difficult capital position the business has found itself in (limiting M&A and rising interest expenses), limited margin improvement with scale, and near-term economic headwinds. This said, we believe the discount is likely too large given the reasonable visibility of margin improvement. This suggests small upside.

Further, MKC is trading at a ~22% premium to its peers on an LTM EBITDA basis and ~49% on a NTM FCF basis. This is warranted in our view due to the company’s superior financial performance, scope for additional growth, and competitive positioning. The size of the discounts appear reasonable given the scope for immediate margin improvement, although we see limited upside beyond this.

Based on this, we see a small upside in MKC’s current valuation. This is not sufficiently attractive in our view, however. As the following illustrates, its valuation has consistently grown during the last decade, only now falling to its ~2019 level. 2018-2019 was a strong period for the company and superior to its current iteration. Finally, its FCF yield is below its historical average (-0.6ppts) implying it is more expensive.

{kind=link}

Final thoughts

MKC is a quality business, owing to its strong brands and ability to execute on its growth mandates through a combination of organic and inorganic growth. We see strength in the industry to maintain good growth, although the near-term may represent a greater risk as inflationary price increases subside.

Our biggest issue with the company is Management’s aggressiveness with its capital allocation. It leaves the company in a (short) buffer period, where debt appears to be running away, restricting distributions and reinvestment in growth. When considering this alongside the wider macro environment (which could cause consumers to trade down), we think MKC could be dead money for a while.

For further details see:

McCormick & Company: Too Spicy, Currently On Financial Weakness