MKC - McCormick's Goodwill Has Started To Be Worrying

2023-11-20 09:54:14 ET

Summary

- McCormick's stock has dropped 30% from its 52-week highs, but caution is advised due to low revenue growth not justifying the 27.7x TTM P/E.

- The company's profitability has been declining over the past 5 years, with a significant decrease in gross margins.

- McCormick's high level of goodwill (66.3% of assets), combined with low revenue growth and declining profitability, raises serious concerns about potential impairments.

McCormick ( MKC ) stock has declined around 30% from 52-week highs but there is good reason for it and investors should be cautious. The company is not cheap enough to peak my interest as revenue growth has been only 4.3% over the past 5 years despite notable acquisitions. Furthermore, earnings growth has been negative over the period due to gross margins shrinking continuously from 43.8% in 2018 to 36.7% in the TTM period. This is a significant decline for what should be a consumer staple company with a mature business and great brands. Until I see this trend stabilize and show signs of reversing, I would be wary to be an investor in this company as it looks to be in decline and at risk from goodwill impairments.

Quick Intro to the Company

McCormick is a manufacturer, marketer, and distributor of seasoning mixes, condiments, and other flavorful products that dates back to 1889. Fun fact, which also speaks a bit to the barriers to entry and economic moat of the company, founder Willoughby McCormick started the company in the basement of a Baltimore home in 1889 going door-to-door selling the company's spices and extracts. The company now sells its products in over 170 countries and segments its business into two main segments; Consumer and Flavor Solutions. While the company's products might be by definition close to commodities, the company's scale, supplier relationships, and distribution network have allowed its products to earn a spot on major groceries' shelves and be the go-to supplier for food manufacturers and foodservice businesses.

Latest Quarterly Results

McCormick's latest results did show growth as sales increased 6% in the third quarter from the prior year period (same in constant currency terms) due to an 8% increase from pricing which was partially offset by a 2% volume and mix decline. GAAP EPS of $0.63 was down 23.2% compared to $0.82 in the prior year period with management's adjusted EPS of $0.65 down 5.8% compared to $0.69 last year. The TTM EPS of $2.40 leaves McCormick trading at an expensive 27.7x P/E.

Revenue Growth Breakdown (from company Q3 2023 investor presentation)

Operating income was 4% higher at $245 million in the third quarter compared to $235 million in the year-ago period with the all-important gross margin figure expanding 150 basis points to 37.0% driven by the previously mentioned price increases as well as some cost savings. Unfortunately, the gross margin expansion for the quarter was offset by higher SG&A expenses which increased $40.9 million (+12.5%) McCormick projects 2023 earnings per share to be in the range of $2.46 to $2.51, compared to $2.52 of earnings per share in 2022. At the mid-point of 2.48x, this would imply a forward P/E of 26.8x at the current market price of $66.36.

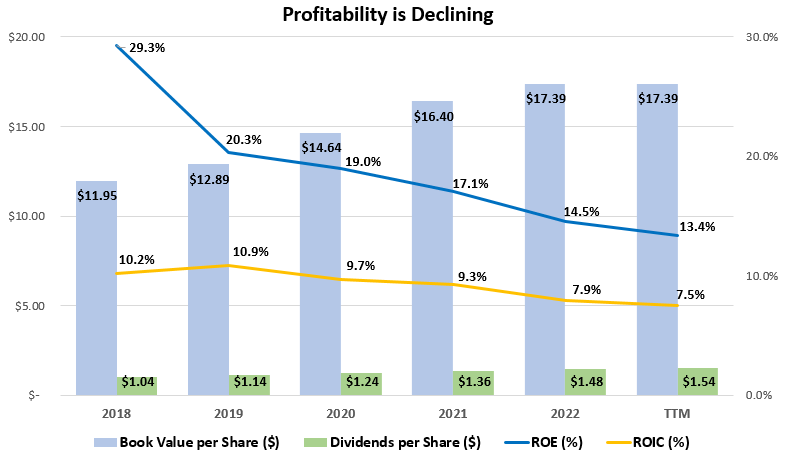

Declining Profitability is a Red Flag

Profitability at McCormick has been in decline over the last 5 years and is approaching levels that start to raise some red flags for me. Since 2018, return on equity and return on invested capital have averaged 18.9% and 9.3%, respectively. While these average levels are above my rule of thumb of 15% ROE and 9% ROIC, the continuous decline over the period has left the company only earning a 13.4% ROE and 7.5% ROIC in the latest TTM period.

Profitability and Growth at McCormick (compiled by author from company financials)

{kind=link}

These declines are not reminiscent of a company with a wide economic moat and something for investors to be wary of. Driving the decline in profitability has been a consistent fall in the all-important gross margin figure from 43.8% in 2018 to 36.7% in the TTM period. This large 7.1% decline in gross margins will be hard for McCormick to make up for with savings in operating expenses and the latest results don't show that happening. I would like to see this trend stabilize and reverse for a couple of years before I could get interested in the company, especially at the pricey 27.7x TTM P/E!

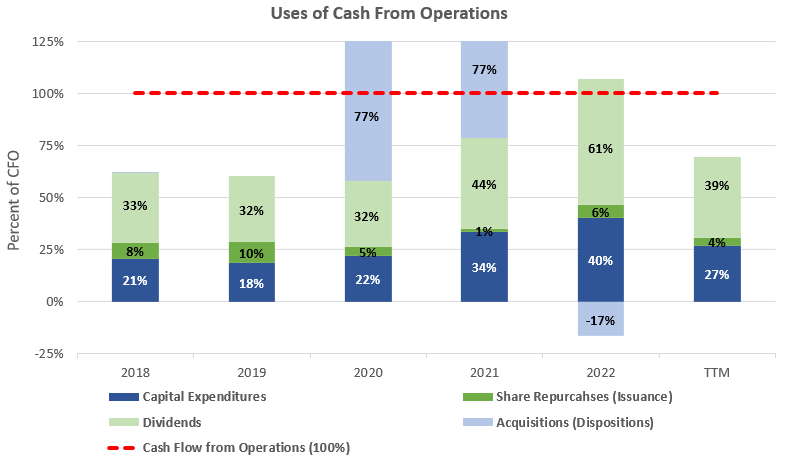

What About the Cash Flows?

Cash flows at McCormick are healthy with the company only spending 27% of cash flow from operations on capital expenditures over the past 5 years. This leaves a good amount of cash to be returned to investors in the form of dividends or share repurchases. However, the company has also regularly spent a considerable amount on acquisitions (approximately a net $1.3 billion) over the period which have averaged a further 23% of cash flows from operations. Notable acquisitions in the 5-year period include Cholula Hot Sauce (Mexican hot sauce company) in 2020 for $800 million and FONA in 2021 for $710 million.

Cash Flow Analysis of McCormick (compiled by author from company financials)

{kind=link}

This type of regular acquisition activity is okay if it leads to superb above-market growth, but McCormick's revenue growth has averaged only 4.3% annually over the 5-year period which is nothing to be too impressed by, especially considering the 27.7x P/E. In my experience, companies with a wide moat and great brands operating in an industry with high barriers to entry are more inclined to repurchase their own shares rather than admire and purchase other businesses. McCormick does not look to be this type of wide-moat business in my opinion as many of their products are commodities that are easily substituted for cheaper private label brands or newer fun brands and upstart local favorites.

With cash flow from operations being at $896 million over the past 3 years, the combined 50% spent on capital expenditures and acquisitions would imply free cash flow to shareholders of $430 million for around a 2.4% free cash flow yield at the current $17.8 billion market capitalization. Adding the 5-year revenue growth rate of 4.3% on top of this calculation would only bring expected long-term returns to 6.7%. This is not an impressive expected shareholder return in our current high interest rate environment.

A Worrying Amount of Goodwill

The acquisition spree of McCormick which started prior to the 5 year period touched on in this article has left the company with a worrying amount of goodwill on the balance sheet. One of the most notable acquisitions from the company over the past decade not yet discussed in this article was the large $4.2 billion acquisition of Reckitt Benckiser's food division back in 2017. This acquisition added notable brands of Frank's Red Hot and French's into the company's portfolio.

As of the latest Q3 financial statements, McCormick's balance sheet now has $5.3 billion of goodwill and $3.4 billion of intangible assets which represent 40.4% and 25.9%, respectively, of total assets. This large amount of goodwill and intangibles combined with the decline in profitably and low revenue growth over the past 5 years are worrying. I would expect to see some large impairments of the goodwill and intangible assets in the coming years as these acquisitions do not look to be justifying their purchase price.

Takeaway for Investors

McCormick shares might be down significantly from 52-week highs but there is good reason for that and investors should be cautious. The 7.1% decline in gross margins over the past 5 years will be hard for the company to compensate for through more efficient operations. Trading at a pricey 27.7x P/E, I would have expected more impressive revenue growth than the annual average of 4.3% over the past 5 years. With goodwill and intangibles representing a whopping 66.3% of total assets and profitability in decline, McCormick looks at serious risk of having to take impairments following their latest acquisition spree.

For further details see:

McCormick's Goodwill Has Started To Be Worrying