MKC - McCormick Stock: Not The Most Flavorful Prospect Out There

- McCormick & Company has fared quite well in recent years, but the company is currently experiencing a bit of weakness.

- Even so, management has positive expectations for the year, with sales and profits expected to rise year-over-year.

- Despite this, shares look a bit lofty and it's likely that investors can find better opportunities elsewhere at this time.

To the vast majority of people, flavor is incredibly important. Generally speaking, humans gravitate toward food that is pleasing to their palate. And while it may seem obvious for companies that focus on food production to emphasize making sure that food tastes as good as possible, there is one multi-billion-dollar company whose primary set of operations is organized around helping our food taste better. This household name is McCormick & Company ( MKC ). In recent years, the enterprise has done well to grow both its top and bottom lines.

It truly is a high-quality business in the food space and, in the long run, it's almost certain that investors will generate attractive returns. Having said that, there are two issues that are worth paying attention to. First, recent financial performance for the business has been somewhat disappointing. This comes as management has remained bullish about the 2022 fiscal year even as they reduced guidance. And second, shares of the company are trading at rather lofty levels. The first issue is largely transitory and, as a result, should not warrant the concern of investors all that much. But the second issue could result in subpar returns moving forward. Because of this latter issue, I have decided to rate the business a 'hold' for now.

Not so tasty

According to the management team at McCormick & Company, the company operates as a global leader in the flavor market. It does this by producing and selling spices, seasoning mixes, condiments, and other flavor-oriented products across the food spectrum. But to best understand the company, we would be wise to break it down into its two key operating segments. The first and largest of these is known as its Consumer segment. Through this, the company sells a variety of flavorful products, such as spices and seasonings, as well as condiments and sauces. In fact, two-thirds of the revenue associated with this segment comes from those four categories. The company also produces herbs, dessert items, and other related products. It offers these products through a variety of industry-leading brands, such as McCormick, French's, Frank's RedHot, Lawry's Club House, OLD BAY, Vahine, Kamis, Gourmet Garden, and more. These products are sold to a variety of retailers, distributors, wholesalers, and other parties, all across roughly 160 different countries and territories. During its 2021 fiscal year, this particular segment accounted for 62.3% of the company's revenue and for an impressive 73.1% of its profits.

The other segment is called Flavor Solutions. Through this segment, the company provides a variety of products to multinational food manufacturers and food service customers. To the food service customers, it offers branded, packaged products sold both by it directly and by distributors indirectly. The specific types of products sold through this segment include seasoning blends, spices, herbs, condiments, coating systems, and compound flavors. Last year, this segment was responsible for 37.7% of the company's revenue and for 26.9% of its profits.

There are some other important notes that investors should make. For instance, while the company is most certainly a global enterprise, it still is heavily reliant on the U.S. market. Last year, for instance, its domestic operations accounted for 60.4% of the company's revenue. This is roughly level with what the picture looked like two years earlier. A further 18.9% of sales came from a combination of Europe, the Middle East, and Africa, while all other countries combined made up 20.7% of sales.

{kind=link}

The general financial picture for the business has been quite robust in recent years. Revenue expanded constantly between 2017 and 2021, climbing from $4.73 billion to $6.32 billion. Growth was particularly strong between 2020 and 2021, coming in at 12.8%. This was driven by a variety of factors. For instance, for its legacy operations, volume and product mix changes pushed sales up by 5.5%. Despite inflationary concerns, pricing actions contributed just 0.8% to the company's top line growth. Foreign currency fluctuations accounted for 2.4%, while acquisitions accounted for 4.1%.

As revenue has risen, profitability has also increased. Although a bit lumpy, net income rose from $477.4 million in 2017 to $755.3 million in 2021. Other profitability metrics also were positive. Between 2017 and 2020, operating cash flow rose from $815.3 million to $1.04 billion. This metric did worsen in 2021, falling to $828.3 million. But if we adjust for changes in working capital, cash flow expansion between 2017 and 2020 would have been consistent, climbing from $655.1 million to $1.02 billion. Meanwhile, EBITDA for the company rose from $897 million to $1.28 billion.

{kind=link}

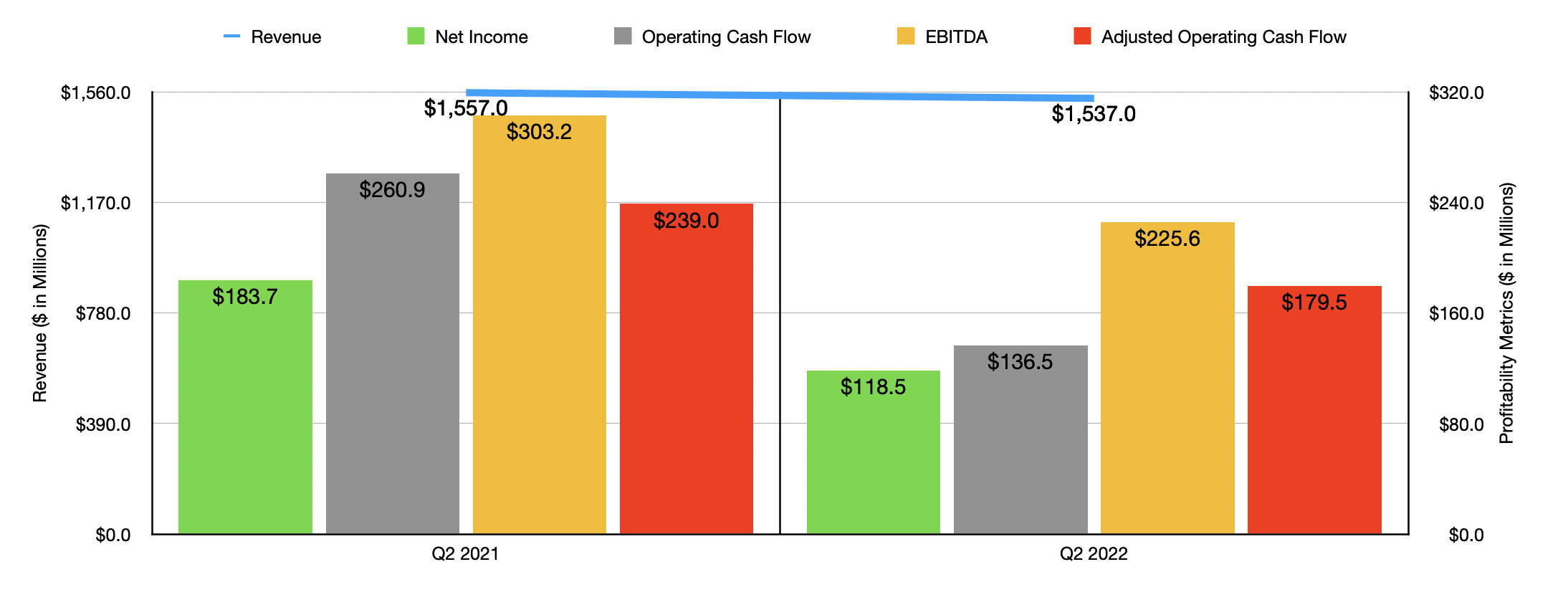

So far, the 2022 fiscal year is looking a bit mixed for the company. For the first half of the year as a whole, revenue of $3.06 billion does translate to a modest increase over the $3.04 billion reported the same time one year earlier. However, overall revenue in the second quarter was a bit weak, falling from $1.56 billion in 2021 to $1.54 billion this year. Not only that, management actually missed expectations on sales to the tune of $70.7 million. There were a number of contributors to this pain. For instance, volume and product mix changes impacted sales to the tune of 6.6%. The Consumer segment was the culprit, with some pain coming as a result of the war between Russia and Ukraine. Lower sales in China and India also impacted the company's operations. Meanwhile, pricing actions offset this, adding 6.8% to the company's revenue. But foreign currency fluctuations hit the business to the tune of 1.5%.

{kind=link}

When it comes to profitability, the picture for the first half of the year is not great. Net income fell from $345.5 million in the first half of 2021 to $273.4 million the same time this year. Net income in the latest quarter alone came in at $118.5 million. That's down from the $183.7 million reported just one year earlier. In addition to declining year over year, the company also missed expectations on its bottom line to the tune of $0.22 per share, with earnings ultimately totaling $0.44 per share. This first-half decline was driven in large part by a decline in the company's gross profit margin from 39.2% to 35.4%, with the second quarter proving particularly painful. The company attributed this to a couple of factors, including the margin dilutive impact of pricing actions the company took in response to inflationary pressures, as well as to increased commodity, packaging material, and transportation costs, amongst other things.

{kind=link}

Despite this pain, management seems to have high hopes for the company. They still believe that revenue will rise between 3% and 5% this year, with constant currency revenue climbing by between 5% and 7%. The total revenue expectation remains unchanged from the company's prior guidance. Management did ultimately reduce expectations for earnings per share for the entire year. Excluding integration costs associated with its aforementioned acquisitions, the company now anticipates earnings of between $3.03 and $3.08 per share. Prior guidance was for earnings to be between $3.17 and $3.22 per share.

{kind=link}

If management expectations for the current fiscal year hold true, the company should generate net profit, on an adjusted basis, of $819.6 million this year. If we assume that other profitability metrics match this year-over-year change, then adjusted operating cash flow should be around $1.10 billion, while EBITDA should come in at around $1.39 billion. Using this data, we can easily value the company. On a forward basis, the firm is trading at a price-to-earnings multiple of 27.1. This is down from the 29.4 multiple the company is trading for if we use our 2021 results. The price to adjusted operating cash flow multiple should drop from 21.8 to 20.1. And the EV to EBITDA multiple should decline from 21.2 to 19.6. As part of this analysis, I decided to compare the company to five similar firms. On a price-to-earnings basis, these companies range from a low of 16 to a high of 38.4. Four of the five companies were cheaper than McCormick & Company. Using the price to operating cash flow approach, the range was from 9.3 to 21.7. And using the EV to EBITDA approach, the range was from 11.8 to 19.2. In both of these cases, our prospect was the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| McCormick & Company |

| 29.4 |

| 21.8 |

| 21.2 |

| Kellogg Company ( K ) |

| 16.0 |

| 13.8 |

| 11.8 |

| Hormel Foods Corporation ( HRL ) |

| 27.6 |

| 21.7 |

| 19.2 |

| Conagra Foods ( CAG ) |

| 16.1 |

| 14.5 |

| 13.9 |

| The Kraft Heinz Company ( KHC ) |

| 38.4 |

| 9.3 |

| 13.8 |

| General Mills ( GIS ) |

| 17.1 |

| 13.9 |

| 13.6 |

Takeaway

Based on the data provided, McCormick & Company has a long history of attractive fundamental performance. Although we are currently hitting a soft spot and it's possible that management could be overestimating the company's ability to overcome that in the near term, the long-term outlook for the company is likely bright. For a quality operator, shares are still a bit lofty on an absolute basis. And relative to similar players, I would definitely call the company pricey. I don't think that long-term investors are at risk of a substantial decline in value in any way, but I do think that there is a meaningful risk of underperformance relative to the broader market. That is based less on the current fundamental weakness and more on the company's current pricing. And because of that, I have decided to rate the business a 'hold' for now.

For further details see:

McCormick Stock: Not The Most Flavorful Prospect Out There