MUX - McEwen Mining: Share Dilution And High Costs But Rising Gold Prices Could Raise Margins

Summary

- McEwen Mining has been struggling in the past year due to declining revenue, rising losses, and high production costs.

- McEwen Mining is facing a challenge in terms of profitability relative to peers, and it needs to become positive in its free cash flow to continue to grow.

- The solution to this challenge lies in a combination of rising gold prices and cost-efficient strategy development.

- They need to become positive in their free cash flow to continue their growth.

Investment Thesis

Despite a very problematic year due to the 1:10 stock split and disappointing revenue figures, McEwen Mining's ( MUX ) share price still managed to make a solid year-end rally, from its low of $2.81 to $7.33 - n increase of no less than 160% in less than five months. This was mainly due to the rally in the gold price because, fundamentally, things are not yet going well for McEwen Mining. It's currently down sharply again. But the future outlook, as well as the three price catalysts I will go into, could cause a strong turnaround at McEwen Mining.

Company Overview

McEwen Mining is a Canadian gold mining company with projects in North and South America. At the head of McEwen Mining is Rob McEwen, indeed one of the most well-known names in the gold mining industry. Mr. McEwen's ownership of 17% in McEwen Mining and 15% in McEwen Copper shows how committed management is and his interest in making McEwen Mining a top gold producer.

Over the past year, McEwen Mining stock has been plagued by a rash of problems and has massive issues in getting profitable. However, it has also demonstrated a strong track record of financial performance and growth.

Troubles in Paradise

The Reverse Stock split on July 28, 2022

You could argue that it is a good sign to do a reverse stock split in order to artificially push the price higher and make the stock more attractive, but in fact, it doesn't change the value of your investment. Although a stock split should increase the liquidity of the stock and make it, in fact, more affordable for investors, it does not take into account the underlying difficulties that the company may be facing. Still, in the case of McEwen, it obviously was a sign that they needed additional capital in the short term because they were struggling financially.

Declining revenue and rising losses

This is a really bad sign.

The revenue figures, of course, prove this:

{kind=link}

Revenue of $25.99 million in Q3 2022, down 15.2% from $31.13 million in Q3 2021. Revenue for all of 2021 was $136.54 million, a continuous increase in revenue since 2019. The revenue forecast for 2022 is at $124.15 according to figures on Seeking Alpha, which, compared to 2021, will still be a decrease of a good 9 percent.

Apart from the disappointing revenue figures, I would still like to draw attention to the loss figures. As shown in the table above, the gross loss has increased almost fivefold, from $344,000 in Q3 2021 to $1.5 million in Q3 2022. Once again, confirming that costs were huge, combined with decreased sales, a sledgehammer blow to profitability for McEwen. And the latter remains a huge problem for the company. Profitability relative to peers is a whole lot worse.

McEwen Mining vs. Peers (Seeking Alpha)

{kind=link}

So relatively speaking, McEwen is doing worse than the industry, but I need more than that sheer profitability. What does matter is the positive cash flows that come from these profits. This free cash flow was a loss of $15.09 million in Q3 of 2022. This loss has to become positive to continue to grow for the further development of the Los Azules project and debt repayment. So future positive cash flows are necessary for profitability and further growth of the company. I provide below what would be the drivers for this development and what for McEwen will drive the stock price up.

The Solution?

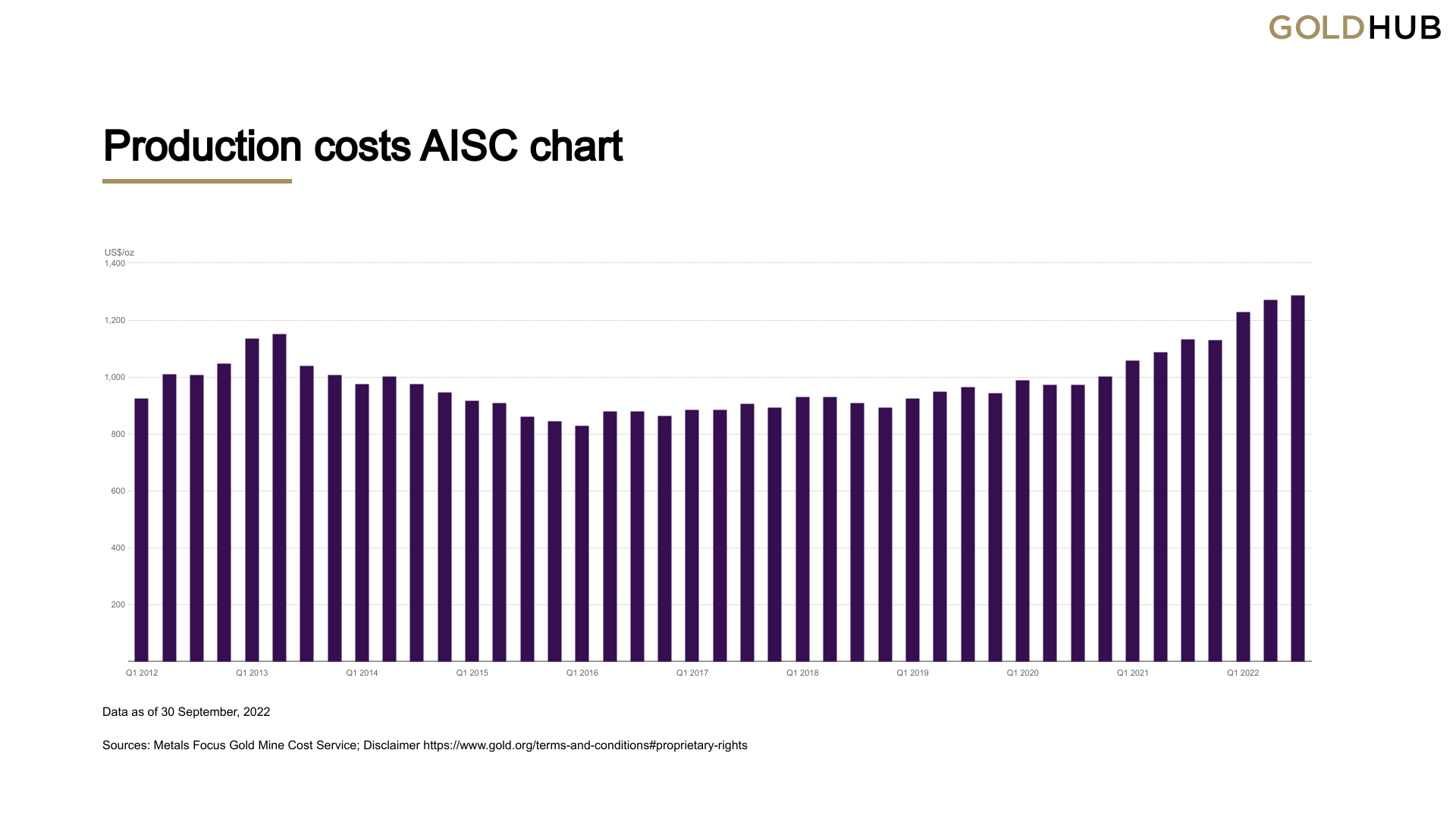

First, a rising gold price could increase margins. McEwen has a very high AISC compared to the industry. First, take a look at the chart below that shows the average AISC of gold miners.

Average AISC in the gold mining industry (Gold.org)

{kind=link}

This data is from Q3 2022. With an all-time high of US$1,289/oz.

McEwen is still well above this production cost, as much as $1,500/oz for its projects with 100% ownership. Even with high gold prices, McEwen continues to operate at high costs, so it will have to combine the two to see margins improve as effectively as possible.

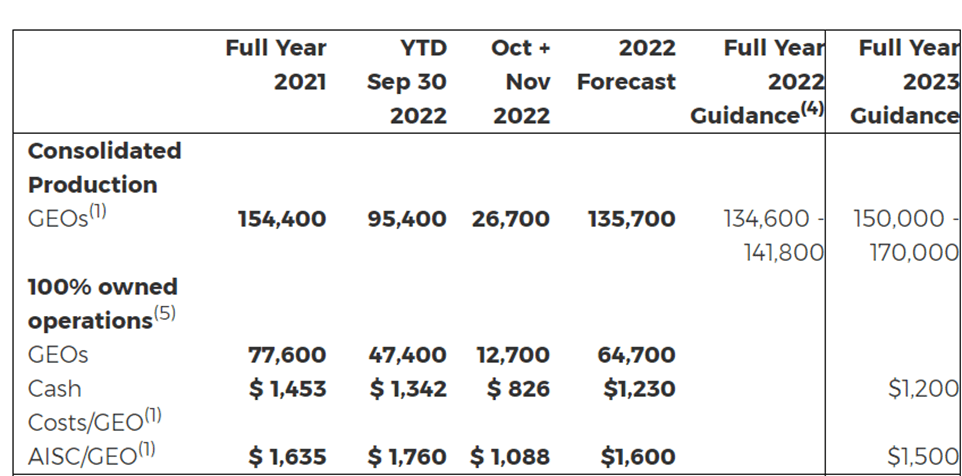

The initiative here should not be with rising gold prices but with McEwen itself to develop a more cost-efficient strategy. And there is a positive note here because, in a press release dated Dec. 21, 2022, they announced that production is up and cost per ounce is coming down. The table below from this press release shows once again the projected expenses for the past year and guidance for 2023.

McEwen Mining website mcewenmining.com

{kind=link}

AISC for the full of 2022 is estimated at $1,600/oz. 2023, on the other hand, they expect a decline to $1,500, as I mentioned above. So we already have a prospect of falling production costs, a macroeconomic consensus for rising gold prices , and hopefully a sustained increase in production. These three factors could be the catalyst for a rising long-term trend in the price of McEwen Mining.

Still Many Challenges Ahead

The private placement financing has brought in significant capital from big names in the copper sector, including Nuton, a Rio Tinto ( RIO ) venture, and they have entered into a collaboration agreement with McEwen Copper to advance the heap leach technology at Los Azules. But, of course, the cost of further development and exploration of the Los Azules project will also take a considerable amount of extra Capex.

Furthermore, the resolution of the critical issue of road access to Los Azules, which will now provide year-round work at the site, and the recent drilling results, which are expected to be used to update the 2017 PEA, will benefit the potential advancement of the project. McEwen Copper has excellent plans for the future, including completing an updated PEA, an initial public listing in the first half of 2023, and a feasibility study to be delivered in 2024. Access to the road at the Los Azules project was a very big problem until recently, and now that they have eliminated this, it is still a good sign that they can still overcome challenges. Not to deny that there will still be challenges to come, but this was a sign of strong cooperation and good work from management at McEwen.

Although fundamentally, it has very strong prospects, there is still the problem of financing. $2.4 billion must be raised to further develop the Los Azules project. Given high inflation, rising capital costs due to interest rates, and high production costs, this $2.4 billion is bound to be higher at present. Positive cash flows are obviously necessary, but with high inflation and rising interest rates, the likelihood of higher CAPEX and more difficult cost control is very likely. This will obviously offer risk for lower margins, which is the last thing McEwen needs.

Valuation

The number of shares is relatively low, which is indeed very positive for investors, but of course, this can be justified because of the 1:10 stock split.

McEwen has doubled in price since November last year, which is largely justifiable because of the considerable rise in the price of gold. The chart below shows the performance of McEwen mining vs. the gold price.

{kind=link}

Currently, gold still has downside risk, and would wait a bit longer to buy McEwen to potentially contain further losses. For a 12% rise in gold, McEwen did a surge of about 100%. That's pretty much a leverage of times 10.

Short-term, these price movements are irrelevant when looking at gold mining stocks for the longer term. That is also what I want to convey here: long-term opportunities in the gold sector.

So once again, everything in a nutshell: Rising gold prices and falling costs drive higher margins, resulting in a higher share price. Since we are mainly looking to the future again here, but McEwen is also already producing, I use the P/E and P/S ratios for my valuation.

EPS is around -0.20. With a share price of $6.05, we have a P/E ratio of -30.25 - negative in this case, which is obviously normal considering McEwen has been posting losses for the past year. With a company that still has a lot of growth ahead of it, the P/E is not a relevant indicator today.

The forward P/S ratio stands at 2.31, which is relatively high for the gold mining sector and therefore not very good. Compared to its peers, the median in the industry is 1.19. Typically, in the gold mining sector, P/S ratios range from 1 to 3, with a P/S ratio of 2.31 near the upper end of that range.

P/S Ratio McEwen Mining (Seeking Alpha)

{kind=link}

In terms of valuation today, McEwen is undoubtedly not that attractive. Still, the future for gold will also give its positives to gold mining companies and then McEwen will become a strong producer, in my opinion. I put it on a hold today and will wait and see.

Key Takeaways

McEwen Mining has faced several challenges in the past year, including declining revenue, rising losses, and a reverse stock split. Despite these issues, the company has demonstrated a strong financial track record and growth in the past. However, for continued growth and profitability, McEwen Mining needs to address its high costs and generate positive cash flows. This can be achieved by either a combination of a rising gold price and a cost-efficient strategy or by solely improving its cost structure. The recent press release from the company indicating an increase in production and a decrease in costs per ounce is a positive sign. With the expected decline in AISC for 2023, McEwen Mining is on the right path towards a more profitable future.

For further details see:

McEwen Mining: Share Dilution And High Costs, But Rising Gold Prices Could Raise Margins