MUX:CC - McEwen Mining: Zero Margin Of Safety At Current Levels

2023-04-04 09:39:16 ET

Summary

- McEwen Mining is one of the best-performing names in the Gold Miners Index over the past year, up 49% year-to-date and over 200% from its Q3 2022 lows.

- The outperformance can be attributed to the market finally beginning to value the stock on a sum-of-the-parts basis, and two large investments made in McEwen Copper (52% held by MUX).

- However, the performance of MUX's two managed operations continues to leave much to be desired, and San Jose (49% MUX ownership) has seen considerable margin compression since 2020.

- Given the positive news surrounding McEwen Copper has masked razor-thin margins at its existing operations, I see this near parabolic rally in the stock above US$8.90 as an opportunity to book more profits.

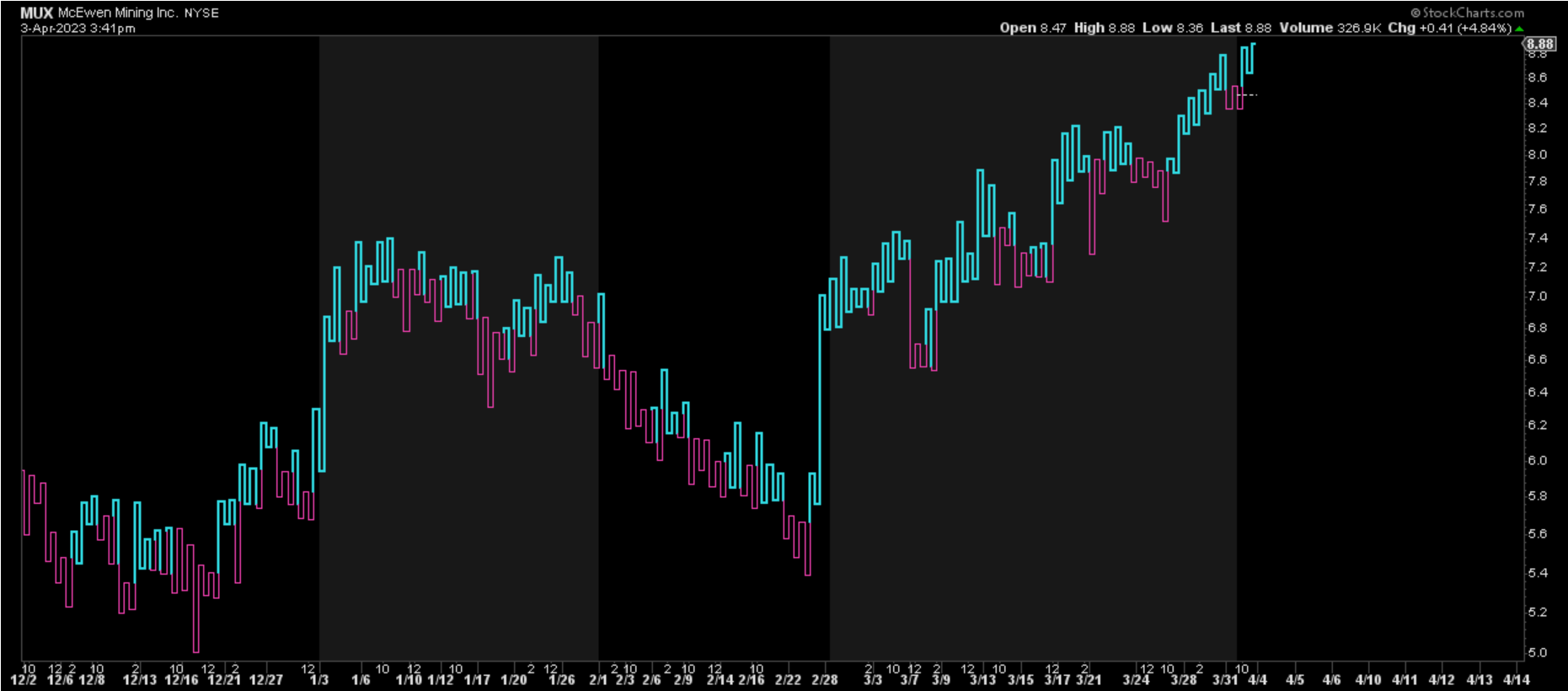

Three months ago, I wrote on McEwen Mining ( MUX ), noting that the stock was one of the best performing names in the market, but it was vulnerable to a correction and rallies above US$7.05 would provide an opportunity to book some profits. While the stock initially corrected sharply and fell ~27% from its January 9th high, it's since made new highs on the back of positive developments for McEwen Copper. For investors that missed it, McEwen Copper not only secured an investment (~$150 million) from Stellantis ( STLA ), a global automaker with brands that include Dodge, Jeep, Chrysler, Maserati, and Lancia, but it also received an additional investment by Nuton, a Rio Tinto ( RIO ) venture.

MUX 4-Month Chart (StockCharts.com)

{kind=link}

These recent investments in McEwen Copper (of which McEwen Mining holds 52%) have placed an implied value on McEwen Copper of ~$549 million, and have helped to clean up McEwen Mining's balance sheet, with the company planning to reduce its debt load with plans to retire its secured debt with Sprott Lending, reducing total debt by ~35% to just $40 million. In addition, this deal has increased the sum-of-the-parts valuation for McEwen Mining, with there clearly being large parties interested in the company's copper assets (Elder Creek, Los Azules). That said, and while this is positive, little has changed regarding MUX's gold/silver assets, which continue to be marginal. So, with the stock on a near-parabolic run and no longer valued attractively, I see this rally above US$8.90 as an opportunity to book more profits.

Q4 & FY2022 Results

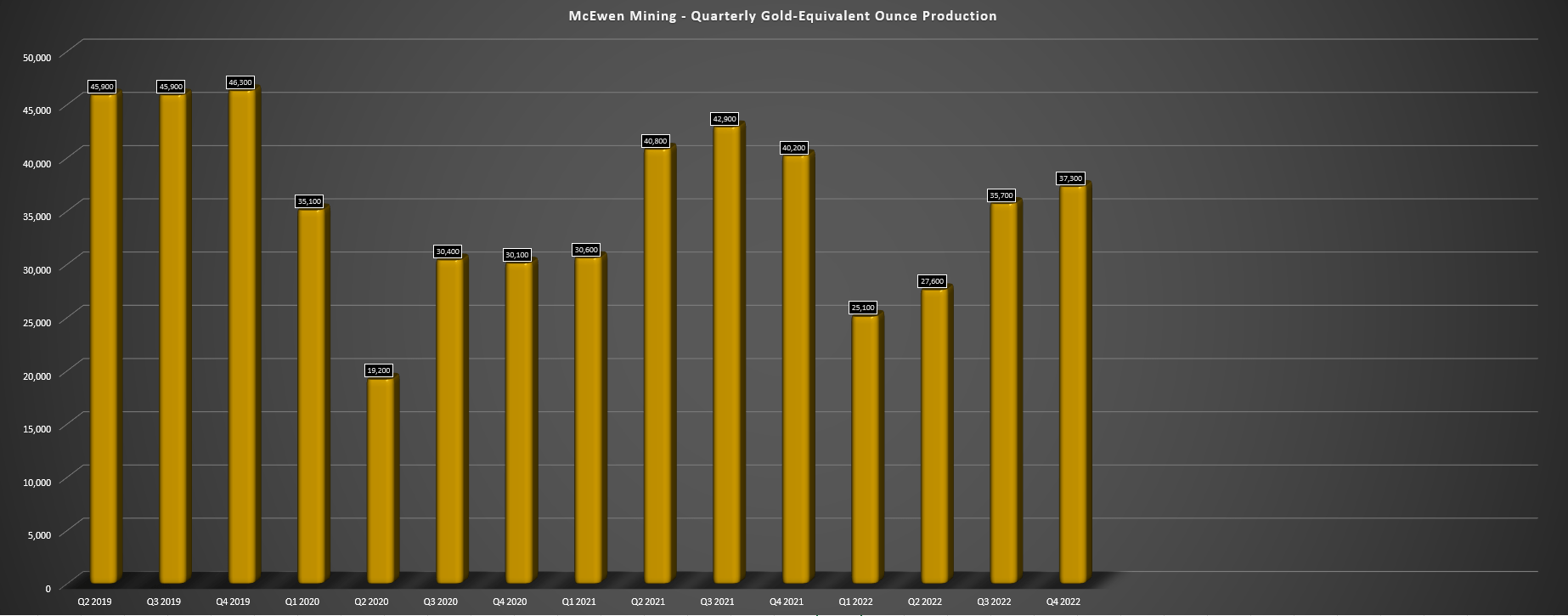

McEwen Mining released its Q4 and FY2022 results last month, reporting quarterly production of ~37,300 gold-equivalent ounces [GEOs] and annual production of ~133,300 GEOs. This translated to a 7% decline in production on a year-over-year basis in Q4 and a 13% decline on a year-over-year basis, as well as a massive miss vs. its initial FY2022 guidance of 153,000 to 172,000 GEOs. The 18% guidance miss vs. the guidance midpoint was related to a much weaker than planned year at its Gold Bar Mine in Nevada, which produced just ~26,600 GEOs, a massive miss vs. the 41,000 GEOs expected when the company provided guidance in March. Meanwhile, Black Fox also came up short of expectations, producing just ~36,700 GEOs vs. FY2022 guidance of 44,000 to 49,000 GEOs.

McEwen Mining - Quarterly GEO Production (Company Filings, Author's Chart)

{kind=link}

As discussed by the company in its Q2 results, the Gold Bar Mine's poor performance was partially because of running into carbonaceous material in H1 and lower than planned contract mining rates because of a staffing shortage. The result was that AISC soared to $1,989/oz for the year, resulting in margins deep in negative territory. Fortunately, mining has since moved to the Gold Bar South deposit. This deposit does not have carbonaceous ore (which is treated as waste) and benefits from higher grades and a lower strip. The result is that FY2023 production should come in at 45,000 GEOs (midpoint), a 60%+ increase from FY2022. That said, given McEwen Mining's history of meeting guidance, it's probably safer to rely on the low end of guidance, which is sitting at 42,000 GEOs for FY2023.

Black Fox Operations (Company Website)

{kind=link}

Moving over to Black Fox, it was a better year for the asset following the transition to mining at Froome, with ~419,000 tonnes mined at an average grade of 3.49 grams per tonne of gold. This was a significant increase from ~200,000 tonnes mined in FY2020 and ~307,000 tonnes mined in FY2021, with grades up just over 3% year-over-year and processed grades up 16% to 3.77 grams per tonne of gold. That said, while output was up on a year-over-year basis (~36,700 GEOs vs. ~30,000 GEOs), production was still below the initial FY2022 guidance of ~46,500 GEOs, with mill availability issues impacting throughput. The silver lining is that mining was on plan and the asset is sitting on a ~120,000 tonne stockpile to de-risk production in 2023.

Finally, at the company's minority owned San Jose Mine in Argentina, Hochschild Mining ( OTCQX:HCHDF ) had a tough year, with annual GEO production of ~69,100 GEOs, with a soft start to the year that wasn't able to be made up in H2. This resulted in a 10% decline in production year-over-year and a further increase in all-in sustaining costs [AISC] to $1,714/oz, up for another consecutive year vs. AISC of $1,603/oz per gold-equivalent ounce in FY2021. Unfortunately, 2023 is not expected to be a much better year for the asset, with FY2023 guidance of 70,000 GEOs at the midpoint. The result was a total gain of just $5.3 million in FY2022 from its share of San Jose and $0.3 million in dividends.

While this is one asset that at least is adding to McEwen Mining's bottom line, the issue I see is that San Jose is running low on reserves, with total reserves of ~1.53 million tonnes as of FY2022 compared to a throughput rate in FY2022 of ~500,000 tonnes per annum. This already points to barely a 3-year mine life, but it's important to note that Hochschild uses very ambitious metals prices to calculate its reserves, using an average gold price of $1,800/oz and an average silver price of $26.00/oz. So, I am not overly optimistic about this asset's future post-2026 unless we see higher metals prices, and especially if hyperinflation persists in Argentina.

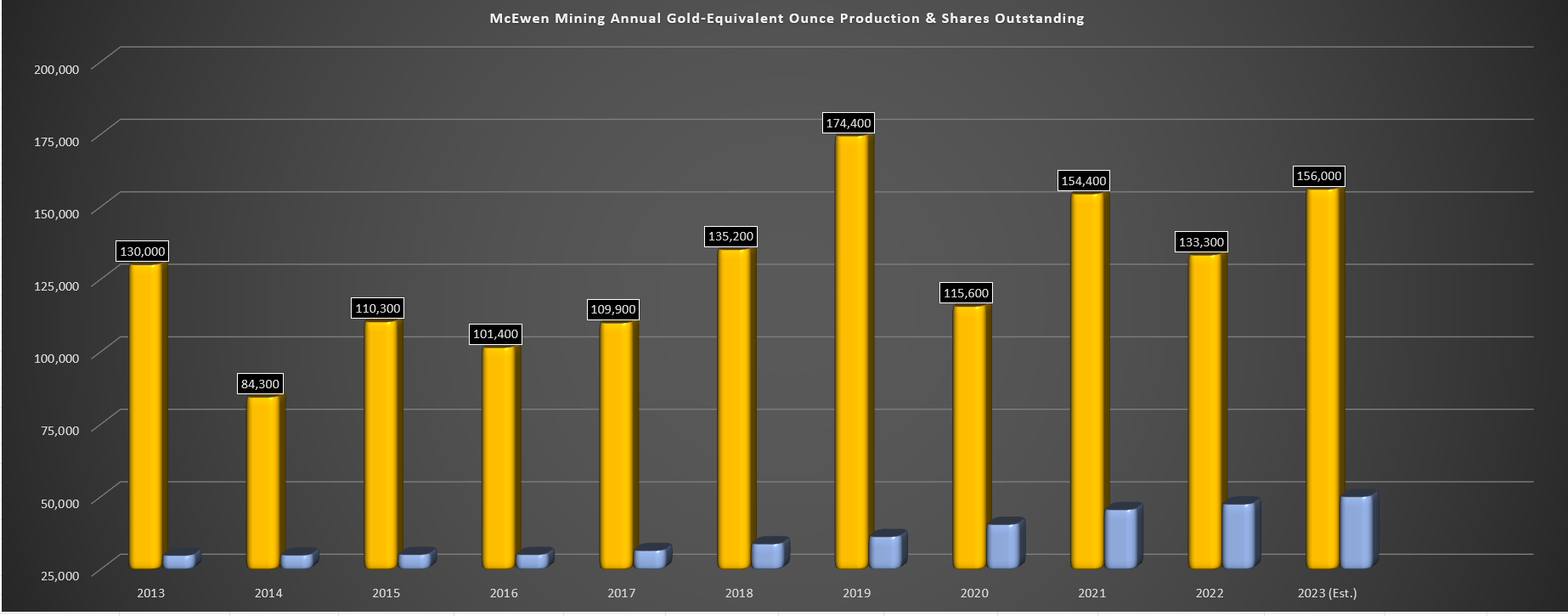

Putting it all together, McEwen Mining saw its annual GEO production decline sharply year-over-year, and it was flat vs. FY2018 levels. While this isn't the worst performance sector-wide as some companies like Great Panther ( OTC:GPLDF ) shuttered operations altogether, it is quite disappointing when we look at it on a per share basis, with MUX's share count up nearly 60% vs. FY2018 while production is down over 1%. The result is that because of considerable share dilution in the period, McEwen Mining investors are getting just 0.003 gold-equivalent ounces of annual production per share held, down from 0.004 gold-equivalent ounces four years ago, meaning their exposure to the metal is declining.

McEwen Mining - Annual GEO Production & Shares Outstanding (Company Filings, Author's Chart)

{kind=link}

If we look at this figure on a trailing-nine-year basis, the results are much worse, with production per share down over 60% in the period as production has been flat and the share count has increased approximately 65%. Plus, it's important to note that while the exposure to gold production has decreased materially, the current production profile is marginal from a profitability standpoint. So, even if production per share held has declined by ~60% over the past decade, the current operations leave much to be desired.

Costs & Margins

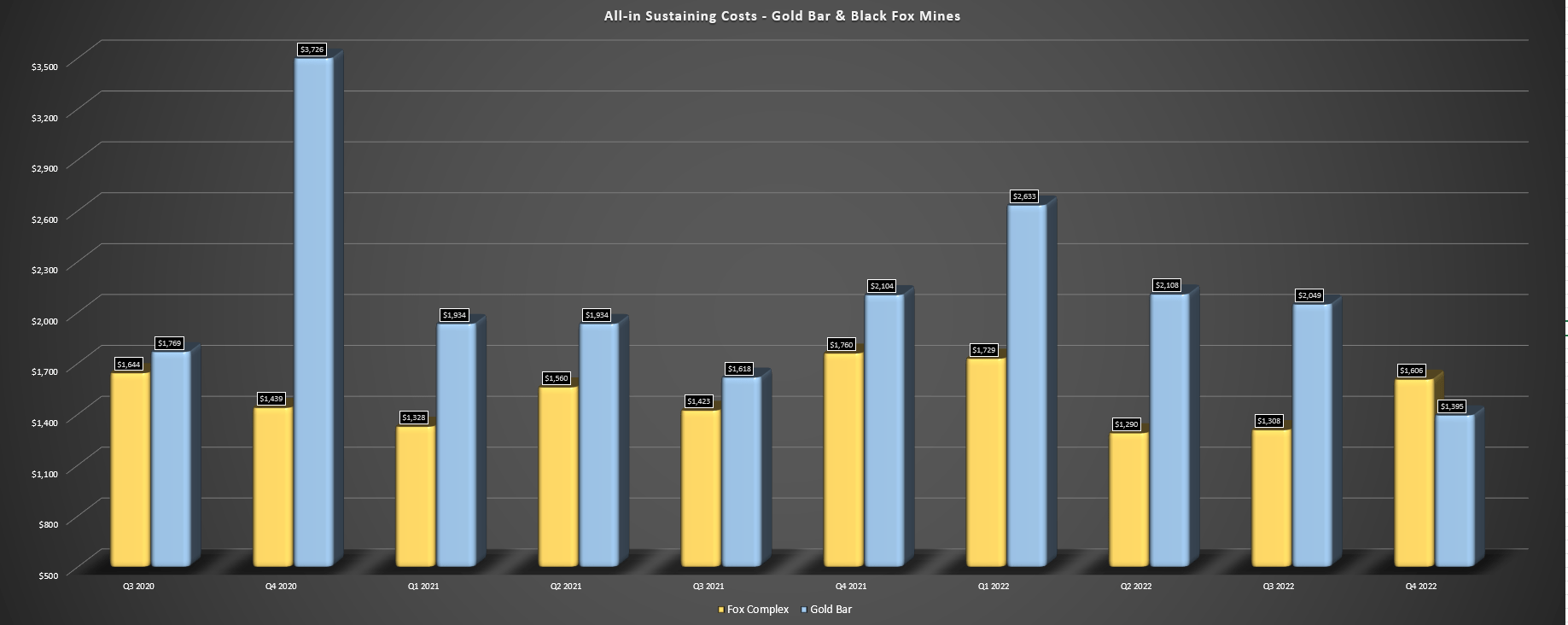

Digging into costs and margins, it was another horrendous year from a cost and margin standpoint, with Gold Bar's AISC coming in at $1,989/oz and Black Fox's AISC coming in at $1,465/oz. These represent some of the highest unit costs sector-wide, and this resulted in managed AISC of $1,688/oz in FY2022, a significant miss vs. the guidance mid-point of $1,630/oz provided in Q1 2022. Meanwhile, San Jose's costs weren't any better with all-in sustaining costs of $1,714/oz, translating to AISC margins of just $74/oz in FY2022, down from $257/oz in FY2020. This was despite a higher average realized gold price of $1,788/oz on a two-year basis, which was up 1% from $1,771/oz in FY2022.

Black Fox & Gold Bar Quarterly AISC (Company Filings, Author's Chart)

{kind=link}

Investors might take solace because the gold price looks to be bailing out these high-cost operations and McEwen Mining should see better cost performance in FY2023 because of higher production at Black Fox and Gold Bar. That said, on an all-in cost basis, these assets are still among the highest cost sector-wide and while McEwen Mining seems to believe it can double production at Froome at sub $1,250/oz AISC ( January 2022 PEA ), I am less confident in these figures. Not only do these figures not incorporate inflationary pressures over the past 15 months, but it's a Preliminary Economic Assessment, where assumptions are rarely tight enough. To summarize, I continue to be unimpressed with the portfolio and without a $2,000/oz gold price, it's hard to see this portfolio generating any meaningful free cash flow.

Recent Developments

Fortunately, McEwen Mining has a proverbial ace in its hole, a 52% ownership in McEwen Copper (100% ownership of Los Azules and Elder Creek) even after the recent investments by Nuton and Stellantis. These investments have put McEwen Mining in a position to pay down debt, reduce its interest costs, improve McEwen Mining's cash position, and they've also added value to the stock of a sum-of-the-parts basis. This is because the updated implied value of McEwen Copper based on recent investments is ~$549 million, placing McEwen Mining's 51.9% stake at a value of ~$285 million. In addition, the company is exploring a lower capex option for Los Azules, planning to forego a flotation concentrator that produces copper concentrate and instead looking at producing leachable copper in a heap leach with a solvent extraction/electrowinning facility to produce copper cathodes.

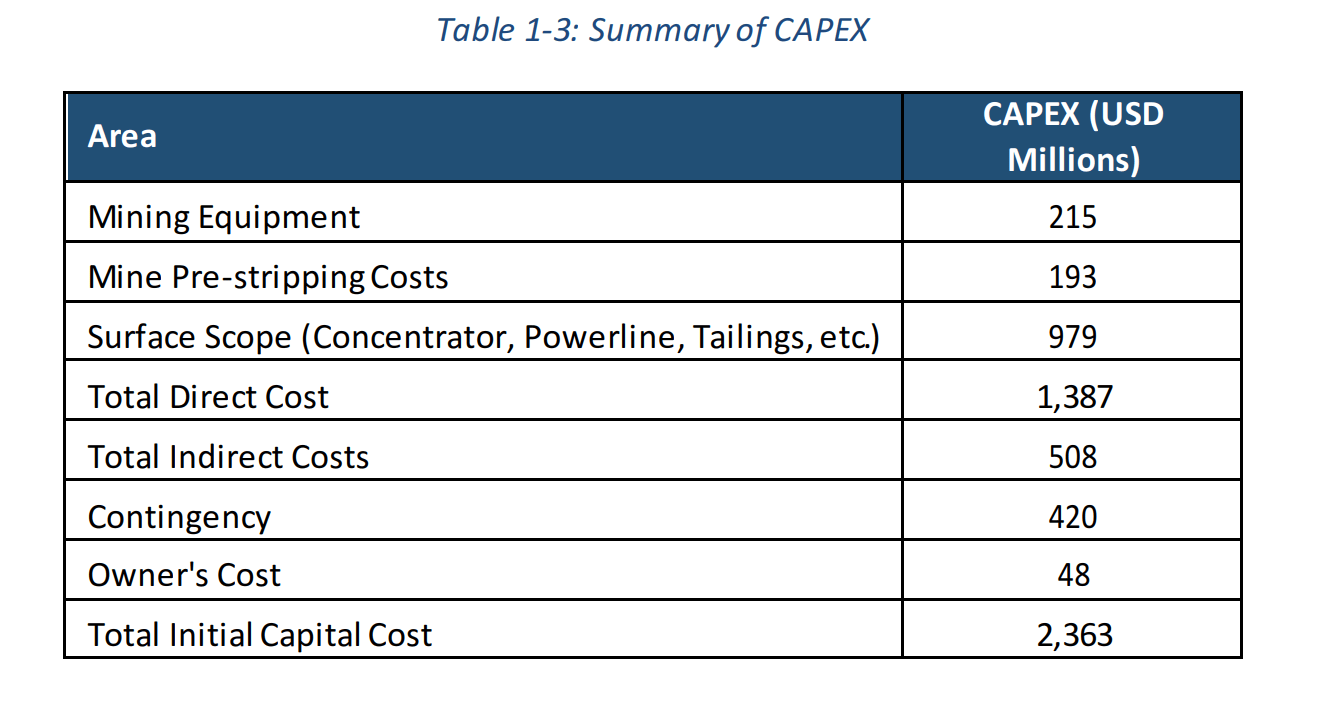

As it stood per the previous PEA, upfront capex was estimated at ~$2.36 billion (surface infrastructure at ~$980 million), a massive figure for a company with a sub $500 million market cap like McEwen Mining. Given that inflationary pressures have increased pre-2020 capex estimates significantly (over 80% with some projects), it was hard to be optimistic about McEwen Mining ever funding this asset. However, with the potential for a lower capex option, two partners in place that appear interested in helping to bring this asset into production and a much higher copper price, there might be a path forward for Los Azules. That said, this is still early days with a PEA expected this quarter that might give us a better idea on economics, the upfront capex bill, and a potential timeline if it's green-lighted.

Los Azules - Capex Estimate (2017 TR) (Company Filings)

{kind=link}

Overall, these are positive developments, and it's not overly surprising that McEwen Mining has risen from the dead following these developments. That said, little has changed with McEwen Mining's operating portfolio, and I remain pessimistic about the future of San Jose (49% interest) unless new discoveries are made soon. So, while we've certainly seen an upgrade to the investment thesis regarding McEwen Copper and McEwen Mining's 51.9% share, the outlook for its other three assets has arguably gotten worse after two years of double-digit inflation with assets lacking economies of scale and lower grades struggling to make the grade in this environment. And the recent spike above $80.00/barrel in the oil price doesn't help, especially for its low-grade assets in Nevada.

Plus, as we'll discuss below, much of this is now priced into the stock after a 210% rally.

Valuation & Technical Picture

McEwen Mining has ~51 million fully diluted shares and a share price of US$8.90, translating to a market cap of ~$454 million. If we value the company on a sum-of-the-parts-basis, it is still arguably slightly undervalued, with its stake in McEwen Copper worth ~$285 million, its royalty portfolio worth ~$40 million, and its gold/silver portfolio worth $200 million. This translates to a fair value of ~$525 million or US$10.30 per share, pointing to 15% upside from current levels. That said, this fair value makes some assumptions that I don't see as conservative.

While it's hard to dispute the value of McEwen Copper given recent investments and the royalty portfolio based on a 1.25% NSR on Los Azules and Elder Creek alone is easily worth $30 million, it's difficult to assign $200 million to an operating portfolio that struggles to generate any free cash flow. In fact, I would argue that Gold Bar isn't worth more than $20 million with all-in costs above $1,800/oz and an inability to generate free cash flow. Meanwhile, I would place a more conservative value for Black Fox at $120 million. Assuming we assign $40 million to San Jose because of its relatively short life (based on reserves), this reduces the value of its gold/silver portfolio to $180 million, reducing McEwen Mining's fair value under the same assumptions to $505 million or US$9.90 per share.

Finally, there's no guarantee that McEwen Mining doesn't raise capital this year to take advantage of its strong share price to drill its properties to increase reserves, which might increase the fully diluted share count to 55+ million shares. So, if we use a higher share count assumption to be on the safe side and the lower fair value assumption of $505 million (more conservative value on its gold/silver assets), fair value comes in at US$9.20 per share using the higher share count. Although this might still point to upside from current levels, I want a significant margin of safety when buying a small-cap producer, and especially one that's highly levered to the gold price with razor-thin AISC margins.

After applying a 50% discount to fair value (US$9.90) which is what I apply to all gold developers or sub $1.0 billion market cap producers, the ideal buy zone for MUX would come in at US$4.95, suggesting that there is no margin of safety baked in at current levels and the risk is to the downside if sentiment turns. So far, there's no reason to believe sentiment will turn and the relentless bid under is propping up many lower-quality names. However, a less robust PEA out of Los Azules, another high-cost quarter out of its operations, a capital raise, and or a reversal in metals prices could change sentiment quickly. In my experience, I prefer to sell into strength for this reason because the sector is full of negative surprises, especially when one invests in names that own lower-quality mines.

{kind=link}

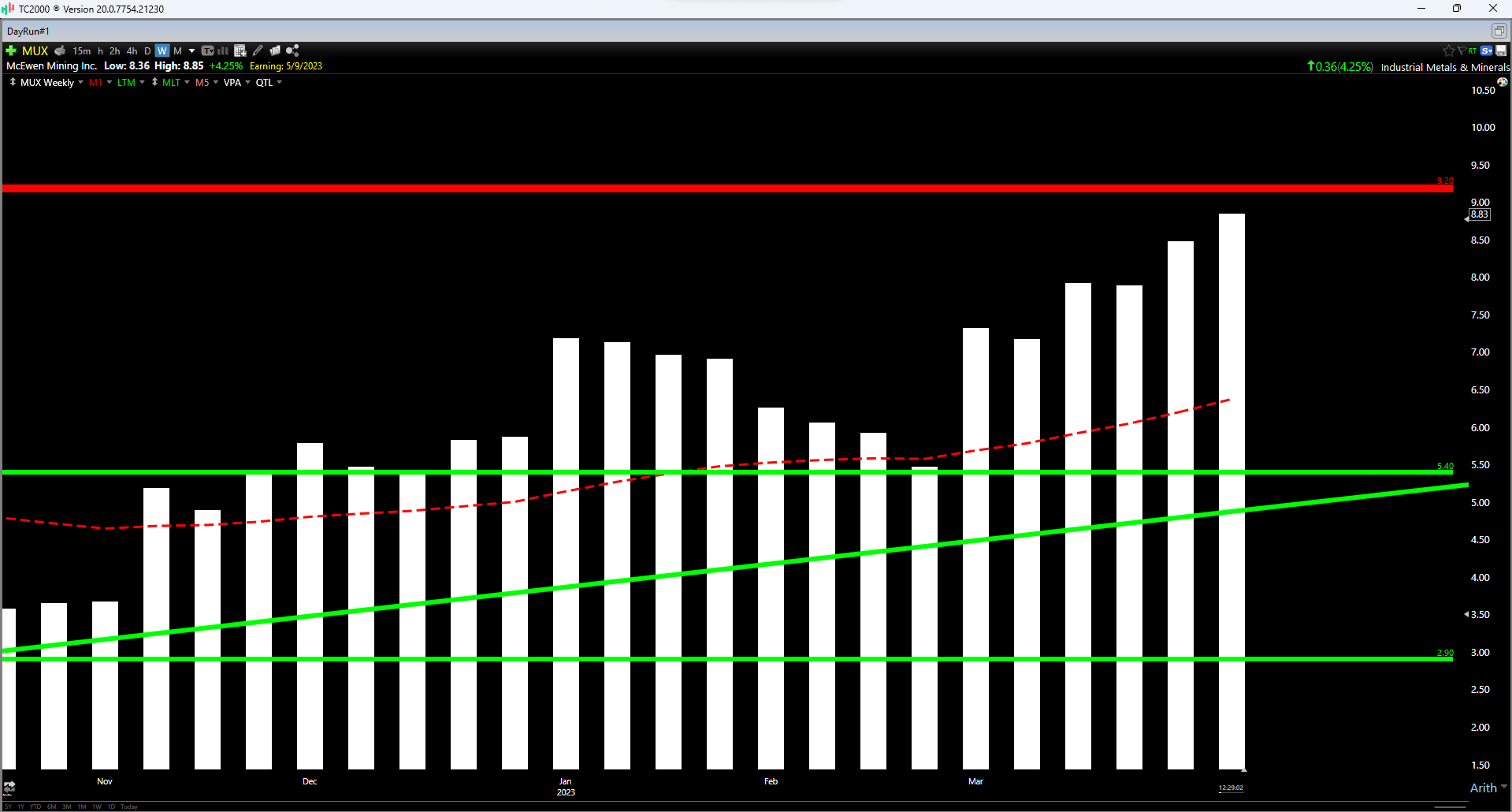

Finally, if look at the technical picture, McEwen Mining is back to trading in the upper portion of its support/resistance range, with no support until US$5.40 and resistance looming just overhead at US$9.20. If we measure from a current share price of US$8.80, this translates to a reward/risk ratio of just 0.12 to 1.0, with $0.40 in potential upside to resistance and $3.40 in potential downside to support. This confirms the view that McEwen Mining is nowhere near a low-risk buy zone when combined with a low-risk buy zone based on valuation of US$4.95 or lower, suggesting there is an elevated risk to starting new positions at current levels.

Summary

McEwen Mining has certainly exceeded my expectations with the copper side of the story finally coming alive, which has hidden what was another miserable year from a profitability standpoint in its managed gold portfolio. The evidence of this was company-wide AISC well above the industry average, a significant guidance miss vs. initial FY2022 guidance, and AISC near $2,000/oz at its Gold Bar Mine. The good news is that larger players are warming up to McEwen Copper and Los Azules, increasing the value of McEwen Mining's stake in the company and making the stock attractive to investors that want exposure to copper at a reasonable price given that it's packed in a portfolio with less desirable assets and in a company that's struggled to deliver on promises.

That said, the stock is now up over 210% from its lows, which has significantly increased the risk in owning the stock given that it's no longer attractively valued on a sum-of-parts basis. This is especially true if the Los Azules PEA comes in below market expectations or if Hochschild can't successfully replace reserves, which makes up much of the value in MUX's gold/silver portfolio. So, with MUX trading within ~10% of updated fair value, which incorporates the updated implied value of McEwen Copper and becoming overbought at US$8.85, I don't see any way to justify chasing the stock here. Instead, I see this near-parabolic rally as an opportunity to book more profits.

For further details see:

McEwen Mining: Zero Margin Of Safety At Current Levels