MGRC - McGrath RentCorp's Q2 Earnings: Promising Valuation And Growth

2023-07-28 12:05:02 ET

Summary

- McGrath RentCorp's Q2 earnings beat expectations, driven by strong performance in its Mobile Modular segment and contributions from the Vesta acquisition.

- The company experienced significant growth in total revenues and adjusted EBITDA, particularly in the Mobile Modular segment.

- Despite a decrease in adjusted EBITDA in the TRS-RenTelco segment and increased debt, McGrath RentCorp presents promising long-term growth opportunities and an attractive valuation.

Thesis

This article examines McGrath RentCorp's ( MGRC ) second quarter earnings for 2023, which showcased GAAP EPS of $1.14 that beat by $0.15, and revenue of $203.03M that beat by $8.45M primarily driven by its Mobile Modular segment and the contributions from the Vesta acquisition. Even with the soft performance of the TRS-RenTelco segment, the company presents promising long-term growth opportunities, robust historical growth rates, and a potentially attractive valuation, despite increased debt.

Company Overview

McGrath RentCorp is a business-to-business rental company that has a wide-ranging presence in both the United States and international markets. Their offerings encompass an assortment of rental and sales services, spanning modular buildings, portable storage containers, electronic test equipment, and liquid and solid containment tanks and boxes. The company efficiently operates through three distinct segments, each serving different needs.

The Mobile Modular segment specializes in renting and selling modular buildings and storage containers, catering to various applications. Meanwhile, TRS-RenTelco focuses on the rental and sale of electronic test equipment to industries like aerospace, defense, and semiconductor. Lastly, the Enviroplex segment is dedicated to manufacturing and selling portable classrooms specifically to educational institutions situated in California.

McGrath RentCorp's Q2 Earnings Highlights

McGrath RentCorp's second quarter financial results revealed a commendable performance, particularly in its Mobile Modular division. The company's total revenues experienced a 32% rise to land at $203 million, and its adjusted EBITDA grew by 34% to reach $77 million. Excluding Vesta's contributions, McGrath showed a growth of 13% in revenues and a 15% increase in adjusted EBITDA.

The Mobile Modular segment exhibited significant advancement, with a 59% increase in adjusted EBITDA to $56.8 million, and total revenues soared by 47% to $164.3 million. Across all revenue sources, the segment saw enhancements, with 21% total revenue growth and a 30% hike in adjusted EBITDA, when Vesta's contributions are discounted.

The Vesta acquisition, coupled with solid organic growth from the commercial, education, and portable storage sectors, contributed to a successful quarter. Particularly notable was the 59% increase in sales revenues to $39.4 million, indicating forward movement in modular sales projects.

There was also a 30% expansion in the average fleet size due to strategic investments in modulars and recent acquisitions, resulting in improved utilization. The company observed a 37% rise in rental revenues, signifying thriving market conditions and fruitful efforts in pricing optimization.

The TRS-RenTelco segment, on the other hand, experienced a minor decrease in adjusted EBITDA due to decreased demand in the semiconductor market. Rental revenues for the quarter dropped by 4%, while the average monthly rental rate saw a 3% increase, a reflection of stable pricing conditions and a shift in equipment mix.

The company has recalibrated its 2023 financial outlook, projecting stronger revenues from new modular sales projects. Expectations for rental operations remain steady, with a slightly softer outlook for the TRS division. Nevertheless, the company envisions potential long-term growth opportunities in its modular segment, powered by favorable pricing trends and contributions from the Mobile Modular Plus and site-related services initiatives.

Performance

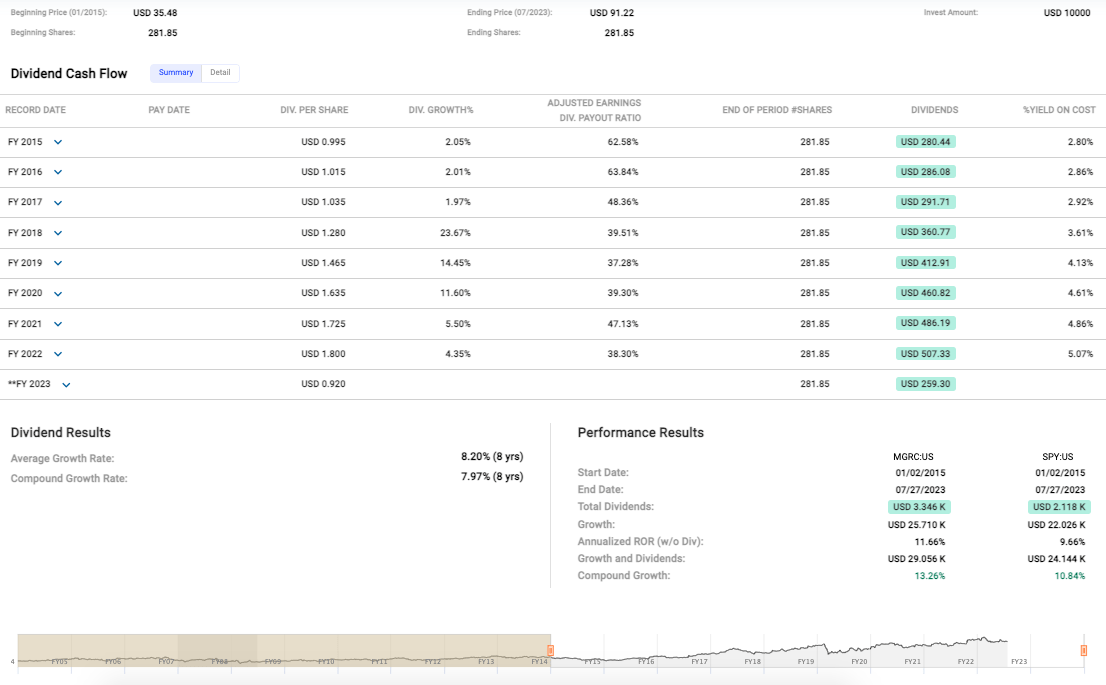

McGrath's share price appreciated in the medium-term from $35.48 in 2015 to $91.22 in 2023 - that's more than 150% growth over 8 years - signifying a compound growth rate of 13.26%. This easily outstrips the S&P 500 Index , which only managed to muster a compound growth rate of 10.84%. Investors in McGrath RentCorp would've been grinning from ear to ear with an annualized rate of return ((ROR)) of 11.66%, especially when you compare it to the S&P's humbler 9.66%.

{kind=link}

And regarding dividends, they've demonstrated a healthy average growth rate that stands at a commendable 8.20% over the illustrated 8-year period.

Valuation

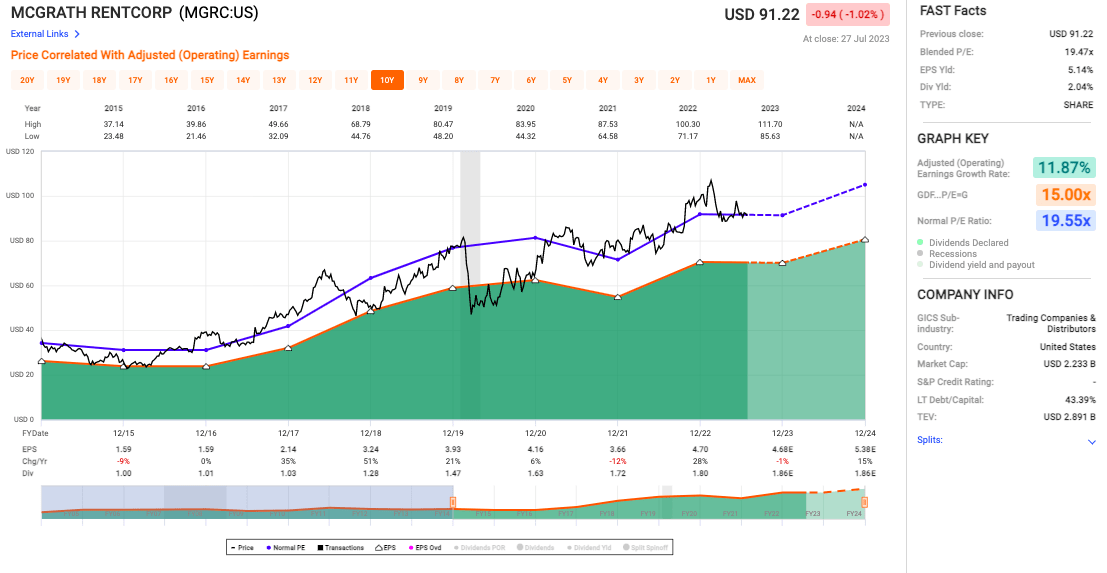

McGrath's blended Price-to-Earnings (P/E) ratio at 19.47x falls slightly below the normal P/E ratio of 19.55x (see chart below), suggesting that the shares might currently be slightly undervalued, offering potential investors an attractive entry point.

{kind=link}

And looking at the Earnings Per Share ((EPS)) Yield of 5.14%, this number shows that the company's profitability relative to its share price is healthy. This complements the steady Adjusted Earnings Growth Rate of 11.87%, which demonstrates a consistent trend of revenue growth.

Risks & Headwinds

A closer examination of the factors at play uncovers a prominent trend: a perceptible softness in demand within the semiconductor sector. This dwindling interest directly impacted general-purpose rentals throughout the quarter, signaling a decreased reliance on or need for these rental services.

Interestingly, the average utilization for the quarter revealed another significant downward shift, receding to 58.2% from a more robust 64.5% the previous year. The softer demand from the semiconductor market was a key contributor to this drop. Adding to the complexity of the situation, extended supply lead times for new equipment further disrupted the usual flow of business operations.

When examining the company's cash flow, a lower volume of net cash provided by operating activities was noted in comparison to the previous year. This reduction can largely be attributed to transaction expenses incurred from recent acquisitions, which have inevitably placed a strain on the company's cash reserves.

Lastly, at the end of this financial period, the company had net borrowings amounting to a significant $673 million. This figure flags an increased level of debt, potentially escalating the company's financial risk and reinforcing the importance of strategic debt management in its future endeavors.

Final Takeaway

Based on the data, I would rate McGrath RentCorp's stock a "Buy." The company showed strong Q2 performance with significant revenue and adjusted EBITDA growth, particularly in its Mobile Modular segment, even excluding Vesta's contributions. And despite minor setbacks in the TRS-RenTelco segment and increased debt, the overall financial health and promising growth trajectory, supported by attractive valuation and robust historical growth rates, justify a "Buy" rating.

For further details see:

McGrath RentCorp's Q2 Earnings: Promising Valuation And Growth