MCI - MCI: A Strong Outperformer But Less Known

2023-06-03 03:20:09 ET

Summary

- Barings Corporate Investors is a lesser-known fund with a strong track record since the 1970s, consistently outperforming the overall markets.

- The fund invests in high-yield corporate debt, preferred stock, warrants, and conversion rights from private companies, and currently trades at a -17% discount against its NAV.

- Despite its impressive history, the fund carries risks due to its investments in "junk" bonds and low liquidity, making it suitable for a small portion of a diversified portfolio.

What if I told you that there is a fund that has been around since the 1970s and consistently outperformed the overall markets but not many people even heard of it. I am talking about Barings Corporate Investors (MCI) which has a very impressive track record but is mostly unheard of (even at Seeking Alpha, this fund has only 1.63k followers).

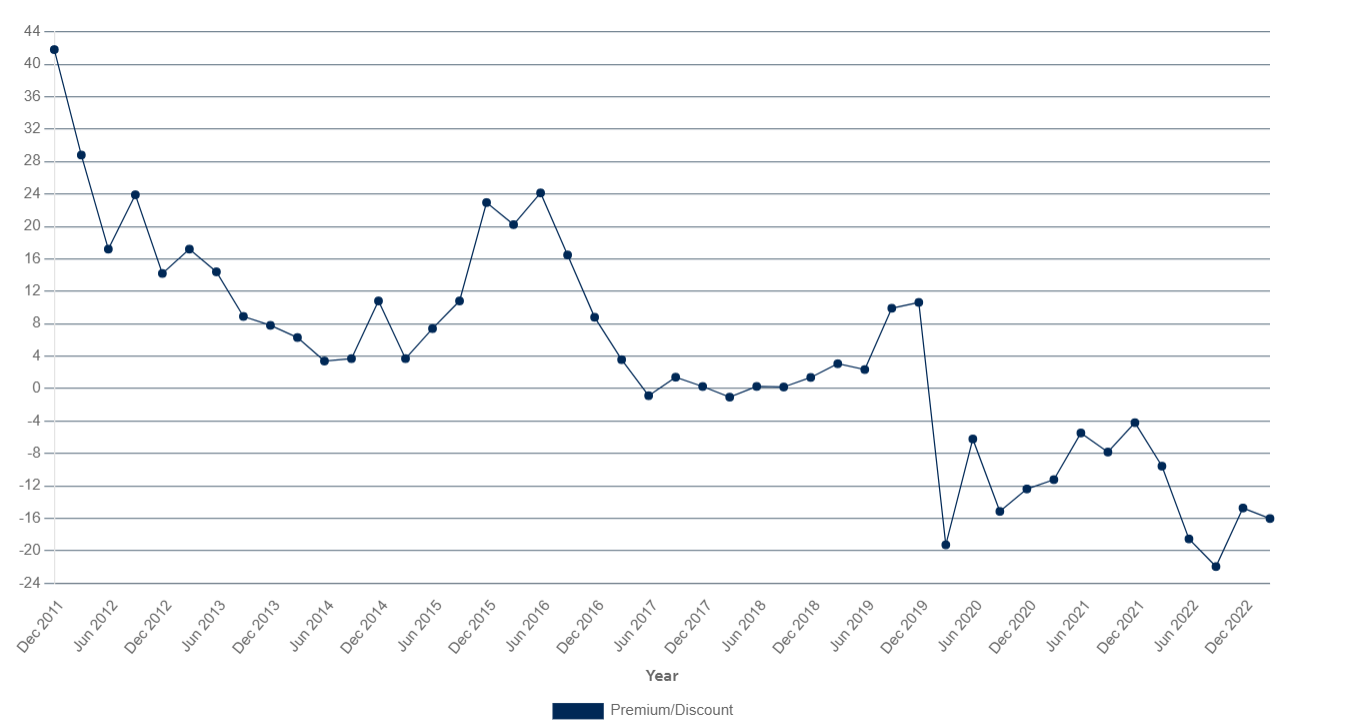

To make the matters even more interesting, the fund currently trades at a -17% discount against its NAV when it had historically almost always traded at a premium. In the last 14 years, the fund has never traded at as deep a discount as it is right now.

{kind=link}

So, what does this fund do that allows it to have such a great performance. It mostly invests in high yield corporate debt, preferred stock, warrants and conversion rights from private companies. This sounds very risky, but the fund has been around for quite a while, and it performed just fine and survived the Great Financial Crisis of 2008-2009 as well as the shutdown crisis of 2020 which hit small companies particularly hard.

The fund distributes virtually 100% of its earnings to investors in dividends each year on quarterly basis. Historically the fund's dividends fluctuated quite a bit but mostly landed somewhere between 20 cents and 40 cents per share, averaging around 30 cents per quarter which means its annual dividends typically fluctuated between 80 cents and $1.60. I could find only a few instances since 1970s that the fund has skipped a quarterly dividend payment which is a huge plus.

Since the fund holds debt and other instruments from private companies that don't trade publicly, it is difficult to calculate the exact value of its holdings. The fund's management provides an estimate of their NAV in each quarter but investors don't have a way to fully verify this. Investors simply need to have faith in management in calculating the fund's value and I would give them the benefit of doubt considering their long track record of outperformance.

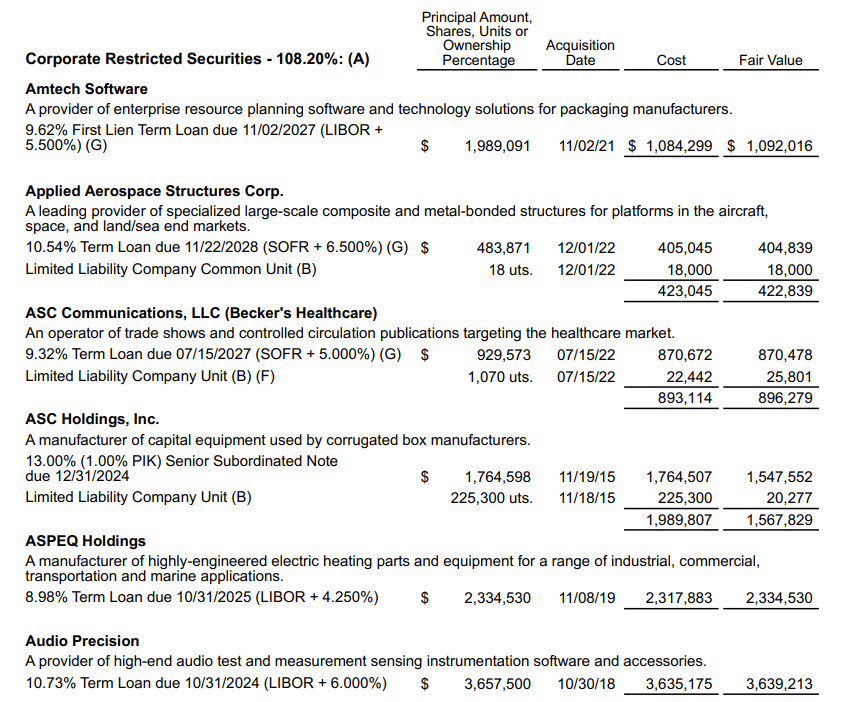

To be fair, the company's annual reports typically list all the companies it holds assets in including a brief description of each company and estimated value of the fund's investment in each company. For example, below image is from last year's annual report :

{kind=link}

Notice that the fund provides line by line items of every asset it holds including the name of the company, description of what that company does, what their loan terms are, acquisition date of each loan, their cost and fair value as well as whether the fund holds any ownership interests in each company apart from debt. At the end of each quarter, the fund also informs investors if it entered into any new positions or if it exited any positions.

Another interesting observation from the list of fund's assets is the fact that a great majority of the debt held by the fund is at floating rate. Only about a quarter of the debt invested by the fund is fixed rate. Many of them actually have rates 3-6% above the rate of LIBOR. As inflation causes rates to rise, this actually benefits the fund but it can also easily backfire if companies have trouble servicing their debt and start defaulting. You want your debt-based fund to enjoy high rates to a point but as soon as they become too high, they pose as much risk as benefit if not more because the risk of default rises exponentially. Currently corporate default rates are historically low even with interest rates rising from 0% to 5% in less than one year but there is no guarantee that this will continue. Sometimes these things happen suddenly and in chain reaction where you see clusters of defaults one after another, so it's impossible to guess what the future looks like in terms of corporate defaults, but there is reason to be cautiously optimistic.

Many of the instruments and assets invested by the fund are not very liquid, so it may be difficult for the fund to get in and out of certain positions especially if the company issuing those assets are in trouble. The fund might also have to go to the court to get its money back if the company in question defaults. Many times bondholders get the first priority in payments after a company goes bankrupt but the process can take a long time and can be quite costly in the court system. This is one of the risk factors that investors should consider.

One thing definitely going on for this fund is the fact that it's been around since 1971 and it's witnessed several recessions, financial crises, credit crunches, global troubles, wars, changing global landscapes but still continued to not only survive but also thrive during this time. The fund's strength was tested time and time again and it never failed. This is not a guarantee that it will never fail and it will survive everything that will ever happen but it's a pretty good sign that the fund is more likely to survive future economic hardships than not. Yes, it mostly invests in "junk" bonds but its management has always been good at picking the safest "junk" debt to invest in over the years. Also, I should note that the fund doesn't use leverage so it can usually manage its risk profile without disrupting too much.

Even with many years of great execution and outperformance, these types of funds can be quite risky because they deal with high yield debt from small companies, start-ups and pre-IPOs. Many of these companies don't have the financial strength of a blue chip and their debt also has low liquidity. This fund can serve greatly as part of a highly diversified portfolio, possibly consisting of 2-4% of the total portfolio value. I would keep adding in small dips and keep reinvesting all or at least a good portion of dividends and try to maintain a good balance.

For further details see:

MCI: A Strong Outperformer But Less Known