MCI - MCI: Solid 8.4% Yield For A Rich Retirement Dream

2023-12-13 16:25:28 ET

Summary

- MCI has been around since 1971, and putting in a total return performance that outshines the S&P 500.

- With interest rate increases nearing their end, debt prices are near their lows. Making an excellent buying opportunity.

- MCI has increased the distribution 3 times so far this year and yields a well-covered and generous 8.4%.

Why Buy Debt Investments Now?

"It was the best of times. It was the worst of times."

This famous quote from Dickens, if flipped around, could describe the debt security market today. 2022 through 2023 is going to be remembered in history as one of the "worst" bond markets in history. By "worst", I mean one of the best markets for bond investors in history. While, I'll admit that prices for bonds are down heavily, that only really hurts the sellers if you're trying to issue a new bond or sell bonds- now is "the worst of times." Yet, if you're someone who has dollars to be able to use, this is a fantastic time for you - "the best of times," as Dickens would say.

In other articles, we have told the story of Hapless Hal who wouldn't buy coffee when Starbucks was offering it at a discount, but rushed and bought 2 cups once the sale ended. Here I want to talk about a once great chain of stores called KMart. They became known for what was called the "KMart Blue Light Special." How this worked was that at various times some flashing blue lights would come on in the store, and products with a special tag could be purchased at an additional discount.

If KMart shoppers had acted like investors in the stock and bond markets, they would have rushed to put all the specially marked products back on the shelf. Instead, customers saw the advantage in buying at a lower price and rushed to purchase the tagged items.

Currently, the FMOC and market forces have been pushing up interest rates. This has caused the prices of debt, even floating-rate debt, to drop but , it is looking more and more like the rate increases have come to an end. How do we know this? Inflation is slowing, and in fact, inflation during October was flat - even the PPI has pulled back. In a sure sign that rate hikes by the Fed are over, the Fed Chairman has rushed to assure us that more rate hikes are possible. The surest sign that a trend is about to end is when folks feel the need to assure us that it isn't over.

Finally, while we like to be out in front of most investors, we don't want to be entirely alone. Kohlberg Kravis Roberts & Co. L.P. ( KKR ) is widely known as one of the largest global asset managers and a very successful one. With over $500 billion in AUM (Assets Under Management) and $200 billion in debt investments, the firm expects interest rates to have peaked and debt investments to be practically a steal, as we recently posted a report on KKR investments . With this type of company, we feel confident that our analysis is correct. Like KKR we are happy to load up on high-yield assets at this time.

This is why we think that now is the time to buy various debt-focused investments. Currently, we haven't explored one area of debt investments, private placement debt. Barings Corporate Investors ( MCI ), yielding 8.4%, is a CEF that focuses on buying private placement debt.

Historical Performance

Debt investments like MCI are bought for income. How has the income been? From 2013 to 2020, MCI paid out $0.30 a quarter in distributions. When COVID hit, the dividend was reduced to $0.24. Starting with the final quarter of 2022 the distribution has been increased each quarter until it reached the current level of $0.37 payable on November 17, 2023.

While debt investments are not typically bought for high total return (on average over longer periods equity investments produce more total return than debt investments), lots of people like to make that comparison.

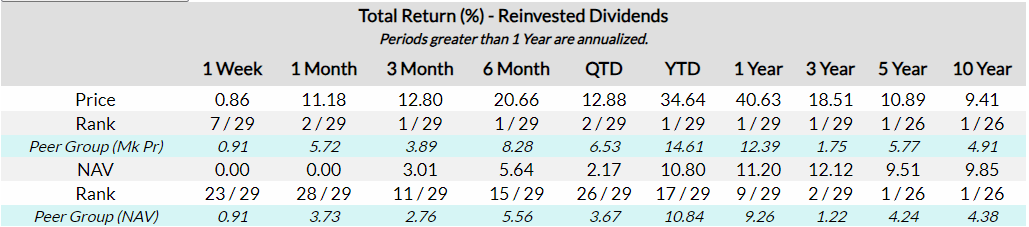

So how did MCI do when compared to the total return over SPY?

Interestingly enough, since the inception of SPY, MCI has beaten SPY in total return. Returning a CAGR of 15.66% compared to SPY's 9.92%. This is fairly unusual as one typically buys debt investments for price stability and gives up some total return to achieve that. Some may say that what the fund did in the distant past isn't relative to whether or not it is a good investment now. So what do more recent comparisons show?

Over the last 3 years, MCI has still outperformed SPY on a total return basis. Returning more than double what SPY did, during a period where rising interest rates caused debt investments to face strong headwinds. Again, I'll point out that typically one buys debt for price stability and income and sacrifices some total return to get those things. It has also beaten long-term treasury bonds by a huge margin. This outperformance compared to long-term treasuries shows how good the management team has done over the last 3 years.

Finally, let's look at the last year. As we can see from ( TLT ) and ( IEF ), it hasn't been a good year for bonds - at least not for the price of bonds. However, MCI produced significant distributions that more than offset the decline in the price of bonds and other debt investments. MCI not only beat the Treasury funds, it produced a significant gain and again beat SPY on a total return basis.

A Closer Look at MCI

MCI has been a top CEF since its inception in 1971, with an annualized return of 12.25% on its NAV over that period, and 12.02% on its market price. This is very impressive for a debt investment and beats the S&P500 over those 50+ years.

MCI relies on Barings' North American Private Finance ("NAPF") platform. According to the fund's 1st quarter 2023 report , it employs more than 60 professionals and has more than $25 billion in private credit commitments. NAPF does all the credit sourcing, due diligence, and portfolio maintenance for MCI. And NAPF does it very well since MCI's 1st quarter 2023 report says NABF has had an annual credit loss rate of only 0.04% since its inception.

Looking at the performance of NAPF, it has served as the Lead or Co-Lead on over 80% of the transactions it has originated. So that low loss record is mostly from transactions where it was in the driver's seat and not just along for the ride. Every investment in the portfolio was directly originated by Barings via a sponsor, where investors collected all of the economic benefits from the investment. The fund has consistently generated a stable dividend for investors, which to date has been paid exclusively from investment income and capital gains - no return of capital. And this was all done with a limited amount of leverage, only 0.12x. The fund invests in high-quality companies in defensive sectors. The fund is well diversified with 30 different industries across 181 assets Over 65% of those investments are first-lien senior secured loans. HDO sees this type of loan as very safe and so it provides strong risk-adjusted returns and reliable income. Around 13% of the market value of the fund is equity-based. This generates about $1.01 per share (or just over $20 million total)in unrealized appreciation as of March 31, 2023.

The individual holdings are not well known as they are small companies, but we can see the different types of holdings MCI has here .

Portfolio (MCI Website)

With a current yield of 8.55% and an increasing NAV now looks to be a good time to buy MCI. But how does that compare to MCI's peers and to its valuation in the past?

CEFData has lots of data on MCI, here . That site shows us how MCI has done compared to peers for both NAV and share price total returns. On a share price basis for total return, MCI has been right near the top for any period of over a week. For NAV returns, MCI began to lag a bit about a year ago. But that was less to do with low performance for MCI, but because its peers were doing very well.

{kind=link}

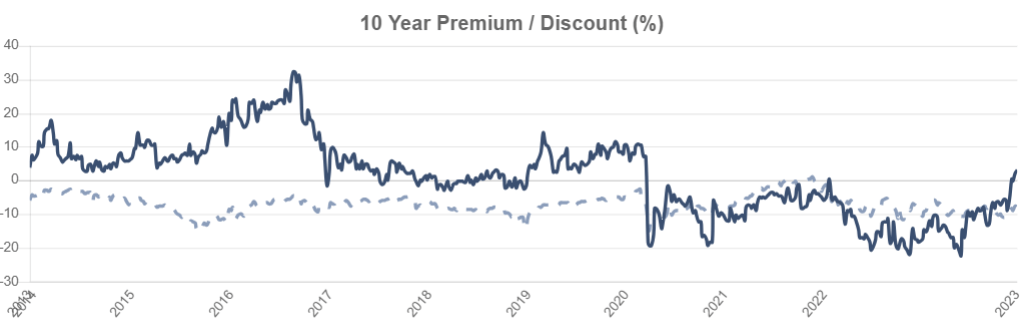

Next, let's look at the discount or premium to NAV that shares are selling at.

I'll use the data from CEFData.com as it includes average data for MCI's peers.

{kind=link}

Note that for most of the 10 years, MCI traded at a significant premium to NAV. That is because of its stellar returns. But we see that the premium declined, and even went into a discount to NAV, right around the time of the COVID crash. The premium has been improving lately, in part likely because of the distribution increases. But the premium is still well below its peak.

Given the increased distribution and the well-covered yield, that MCI is still well below its peak NAV premium offers a good entry price and a good valuation.

Risks

No investment is without risk, even one that has been doing well since the early 1970s. So what risks are there for MCI and its shareholders?

MCI uses very little leverage, so increasing interest rates isn't likely to have a big impact on its costs. The interest it collects is far more likely to increase faster than the cost of its borrowings.

A bigger risk from increasing interest rates is likely to come from its borrowers not being able to handle their increased interest rates. However, since 1971, MCI has been doing a good job of picking companies that can pay their debt. Don't forget that the current team doing credit analysis for them has a failure rate of only 0.04%.

However, we think it is far more likely that we are at the peak of interest rates. It might even be that we will see interest rate decline going forward. This would be a good thing for the price of MCI's assets (even though MCI has managed to increase its NAV). However, the most likely reason that interest rates would decline is that the economy has slowed into or near a recession. This could cause some of MCI's borrowers to go into default. As we pointed out, first-lien secured loans are the least likely to be defaulted on and tend to have high recovery rates. And MCI has experienced many recessions since its IPO in 1971.

For a yield above 8%, the risks MCI faces are fairly small.

Conclusion

With increasing interest rates having pushed debt investment prices down, we think now is the time to be buying debt. Particularly since we are now most likely to the end of interest rate increases. This might not be the bottom, but it is close enough to give us a very good price.

With a strong track record, multiple distribution increases this year, and sporting an attractive 8% yield, MCI is a fund that is well worth holding, especially when we understand the forces that are impacting the prices of fixed income. So many investors are running away from a sector that is likely to combine income with high returns in the months and years to come. Right now the blue light is flashing, and investors should be running to buy like the Kmart shoppers of old! This is the closest to a Black Friday sale on fixed income that we've seen in decades.

When it comes to retirement, the last thing you want is something unproven and unsure for your base. Instead, you want a solid investment that you can stand on and rely on. This is one reason why so many retirees have fallen into the trap of trusting annuities or trusting Social Security. While both may have a role to play in providing retirement income, neither is as effective as it used to be. Today, with MCI, you can buy into a fund that provides a long track record of success. That success can then be harnessed to propel you to new levels of financial security.

That's the beauty of the HDO Income Method. That's the beauty of income investing. Going forward we want to make sure that MCI continues to have a well-covered distribution, including no ROC. An even better sign would be if the distribution was increased yet again. But in the coming days, we certainly want to see an announcement where the $0.37 distribution is continued for the next quarter.

For further details see:

MCI: Solid 8.4% Yield For A Rich Retirement Dream