MCI - MCI: Superb Long-Term Returns But Challenging Macro

Summary

- The MCI CEF focuses on privately placed loans to middle-market U.S. companies.

- The fund has a superb track record, with 12.3% average annual returns since inception in 1971.

- The short-term worry regarding MCI is a pending economic slowdown/recession that may cause credit stress to MCI's portfolio. Already, its largest holding was recently downgraded by Moody's.

Recently, I wrote a review of the Barings Participation Investors ( MPV ) fund and concluded it was a well-run middle-market focused credit fund. Some commentators recommended I take a look at the Barings Corporate Investors ( MCI ) fund, MPV's larger sibling.

The MCI fund provides exposure to privately placed non-investment grade loans to small and middle-market U.S. companies. It has superb long-term returns and pays a hefty distribution yield of over 7%. My only concern regarding MCI is with regards to the macro environment.

It appears we are headed for a recession in 2023, hence I am hesitant to put capital to work in levered credit funds due to the elevated credit risks. For example, the MCI fund's largest position, Madison IAQ, was recently downgraded by Moody's due to its heavy debt load and poor revenue outlook.

However, I am definitely putting the MCI fund on my watchlist for funds to buy when/if credit spreads blow out in a recession scenario.

Fund Overview

The Barings Corporate Investors is a closed-end fund ("CEF") that provides current income as a primary objective by investing in privately placed non-investment-grade corporate debt, including bank loans and mezzanine debt instruments. The fund was incepted in 1971 and currently has over $330 million in assets.

Strategy

Similar to its sibling fund, the MCI CEF primarily invests in private placements of non-investment-grade loans to small and middle-market U.S. companies that are typically purchased directly from the issuers. In addition, the MCI fund may invest in marketable debt securities like high-yield or investment grade ("IG") securities and common stocks that the manager deems to be attractive.

The fund distributes substantially all of its net income each year via quarterly distributions.

Portfolio Holdings

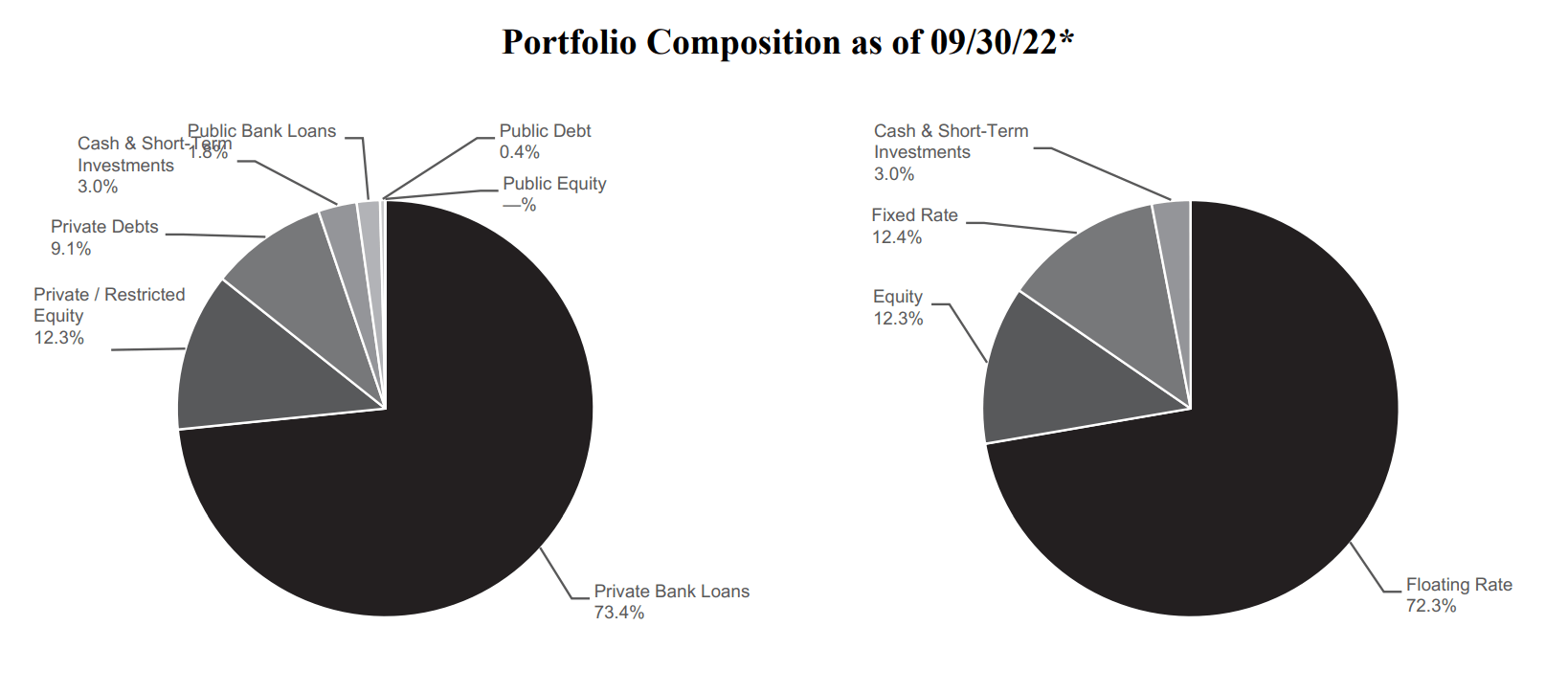

Figure 1 shows the asset allocation of the MCI fund. The MCI fund's assets are predominantly invested in private bank loans (73% of the portfolio), restricted equities (12%), and private debts (9%). In terms of interest rate exposure, 72% of the portfolio is on floating rate and 12% is fixed rate.

Figure 1 - MCI asset allocation (MCI September 2022 quarterly report)

{kind=link}

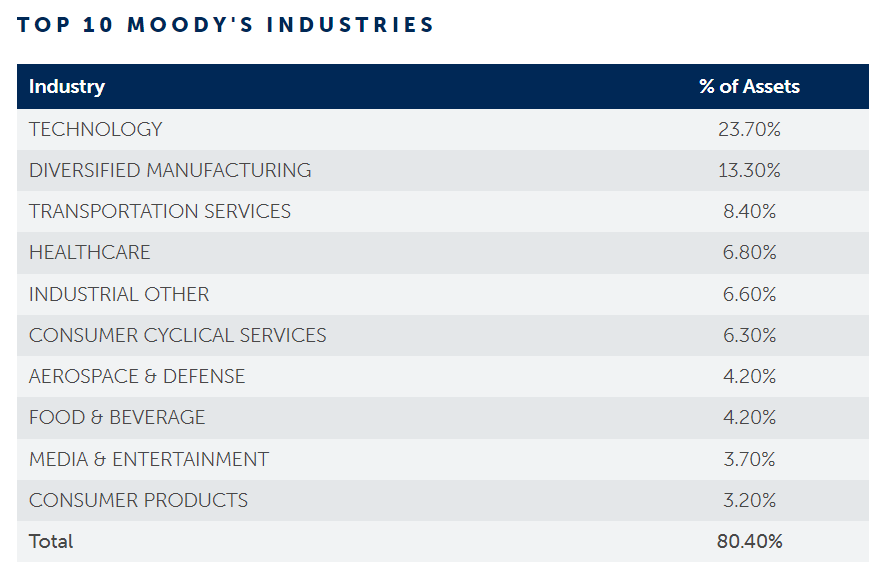

Figure 2 shows MCI's industry concentration. The MCI fund has 80% of its assets concentrated in 10 industries, with technology (24%), diversified manufacturing (13%), and transportation (8%) being the biggest weights.

Figure 2 - MCI top 10 industries (barings.com)

{kind=link}

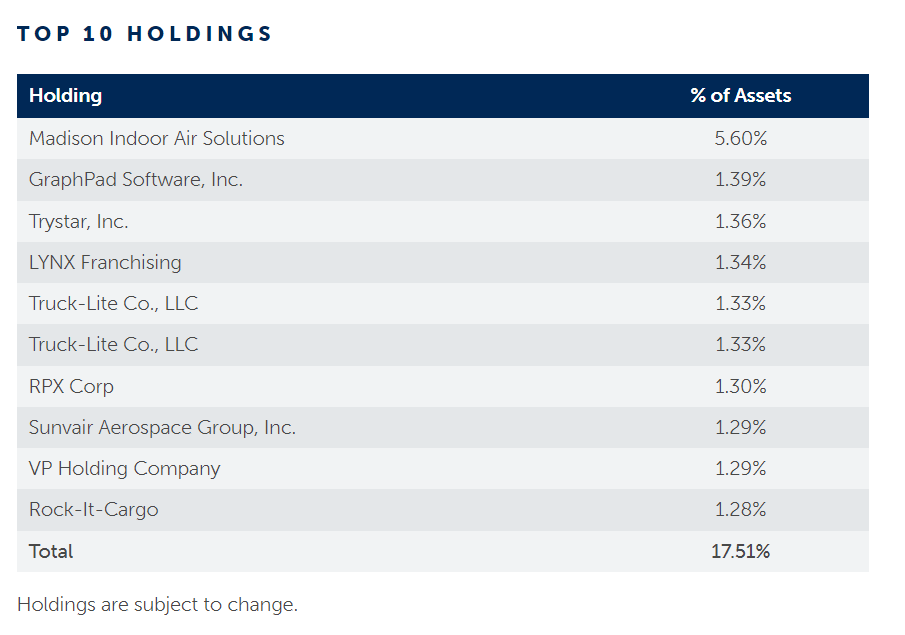

Finally, figure 3 shows MCI's top 10 positions. Similar to the MPV fund, the MCI fund has its biggest weight in Madison Indoor Air Solutions, at a 5.6% weight. Other than the substantial concentration in Madison across MCI and MPV, the MCI fund appears pretty well diversified, with the top 10 positions accounting for only 17.5% of the portfolio.

Figure 3 - MCI top 10 holdings (barings.com)

{kind=link}

What Is Madison Indoor Air Solutions?

Given the large weight of Madison Indoor Air Solutions in both the MCI and MPV funds, it is perhaps worthwhile to dig a little deeper to see what the company is about.

Madison Indoor Air Quality ("Madison IAQ") is part of Madison Industries, one of the largest privately held company in the U.S. Madison IAQ includes many subsidiary companies focused on developing technologies that help deliver clean air for people around the world. Its brands include Addison, Airxchange, Broan-NuTone, CLEANSUITE, Nortek, and many others.

According to a recent Moody's credit downgrade report, Madison IAQ generated revenues of $3.0 billion in the 12 months to June 30, 2022, with EBITDA margins of ~20%. While EBITDA margins were strong, the company has a literal mountain of debt at over $4.5 billion, adjusted for pension and operating leases. This translates to a debt-to-EBITDA ratio of 7.5x.

Moody's downgrade of Madison IAQ's corporate family rating from B2 to B3 is based on projections for a low-single-digit ("LSD") revenue decline in 2023, combined with its heavy debt burden. Moody's estimates that each 50bps increase in interest rates will increase Madison IAQ's interest burden by $13 million. An increase in the debt-to-EBITDA ratio above 8.0x will warrant a further credit downgrade, while a decline below 6.0x will see a credit upgrade.

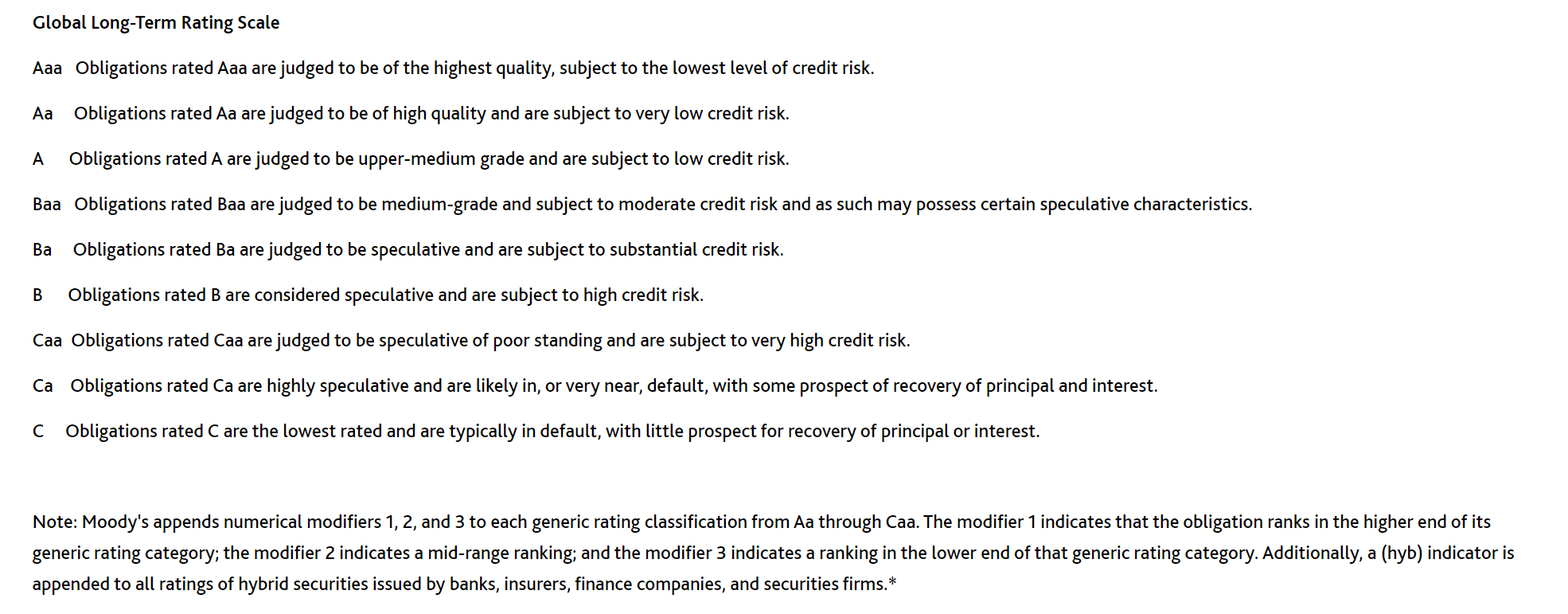

According to Moody's credit rating definition , Madison IAQ's current corporate rating of B3 is considered speculative and subject to high credit risk (Figure 4).

Figure 4 - Moody's credit rating definition (moodys.com)

{kind=link}

Note, Madison IAQ's corporate family rating was originally rated B2 , following the company's leveraged takeover of Nortek in June 2021 , so MPV and MCI investors should see some NAV decline at the upcoming December 2022 quarterly report from the credit downgrade to its largest holding.

Returns

The MCI fund has had strong long-term returns, with 3/5/10 Yr average annual returns of 9.4%/8.6%/10.5% respectively, to September 30, 2022 (Figure 5).

Figure 5 - MCI returns (barings.com)

{kind=link}

Similar to my article on MPV, it appears MCI's 2022 returns are a little too good to be true. YTD to September 30, 2022, the MCI fund has returned 2.4% vs. the Invesco Senior Loan ETF ( BKLN ) which has returned -4.8% (Figure 6).

Figure 6 - BKLN returns (invesco.com)

BKLN tracks the Morningstar LSTA US Leveraged Loan 100 Index, an index designed to track a portfolio of the largest institutional leveraged loans. In theory, BKLN's loans should be less risky than MCI's, as it focuses on larger companies with better access to capital markets and tighter credit spreads. Therefore, it is a little unbelievable that MCI has outperformed BKLN by over 700 bps YTD.

In fact, after several quarters of benign credit conditions, the credit cycle is finally turning, with leveraged loan credit downgrades exceeding upgrades by a 2:1 margin in the third quarter.

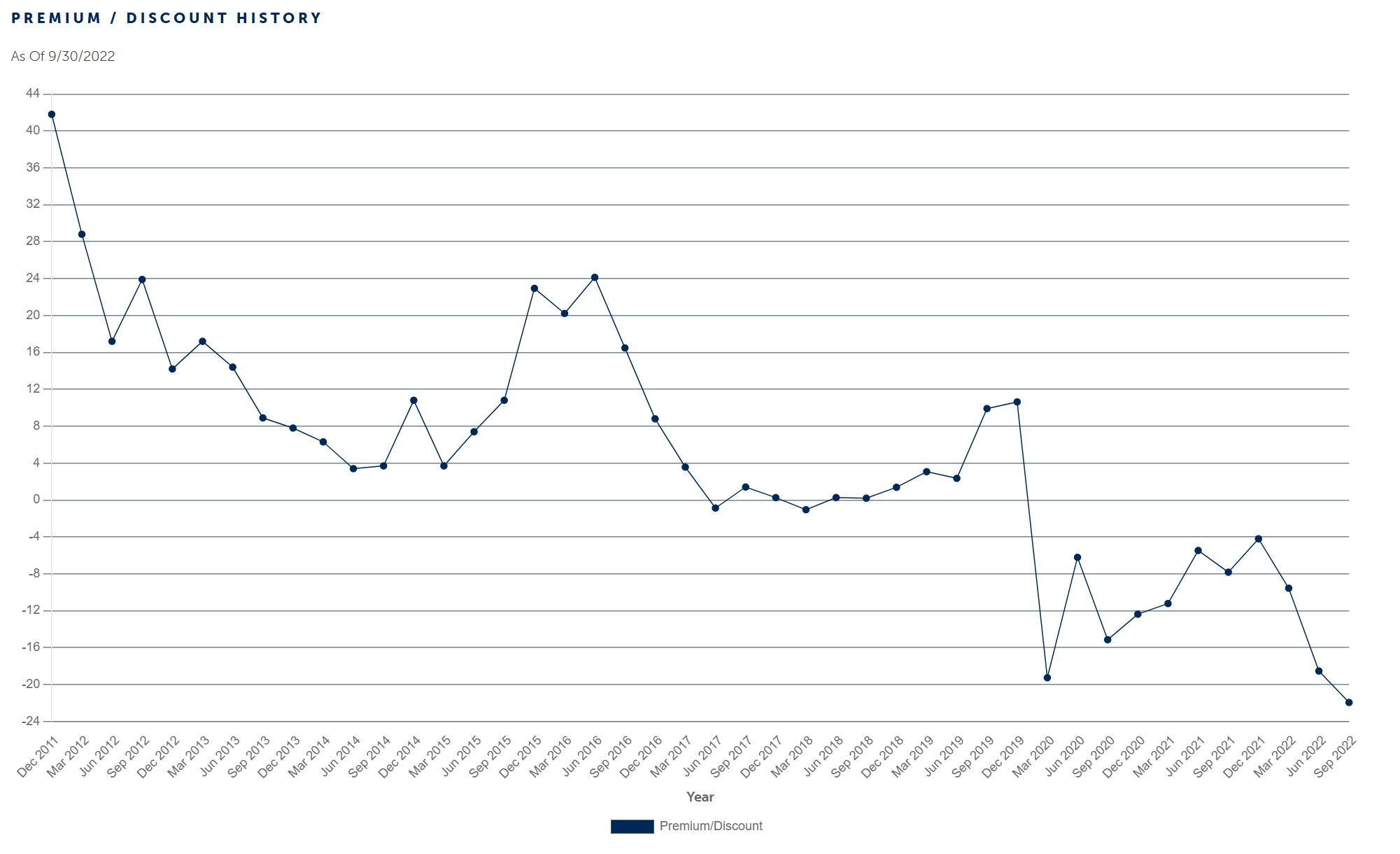

It appears MCI's 10-year unblemished returns record will be put to the test in the coming months. Skeptical investors have already marked down the market price of MCI's shares to a 22% discount to NAV likely in anticipation (Figure 7).

Figure 7 - MCI discount to NAV (barings.com)

{kind=link}

Distribution & Yield

All of the net investment income of the MCI fund is paid out to shareholders through quarterly distributions. In the most recent quarter, the fund announced a $0.26/share distribution, slightly below the latest quarterly net investment income of $0.29/share. The distribution annualizes to an 8.5% market yield or a 6.3% yield on NAV.

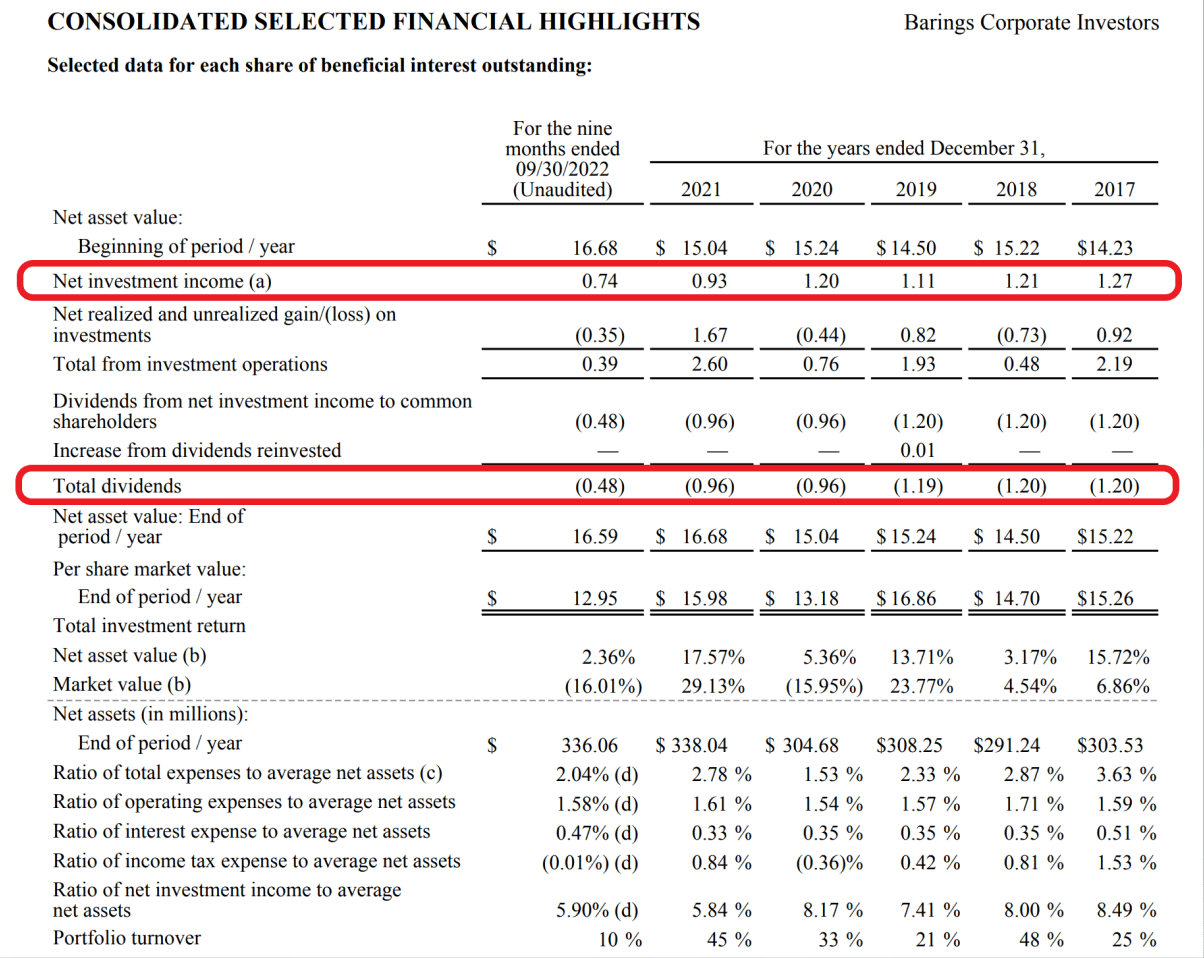

Similar to MPV, the MCI fund's distribution appears sustainable, as it pays a distribution that tracks the net investment income and realized/unrealized gains have been a net positive over the years. This has allowed the MCI fund to grow its NAV/share from $15.22 at the end of 2017 to $16.59 at September 30, 2022 (1.8% CAGR) while paying its substantial quarterly distribution (Figure 8).

Figure 8 - MCI financial summary (MCI September 2022 quarterly report)

{kind=link}

Fees

MCI charged a reasonable total expense ratio of 2.04% of net assets in the 9 months ended September 30, 2022.

MCI vs. MPV & Peers

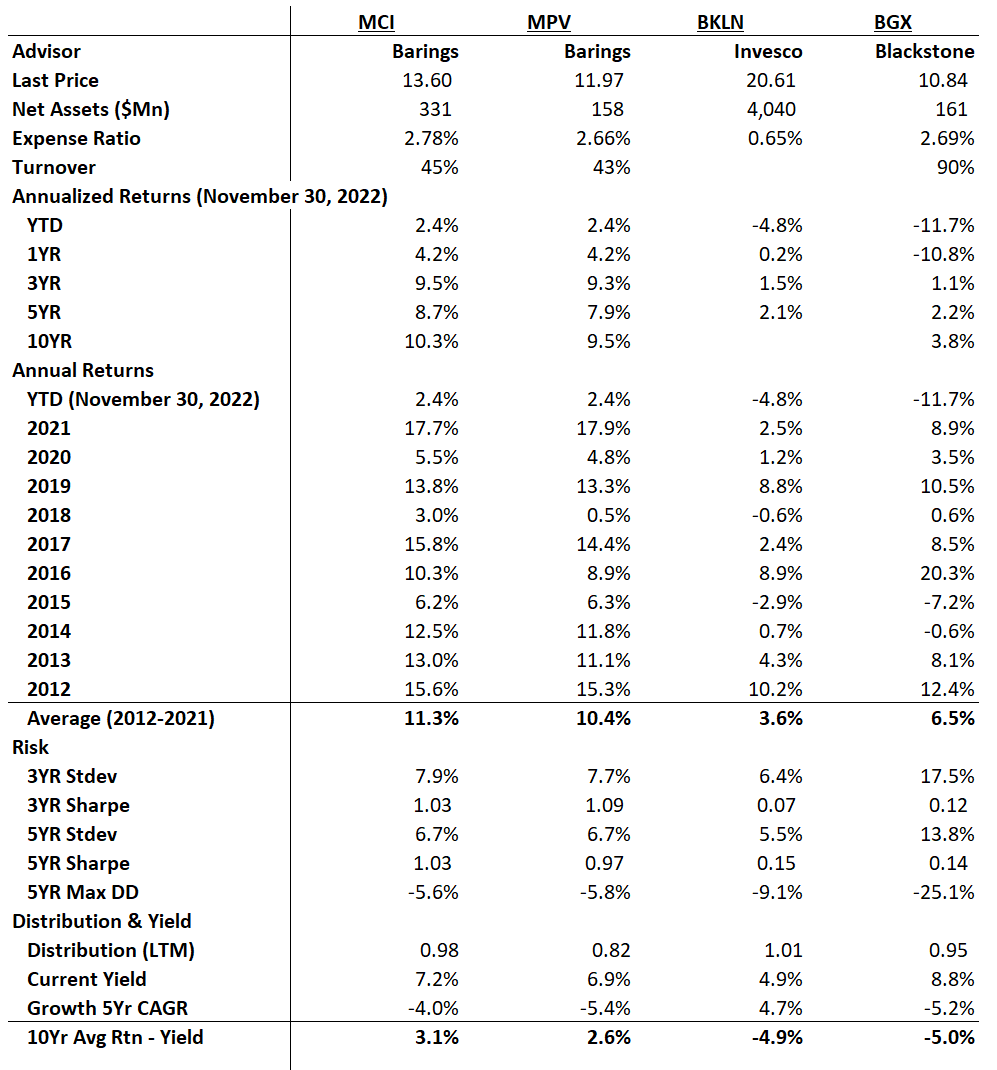

Given the similarities between MCI and MPV, the question in my mind is which fund is better? Figure 9 below compares MCI and MPV side-by-side. It also compares the two Barings funds against the BKLN ETF and the Blackstone Long-Short Credit Income Fund ( BGX ), a CEF that also has 70%+ of its assets invested in senior loans.

Figure 9 - MCI vs. MPV, BKLN, and BGX (Author created with returns and risk from Morningstar and fund details and distribution from Seeking Alpha)

{kind=link}

As we can see, although the two funds are very similar, MCI has slightly better annual returns, with 5 Yr annual returns of 8.7% vs. 7.9% and 10 Yr annual returns of 10.3% vs. 9.5%.

Volatilities are lower for MPV, although MCI's higher 5Yr returns give it an edge on Sharpe Ratios. MCI also has a slightly higher trailing yield.

Finally, when comparing the two Barings CEFs to the BKLN ETF and the widely touted BGX fund, it really is no comparison. Both Barings funds have vastly superior returns and Sharpe Ratios. It's also notable that BGX's 3yr volatility is 17.5%, more than double the Barings funds and the BKLN ETF.

Conclusion

The Barings Corporate Investors fund provides exposure to privately placed non-investment grade loans to small and middle-market U.S. companies. It has superb long-term returns and pays a hefty distribution yield. My only concern regarding MCI is with regards to the macro environment.

It appears we are headed for a recession in 2023, with the credit cycle turning and leveraged loans being downgraded at the fastest pace since 2020. At this time, I am hesitant to put capital to work in levered credit funds due to the elevated credit risks. However, I am definitely keeping an eye on MCI for the right time to accumulate shares.

For further details see:

MCI: Superb Long-Term Returns But Challenging Macro