MCK - McKesson: Still Trading For A Huge Discount

2023-09-06 16:14:57 ET

Summary

- McKesson is reporting great results for the first quarter of fiscal 2024 and is optimistic for the full year 2024.

- The company will be able to grow its bottom line by using share buybacks and aside from top line growth, McKesson might also be able to improve its margins.

- The stock is still trading for low double-digit valuation multiples and clearly below a calculated intrinsic value.

My last article about McKesson Corporation ( MCK ) was published in December 2022. And after a very bullish article in October 2021, I was only “bullish” and saw the stock as a “Buy” in my last article. But I stated that the stock was still trading below its intrinsic value and McKesson increased about 12% in the meantime – a performance that was more or less in line with the performance of the S&P 500 ( SPY ).

In the following article I will take another look at McKesson and confirm my “Buy” rating as I still see McKesson undervalued at this point.

Quarterly Results

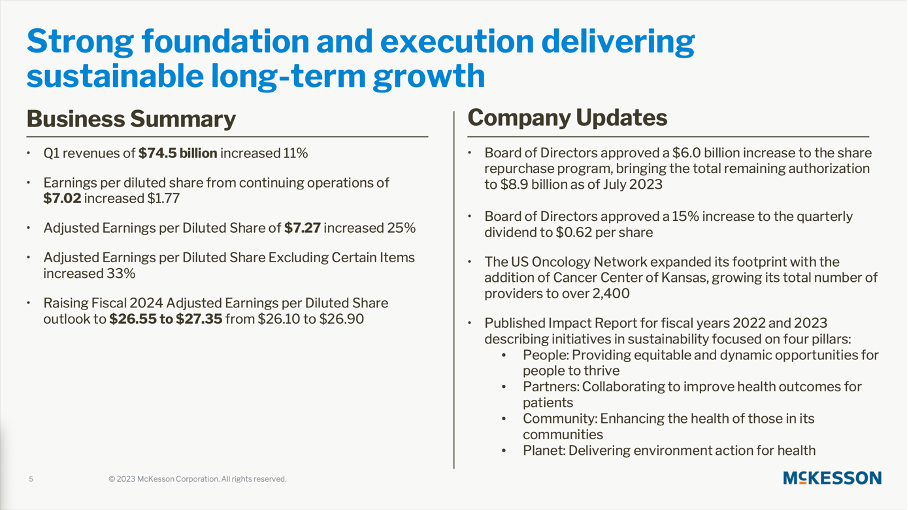

When looking at the results for the first quarter of fiscal 2024 reported August 2nd , we see a business that is not only performing great but also reporting high growth rates. Revenue increased 10.9% year-over-year from $67,154 million in Q1/23 to $74,483 million in Q1/24. Operating income also increased from $1,036 million in the same quarter last year to $1,100 million this quarter – an increase of 6.2% year-over-year. And finally, diluted earnings per share increased from $5.26 in Q1/23 to $7.02 in Q1/24 – resulting in 33.5% year-over-year growth.

{kind=link}

McKesson Q1/24 Presentation

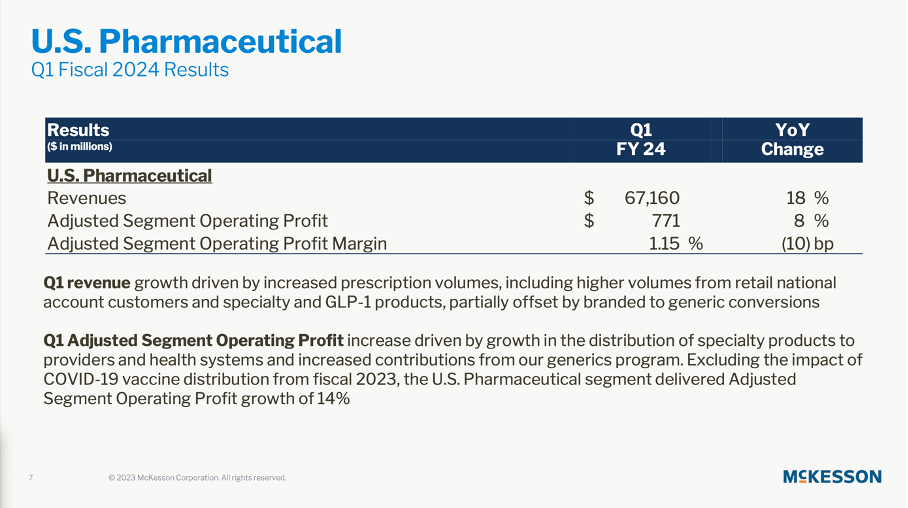

McKesson is reporting in four different segments and while the International segment had to report a steeply declining revenue the three other segments contributed to growth. U.S. Pharmaceuticals generated $67,160 million in revenue in the first quarter resulting in 18% year-over-year growth, which was especially driven by increased prescription volumes (specialty and GLP-1 products are worth mentioning). Revenue increases were partly offset by conversion from branded to generic drugs. Adjusted segment operating profit increased 8% to $827 million and when excluding the impact from COVID-19 vaccine distribution in Q1/23 adjusted operating profit grew even 14% year-over-year.

{kind=link}

McKesson Q1/24 Presentation

Prescription Technology Solutions generated $1,244 million in revenue resulting in 17% year-over-year growth, which was mostly driven by third-party logistics and technology services businesses. Adjusted segment operating profit increased 35% to $223 million, and margin also improved 245bps to 17.93%. And McKesson will continue to penetrate the market: solid prescription trends will also lead to higher demand for RelayRx™ PriorAuthPlus - a software to automate the prior authorization process.

A third segment is Medical-Surgical Solutions , which increased revenue only 1% year-over-year to $2,611 million. And while the segment had to report a declining adjusted segment operating profit, it would have grown 7% when excluding the impact of COVID-19 related items.

Outlook for 2024 and Beyond

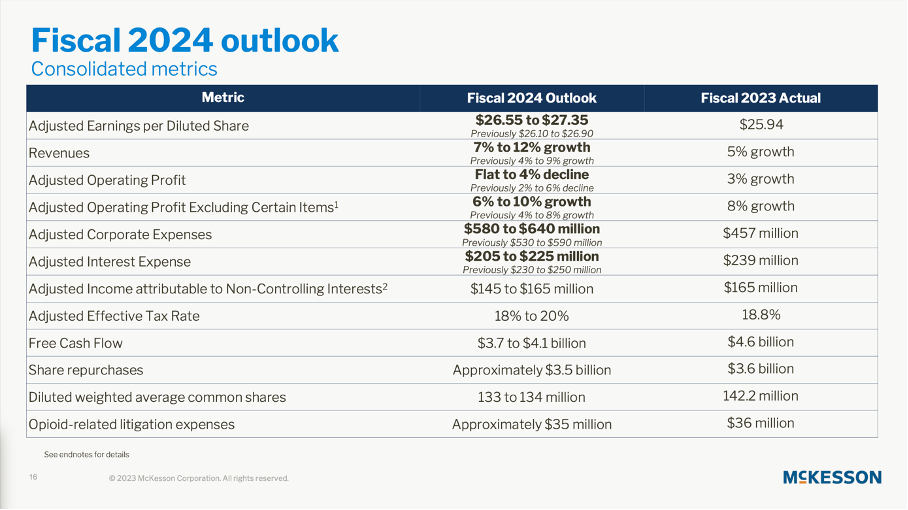

And not only did McKesson report great results for the first quarter of fiscal 2024 – management is expecting great results for the entire fiscal year and raised its guidance. The company is now expecting revenue to grow between 7% and 12% in fiscal 2024 – compared to previous growth expectations of 4% to 9%). And adjusted earnings per share are now expected to be in a range of $26.55 to $27.35 (compared to the previous range of $26.10 to $26.90).

{kind=link}

McKesson Q1/24 Presentation

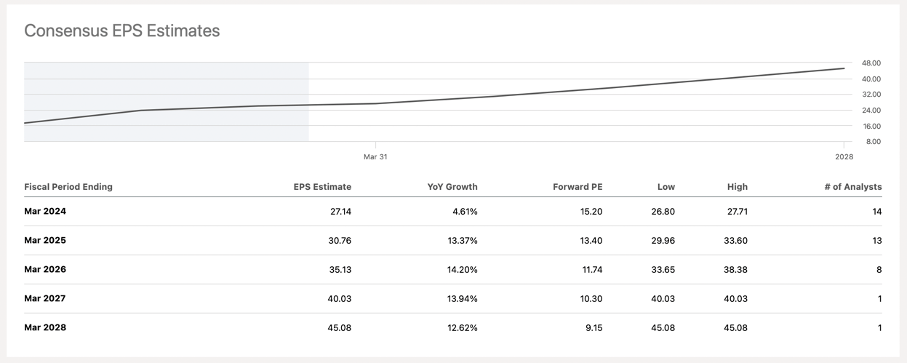

And analysts are expecting McKesson to continue growing in the double digits in the years to come. Between fiscal 2023 and fiscal 2028 analysts are expecting earnings per share to grow with a CAGR of 11.69%.

{kind=link}

McKesson EPS Estimates (Seeking Alpha)

McKesson is profiting from higher prescriptions of GLP-1 as well as obesity medications. When looking at the guidance of Eli Lilly ( LLY ) as well as Novo Nordisk ( NVO ) and analysts’ expectations we can expect these trends to continue in the years to come and be a tailwind for McKesson. Looking at U.S. Oncology, same-store patient visits grew at a good pace and McKesson is continuing to expand the reach of the network. I already wrote in previous articles about the growing oncology business:

And the oncology market is large and growing. About 18 million people in the United States of America are living with cancer today and about 1.9 million are diagnosed annually. McKesson has built a network with over 2,000 provider and more than 500 sites of care in 25 states. And McKesson is expecting the oncology drug market to grow with a CAGR of 14% in the next five years. Right now, there are more than 300 oncology drugs on the market.

Aside from growing the top line, McKesson can also grow its bottom line by improving margins. McKesson is still a low margin business and therefore even small improvements can have a huge impact. When looking at the gross margin in the last ten years we see a constant decline from about 6.4% almost 10 years ago to 4.35% right now. This is certainly not a good sign and indicating missing pricing power. However, McKesson managed to improve operating margins again in the last few quarters and I assume the operating margin will also improve again.

And one reason to be optimistic for improving margins are the other business segments aside from U.S. Pharmaceuticals. Despite being the most important segment (generating almost all revenue and the biggest part of operating income) it has only a margin of 1.2%. The Medical-Surgical Solutions segment had an operating margin of 8.7% and the Prescription Technology Solutions segment had a margin of 18.6%. And if these two segments can continue growing revenue with a high pace, overall margin for McKesson will improve over time and have a positive effect on the bottom line.

Another way to grow the bottom line is by buying back shares. And at least in the last 15 years, McKesson has been constantly buying back shares. The number of outstanding shares was reduced from 319 million in 2006 to 136.60 million right now – resulting in a CAGR of almost 5%.

In the first quarter of fiscal 2024, McKesson continued to repurchase shares and spent $696 million. And the Board of Directors – aside from increasing the dividend by 15% to $0.62 per share per quarter – approved an additional $6 billion of share repurchase authorization, bringing the total remaining share repurchase authorization to approximately $9 billion.

Still a Bargain?

And according to the guidance for fiscal 2024, McKesson will spend about $3.5 billion on share buybacks – almost the entire free cash flow the company is expecting for the year. One can interpret that move as confidence by management that the stock is still undervalued. It could also just show that McKesson doesn’t have a better way to spend the generated free cash flow.

But the two major simple valuation metrics – the price-earnings ratio as well as the price-free-cash-flow ratio – are also indicating an undervalued stock. At the time of writing, McKesson is trading for 15.4 times earnings (I didn’t include the P/E ratio in the chart as the triple digit P/E ratios in previous years would mess up the chart) and 12.9 times free cash flow. And for a high-quality business these valuation multiples seem rather cheap and indicating that we might be looking at a bargain.

Additionally, we can also calculate an intrinsic value by using a discount cash flow calculation. In my last article I calculated an intrinsic value of $680 for McKesson and in this article, we will update the calculation. We are calculating with a 10% discount rate (as always) and 136.6 million diluted outstanding shares. As basis for our calculation, we take the midpoint of the free cash flow guidance (which is $3.9 billion). And this is very close to the average free cash flow of the last five years and therefore an amount we can take as basis for our calculation.

To be fairly valued, McKesson has to grow its free cash flow only slightly above 3% from now till perpetuity and this seems like (easily) achievable growth assumptions for the business.

However, when trying to calculate with realistic growth assumptions, we should assume a higher growth rate for McKesson. In my opinion, 6% growth seems like a realistic assumption for the business. Not only is the growth rate below analysts’ expectations for the years to come, McKesson also reported higher growth rates during the last decade. While revenue increased with a CAGR in the last ten years of 8.49%, operating income increased with a CAGR of 7.11% and earnings per share grew even 16.17% annually during that time. And as we argued above, McKesson can almost reach this bottom-line growth by buying back shares (of course, this assumption is based on the stock continuing to trade for similar valuation multiples as right now).

When calculating with 6% growth till perpetuity – and all other assumptions being the same – we get an intrinsic value of $713.76 for McKesson and the stock is still deeply undervalued.

Conclusion

McKesson will be able to grow with a solid pace and even when assuming moderate growth rates, the stock is undervalued. However, when looking at the P/FCF ratios in the last ten years we can see that McKesson was always trading for a rather low valuation multiple. This can be interpreted as the market being rather cautious to ascribe the business a higher valuation multiple and might be an argument for the stock not reaching the calculated intrinsic value of $700 anytime soon. But from a fundamental point of view, the stock price should continue to move higher in the coming quarters.

For further details see:

McKesson: Still Trading For A Huge Discount