MCK - McKesson: Strong Free Cash Flow But Shares To The Expensive Side Vs. History

2023-05-07 05:40:53 ET

Summary

- This earnings season has featured a strong beat rate, but companies topping EPS forecasts have not seen favorable stock price reactions.

- McKesson reports Monday night, and a positive performance history is an arrow in the bulls' quiver, but with a valuation that is stretched compared to its history.

- I outline key price levels to watch on MCK's bullish technical chart.

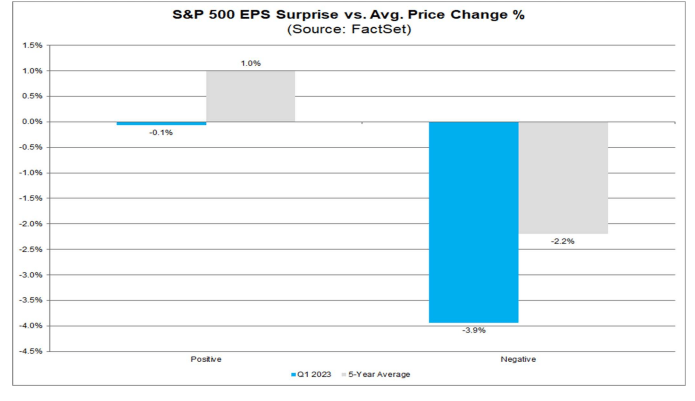

Companies beating on bottom-line estimates have not been rewarded so far this earnings season. According to FactSet, the typical stock price reaction is a decline among beaters, while those missing on consensus estimates have seen their stock price fall by nearly 4% compared to the market.

I have a hold rating on McKesson (MCK) given its lofty valuation compared to its history. Still, its free cash flow is strong, and the technical view is also encouraging.

No Rewards For Beats This Earnings Season

{kind=link}

According to Bank of America Global Research, MCK is the largest drug distributor in the US and has sizable businesses in Canada and Europe, including distribution and retail pharmacy assets. MCK is the largest medical surgical distributor in the non-acute care market and offers various supply chain services and technology, although it recently divested its clinical health IT platform.

The Dallas-based Health Care Distributors industry company within the Health Care sector trades at a near-market 16.8 trailing 12-month GAAP price-to-earnings ratio and pays a small 0.6% dividend yield, according to The Wall Street Journal.

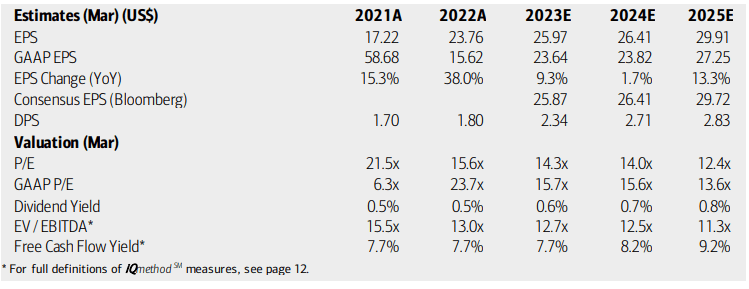

Back in February, MCK topped earnings estimates while missing on the top line. Sales growth was just +3% year-on-year, and the expectation this time is for just a 3% sales rise. What was encouraging about the previous EPS report was that the company increased its 2023 adjusted EPS (diluted) guidance range to $25.75 to $26.15, from the prior range of $24.45 to $24.95 versus a $24.80 consensus.

The company is now into its FY 2024, though, and earnings growth is actually quite sluggish. With three straight guidance increases, however, it is quite possible that the management team offers up more sanguine forecasts. As a strong free cash flow generator, the business appears on sound footing. Downside risks include increasing competition in the drug pricing market along with opioid litigation risks.

On valuation , analysts at BofA see earnings rising at a solid clip this year before per-share profit growth slows in 2024. But a reacceleration is expected in 2025. The Bloomberg consensus forecast is about on par with BofA’s projection. Dividends, meanwhile, are expected to rise at a steadier pace than EPS, though the yield should remain modest.

Both MCK’s operating and GAAP P/E ratios are compelling considering the general growth rate through 2025. The EV/EBITDA ratio is near the S&P 500’s average, however. With solid free cash flow and a generally stable business outlook, MCK can be thought of as both a value play with some growth along with sporting some defensive characteristics.

MCK: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

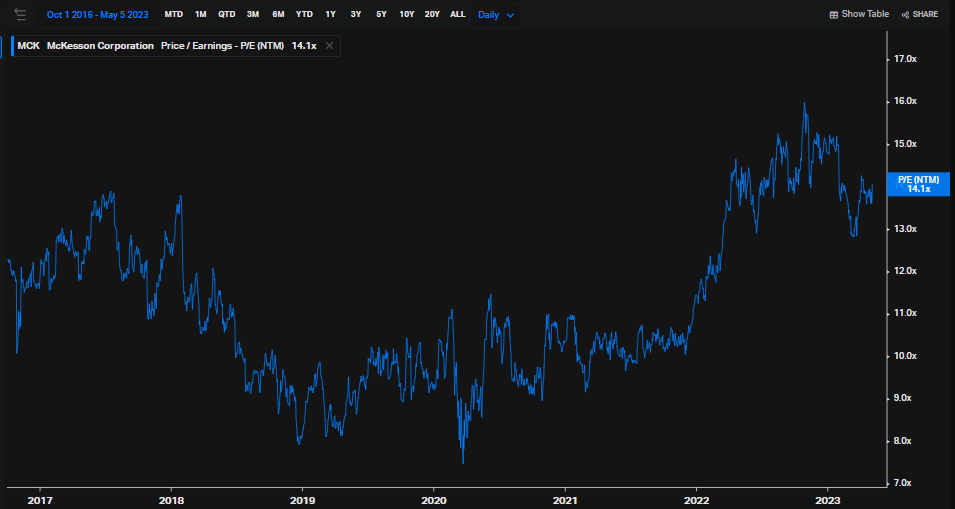

Considering the company’s 5-year average P/E is just 11 while its typical PEG is 1.25, it would appear the valuation is not that great versus history. Even a normalized PEG comes to about 2 (assuming 7% EPS growth on a 14 multiple). So, I’m not all that enthusiastic about how MCK is priced today. I concede that the firm’s long-term valuation could be re-rating higher toward a P/E in line with the markets.

Overall, however, I see fair value near $378 based on $27 of earnings on a 14 multiple.

MCK: Compelling Absolute Valuations, But Not To Its 5-Year Average

Seeking Alpha

MCK: P/E Historically Stretched

{kind=link}

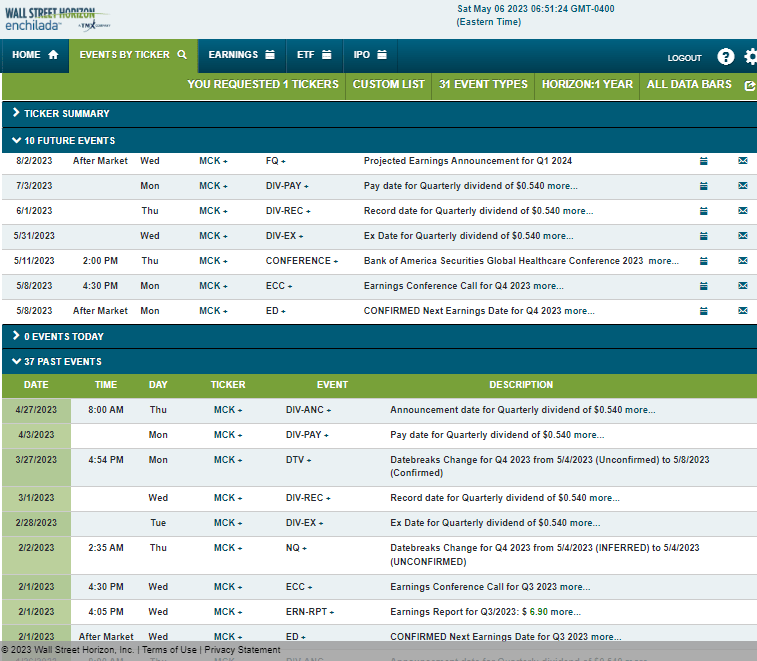

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2023 earnings date of Monday, May 8 AMC with a conference call immediately after results cross the wires. Later in the week, the management team is slated to present at the BofA Global Healthcare Conference 2023, so there could be additional business updates provided then.

Corporate Event Risk Calendar

{kind=link}

The Options Angle

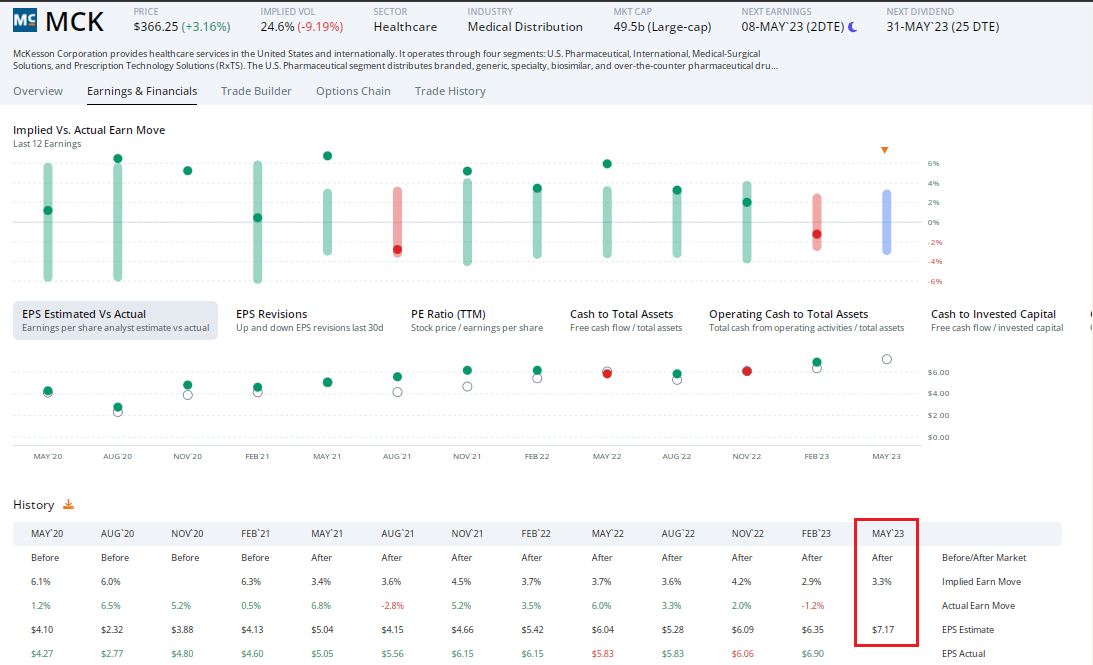

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $7.17 which would be a sharp 23% increase from $5.83 of per-share profits earned in the same period a year ago. MCK has a solid EPS beat rate history, and the stock has traded higher post-earnings in all but two of the past 12 instances. So, the trend is with the bulls.

This time around, the options market has priced in a small 3.3% earnings-related stock price swing when analyzing the at-the-money straddle, expiring soonest after Monday night’s earnings report. That aligns with muted share price reactions over recent quarters, so I would rather play the stock itself rather than the options. Implied volatility is just 25% ahead of the announcement, per ORATS.

MCK: Not Expecting A Big Earnings Move

{kind=link}

The Technical Take

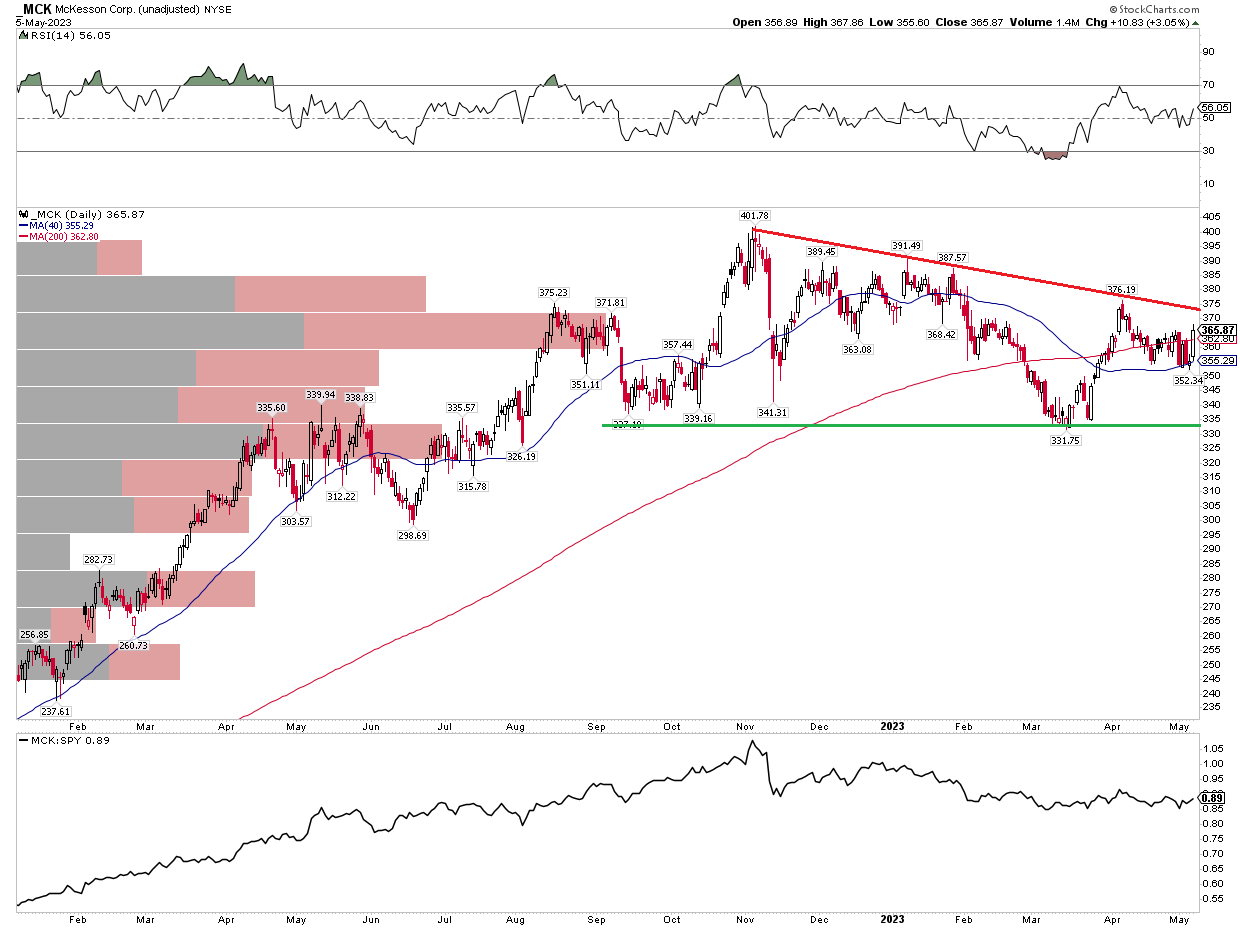

MCK has been one of the market’s leaders over the last few years. Shares have been consolidating in a bullish descending triangle pattern – the presumption is that the pattern will resolve with price moving in the trend of a larger degree – which would be higher in this case. The measured move price objective assuming a breakout would be to near $450 (based on the $70 triangle's range added on top of a potential breakout point of $380).

But a bearish breakdown under $332 support would trigger a price target to near $260. But with a rising 200-day moving average, the trend favors the bulls, and the stock continues to exhibit decent relative strength compared to the S&P 500.

MCK: Bullish Consolidation, Eyeing $380 For A Breakout

{kind=link}

The Bottom Line

I am a hold on MCK into earnings. I like the technical setup longer-term, but the valuation is not overly compelling following the major share-price rally over the last few years. EPS growth is not very strong this coming year.

For further details see:

McKesson: Strong Free Cash Flow, But Shares To The Expensive Side Vs. History