MCK - McKesson: Why The Company Is Too Richly Valued

2024-01-19 05:55:53 ET

Summary

- McKesson is a Texas-based healthcare company that distributes pharmaceuticals, provides health information tech, medical supplies, and care management tools.

- The company has strong fundamentals but is currently overvalued, leading to a "HOLD" rating.

- McKesson's low profitability, pressure on reimbursement, and political scrutiny in the healthcare industry pose risks to its future growth.

Dear readers/followers,

A subscriber recently inquired as to my stance on McKesson (MCK). This is a company that I've kept an eye on, but have never actually invested in, even if I have invested in some of the company's competitors and peers.

In this article, I'll establish for you my base thesis for McKesson - so this is the first article for me on this company with a fresh stance. We'll look at what McKesson can offer you as an investor, why it might be a good investment (or indeed, why it might not be), and what sort of returns can be expected from the company going forward.

I'll spoil this one a bit early. I view McKesson as an overvalued prospect at this particular point in time. The company has a very rich valuation both historically, and as a product of its market share and fundamentals, but I believe this has gone too far.

I'm therefore going in with a "HOLD" rating for this company. However, I view McKesson's worth as looking at, and I'm going to make it clear to you why you should put this one on your watchlist, and indeed why I have done so.

Let's get going.

McKesson - A company with strong fundamentals

First off, what exactly is McKesson?

McKesson is almost 200 years old at this point, founded back in 1833. It's a Texas-based healthcare company with customers across the entirety of the US. It employs over 50,000 people, and the company is in the business of:

- Distributing Pharmaceuticals

- Providing Health information tech

- Providing Medical supplies

- Providing care management tools.

A large part of all pharmaceuticals delivered across the entire nation and indeed across NA, are delivered by McKesson. In short, it can be said the business is working with the healthcare value chain, from systems to supplies, pharmaceutical products, and network infrastructure for the industry.

In the most recent history, McKesson was a key distributor of vaccines in North America, and played a big part in distributing the COVID-19 vaccine, serving as the government's centralized distributor for these purposes with over 1 billion doses across the US. That is the sort of powerful supply chain and management infrastructure that we have to work with here.

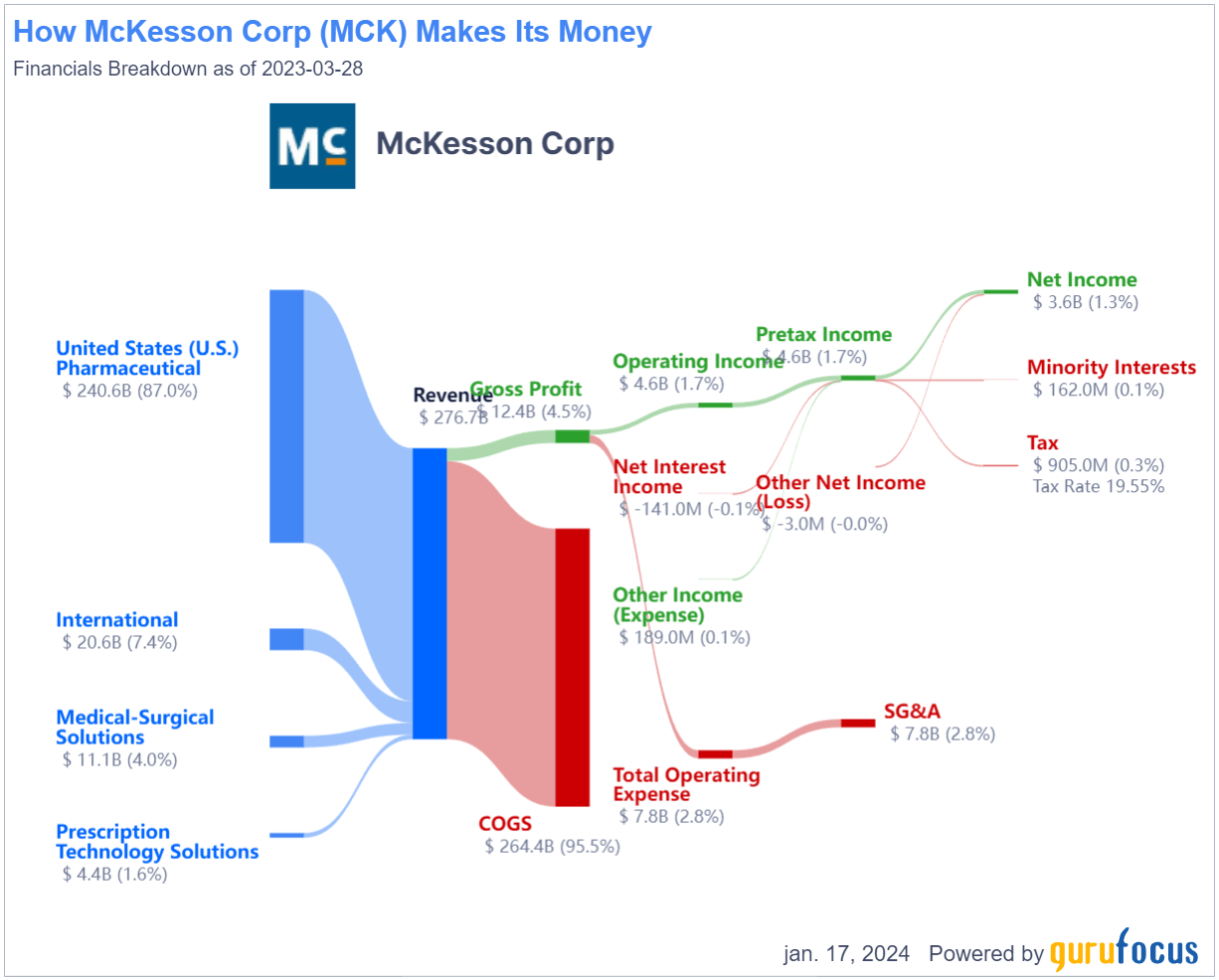

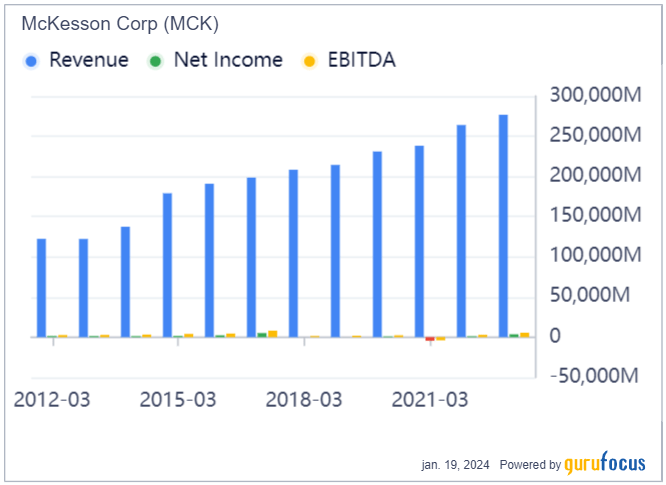

The company, as of 2023, was ranked as the 9th-largest US corporation by Fortune 500 and manages annual revenues of over $275B. On those revenues, they manage a gross margin of around 4-5%, with an operating margin of less than 2%, and a net margin of less than 1.4%. Given the sheer size of the company's top line, this is still an impressive profit in the billions - but it's also, when we look at its segment, not a market-beating or even market-above-average company - specifically medical distribution.

I am personally no longer invested in the sector of medical supply distribution. Years ago, I was invested in several companies, as I believed that the players making a razor-thin profit on these revenues were bound to impressive futures. But when those companies went up in valuation - companies like Cardinal Health (CAH), I then went ahead and sold my stakes in all of them. I do not regret this, and I am in no hurry to get back into his sector unless I can do so at a very attractive valuation.

Because while the companies are large, and while they are certainly important businesses, I also believe them to be very richly valued here.

They are also extremely pharma-focused, at least McKesson. While I've now mentioned that the company does other things, here are the current business model specifics.

McKesson Business Model (GuruFocus)

{kind=link}

This is the highest COGS that I have seen in a company of this size. And because of how this sector works - with extremely costly overheads and supply chains - these companies' potential of actually lowering their COGS is smaller than you might think.

The results we have for the company are 2Q24 - and you can find those here.

The company managed impressive, double-digit growth in top-line sales, but a significant EPS decline on a diluted basis due to bad debt related to the bankruptcy of Rite-Aid (RAD). Excluding these certain items, EPS grew by 14%, and the company raised its fiscal 2024 outlook to a high-end EPS of $27.4/share, up around 5 cents from the last forecast.

McKesson continued reporting strong trends, including new contract awards from the FDA.

{kind=link}

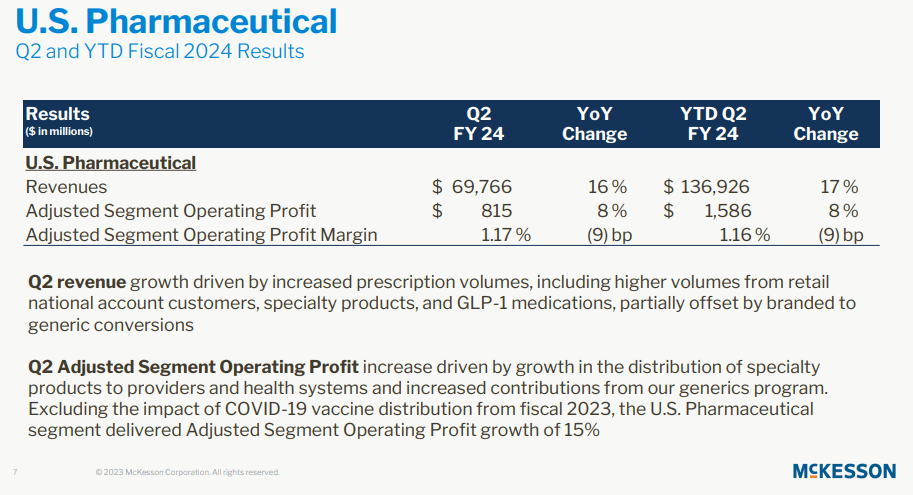

However, digging down into numbers, we find that while the top line increased, the company is having a harder with the margins in some segments. The by far largest segment is pharmaceuticals. While revenues were up 17%, the company's profit margins were down 9 bps and saw 1.16% down from 1.16% on operating profit. It's the largest segment, but also with the lowest profitability.

{kind=link}

Compare this to prescription technologies, and we instead see a margin expansion of 344 bps, to 18.33% as well as top-line growth. If we expect McKesson to grow, it'll likely be on the back of segments like these with better margins. The company's other segments are mixed. Medical-surgical solutions saw flat revenue and declining margins due to the continued decline in COVID-19 tests, and the company's international segment was profitable, and growing in margins, but managing barely 2.6% operating margin on an adjusted basis, with a halving of the revenue, related to McKesson's selling of the European business to become more US-centric.

To call McKesson a low-margin business would be an understatement. I've seen lower, still-profitable margin businesses, but not of this size. Still, the company's fundamentals are very solid. We're at a BBB+ rating, but with a dividend of less than 0.55%, which makes the dividend near-irrelevant in terms of the company's return profile.

And the return profile is where I believe this company becomes not only tricky, but even dangerous. With the advent of the COVID-19 crisis, this company, alongside much of the sector and companies in similar segments, saw strong upticks in valuation, as well as sales and demand. This has resulted in some of these companies' valuations being at very elevated levels for a long time.

While some analysts believe this is a "normal" that may persist for these companies, I am of a different mindset. Let me clarify where I see risks and rewards for this company here.

The 3Q23 earnings are coming in early February. What I would watch for or look for in terms of changes to my overall thesis or target is if there is a material improvement not only in top line, but in the margins for the company. I would also look specifically at the company's growth in the higher-margin segments , rather than just pharma and international. MCK has given us forecasts and projections for the full year. If we look at the 2Q23 results over the longer term, it's a confirmation of the pricing and margin pressure that this company is going through, which also to my mind makes these businesses so difficult to invest in - because the margins are so low. The argument can be made that the company has sectors with significantly higher margins, that can be used to deliver better growth. Prescription solutions is one such sector - but their relative size makes any contribution here to the bigger picture relatively minor.

Risks & upside for McKesson

The primary risk that I am going to argue for here, and which I will highlight in the next segment, is the company's valuation. I view this as way too high - and I'm far from the only one to do so. Typical analyst services such as GuruFocus and Morningstar view the company with a significant amount of valuation worry as well, giving the business no higher than around $400/share.

The risks are not only valuational in nature though. One of the primary reasons I left this space behind, and am hesitant to invest in any pharma or healthcare except at the more undervalued entries, is the sheer pressure on pharma and healthcare customers to provide services and products at lower costs. This pressure on reimbursement might affect a giant like McKesson less than smaller businesses, but McKesson also doesn't have much net margin to give - if we drop another 40-50 basis points, we're below 1% net margin.

The sentiment against these businesses can be described, I believe, like a political firestorm with scrutiny from the public, media, and politicians for prices for drugs being a high priority, from both sides of the political aisle. This could result in top-line growth for McKesson slowing down, but more importantly, margin pressure.

While this company is without a doubt a strong market performer with a share of a third of the industry, that means that MCK has substantial tailwinds when it comes to negotiating to price, and there might still be some gains from technology and AI to "get", I am skeptical just how much savings it is possible to see from this, and how much this company's profitability can grow.

This would not be a problem, or at the very least less of one if McKesson was cheaper.

But now we come to the clincher.

Valuation for McKesson

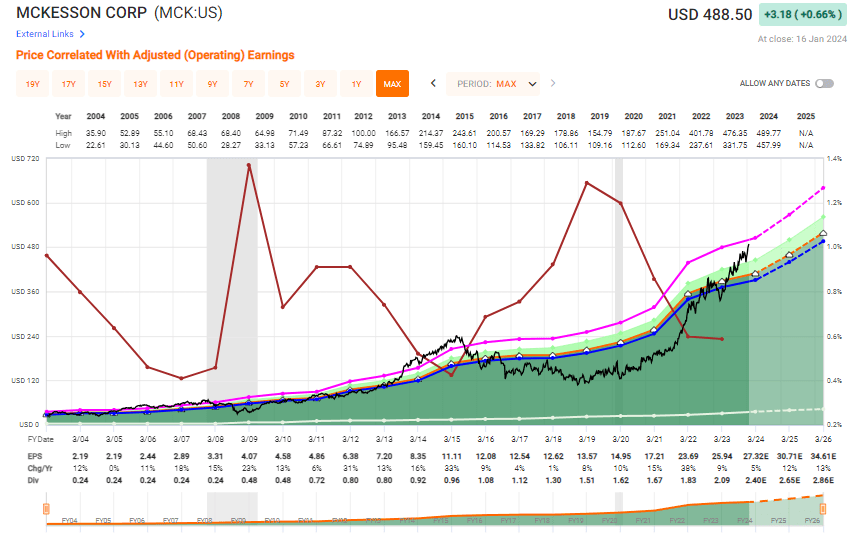

Valuation is the problem for this company. While McKesson has seen historical periods of trading at over 15x P/E, those periods have been short, followed by long years of trading at sub-15x P/E, at some time even sub 10x - for far longer than the company has traded at any sort of premium.

F.A.S.T graphs McKesson (F.A.S.T graphs)

{kind=link}

If you're a valuation-oriented investor such as me, you're likely looking at this and indeed seeing a bit of a problem with buying the company at this valuation. We're over 18x P/E for a company that on a 20-year average is at 13-14x, and at a 5-year average manages 11-12x. Estimating MCK at 15x P/E gives us an annualized RoR of 3.35% - estimating it at anything close to its long-term averages turns this annualized rate of return to negative numbers, at the lowest to around negative 25% total RoR in 2026E, with a PT of $360 for a 10-11x P/E.

If you're bullish on this company, and if you give credence to valuation, you need to believe this company manages to retain at least a 19x P/E, higher than today , in order to see what I consider my target, 15% annualized or above. This is because of the low company yield, and what is already a high multiple for this business.

My own target comes to $380/share. Why $380? Unpacking this target, I use P/E multiples here, and this comes to a conservative 12.5x 2024E P/E, which would mean above 0.7% yield and an upside to a 15x P/E of double digits. The reason why I consider specifically historical averages to be a good indicator of where the company should trade is the company's lack of overall cyclicality. If you look at earnings, these are relatively linear, and while their quality margins have fluctuated some, it hasn't shifted much. A linear-growing company such as this is perhaps the best example of a business where historical averages and forecast statistics make for a good valuation indication. And while I believe the company's margins to actually deteriorate further, I believe this deterioration will be a process of years - not any sort of short time frame.

While MCK is estimated to grow, it's only estimated to grow 5% this year - and I don't believe a company growing at 5% should be valued at 18x if it only has margins of 1.3% for the net margin - however good its fundamentals may be.

If you want a high multiple, you need to show high growth. If you don't show high growth, you better have a high yield - then I can accept a 10-15x P/E, maybe even 18-20x if the safety is good enough. But MCK has decent growth, and a sub-par yield, and that's not a combination, together with the pharma/medical supply segment exposure, that I am looking at. That is my reasoning for my PT.

Other analysts? S&P Global averages come from $400 to $563, so unlike me, many of those analysts do confirm the company's premium here, with 8 out of 15 at a "BUY". I can see and understand the thesis and rationale that would result in this sort of PT - but I don't agree with it.

Here is my current thesis for MCK.

Thesis

- McKesson is among the market leaders in the distribution of pharmaceutical products and related sectors. Very few companies can come close to what this business offers, and with BBB+ credit and inarguably safe fundamentals, it will take something herculean to dislodge McKesson from its position in the market.

- However, the company has less than 1.5% net margin and less than 2% operating margin. It's in a sector under heavy and consistent political scrutiny that I do not consider likely to get less or disappear.

- This combined with a very unattractive valuation with an upside-only if the company outperforms and if you accept a high premium means that my interest in the company here is very low.

- I give McKesson a share price target of $380/share at most and go in at a "HOLD" here.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversion.

This company fulfills only the quality indicators of my requirements, making it a clear "HOLD" to me here.

For further details see:

McKesson: Why The Company Is Too Richly Valued