MCN - MCN: This Covered Call Fund Is Getting Much More Attractive

2023-10-12 17:55:09 ET

Summary

- The Madison Covered Call and Equity Strategy Fund offers a high level of income and potential for upside compared to fixed-income funds.

- The MCN closed-end fund has underperformed the S&P 500 Index over the past two months, but its distribution partially offsets share price declines.

- The fund employs a strategy of writing covered calls on stocks in its portfolio to generate income, resulting in a higher yield than peer funds.

- The fund's poor performance can be partly explained by its price premium narrowing. The fund's valuation is currently more attractive than it has been in months.

- The MCN distribution is probably sustainable, although the fund partially had to rely on unrealized gains to stay positive over the first half of the year.

The Madison Covered Call and Equity Strategy Fund ( MCN ) is a rather underfollowed covered call-writing closed-end fund ("CEF") that investors who are seeking to earn a high level of income from their portfolios but still wish to maintain a degree of equity exposure might appreciate. The fund's 10.47% yield is quite attractive even in today's high-rate world, and the fact that the fund still has the potential to provide greater upside than a typical fixed-income fund is something that we should find somewhat attractive.

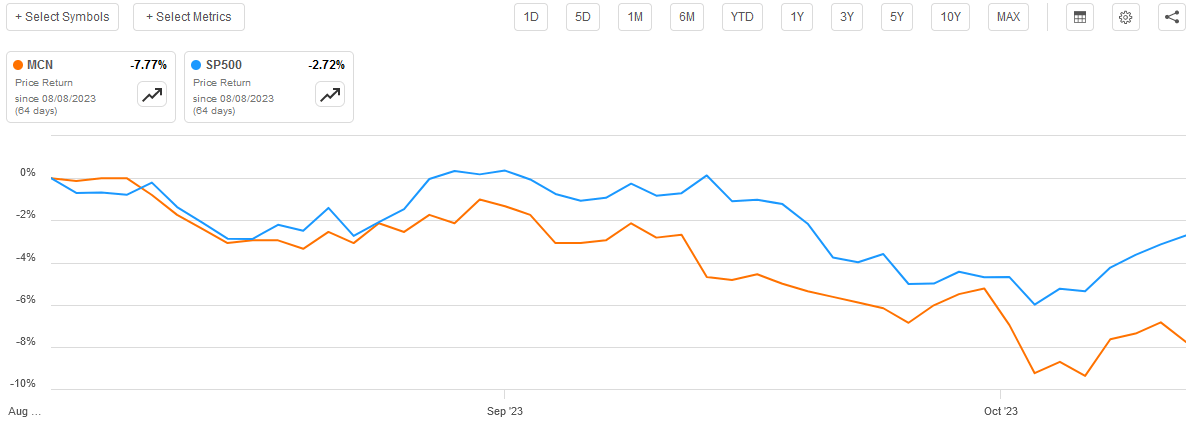

As regular readers may recall, we last discussed this fund back in early August. Unfortunately, its performance since then has left a great deal to be desired, as the fund's shares have underperformed the S&P 500 Index ( SP500 ) by quite a lot. Considering that the S&P 500 Index itself is down fairly considerably over the period, this is saying something:

{kind=link}

Fortunately, the fund does do a bit better when we consider the fact that its distribution will partially offset some of the share price declines, but even then, investors who purchased the fund on the date that my last article was published have lost 5.43%. It is probably a good thing that, while I liked the fund overall, I did not recommend buying it because it traded at a price that was significantly above the intrinsic value of the shares. The fund's shares have declined a bit more than its assets have over the past two months, which has brought the valuation a bit closer to where it should be, but the shares are still slightly expensive.

It is probably a bit redundant to say that conditions in the market have changed quite a bit since early August. After all, it appears that investors, in general, have finally woken up to the very real likelihood that today's high interest rates and tight financial conditions are likely to be with us for quite some time. As a result, they have bid down the price of most assets and capital gains seem to be harder to find. Fortunately, that is exactly the kind of environment that a fund like this thrives in, so it is probably a good idea for us to revisit it today and see if our thesis still remains applicable.

About The Fund

According to the fund's website , the Madison Covered Call and Equity Strategy Fund has the primary objective of providing its investors with a high level of current income and current gains. This is a fairly common objective for a closed-end fund that invests in equity securities, although equities are not generally the best place to invest for people who are looking for income. After all, the S&P 500 Index only yields 1.49% at its current level. In fact, even the traditionally high-yielding utility sector ( IDU ) is rather disappointing with a 2.95% current yield. These figures are both well below what even a bank savings account or money market fund will yield right now. This is the big reason why just about any fund that is focused on the generation of income prefers to invest in fixed-income securities.

In order to overcome this problem, the Madison Covered Call and Equity Strategy Fund employs a somewhat novel strategy to generate income off of an equity portfolio. As the website explains,

We believe these goals can be met by investing in large and mid-capitalization stocks that are, in our opinion, selling at a reasonable price with respect to their long-term earnings growth rates. The income comes in the form of option premiums, which are generated by writing covered calls on a majority of the stocks in the portfolio.

This is a strategy used by other funds such as the BlackRock Enhanced Capital and Income Fund ( CII ) and the two Eaton Vance Enhanced Equity Funds. However, the Madison Covered Call and Equity Strategy Fund has a substantially higher yield than any of these peer funds:

| Fund |

| Current Yield |

| Madison Covered Call and Equity Strategy Fund |

| 10.47% |

| BlackRock Enhanced Capital and Income Fund |

| 6.42% |

| Eaton Vance Enhanced Equity Income Fund ( EOI ) |

| 8.43% |

| Eaton Vance Enhanced Equity Income Fund II ( EOS ) |

| 7.95% |

This could make the Madison Covered Call and Equity Strategy Fund somewhat more appealing to those investors who are seeking a high level of current income from their assets. There is a growing number of people in this category, especially among retirees who are generally dependent on their portfolios for income. The fact that this is the only fund in its category with a yield that can compete with most fixed-income funds is likely to be appealing to those who do not want to give up their equity exposure completely.

The unfortunate downside of this fund's strategy is that it effectively caps the upside potential of that portion of the portfolio upon which call options are written. After all, the fund has to sell the stock at the strike price of the call option if the option gets exercised, regardless of the price of the stock in the market. As this fund has 93.4% of its portfolio overwritten, that is a very big disadvantage to this strategy. However, that disadvantage is mostly only a problem during bull markets. Right now, the stock market is not really appreciating very rapidly, so the odds that an option will actually be exercised against the fund are much lower than it was back during the 2010-2022 bull market. Indeed, covered call strategies are generally known for delivering outperformance during flat or bear markets, which is pretty much what we have today. Unfortunately, though, this fund has not been outperforming the S&P 500 Index recently.

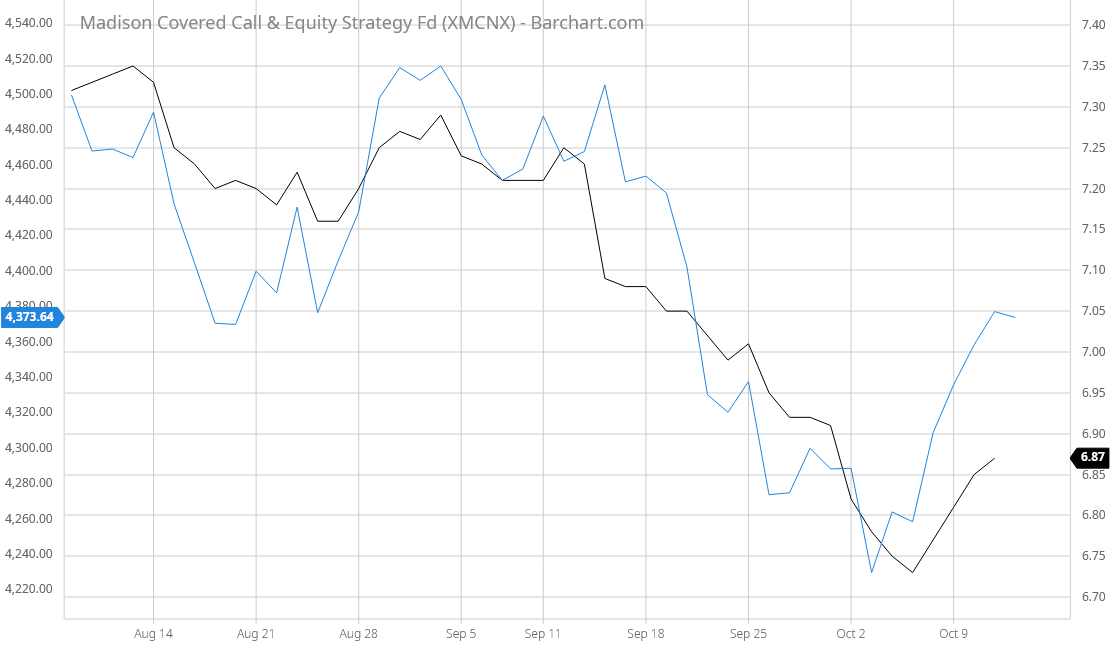

However, we do see a bit of a different story when we look at the performance of the fund's underlying portfolio compared to its share price. This chart compares the fund's portfolio value to the S&P 500 Index from August 8, 2023 (the date that my previous article on this fund was published) to today:

{kind=link}

This is a very different chart to the one that we saw earlier. Here it does indeed appear that this fund does better than the index at times when the index is declining. That is generally what we would expect because the call premiums received should offset some of the unrealized losses from the declining stock prices. At the same time, we do not really expect that an option buyer would actually exercise a call option against the fund because it would pretty much always be cheaper to just buy the stock in the market.

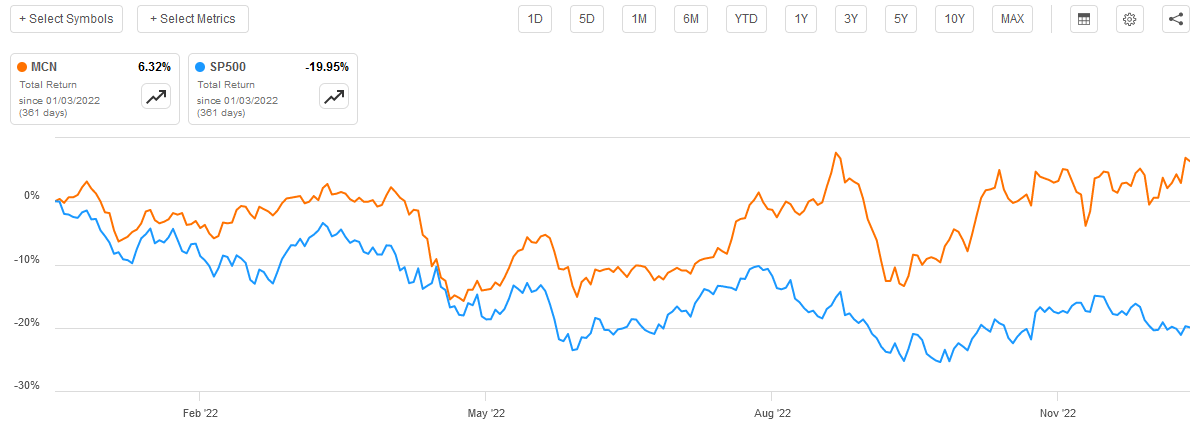

With that said though, the fund's net asset value fell from $7.32 per share to $6.87 per share over the period. That is a 6.15% decline, which is still worse than the S&P 500 Index over the period, but it is much better than the performance that the fund's shares delivered, and when we consider that the fund paid distributions over the whole period, the decline was actually less than that. That still does not change the above statement that the fund's strategy should generally outperform during flat or bear markets. For example, if we look at the fund over the full-year 2022 period, it outperformed the S&P 500 Index by a lot:

{kind=link}

Thus, this fund may be quite useful for someone who expects that we will not see a raging bull market again for a while. I personally am in that category, although I do see a few pockets of the market where opportunities can be found.

As mentioned in the previous article on this fund, the Madison Covered Call and Equity Strategy Fund tends to invest in companies that we do not frequently see among the largest positions in a fund. This continues to be the case, which we can clearly see by looking at the fund's largest holdings. Here they are:

Madison Funds

This is very different than what we normally see in an equity fund. For example, we do not see any of the mega-cap technology stocks that tend to be held by nearly every fund in the market. We also see much more in the way of both energy and basic materials stocks here. This is, to put it mildly, the only broad-market (non-sector specific) fund that I have ever seen with positions in both Transocean ( RIG ), APA Corp. ( APA ), and Barrick Gold ( GOLD ). This is actually pretty nice from a diversification perspective. After all, including this fund in a portfolio that also includes other funds will have the effect of reducing your exposure to certain companies and provide you with exposure to other firms that you may not have had.

There have been surprisingly few changes since the last time that we discussed this fund. In fact, the only major changes here are that T-Mobile US ( TMUS ) and CME Group ( CME ) were removed and replaced with American Tower ( AMT ) and Barrick Gold. When we consider that this fund has a 104.00% annual turnover, that is a surprisingly low number of position changes over a two-month period. Of course, the fund's exposure to Las Vegas Sands ( LVS ) was significantly reduced over the period, so that will also contribute to the fund's trading activity.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Madison Covered Call and Equity Strategy Fund is to provide its investors with a high level of current income and current gains. In order to provide the income component of this objective, the fund employs a strategy of writing covered call options against the individual stocks in its portfolio. This provides these stocks with a synthetic dividend, and the yields can be fairly high. For example, consider the Global X NASDAQ 100 Covered Call ETF ( QYLD ), which writes one-month call options against the NASDAQ 100 Index and consistently generates a yield of around 12% annually. This fund does not do that, as it is not fully overwritten and it does not necessarily write at-the-money call options, but we can still see the yield potential here. When this is combined with any capital gains that the fund manages to realize from the appreciation of the common stocks in its portfolio, we can very quickly see how its investment returns can be quite respectable. The fund collects all of the money that it manages to generate through this strategy and pays it out to its shareholders, net of its own expenses. As such, we can probably expect that this fund will boast a fairly high yield itself.

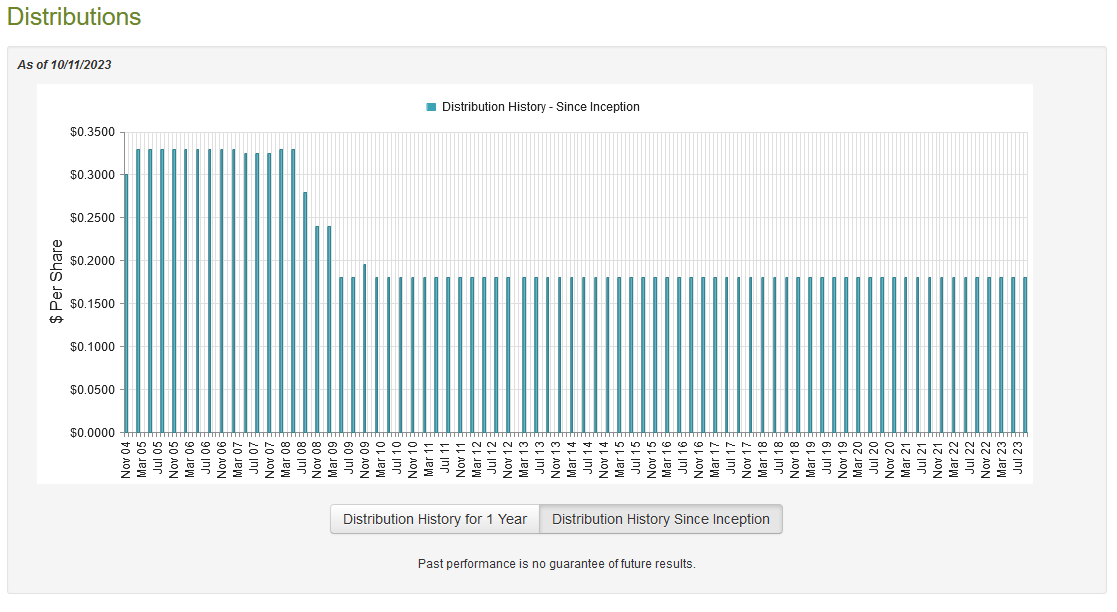

That is certainly the case, as the Madison Covered Call and Equity Strategy Fund pays a quarterly distribution of $0.18 per share ($0.72 per share annually), which gives it a 10.47% yield at the current price. This fund has been remarkably consistent with respect to its distributions over the years, as it has maintained its current payout since May of 2009:

{kind=link}

This consistency will undoubtedly appeal to any investor who is seeking to earn a stable and consistent source of income from the assets in their portfolio. Although we might like a rising distribution during periods of inflation, it is fairly simple to only live on part of the distribution and reinvest the rest so that your income increases every quarter. This track record compares favorably to many other funds in the market, as this is one of the few funds that has not cut its distribution over the past eighteen months.

As is always the case, we want to have a look at the methods through which the fund is financing its distribution. After all, we do not want to be the victims of a distribution cut that reduces our incomes and almost certainly causes the fund's share price to decline.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund, which is nice simply because the fund has paid out distributions for quite some time since the annual report was released. The period of time covered by this report was generally a period of market strength, as many optimistic traders expected that the Federal Reserve would quickly pivot on its monetary policy, reigniting the "everything bubble" and making things much like they were back in 2021. That obviously proved to be a false assumption, but it did provide the fund with the opportunity to generate some capital gains by selling appreciated stocks into the market to earn some quick capital gains.

During the six-month period, the Madison Covered Call and Equity Strategy Fund received $1,088,538 in dividends and $779,407 in interest from the assets in its portfolio. When we subtract the money that the fund had to pay in foreign withholding taxes and add in a small amount of income that was received from other sources, we see that the fund had a total investment income of $1,861,944 during the period. The fund paid its expenses out of this amount, which left it with $1,040,199 available for the shareholders. Obviously, this was nowhere close to enough to cover the distributions that the fund paid out. During the six-month period, this fund paid out $7,567,594 in distributions to its investors. This is something that could be very concerning at first glance as the fund's net investment income was not sufficient to cover its distributions.

However, this fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, the fund might have been able to realize some capital gains through stock sales that can be paid out. It also brings in money through the covered call-writing strategy that is not included in net investment income. Fortunately, the fund did enjoy some success here as it reported net realized gains of $5,821,610 and had another $3,585,068 net unrealized gains during the six-month period.

Overall, the fund's net assets went up by $3,019,150 during the period. It did therefore manage to cover its distributions, although it did have to rely somewhat on unrealized gains to do it. This money can be erased during a weak market, so this is no guarantee that the fund is in good shape. However, this fund does seem to be in better financial shape than many others in the market right now.

Valuation

As of October 11, 2023 (the most recent date for which data is currently available), the Madison Covered Call and Equity Strategy Fund has a net asset value of $6.87 per share but the shares currently trade for $6.81 per share. This gives the fund a 0.87% discount on net asset value at the current price. This is an incredibly attractive price for this fund that ordinarily trades at a premium. In fact, it has averaged a 2.32% premium over the past month.

However, the fund actually opened at $6.88 this morning, which was a 0.15% premium on net asset value. Thus, the fund seems to be pretty close to trading at net asset value right now, and it has been for the past few days. The current pricing seems to be the best that we have seen in a while, as shown here:

CEF Connect

The current price may or may not be a discount as it ultimately depends on just how much the fund's net asset value declined today. However, it is probably okay to buy the fund if you can get it at a small premium since the distribution will offset it after a month.

Conclusion

In conclusion, the Madison Covered Call and Equity Strategy Fund is a closed-end fund that invests in equity securities but still manages to deliver a very high yield to its shareholders. The fund appears to be financially stable, too, which is better than many funds can claim. In terms of valuation, the fund is looking better than it has over most of the past year, so that seems okay too. Honestly, this one might make sense to buy right now.

For further details see:

MCN: This Covered Call Fund Is Getting Much More Attractive