MDU - MDU Resources Group: Backlog Rate Hikes And Infrastructure Funding Should Drive Growth

2023-05-09 15:47:34 ET

Summary

- MDU should benefit from a healthy order backlog, rate hikes, and additional capacity at its plant.

- The funding under the IIJA and IRA should benefit the company in the medium to long term.

- I have a buy rating on the stock.

About the company

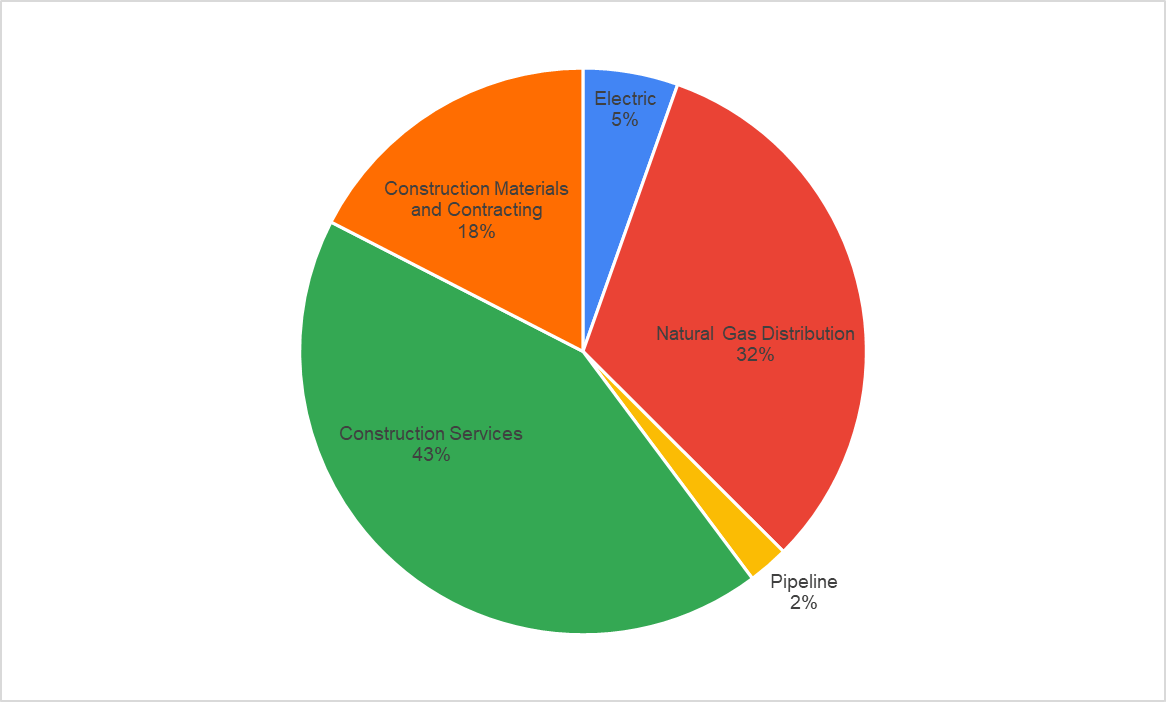

MDU Resources Group (MDU) is a prominent player in the energy delivery and construction materials and services industries. With its diverse portfolio, the company operates through five distinct segments: Electric, Natural Gas Distribution, Pipeline, Construction Materials and Contracting, and Construction Services. However, MDU made a strategic decision to separate its Construction Materials and Contracting business, Knife River, through a spinoff by the end of May. By separating its operations, MDU will be able to enhance its focus on energy delivery in one entity while dedicating the other entity solely to the construction materials sector. This move is expected to unlock new growth opportunities for both entities and provide enhanced value to shareholders, customers, and other stakeholders. As the spinoff nears, MDU stands poised to enter a new chapter, leveraging its expertise and resources to continue thriving in its respective industries.

MDU's segment distribution (Created by DzD Analysis by taking data from MDU)

{kind=link}

Q1 FY23 financial overview

MDU Resources Group recently announced its first quarter FY23 financial results, exceeding expectations and demonstrating solid performance. The company reported a notable 22.6% increase in revenue, reaching $1.74 billion for the quarter, surpassing the consensus estimate of $1.38 billion. This remarkable growth can be attributed to positive developments across all segments, except for the construction materials and contracting segment. Furthermore, MDU Resources Group witnessed a substantial 15.2% year-over-year increase in EBITDA, reaching $167.2 million in the quarter. This growth was primarily driven by successful pricing actions and increased volumes. However, the impact of labor and material inflation partially offset these gains. Despite these challenges, MDU Resources Group managed to deliver strong financial results. Moreover, the adjusted EPS for the quarter experienced a remarkable 43.7% year-over-year increase, reaching $0.23 per share. This impressive performance outperformed the consensus estimate of $0.20 per share. The substantial growth in adjusted EPS reflects the company's effective execution of its strategic initiatives and efficient operations management.

Segment-wise analysis

MDU Resources Group's first quarter FY23 financial results showcased varied performance across its operating segments. In the electric segment, revenue witnessed a $2 million year-over-year increase. This growth can be attributed to interim rate relief in North Dakota and Montana, along with a notable 3.3% rise in retail sales volume driven by increased demand from commercial and industrial customers. The natural gas utility segment experienced a significant 25.5% year-over-year revenue increase. This growth was primarily fueled by improved rate relief in Washington and a 4.2% year-over-year increase in retail sales volume across all customer classes. The colder weather conditions played a key role in boosting sales, although the impact of weather normalization and decoupling mechanisms in Oregon partially offset the gains. Meanwhile, the pipeline business reported a 10% year-over-year revenue increase. This growth was driven by higher transportation volumes, mainly attributable to the successful completion and activation of the North Bakken Expansion project in February 2022. In contrast, the construction materials and contracting segment experienced a 1% year-over-year decline in revenue. This decrease can be attributed to unfavorable weather conditions across the Knife River markets, compounded by the sale of the Beaumont operations at the end of 2022. Record snowfalls in North Dakota, Montana, and Minnesota, along with heavy rain in California, adversely impacted volumes. However, a higher average selling price helped mitigate some of these challenges. Lastly, the construction services segment saw an impressive 37% year-over-year increase in sales. This growth was primarily driven by expanded commercial, industrial, and institutional workloads. However, lower renewable workloads presented a partial offset to the overall increase.

Outlook

Looking ahead, in the electric and natural gas segments, revenue growth should be driven by rate hikes and a growing customer base. The rate base in 2022 increased by 7.8%, and I believe it should continue to be in that range given the increased consumption.

I believe the pipeline business is poised to benefit from the continued impact of the North Bakken expansion project, which commenced in 2022. Additionally, MDU Resources Group is actively working on three gas pipeline expansion projects expected to be operational later in 2023. These projects, including the addition of a compressor station, a 15-mile pipeline in North Dakota, and a compression unit in western South Dakota, will collectively increase the segment's capacity by approximately 300 million cubic feet per day. Furthermore, the company has filed for a rate increase with the Federal Energy Regulatory Commission (FERC) for transportation and storage services, with the approval expected to take effect in August 2023.

In the Construction Services segment, I believe the healthy backlog should drive revenue growth in 2023 and beyond. The backlog witnessed a notable 25.8% year-over-year increase, reaching $2.1 billion in Q1 FY23. This surge can be attributed to new project opportunities in the commercial, industrial, institutional, and transportation markets. The transportation market has the largest percentage of its backlog due to two key projects, including a streetcar expansion project and a U.S. 69 Expressway project. Moreover, the segment stands to benefit from federal and state-level funding initiatives. Notably, the Infrastructure Investment and Jobs Act (IIJA) has allocated $1.3 trillion for transportation systems, electric and grid infrastructure, and other programs, while the Inflation Reduction Act (IRA) has provided $369 billion for clean energy programs. These funding sources, coupled with the strong order backlog, present promising opportunities for the Construction Services segment.

Overall, I believe MDU is well-positioned for revenue growth in the near-to-medium term. The company's strategic focus on rate hikes, a robust order backlog, increased plant capacity, and the favorable funding environment will support its overall growth trajectory.

Valuation

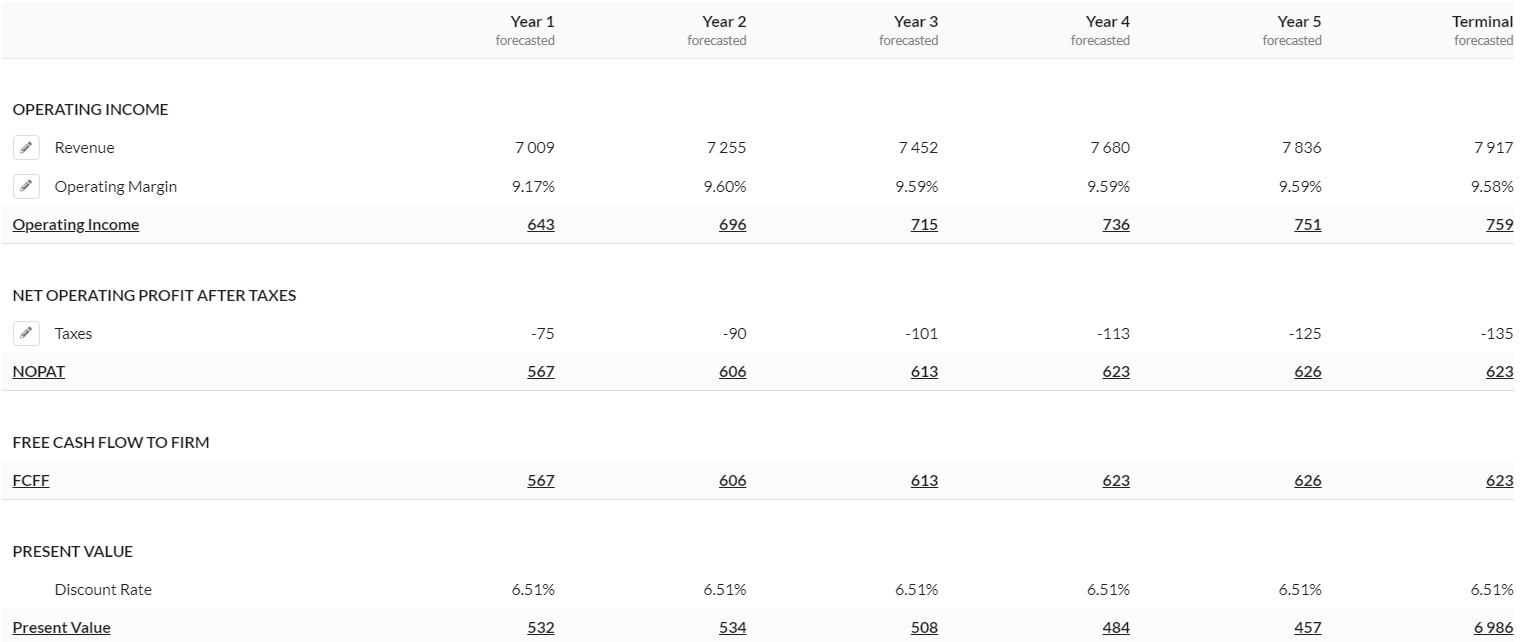

DCF valuation (Created by DzD Analysis using Alpha Spread)

{kind=link}

In my DCF calculations, I am assuming revenue growth to be flat Y/Y in 2023, given the tough year-over-year comparison and the separation of Knife River. Beyond 2023, I have assumed growth to be in the low-single digits, with a terminal growth rate in the low-single digits, as the company will continue to benefit from infrastructure funding, increased capacity, and rate hikes. I used a discount rate of 6.51% by using the cost of equity of 7.23% and arrived at a fair value of $33.02 for MDU.

Conclusion

Rate hikes, a robust order backlog, increased plant capacity, and a favorable funding environment collectively position MDU Resources Group for sustained growth in the near-to-medium term. With its strategic focus on meeting customer needs, pursuing regulatory recovery, and leveraging market opportunities, the company is well-equipped to create value for its shareholders, customers, and other stakeholders. As the company continues to execute its strategic initiatives, it is poised to maintain its upward trajectory and further solidify its position in the energy delivery and construction services industries. Hence, I have a buy rating on the stock.

For further details see:

MDU Resources Group: Backlog, Rate Hikes, And Infrastructure Funding Should Drive Growth