MFIN - Medallion Financial: An Agile Company In A Cyclical Environment

Summary

- Medallion Financial Corp. maintains a well-balanced growth, with its stable revenues and margins.

- It has a distinct business model that has decent prospects this year.

- Liquidity remains impressive, allowing it to sustain and even expand its capacity.

- Dividend payments have resumed after years of cuts.

- The stock price has been moving sideways with upward potential.

Medallion Financial Corp. (MFIN) maintains operational stability amidst market volatility. Its well-diversified portfolio remains one of its cornerstones. Also, it maintains an excellent financial positioning with excess liquidity. This aspect allows it to cover the operating capacity without depleting cash reserves. As such, MFIN remains a secure company with high-risk tolerance amidst macroeconomic changes.

Even better, the company has resumed its dividends after years of no payouts. It can cover dividend payments even without raising borrowings or reissuing shares. Meanwhile, the stock price moves sideways and reflects the company's intrinsic value.

Company Performance

Medallion Financial Corp. is a company operating in a highly cyclical industry. But it has emerged unfazed as it sustains its robust performance while hedging risks. It has capitalized on prudent expansion and portfolio diversification. It has added and sold several private placements for the past two years. And now, its effort continues to pay off as its commercial and consumer lending remains robust.

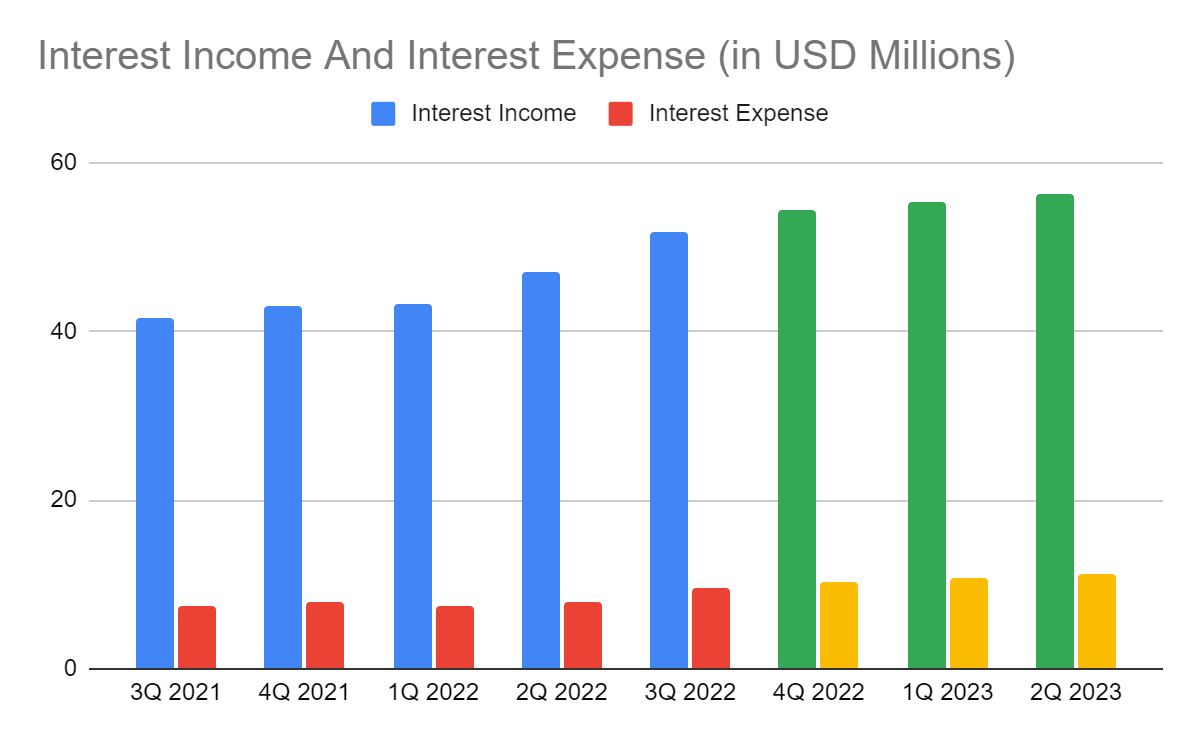

The operating revenue amounts to $51.56 million, a 5% year-over-year growth. It is primarily composed of interest income, with $51.69 million, a 25% year-over-year growth. The remaining components are deductions, such as valuation losses and collateral foreclosure. Interest income keeps increasing in line with interest rate hikes, thanks to the interest-sensitive Balance Sheet that optimizes portfolio yields. Loans remain well-diversified across different segments. Most are recreational loans. It can be risky now as fuel prices remain high. But the upsurge in travel demand and the easing of restrictions in the US appear to offset inflation. After all, fuel prices are now more stable than in 2Q 2022. The second-largest loan component is home improvements. These loans may be influenced by changes in the real estate market. As of mid-4Q 2022, property construction starts have risen by 17% . It may remain unchanged, despite worries over potential economic stagnation. The remaining components are commercial, strategic partnerships, and Medallion loans. They also show impressive growth, except for Medallion loans. These loans have also been suitable for the 2022 market conditions. It is no surprise loan originations rose on higher interest rates.

The other revenue component is interest and dividends on investment securities. It also reflects prudent and efficient management of interest-sensitive assets. Investment securities also fit the high-interest market environment due to their nature. All of them are backed by the federal and municipal governments. As such, they are more flexible to changes and can hedge valuation loss risks better.

Interest Income And Interest Expense (MarketWatch And Author Estimation)

{kind=link}

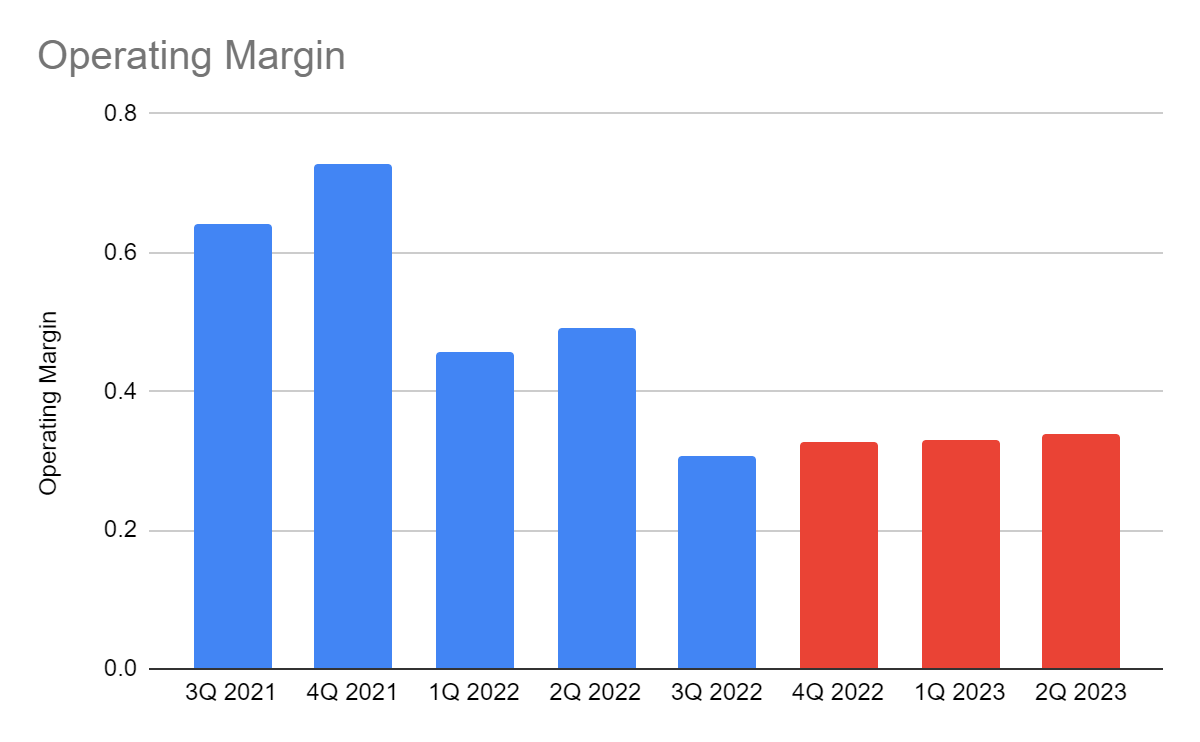

Interest expense also increases since deposits and borrowings are sensitive to interest rates. It amounts to $9.65 million, a 30% year-over-year growth. Despite this, net interest income stays in an uptrend, reaching $42 million. Even better, non-interest expenses remain stable despite the elevated inflation. The net value will still be in an uptrend even if we deduct them from net interest income. From there, we can see MFIN handles its interest-bearing assets and liabilities prudently. It also keeps improving its operational efficiency to cope with inflation. However, the operating margin is only 31%, less than half its value in 3Q 2021. Nevertheless, the massive decrease is still logical. Provisions are high, comprising 20% of interest income on loans. It is a conservative and strategic move since the risks are higher. Also, the company reflects the impact of equity investment valuation losses. The thing is, the core operations remain viable amidst drastic market changes.

This year, I expect Medallion Financial Corp. to maintain its solid core operations. Interest income may still increase, although income growth may cool down. I attribute it to higher interest rates, booming tourism, and property and RV demand. They may offset each other, leading to an almost unchanged outcome. As for the operating margin, I expect it to be more stable with a slight increase. The inflation lull may help stabilize non-interest expenses and the valuation of securities.

Operating Margin (MarketWatch And Author Estimation)

{kind=link}

How Medallion Financial Corp. May Fare This Year

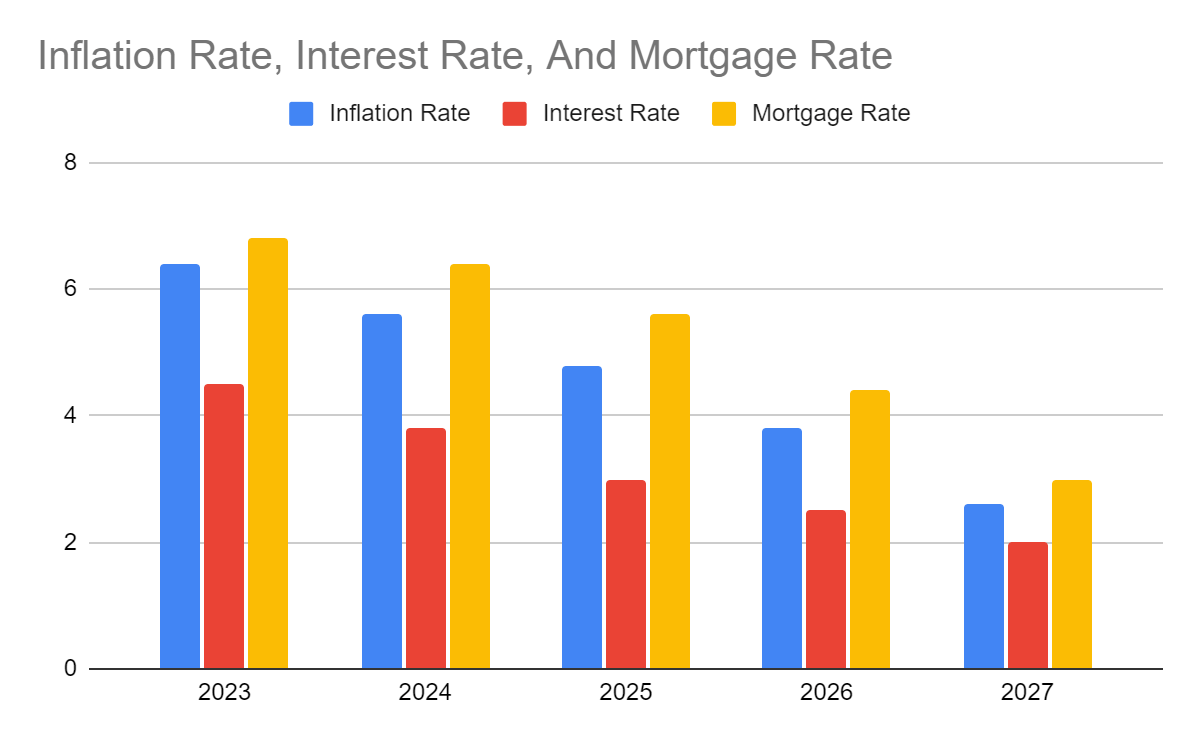

I expect Medallion Financial Corp. to stay solid, although near-term growth prospects may be less robust than in 2022. But I stay optimistic about its performance, given its current portfolio and fundamentals. It can cushion the blow of a potential recession and bounce back. With its well-diversified interest-sensitive assets and excess liquidity, MFIN is well-prepared for it. I expect the recession to be less intense than expected. We must consider that inflation is driven by excessive demand, not the cost of production. Also, the inflation lull has sped up as it lands on 6.5% from the 9.1% peak. With that, I expect interest rates to keep rising, but increments may flatten. I estimate it at 4.5-4.8% versus the 5-5.25% estimates.

Interest Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

Regarding its home improvement loan segment, I believe it will stay secure. I also don't agree with the supposition of a housing crash due to low property inventory. So as sales cool down, mortgage rates may decrease but remain slightly elevated. In turn, home improvements may remain a staple. The prevalent remote work setups may drive home improvement loans. Although it's more behavioral, this observation may be logical. Meanwhile, recreational loans may see contrasting changes due to market changes. This year, RVs and recreational boat demand may normalize and change with seasonality. Aside from interest rates and fuel prices, changes in trip plans may have an impact. In a recent study, 96% of Americans will travel more this year. About 80% of them will either spend the same or higher on travel. In another report, there is a 13% increase in travel plans with RVs. Demographic changes also play an integral role here. Millennials comprise the largest portion of potential RV buyers or renters. It shows the sustained strength of the RV industry and the essence of recreational loans. The top reasons for buying RVs are more predictable travel costs and privacy.

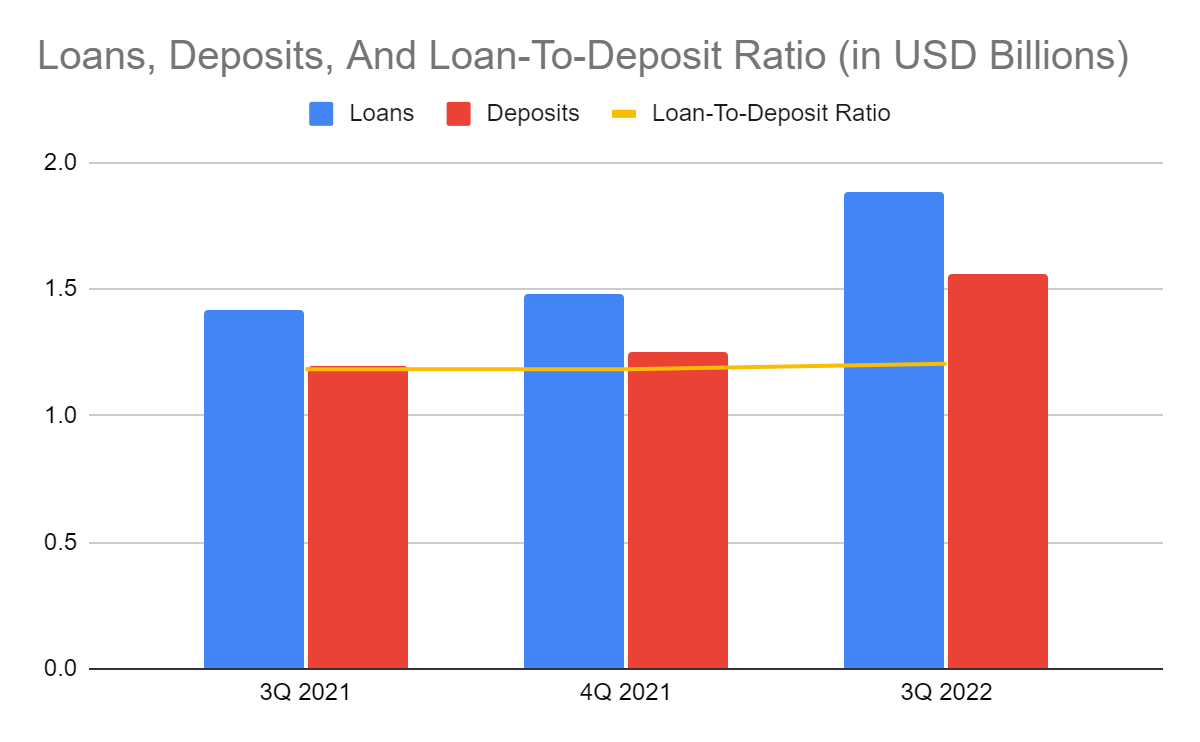

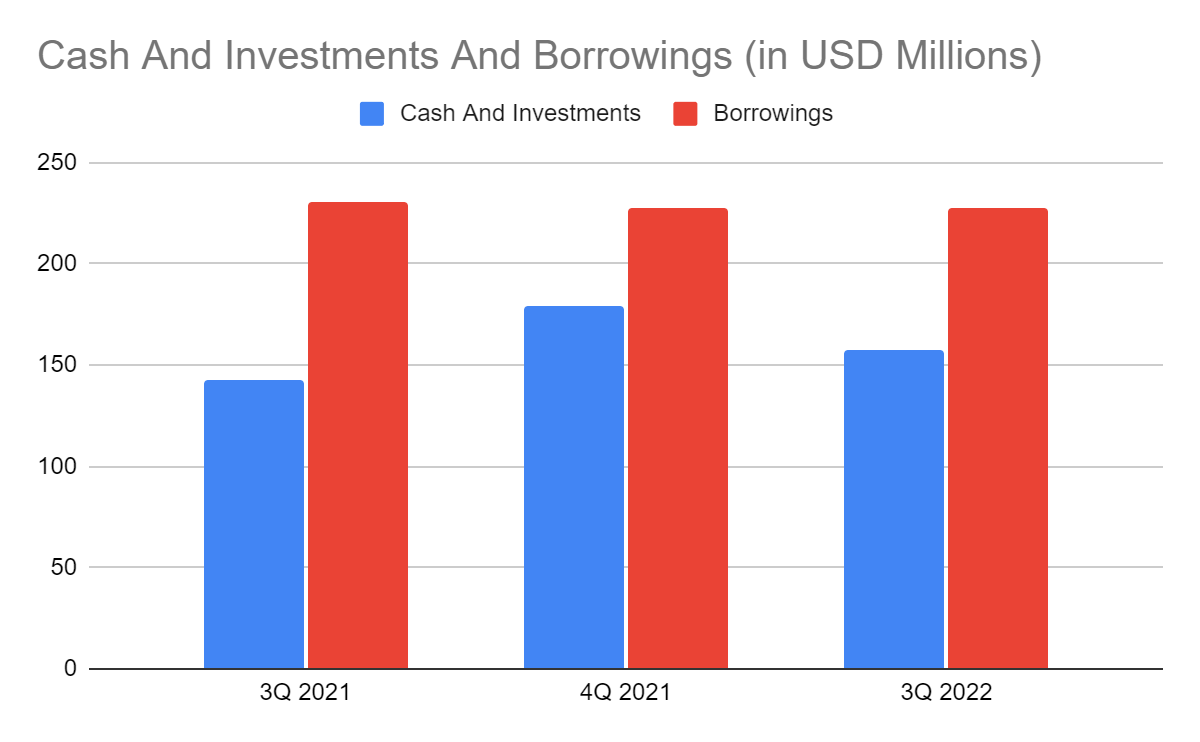

What makes MFIN highly secure is its financial preparedness for market changes. Its solid financial positioning shows excess liquidity, which is one of its strongholds. Loans and deposits increase proportionately. Its loan-to-deposit ratio of 120% remains almost unchanged. Initially, it can be alarming, given the limited reserves. But given the higher loan originations and yields, lending can help the company. Also, it has ideal loan quality with lower delinquencies and non-performing loans. Provisions are 3% of loans and way higher than in the previous quarters. If that's not enough, the company may increase its interest rates to entice more deposits. Even better, cash and borrowings are stable, which shows excess liquidity. It is vital for its sustained capacity in a high-interest market landscape. Its Net Debt/EBITDA is less than 1x, so it is earning more than enough to cover borrowings. So, it proves prudence and efficiency in managing the interest-sensitive portfolio, maximizing returns. It also shows the maintained balance between its growth and fundamental stability.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch) Cash And Investments And Borrowings (MarketWatch)

{kind=link}

{kind=link}

Stock Price Assessment

The stock price of Medallion Financial Corp. has been moving sideways after rebounding from its dip. The uptrend is more prominent but did not bounce back to 2022 highs. At $7.94, it remains over 20% higher than its value last year but 13% lower than the peak. Despite this, the PE Ratio is not convinced about its actual value. If we multiply the price-earnings multiple of 3.89x by my estimated EPS of $1.55, the target price will be $6.03. NASDAQ is more optimistic with an estimated EPS of $1.62 and a target price of $6.30. Either way, there may be a 20-24% downside. Meanwhile, there may be an opposite price pattern if we use the tangible book value. Currently, the TBVPS of the company is 5.09 while the PTBV is 1.56x, lower than the average of 1.88x. If we use the current TBVPS and multiply it by the average PTBV the target price will be $9.56, a 20% upside. It shows that the stock price is reasonable as it reflects the intrinsic value of the company. We can see increasing tangible book value. It sustains expansion while preserving shareholder value.

Moreover, dividend payments are back, with exciting yields of 4.03%. It is way better than the NASDAQ average of 1.30%. Also, dividend payments remain well-covered, given the dividend payout ratio of 19%. To assess the stock price better, we will use the DCF Model.

FCFF $11,990,000

Cash $98,200,000

Borrowings $228,200,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 23,180,000

Stock Price $7.94

Derived Value $7.24

The derived value agrees with the potential undervaluation using the price-earnings multiple. There may be a 9% downside in the next 12-18 months. Now, there is a 2-1 observation among the three price metrics. Investors must be more careful before making a position. But if we observe the trend, we can see how the stock price appears sensitive to the EPS. We can also see that as long as the actual EPS beats the estimates the uptrend takes place and persists. Hence, the safest advice is to wait for the 4Q report.

Bottomline

Medallion Financial Corp. is a solid company with well-balanced growth and fundamental stability. Its well-diversified portfolio and excess liquidity provide its cushion for a potential recession. It can also cover borrowings and dividends using its adequate cash reserves. Meanwhile, the stock price moves sideways while metrics show mixed observations. As discussed, the stock price pattern seems to follow the actual versus estimated EPS. It may be a smart move to wait for the 4Q report before making a position. The recommendation, for now, is that Medallion Financial Corp. is a hold.

For further details see:

Medallion Financial: An Agile Company In A Cyclical Environment