MFIN - Medallion Financial: Cyclical Industry Rising Interest Rates And Competition

2023-10-06 18:30:11 ET

Summary

- Medallion Financial is a financial services company specializing in home improvement and RV loans.

- The company faces challenges due to a cyclical industry, rising interest rates, and competition.

- The RV and home improvement industries have shown signs of weakness, impacting Medallion's financial performance.

Introduction

Medallion Financial ( MFIN ) is a financial services company mainly financing home improvement and RV loans. The company has a strong track record of profitability and growth in both industries and a deep understanding of the RV and home improvement industries. Furthermore, the reduction of its medallion segment is probable to increase its profitability. However, Medallion faces a number of challenges, including a cyclical industry, rising interest rates, and competition.

Business Overview

Medallion Financial is a specialty finance company that provides financing for home improvement, RV, boat loans, and commercial loans. The company funds its operations through various interest-bearing sources, including bank certificates of deposit issued to customers, debentures issued to and guaranteed by the SBA, privately placed notes, and preferred securities. In addition to interest income, the company also earns income from debt, mezzanine, and equity investment capital to companies in various commercial industries.

Medallion Financial started providing loans to taxi medallion owners, but the medallions lost almost all their value owing to the rise of Uber ( UBER ) and Lyft ( LYFT ). Thus, to avoid going out of business, the company began to provide loans for recreational vehicles, boats, motorcycles, and home improvements. Furthermore, it started commercial loans. At the end of 2022, the medallion segment comprised less than 1% of the total loans receivable. Hence, the results from the segment won't affect the financial performance.

Some Clouds On The Horizon

Medallion relies heavily on two cyclical industries: RVs (including boats and motorcycles) and home improvements. Both industries have shown signs of weaknesses in 2022 and 2023 as interest rates and living costs rise. For instance, the shipments of RVs plummeted during 2022 and the first half of 2023, according to RV News .

RV News RV News

I expect fewer shipments for the rest of 2023 than in 2022 as interest rates keep increasing and the economy continues its slowdown, reflecting a highly cyclical industry.

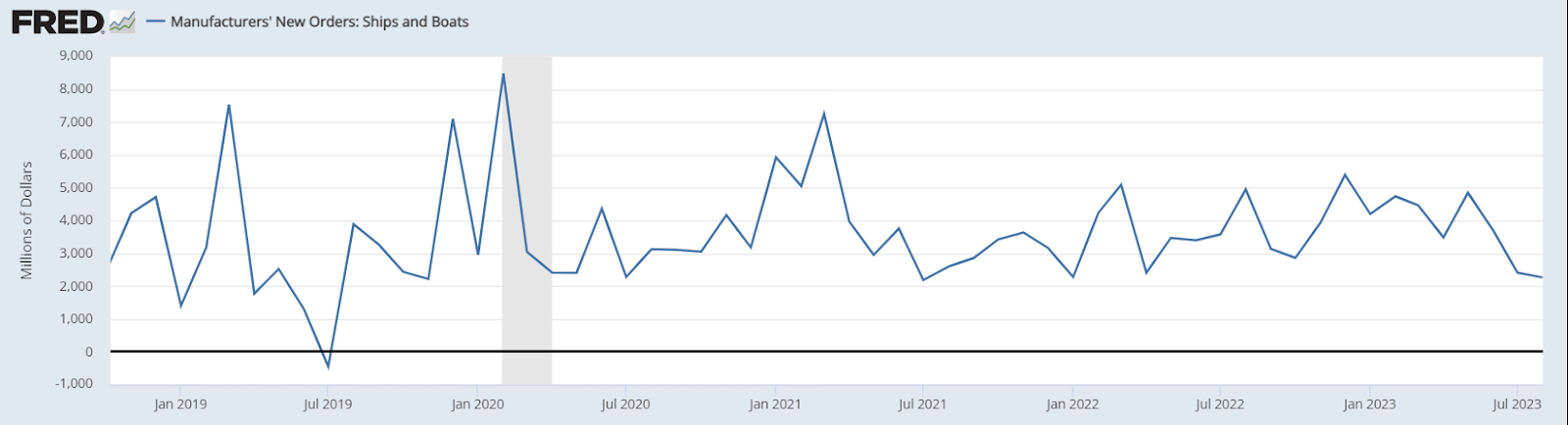

Nevertheless, the boat market remained flat relative to the previous two years. Still, in recent months (since December 2022), there has been a downward tendency in the value of Manufacturers’ New Orders. At the moment of writing this article, the value of orders is close to the minimum of the last two years; hence, I think the industry is undergoing an adverse cyclical swing.

{kind=link}

Nonetheless, Medallion doesn’t have to replace its current loans with new ones, as the weighted average maturity in the recreational segment is 9.9 years . Thus, I believe the slowdowns in the boat and RV segments will only decrease the interest income growth rate rather than the interest income as an absolute measure. Even so, the net interest income has been affected, as the firm has to pay more interest on its deposits and higher provisions for credit losses. The latter increased principally due to adopting the CECL accounting standard and rising loss rates. Nevertheless, I don’t think the rise in provision is worrying, as the delinquency status stood at 0.39% in 2Q23, which is low considering how the industry and other types of credit are doing it. For example, the delinquency rate on credit cards is 2.77% , and the auto loan delinquency rate is 3.82% . However, in the case of credit cards, delinquent debt is defined as 30 days or more past due, while the company stipulates a delinquent debt as 90 days or more past days, limiting the compatibility of the measures.

Nevertheless, the charge-off ratio passed from 0.56% to 1.86%, so some indicators are alarming even if the credit conditions are not deteriorating significantly.

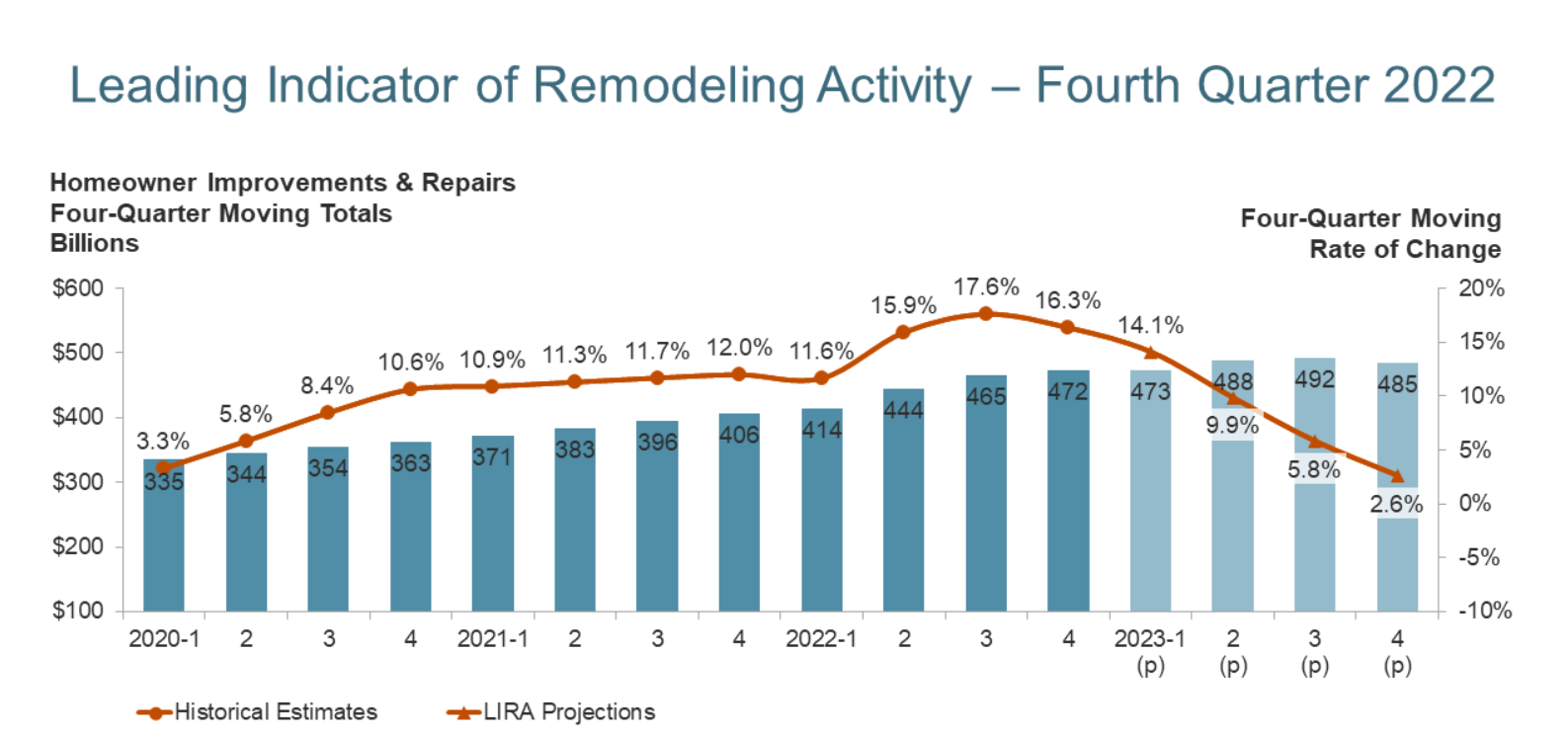

Regarding the home improvement segment, the Leading Indicator of Remodeling Activity ((LIRA)) projects a sudden deceleration in the expected reparation and improvement expenses in 2023. The LIRA showed double-digit growth in the home reparation and remodeling industry during 2022; however, it estimates only a gain of 2.6% in the last quarter of 2023. Hence, as the recreational segment, it’s reasonable to expect lower growth as the demand for improvement projects slows.

{kind=link}

The worsened conditions in the market are affecting the financial performance of Medallion, as the ROA in the segment has fallen from 2.49% to 1.28%, owing to an increase of approximately 94.32% in the provision for credit losses (after adjusting them by CECL standard). Furthermore, the delinquency status passed from 0.07% to 0.16% (more than double) in 2Q23, pointing out worsening customers’ financial conditions. Even the charge-off ratio stood at 1.12% in 2Q23, when it was only 0.42% in 2Q22.

However, the loans originated in the recreational and home improvement segments are fixed-rate, and the sources of reserves bear variable interests, principally the deposits, which account for 87.95% of total liabilities. Moreover, the mismatch between the maturity of liabilities and assets worsens this problem, as the company will need to refinance 37.38% of its certificate of deposits in less than a year (and 31.01% in less than two years). The refinance will probably be carried at a higher interest rate; consequently, the net interest margin ((NIM)) may shrink further. Furthermore, as there is less demand in both segments, I expect Medallion cannot improve the NIM with higher interest on new loans. For example, although the interest rates are soaring in 2023, the interest yield in the home improvement segment has barely increased from 8.51% in 2Q22 to 8.79% in 2Q23. The same applied to the recreational segment, whose interest yield in 2Q22 was 12.83% and in 2Q23 was 13.03%.

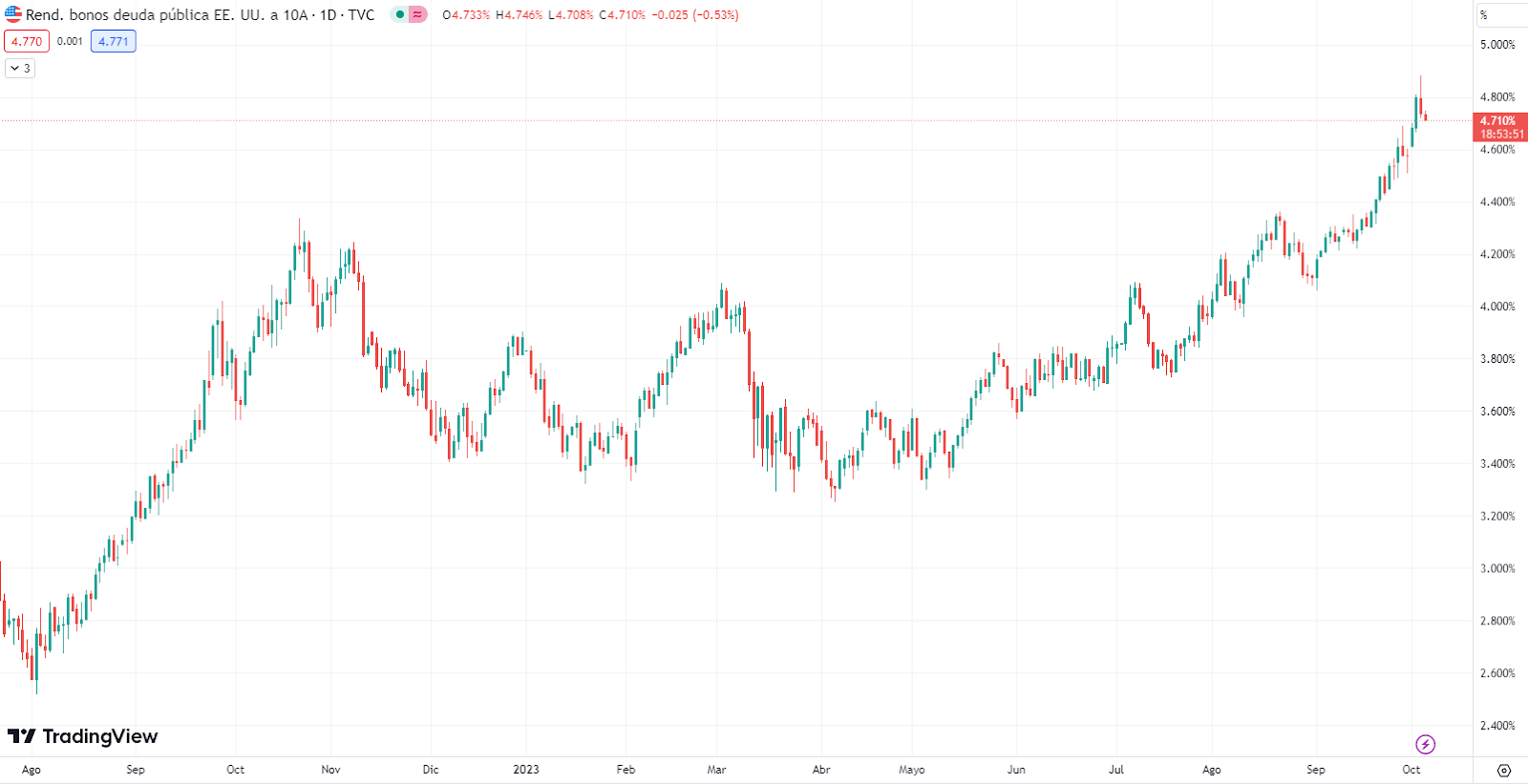

As the interest rates soar further, I expect the ROA and ROE to continue to decline as the NIM decreases owing to a higher cost of funds. It’s virtually impossible to predict where the interest rates will stop; however, the FED is committed to its politics ‘higher for longer.’ Meanwhile, the 10-year Treasury Bond Yield is already at 4.71%.

{kind=link}

Nevertheless, I believe Medallion is in a healthy financial position thanks to the low delinquency rates, along with ‘good’ (recreational) and ‘very good’ (home improvement) FICO scores. Furthermore, as of June 30, the company has an asset-to-equity ratio of just 6.49, which is lower than many banks; hence, the company is conservatively leveraged. Also, the company has reduced the total amount of long-term debt (from $214 million to $178 million), which bears an interest rate of 7.68% (weighted average), and increased its cash reserves from $33 million in December 2021 to $82 million. Even if higher cash reserves may impair the margins, they decrease the distress risk without incurring losses as the company can find acceptable yields in the money market securities, which are higher than the interest rate of its liabilities (3.05%). Consequently, I consider the firm maintained a healthy balance sheet as of June 2023. Nevertheless, a fast deterioration in the quality of its loans could impair its ability to honor its obligations; however, it seems improbable, given the low delinquent rate.

Competition and Long-term Prospects

The lending market is highly competitive, mainly due to the pricing competition (loan interests). Thus, other lenders always try to offer the lowest interest rate given the risk to customers. In this sense, Medallion competes with other lending in the RV and home improvement industries and with any other lending company in the consumer credit industry. Of course, Medallion has an advantageous position over non-niche players, as it has an extensive network of dealers, contractors, and financial service providers, as well as a better knowledge of the industries. Nevertheless, compared to other niche players, this advantageous position fades. Voyager Credit, My Financing USA, and Southeast Financial are some of its competitors in the RV market. Consequently, I don’t expect the company to have better financial performance than other competitors in the long term.

The RV industry is expected to grow at a CAGR of 8.15% , the global boat industry is expected to grow at a CAGR of 6.4% , and the home improvement market at a CAGR of 4.3% . Thus, over the long term, it’s plausible to say the company will have enough demand to keep growing. Furthermore, I believe the company will be more profitable than in the past, as its medallion segment has declined significantly in volume after hindering sales in the pre-pandemic years.

The average ROE of the recreational segment in recent years is 24.02% or 23.02%, excluding 2021, which was an exceptional year for the industry that hardly will happen again. The worst year for the segment was 2019, when the charge-off ratio soared to 2.50%, and the NIM decreased from 14.18% to 13.33%.

Author's Elaboration with data from Annual and Quarter Reports

*Medallion adopted the CECL Standard

Furthermore, the NIM has been decreasing since 2018. The ROA and ROE have reduced from 2021 levels, and I believe it’s highly probable they will keep falling in 2023 and 2024 because the interest rates increase, making the NIM narrower, and the adoption of the CECL accounting standard. If interest rates decline before 2024, the company will face a more favorable environment.

In my opinion, in the long term, Medallion will be capable of maintaining a ROE of at least 17% in the recreational segment, given its historical performance. Nevertheless, the high ROE comes with a higher risk, as the industry is highly cyclical, and the loans bear fixed interest rates, making the business vulnerable to business cycles.

Relative to the home improvement segment, the average ROE is 11.03% and 10.36% if 2021 is excluded. However, the ROE in the last two quarters fell under 10%, and the charge-off ratio increased rapidly since 2022. Thus, the consumers’ credit conditions in the home improvement market are decaying; the effect of the CECL standard in the home improvement segment is not as significant as in the recreational segment, as the provision for losses in this segment only increased by 13.39% after adopting it.

Author's Elaboration with data from Annual and Quarter Reports

*Medallion adopted the CECL Standard

Valuation

Medallion originated most of its loans when the interest rates were low. Now, the business faces an increase in its interest costs as deposits bear a higher interest rate, most of which are due in the next two years. Moreover, as most of its loans are in cyclical industries, the current demand is slowing, and replacing low-interest yield loans with new high-interest yield loans is challenging. That’s why I think the return in 2023 and 2024 will be disappointing compared to past years. Moreover, if interest rates do not fall or the demand does not recover, Medallion could expect a lower return even in the medium term (2 to 3 years). Nevertheless, as the medallion segment has almost extinguished, it won’t decrease the financial performance as it did in 2018 and 2020 when the charge-off ratio soared to 59.3% (2020), and the delinquency ratio was 9.43% (2018), increasing the provision for losses. Hence, I believe the P/B could be higher if credit conditions improve. Furthermore, I expect the company to keep positive EPS, which has not been the case for pre-pandemic years, as the medallion segment was hampering financial results.

Author's Elaboration with data from QuickFS

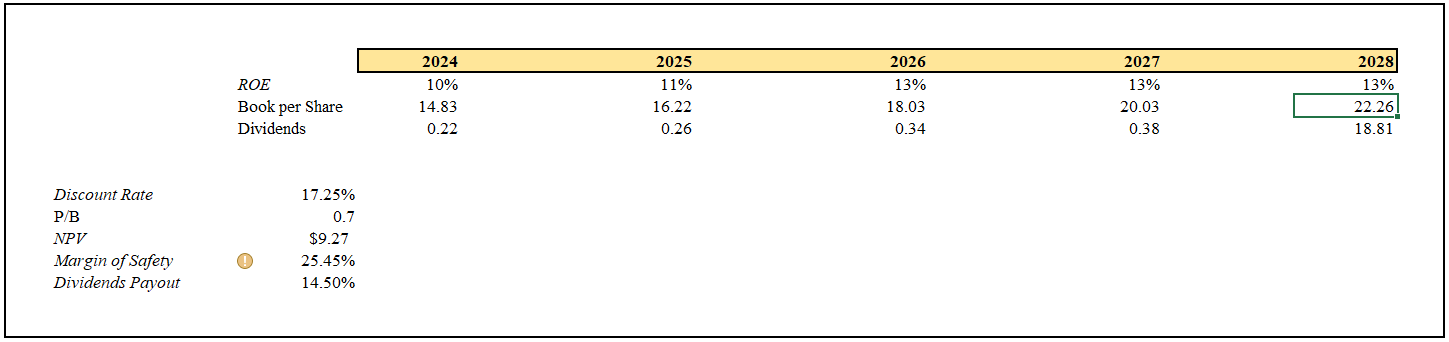

For my DCF model, I assume that the company will achieve a ROE of 10% in 2024, as lower demand and higher interest rates lead to a narrower NIM. I expect better credit conditions in 2025, thus a ROE of 11%. For the rest of the projection, I'll use a ROE of 13%, as the recreational segment (average ROE of 24.02%) currently accounts for approximately 57.29% of total earning assets, and the home improvement segment (average ROE of 11.03%) accounts for 31.60%. Notably, 13% is lower than the ROE weighted average of both segments (even if the other 10% has a zero return), but I think it is too optimistic to project a higher ROE, as the underlying industries experienced a unique strong growth. Furthermore, the discount rate will be 17.25% because I believe the business model is highly vulnerable to business and credit cycles.

{kind=link}

According to my DCF, Medallion is a 'Hold' as the margin of safety is not enough to protect from the downside risk. Moreover, I will wait for signs indicating a change in the interest yield upward tendency because there’s a risk of important underperformance if interest rates keep increasing and the demand for Medallion’s loans freezes more.

Conclusion

In my opinion, the risks outweigh the rewards at this time. Investors should closely monitor the company's financial performance in this challenging environment, seeking indicators that announce a turnaround. However, the long-term prospects of the RV and home improvement industries may bring a future recovery. Even so, the Medallion business model keeps being vulnerable to business cycles.

For further details see:

Medallion Financial: Cyclical Industry, Rising Interest Rates, And Competition