SBRA - Medical Properties Trust: Fantastic Upside Warranted Despite Its Recent Slide

Summary

- Medical Properties Trust was hit hard the other day due to reduced expectations regarding the 2023 fiscal year.

- Though disappointing, this does nothing to change the fact that shares look very cheap right now.

- The firm may not be as attractive as I previously thought, but its low valuation and continued improvements justify upside moving forward.

Most investors, including the best investors, will often have one or two holdings in their portfolio that they dub their 'problem children'. These are the holdings that are drastically underperforming expectations. In my case, I currently have two out of 10 holdings that I would classify in this manner. One of them, the firm that has been hit the hardest, is Medical Properties Trust ( MPW ). Despite being down 31% on the business since acquiring stock in it in March of last year, I remain confident that the company is drastically undervalued and will eventually generate an attractive return for me. Although the market did not behave kindly to the financial results that the company reported for the final quarter of its 2022 fiscal year, the data in its entirety demonstrated once again just how cheap shares of the business are. In all fairness, the developments that were made public suggest to me that the upside may not be quite as great as I thought when I first purchased the stock. But it is high enough that I believe the 'strong buy' rating that I assigned the business previously still makes sense.

A decent quarter

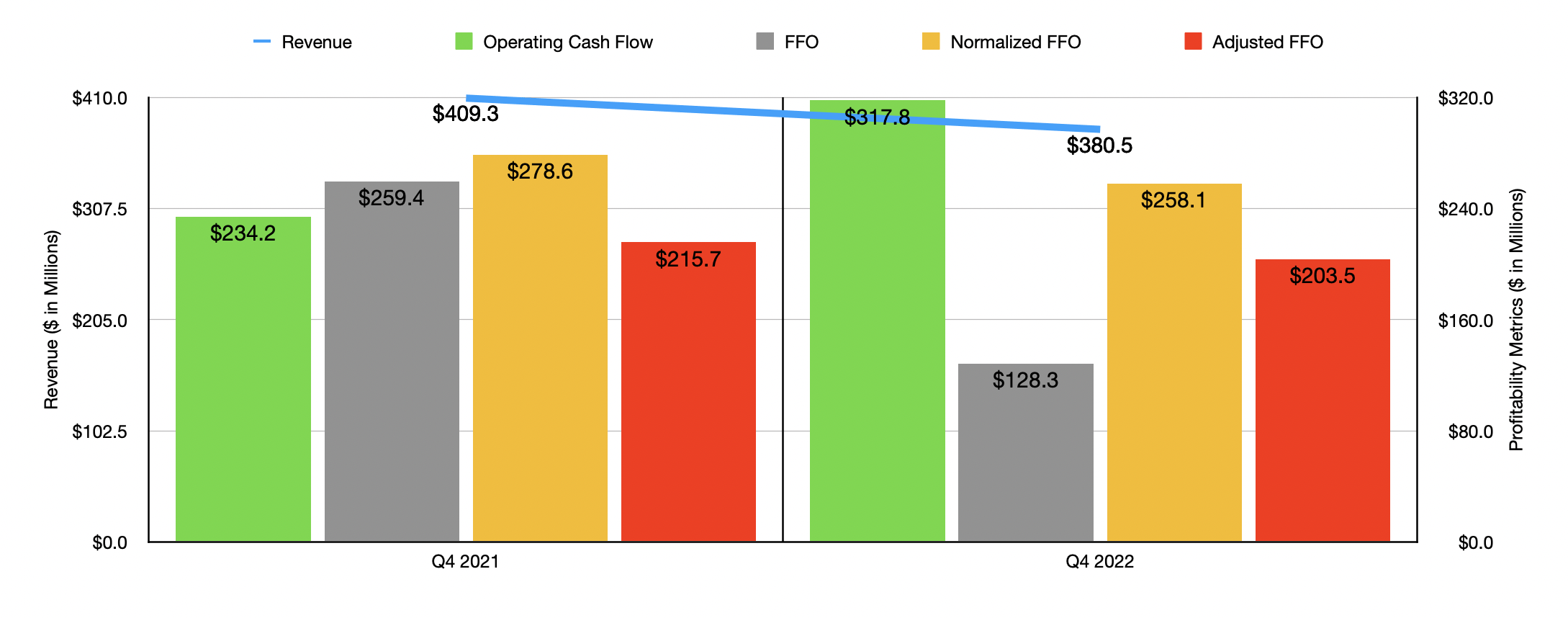

On February 23rd, before the market opened, the management team at Medical Properties Trust announced financial results covering the final quarter of the company's 2022 fiscal year. In response to the data reported, shares of the REIT plummeted 8.7% for the day. Interestingly, if you focus solely on the headline news reported by management, you might be perplexed as to why shares dropped at all. Revenue, as an example, came in during the quarter at $380.5 million. While this was down from the $409.3 million, the company reported the same time one year earlier, it did come in higher than what analysts anticipated by nearly $7.5 million.

{kind=link}

While revenue is important, what's more important for any business is the amount of profitability it generates. Typically, net income is not all that important for a REIT. But there are other profitability metrics that investors should be paying attention to. For starters, we have FFO, or funds from operations. This number came in at $0.21 per share, down from the $0.43 per share reported one year earlier. But on a normalized basis, it totaled $0.43 per share compared to the $0.47 per share reported the same time of the 2021 fiscal year. While any kind of decline can be construed as a negative, it's important to note that this number was in line with what analysts anticipated.

Total FFO for the company came in at $128.3 million. That was down from $259.4 million reported one year earlier. Adjusted FFO, meanwhile, dipped from $215.7 million to $203.5 million. There's also EBITDA to consider. Unlike the FFO variants, EBITDA actually increased year over year, rising from $373.5 million to $424.5 million. Generally, I would also like to look at operating cash flow. Unfortunately, management has not revealed these numbers yet. More likely than not, they won't be released until the company releases its 10-K in the coming days or weeks. For context, the company required nearly a month after releasing its fourth quarter results in 2022 for the 2021 fiscal year before releasing its 10-K.

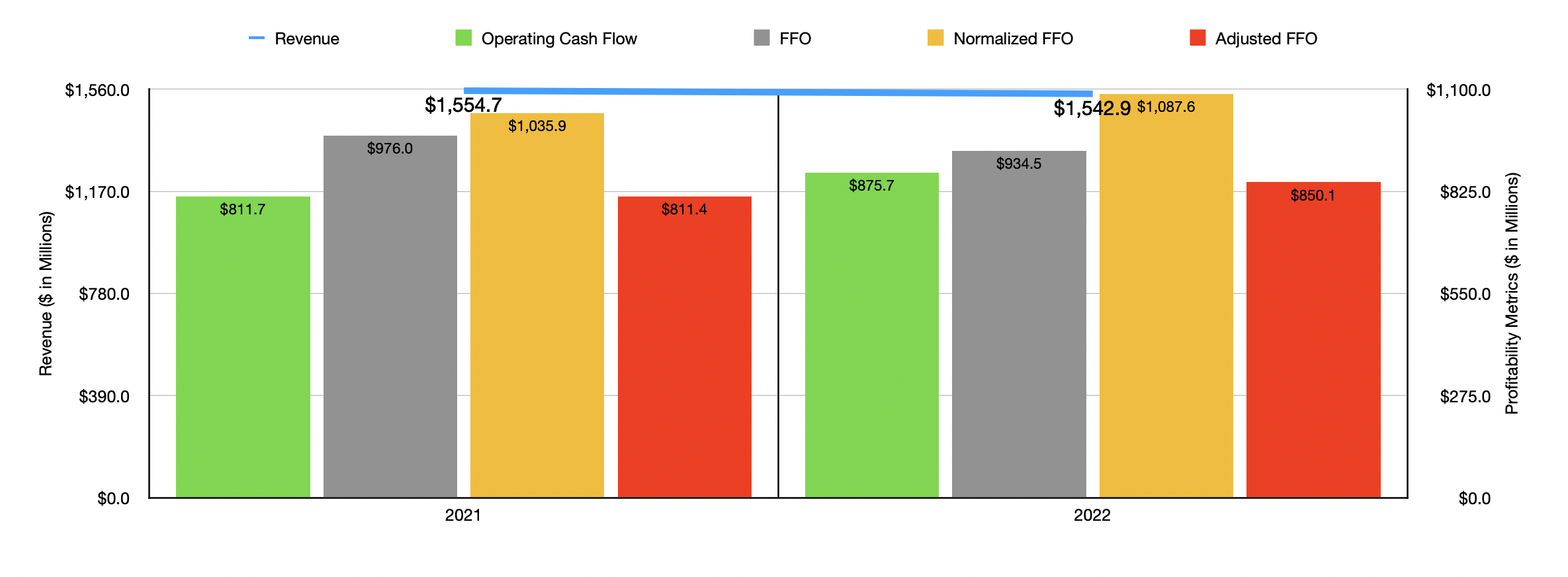

The results the company reported in the final quarter naturally played a role in how the company performed for 2022 in its entirety. Revenue, for instance, came in at $1.54 billion. That was down only slightly from the $1.55 billion reported one year earlier. FFO dropped from $976 million to $934.3 million, while normalized FFO rose from $1.04 billion to $1.09 billion. On an adjusted basis, FFO managed to increase from $811.4 million to $850.1 million. EBITDA, meanwhile, fell slightly from $1.54 billion to $1.40 billion.

{kind=link}

When it comes to the 2023 fiscal year, management has provided a bit of guidance. Their current expectation is for normalized FFO per share and for FFO per share to each be between $1.50 and $1.65. This might be one area where the market didn't like what it saw. After all, analysts were anticipating $1.75 per share for the year. Taking the midpoint of expectations, the company should still generate FFO and normalized FFO of around $941.9 million. If we assume that the year-over-year decline implied by the normalized FFO reading will be applicable to other profitability metrics, then we should anticipate adjusted FFO of $736.2 million and EBITDA of $1.21 billion. Again, management has not provided operating cash flow data yet. But based on my own estimates, it will likely have been around $875.7 million for 2022, and it should drop to $758.4 million in 2023.

Some investors may be turned off by the implied declines in profitability for 2023. But it's important to keep in mind that this is not because of worsening business conditions. Instead, it has to do with a number of changes the company has made in recent months. For instance, in December of this year, the company acquired six behavioral health facilities for £233 million. A combination of fixed rent escalators and CPI-based cash rent adjustments should also contribute around $50 million to the company's topline in 2023. On the other hand, the company has experienced other developments, including items I wrote about in a recent article about the firm. There is expected to be some pain, though. Notably, the firm's assumptions for 2023 assume that it might not be able to book any of its revenue associated with its Prospect operator for 2023 until sometime in 2024 or beyond. If guidance comes in on the high end, it will be because some of the amounts recovered from Prospect will have been recognized as revenue in the second half of 2023. Asset sales are also a factor here.

{kind=link}

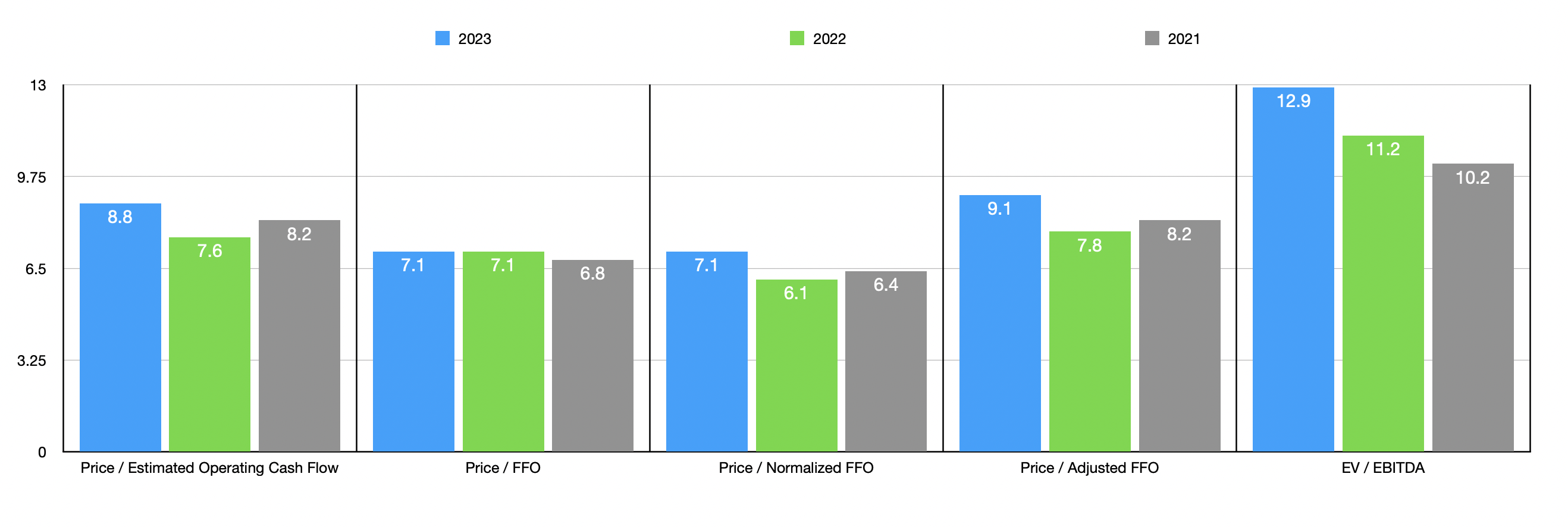

Assuming the numbers that management reported do turn out to be accurate, and if the assumptions I made are also accurate, shares of the company still seem to offer significant upside potential. In the chart above, you can see the company priced using all of the aforementioned profitability metrics. As part of my analysis, I took two of these metrics and compared the company to five similar firms. On a price to operating cash flow basis, these firms ranged from a low of 8.3 to a high of 20.7. And when it comes to the EV to EBITDA approach, the range was from 11.5 to 25.5. Even using the more conservative 2023 pricing estimates for Medical Properties Trust, I found out that only one of the five companies was cheaper than our target.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Medical Properties Trust |

| 8.8 |

| 12.9 |

| Healthcare Realty Trust ( HR ) |

| 20.7 |

| 25.5 |

| Omega Healthcare Investors ( OHI ) |

| 10.6 |

| 11.5 |

| Physicians Realty Trust ( DOC ) |

| 13.0 |

| 14.2 |

| Sabra Health Care REIT ( SBRA ) |

| 8.3 |

| 19.6 |

| National Health Investors ( NHI ) |

| 13.0 |

| 18.6 |

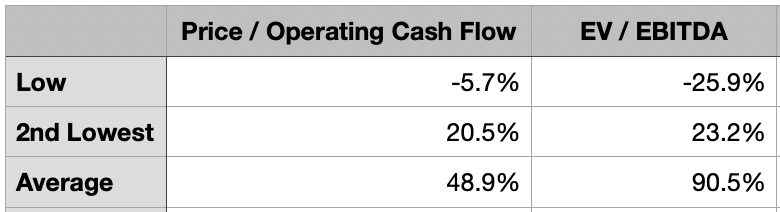

Another step I took in the analysis was to see what kind of upside or downside the company might experience if it were to trade at different multiples. I looked at three different scenarios. In the most conservative scenario, I looked to see what kind of upside or downside shares might experience if they were to trade at the multiple of the cheapest of the five firms I compared it to. Using the price to operating cash flow basis, downside would be 5.7%, while the EV to EBITDA approach would result in downside of 25.9%. This is rather discouraging to see. But in the second scenario, I looked at what kind of outcome investors should expect if the company is worth the second cheapest of the five firms. This changes the picture drastically, giving us upside of between 20.5% and 23.2%. In my opinion, the two firms that are cheaper than Medical Properties Trust (one firm from an operating cash flow perspective and the other from an EBITDA perspective) are clear outliers. And in the final scenario, I averaged out the multiples of each of the five firms and assumed that our prospect would trade at that average. Using the price to operating cash flow approach, we would get upside of 48.9%. When it comes to the EV to EBITDA approach, upside is even greater at 90.5%.

{kind=link}

Takeaway

I understand why Medical Properties Trust is not necessarily a crowd favorite. Historically speaking, the company has had a great deal of exposure to just a couple of tenants that have been reported to be in financial trouble. Throughout 2022, management did a great job reducing that exposure, and the firm in general has continued to make some interesting moves aimed at reducing the risk for shareholders. Given the myriad of developments, I would not be surprised if we see fundamental performance figures experience volatility moving forward. But with management actively addressing the weak spots of the business, and with shares trading at such a low price at this time, I believe that the 'strong buy' rating I gave the company in the past still holds firm.

For further details see:

Medical Properties Trust: Fantastic Upside Warranted Despite Its Recent Slide