OHI - Medical Properties Trust: More Crazy Upside Is Warranted

2023-10-27 21:14:34 ET

Summary

- Medical Properties Trust shares rose 15.7% after exceeding analysts' forecasts for FFO and revising profitability forecasts higher.

- MPT is working to reduce its high leverage and is evaluating divestiture and joint venture opportunities to repay debts.

- The company's exposure to its largest tenant, Steward, is multifaceted but appears to be on decent footing.

- Shares are drastically undervalued and have significant upside potential from here.

Oct. 26 ended up being a really good day for shareholders of Medical Properties Trust ( MPW ). Although most of the company’s shareholders are likely still underwater, it's unlikely that many were complaining after seeing shares shoot up for the day, closing 15.7% higher than they closed at a day earlier. There were multiple interesting data points provided by management, including FFO (funds from operations) that exceeded analyst forecasts, statements by management regarding the future monetization of assets, continued debt reduction, and revising profitability forecasts for this year slightly higher than they were previously. While the company still has a long way to go, it does seem quite clear that the market is finally recognizing just how insanely undervalued shares of the company are. Despite the challenges that remain, I would argue that this represents one of the most appealing prospects on the market for those who don't mind accepting risk that's a bit higher than normal.

The picture isn’t perfect, but it’s getting better

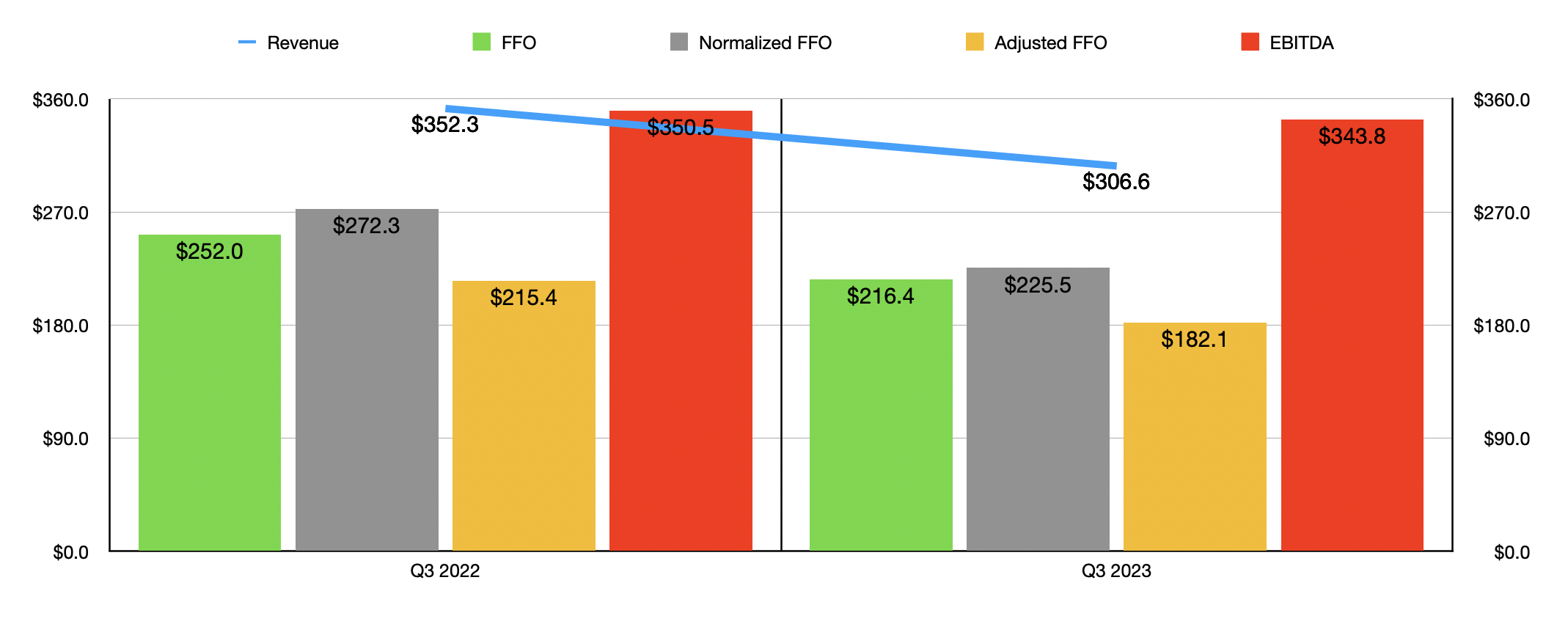

Before the market opened on Oct. 26, the management team at medical property REIT Medical Properties Trust announced financial results covering the third quarter of its 2023 fiscal year. By this point, you have probably seen the basic headline news. So we will only cover that slightly. In short, revenue for the company came in at $306.6 million. That was $35.3 million lower than what analysts forecasted and it was down from the $352.3 million generated one year earlier. Although any sort of decline is negative, it's important to note that the company has been going through some significant changes over the past year or so. I have documented some of them such as here and here . And when you are selling off assets, you can't normally expect revenue to stay elevated.

{kind=link}

What's perhaps more important is the bottom line. FFO per share came in at $0.36, which also was down year over year from the $0.42 reported previously, while normalized FFO per share was $0.38 compared to last year’s $0.45. The normalized FFO per share reading came in $0.02 per share higher than what analysts expected. These results translated to FFO of $216.4 million and normalized FFO of $225.5 million. These numbers are both down from the $252 million and $272.3 million, respectively, generated the same time last year. Year over year, adjusted FFO fell from $215.4 million, while EBITDA, adjusted for transactions and other things, dipped slightly from $350.5 million to $343.8 million.

{kind=link}

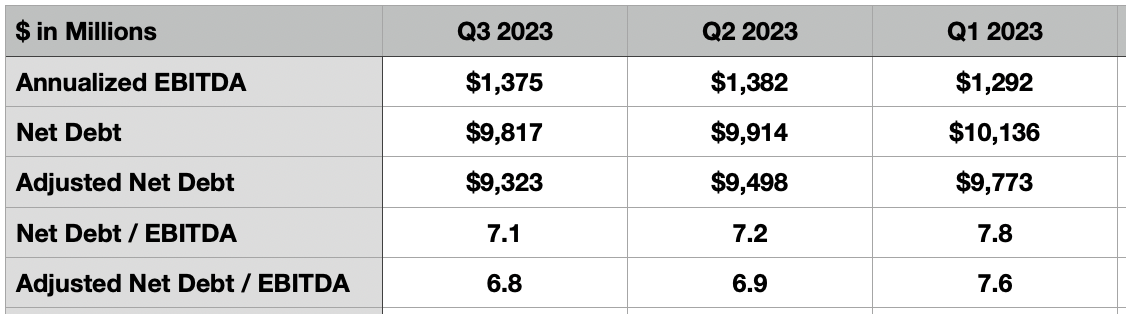

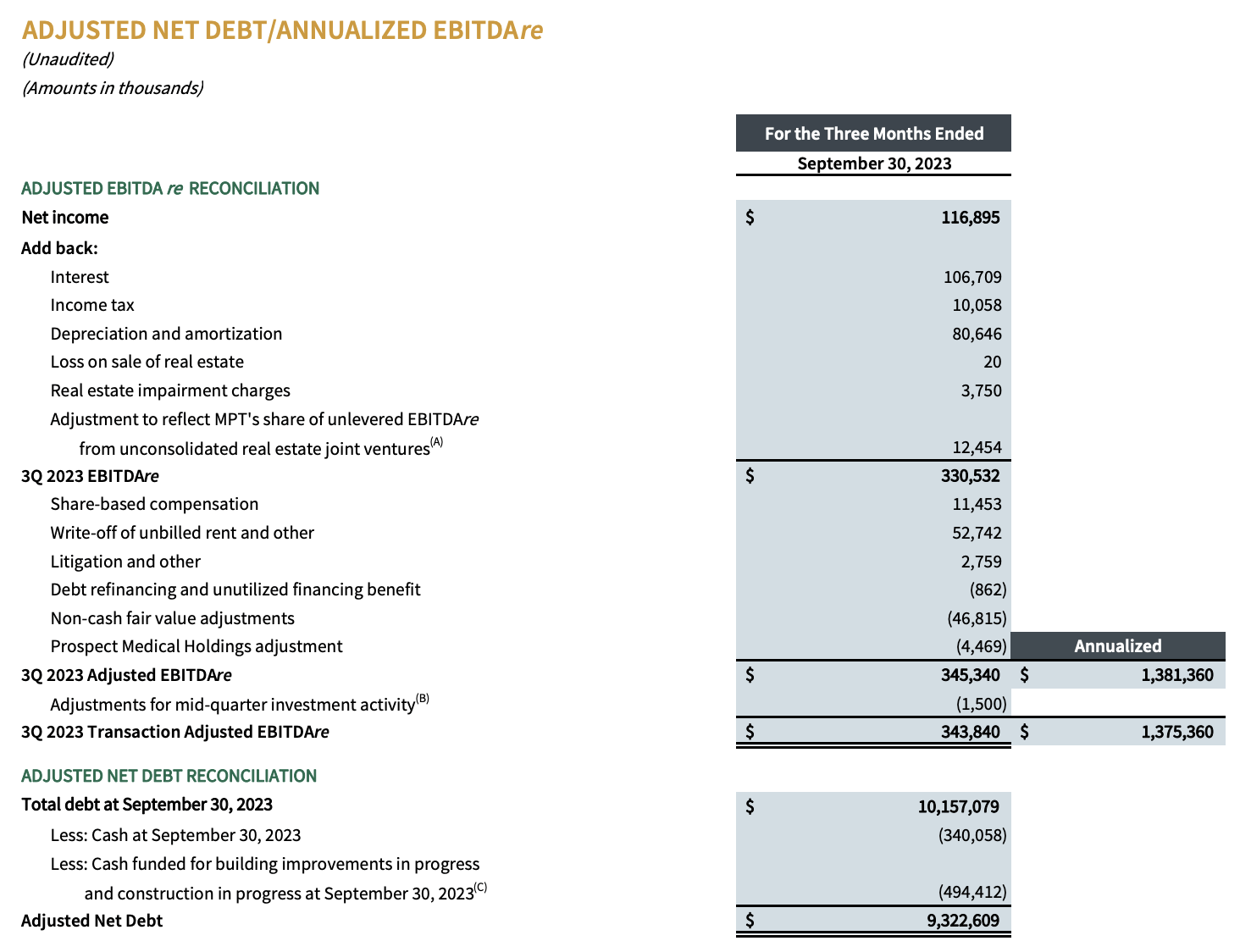

Again, asset sales are a big contributor when it comes to these declines. When putting in context of the company's overall health, however, it does appear as though the business is doing really well for itself. On an annualized basis , the EBITDA for the company comes out to just under $1.38 billion. When stacked up against the net debt that the company has of $9.82 billion, this translates to a net leverage ratio of 7.1. In the table above, I compared the company as it stands today to how it looked like during each of the past two quarters. Back in the second quarter, the net leverage ratio was 7.2. And in the first quarter it was a lofty 7.8. Management does have another measure of net debt, which credits the company for cash funded for building improvements that are in progress as well as cash allocated toward construction and progress. This would reduce net debt further to $9.32 billion for a net leverage ratio of 6.8. This is down from the 7.6 reading that we get using data from the first quarter of the year. In addition to seeing EBITDA increase during this time, net debt has fallen from $10.14 billion to $9.82 billion, while the adjusted figure for it has dropped from $9.77 billion to $9.32 billion.

{kind=link}

To be very clear, this is not a great situation for the company to be in. It's not untenable, but the high amount of leverage does cause concern among investors and prospective investors. That's why management made it very clear that they have a goal to address this. Not only did the company slash its distribution earlier this year as. Management also stated in the third quarter press release that "in the interest of expediting the repayment" of its debts, the firm is evaluating divestiture and joint venture opportunities. They're also looking at secured debt financing options that might provide immediate liquidity based on the company’s assets. Regardless, they believe that they can raise around $2 billion in new liquidity over the next 12 months. This is unlikely to include recent proceeds.

For instance, earlier this month, management announced that they had completed the sale of the rest of their operations in Australia. That sale brought in around $305 million and, while it's still reflected in the debt, management earmarked those proceeds to pay off $302.4 million in debt associated with those assets. Management also agreed, but has not closed the deal on, to sell seven facilities to one of its tenants for roughly 1% of its total assets. That should be somewhere around $190 million in additional capital. It's unclear how much the company will have to sell. But as of the end of the most recent quarter, it boasted ownership over 441 properties and 44,000 licensed beds. After the end of the quarter management sold four properties, bringing this down to 43,000 licensed beds.

The company also provided some other interesting details that investors should be paying attention to. For starters, the firm ended up changing guidance for the year. Guidance was ultimately narrowed, with FFO now forecasted to come in at between $1.58 and $1.60. That stacks up nicely compared to the $1.56 to $1.60 previously forecasted. Normalized FFO also has been adjusted from between $1.53 and $1.57 to between $1.56 and $1.58. Both of these revisions imply higher levels of cash flow than what the company thought it could achieve when it announced guidance in the second quarter of the year.

Management also provided some very interesting details regarding its largest tenant. If you follow Medical Properties Trust closely, you will know that the tenant in question is Steward. For several quarters now, management has been working to reduce exposure to Steward, in large part because there have been concerns about the company's health. The good news is that we now have more data on that front. But it does take a bit to unpack. And that's because Medical Properties Trust’s exposure to it is multifaceted.

{kind=link}

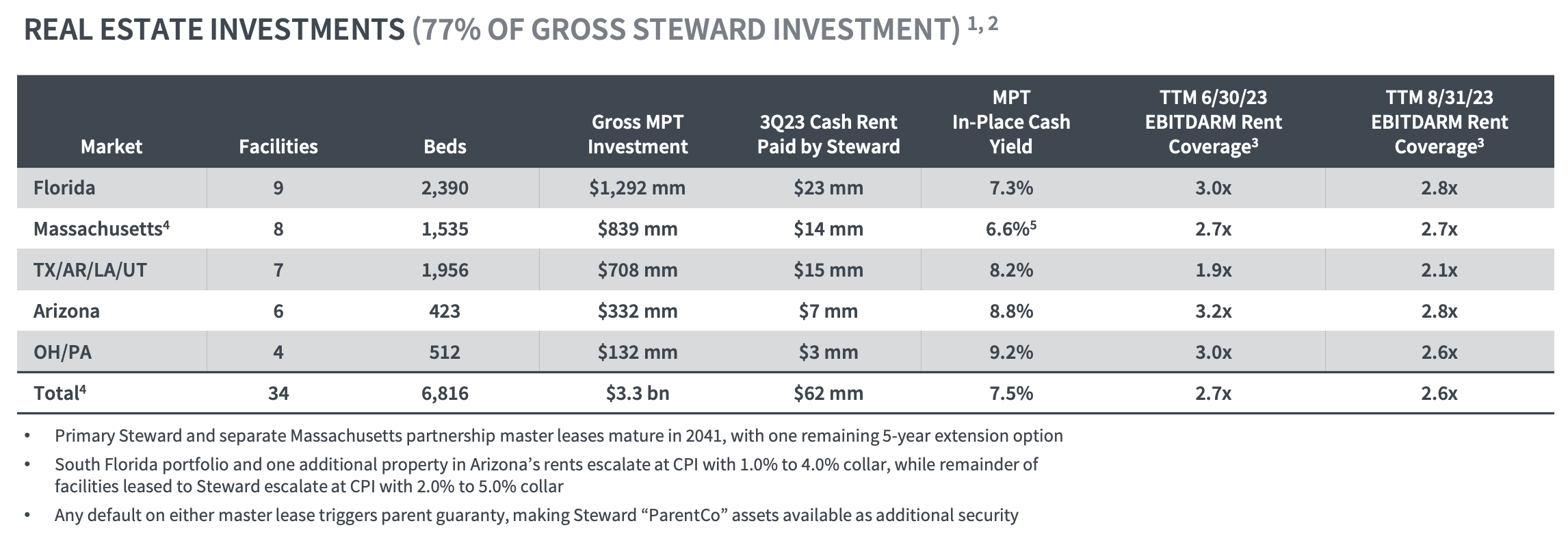

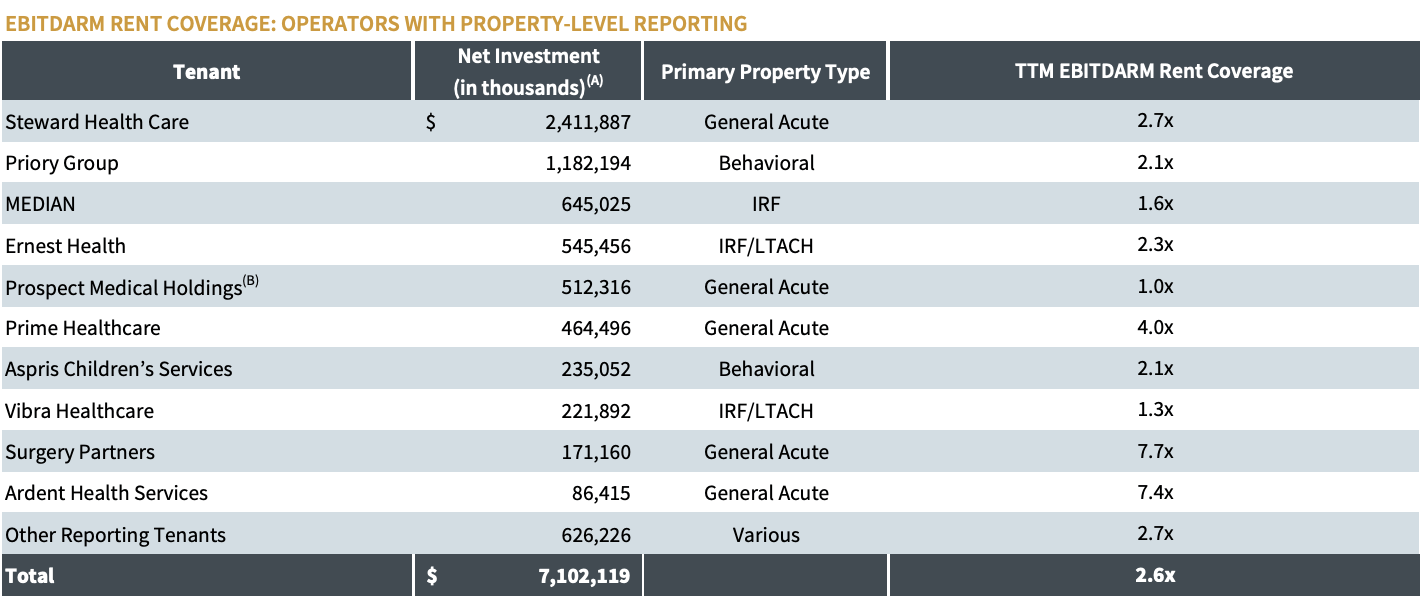

For starters, about 77% of its gross investments in Steward are in the form of medical properties that are under lease to Steward. They total about $3.3 billion of the company's $19 billion in assets. In the third quarter of this year alone, Medical Properties Trust generated $62 million of cash rent paid by Steward off of these assets. And all combined, this accounted for approximately 20.2% of Medical Properties Trust’s revenue during the third quarter of the year. Their really important data point on this involves the EBITDARM rent coverage. EBITDARM refers to traditional EBITDA, but it also has added back to it rent and management fees. This figure for the trailing 12-month period ending on Aug. 31 of this year came in strong at 2.6. As you can see in the image below, this is actually stronger than a lot of the company's other tenants. While it would be nice to know more details, such as the interest expense that Steward has and any rent or management fees outside of what we know, it seems to me as though the firm is on decent footing at this time.

{kind=link}

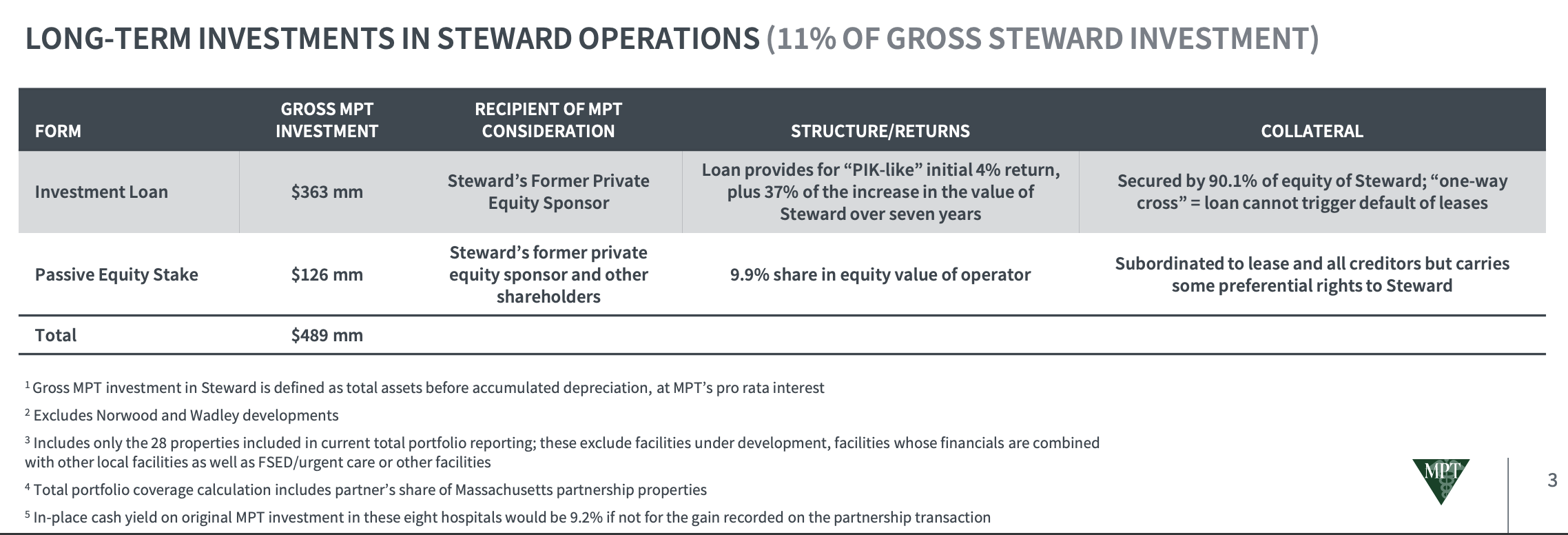

The next largest concentration of risk for Medical Properties Trust when it comes to Steward is the 11% of its gross investment in that company that's in the form of long-term debt or equity. This includes $363 million in the form of a loan that provides an initial 4% return and 37% of the increase in the value of Steward over a seven-year window. It also includes $126 million in the form of a 9.9% ownership stake in Steward. This stake very likely would be worth nothing if Steward were to declare bankruptcy. And it is unclear about the loan. Another 7% of its exposure is in the form of $90 million that was invested so far on construction and progress at the Wadley Regional Medical Center and $175 million invested so far on improvements related to the rebuilding of the destroyed Norwood Hospital in Massachusetts. It is highly probable that these investments, as relatively new contributions to new facilities, will be worth at least what management has allocated.

{kind=link}

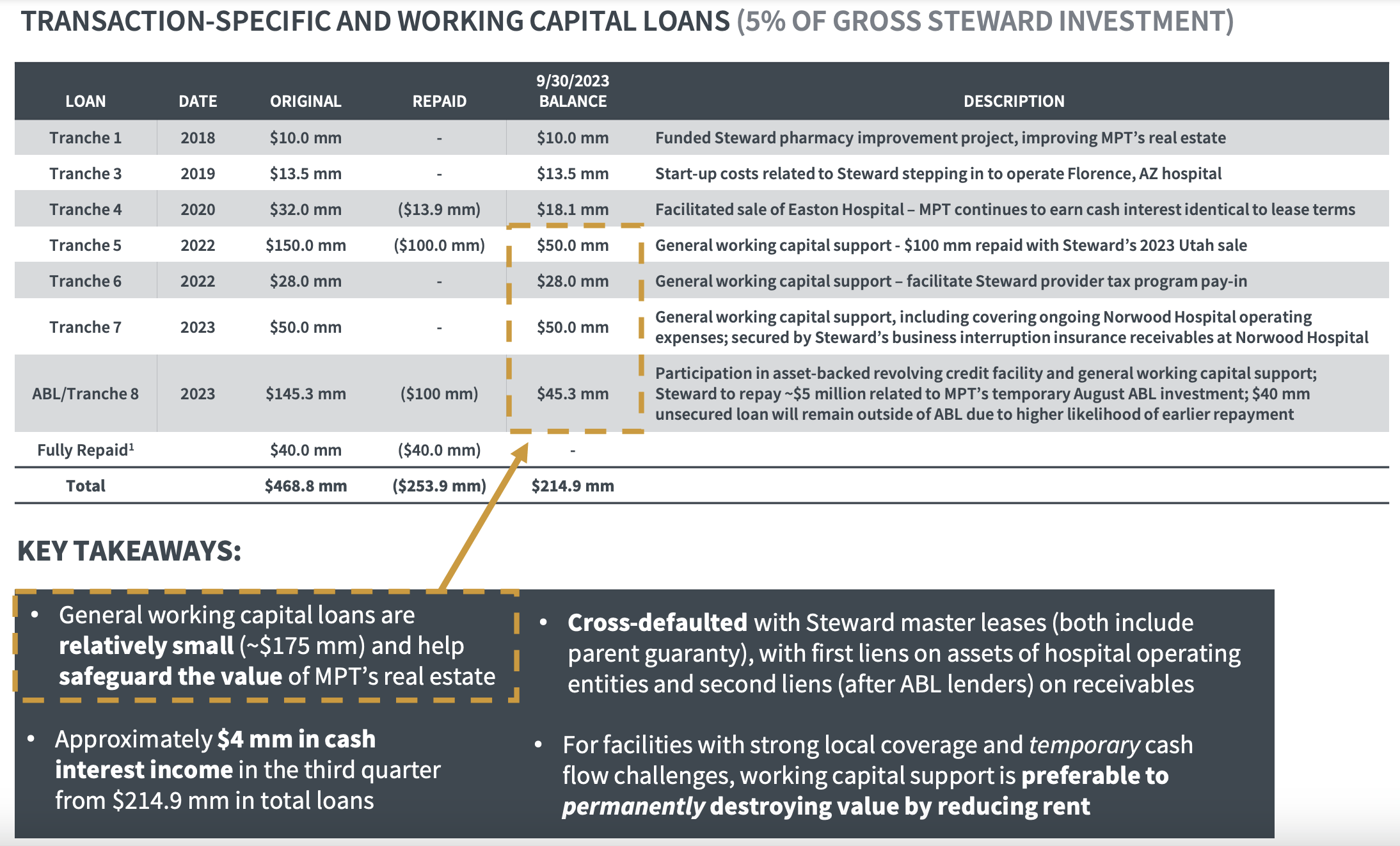

After all is said and done, this leaves us with only 5% of its investment. This has been in the form of transaction specific and working capital loans made to Steward over time. Originally, this came out to $468.8 million. But from some asset sales and other initiatives, this number has been reduced considerably to $214.9 million. Steward continues to pay interest on these amounts at an annualized rate of roughly 7.4%. That's approximately $16 million in funding that flows into Medical Properties Trust each year. And while this is also riskier than some of the other amounts discussed, when you consider the stability that Steward seems to have, I wouldn't be terribly concerned about management’s exposure to the firm. The fact that the company also received cash payments, as expected, from Prospect, another of its tenants but one that went through restructuring, for both September and October, also likely served to boost confidence of investors in the enterprise.

{kind=link}

Shares still have robust upside

{kind=link}

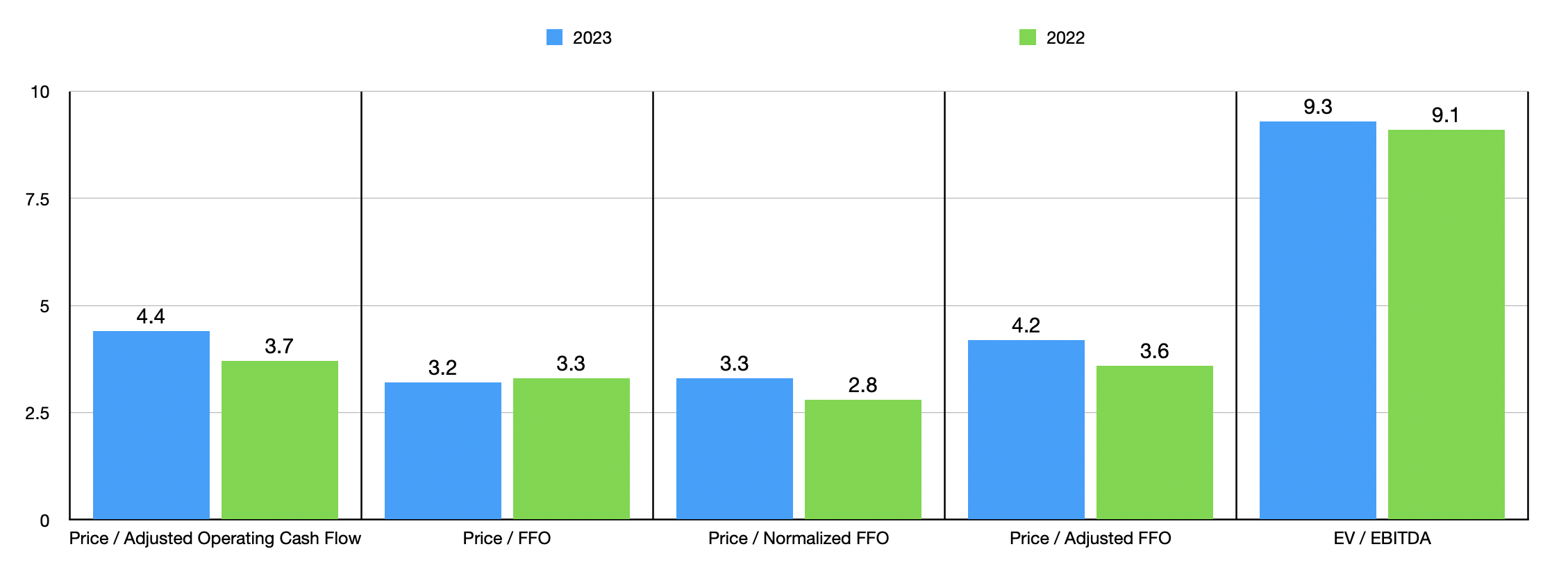

Despite shares of the company skyrocketing on Oct. 26, further upside for investors is highly probable. Using management's guidance for the current fiscal year and comparing that to financial performance for last year, I arrived at some reasonable approximations as to not only FFO and normalized FFO, but also adjusted FFO, adjusted operating cash flow, and EBITDA. In the table above, you can see how the company is priced relative to these metrics on both a forward basis for 2023 and using data from 2022. I find the 2023 data to be far more relevant given asset sales that have already occurred.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Medical Properties Trust |

| 4.4 |

| 9.3 |

| CareTrust REIT ( CTRE ) |

| 14.8 |

| 24.8 |

| Omega Healthcare Investors ( OHI ) |

| 13.7 |

| 16.5 |

| Physicians Realty Trust ( DOC ) |

| 10.3 |

| 12.1 |

| Sabra Health Care REIT ( SBRA ) |

| 10.2 |

| 30.7 |

| National Health Systems ( NHI ) |

| 12.8 |

| 14.5 |

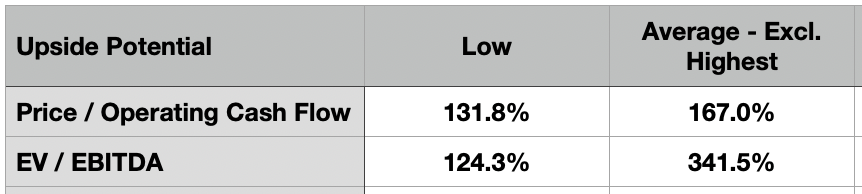

In the next table, shown above, you can see how Medical Properties Trust is priced compared to five similar firms. As you can see, it's substantially cheaper. In the table below, you can see what kind of upside scenario shares of Medical Properties Trust might experience under different scenarios. For instance, I looked at how much upside the stock might warrant if it were to trade at the lowest trading multiple of its five peers, both on a price to operating cash flow basis and on an EV to EBITDA basis. Upside here should range between 124.3% and 131.8%. I then did the same thing by stripping out the most expensive of the five and averaging out the trading multiples of the other four. This gave us a much wider range of upside of between 167% and 341.5%.

{kind=link}

Of course, it would be helpful to know whether these companies are truly comparable to Medical Properties Trust. In the table below, I decided to look at what might be the most important metric in determining that. That would be the net leverage ratio. Earlier in this article, I mentioned that, using the traditional way of looking at the net leverage ratio, and ignoring any asset sales that were not completed prior to the third quarter ending, the company had a reading of 7.1. As you can see in the aforementioned table, three of the five companies I compared our prospect too come in quite a bit lower than that. But two of them actually come in higher. And both of these are substantially more expensive than our target as well.

| Company |

| Net Debt / EBITDA |

| Medical Properties Trust |

| 7.1 |

| CareTrust REIT |

| 5.0 |

| Omega Healthcare Investors |

| 7.3 |

| Physicians Realty Trust |

| 5.9 |

| Sabra Health Care REIT |

| 7.5 |

| National Health Investor |

| 4.2 |

Takeaway

From all that I can see, Medical Properties Trust is doing a really fantastic job. Somebody looking at just the headline news items might be concerned because of the drop in revenue and profits. But when you dig deeper and really put everything into context, it becomes clear, at least to me, that shares are drastically undervalued and that upside potential for investors is massive. Unless something changes in the meantime or unless I find a better opportunity elsewhere, I very likely will hold my shares until I can get a triple out of them without factoring in the distributions the company is paying out. Until then, I'm happy to collect the 11.6% yield the company is currently paying out and the 5.7% that I'm getting on my weighted average purchase price. And given these current developments, I likely will increase my exposure, which would bring down my weighted average purchase price some. Naturally, if this is how I'm proceeding, I'm keeping the company rated a "strong buy" for now.

For further details see:

Medical Properties Trust: More Crazy Upside Is Warranted