SBRA - Medical Properties Trust: On Better Footing Than You Think

2023-03-24 17:01:08 ET

Summary

- Medical Properties Trust has struggled in the market in recent months, with fears about the company's prospects moving forward.

- This comes even as the firm has worked to improve its financial position and as shares have gotten materially cheaper.

- Investors likely also fear a distribution cut, but this may very well not be needed.

- All in all, the company offers investors significant upside potential from here.

Beyond any doubt, one of the most controversial investment opportunities on the market today is Medical Properties Trust ( MPW ), a healthcare REIT that has been beat up by concerns over the health of its largest operator and because of worries about its large amount of debt. Over the past year, shares have fallen 62% due to these problems. And for investors who have been along for the ride, the pain has been extraordinary. At the same time, this also represents an opportunity if those who are currently bullish on the firm end up being correct. In addition to having the potential to see its units rise significantly, the company also has an effective yield right now of almost 15%. One big question that many investors are likely asking at the moment, however, is whether or not that yield is safe. In my opinion, the yield is not as secure as I would normally like. But I don't believe there is a high probability of management being 'forced' to cut the distribution. Does this mean that management shouldn't? Not exactly. In fact, reducing the distribution might be a good way to reduce risk and to create long-term shareholder value. But at the end of the day, we need to be guided by the numbers.

Recent concerns

Any serious discussion regarding the health of the distribution should first touch on the overall leverage of the business. When it comes to this topic, we have had some interesting discourse as of late. On March 16, news broke that BofA Securities analyst Joshua Dennerlein had decided to cut his rating on Medical Properties Trust down to Neutral in response to concerns regarding debt and certain tenants. While acknowledging that the REIT's valuation is 'compelling', he said that investors need to see positive developments on both of these fronts in order for whatever upside exists to be achieved. At first glance, this doesn't seem to be horrible news. And when it comes to the tenant issues specifically, details of how the company is handling them have been made abundantly clear. But in his downgrade, Dennerlein made a rather drastic call when it came to the company's debt position.

{kind=link}

As of the end of the latest quarter , Medical Properties Trust had net debt of roughly $10 billion. But after adjusting for proceeds from certain sales, this number would drop to just over $9 billion. Of this amount, $7.77 billion matures after the year 2024, with some of it maturing as late as 2031. The overwhelming majority of the debt on its books has interest rates that are fixed and that range between 0.99% and 5%. However, the company does have a revolving credit facility, as well as four different term loans. While the company has done well to lock some of these in place with fixed interest rates through interest rate swaps, some of it is still susceptible to rising interest rates.

Of particular concern was the interest rate at which long-term debt might need to be refinanced. Instead of the 3.5% weighted average rate today, Dennerlein believes the company may be forced to pay between 10% and 11% per annum. From what I see, this does not make any sense. As recently as November of last year, Moody's ( MCO ) reaffirmed its Ba1 rating on the company's debt, giving it a stable outlook. This is the same rating that the company has had on its debt for the past several years now. It is true this picture could change, but there is no concrete evidence that this is likely to occur.

| Company |

| Net Debt ($ in Millions) |

| EBITDA ($ in Millions) |

| Net Debt/EBITDA |

| Medical Properties Trust |

| $9,014.8 |

| $1,345.5 |

| 6.70 |

| CareTrust REIT ( CTRE ) |

| $706.3 |

| $162.8 |

| 4.34 |

| Omega Healthcare Investors ( OHI ) |

| $4,986.2 |

| $719.0 |

| 6.93 |

| Physicians Realty Trust ( DOC ) |

| $1,810.4 |

| $318.2 |

| 5.69 |

| Sabra Health Care REIT ( SBRA ) |

| $2,452.8 |

| $326.6 |

| 7.51 |

| National Health Investors ( NHI ) |

| $1,128.2 |

| $214.6 |

| 5.26 |

I am not saying that management should not be focused on debt reduction. Frankly, it should be. The net leverage ratio, based on my calculations and using forward estimates for the 2023 fiscal year, should be about 6.70 (using management's low-end estimate). As you can see in the chart above, I compared the business to five similar healthcare REITs. They currently have net leverage ratios ranging between 4.34 and 7.51. Of the five firms, two have greater leverage than Medical Properties Trust does. The average of the five firms is 5.95. Excluding the clear outlier that is CareTrust REIT, this average rises to 6.35. In order for Medical Properties Trust to come down to this level, it would need to reduce net debt by only $115.9 million. Without the outlier being removed, debt reduction would need to be $676.5 million.

A significant yield

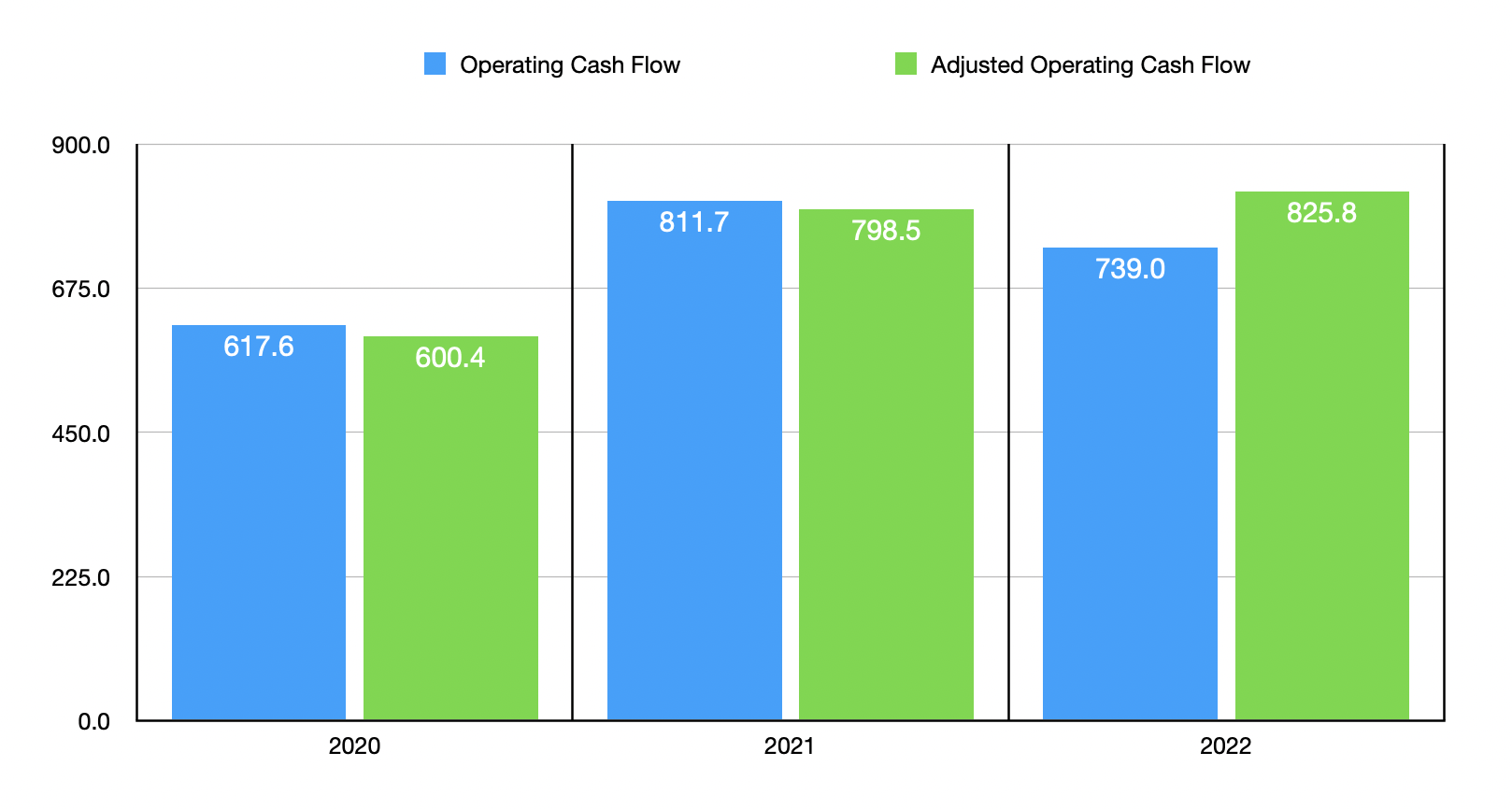

While debt is most certainly elevated, it doesn't seem to be at a level that is untenable compared to similar firms. Of course, when debt does come due, it almost certainly will be subjected to higher interest rates should management be forced to roll said debt over as opposed to paying it off. To put this in perspective, a 1% increase to the company's total debt holdings would cause annual interest expense to climb by $90.1 million. To see how much wiggle room the company has on its significant 15% yield, we need to do some other math. The most important metric, I believe, when it comes to this is adjusted operating cash flow. This is defined as operating cash flow after adjusting for changes in working capital.

{kind=link}

*$ in Millions

Over the past three years, operating cash flow for the company has bounced around. It was $617.6 million in 2020. It rose to $811.7 million in 2021 before dropping to $739 million in 2022. If we adjust for changes in working capital, however, the metric would have risen consistently year after year, climbing from $600.4 million to $825.8 million. Making certain adjustments for changes in its asset base, I estimate that this figure will be around $734.2 million for the 2023 fiscal year. What you can see in the table below is the ratio of the firm's distributions to its adjusted operating cash flow over the past three years, and on a forward basis if my estimate is correct and if management keeps the distribution unchanged.

| Company |

| Operating Cash Flow ($ in Millions) |

| Distribution ($ in Millions) |

| Distribution/OPCF |

| Medical Properties Trust |

| $734.2 |

| $698.5 |

| 0.95 |

| CareTrust REIT |

| $144.4 |

| $106.1 |

| 0.73 |

| Omega Healthcare Investors |

| $625.7 |

| $632.9 |

| 1.01 |

| Physicians Realty Trust |

| $258.4 |

| $209.4 |

| 0.81 |

| Sabra Health Care REIT |

| $315.7 |

| $277.2 |

| 0.88 |

| National Health Investors |

| $185.3 |

| $161.8 |

| 0.87 |

Nearly all of the company's cash flow is being dedicated toward distributions. But that's not uncommon for a REIT. In fact, REITs are required to pay out 90% of their taxable income to qualify for the designation. As a result, REITs are known for distributing most if not all of the cash that they can directly to investors. But of course, this leaves little in the way of wiggle room should difficult times strike. To see how the company compares, I stacked it up against the same five firms as I did previously. These firms have ratios ranging from 0.73 to 1.01 when looking at the 2022 fiscal year. The average between the five comes out to 0.86 which, for Medical Properties Trust, would require a roughly 9.6% cut to its distribution to match. Excluding the lowest of the five, the reduction would need to be 6.2%.

This is not to say that Medical Properties Trust will be forced to cut the distribution or that it necessarily should. What this does illustrate, however, is that the company's debt situation is not all that extreme relative to similar firms. In addition to that, the payout, while elevated slightly, is not outside of the range that you would expect if you were looking at other players in the space. Even so, the yield on the business is significantly greater. Of the five companies I compared it to, the closest we get is Sabra Health Care REIT, with a yield of 11.2%. The average of the five companies I compared Medical Properties Trust to start at about 8.1%.

| Company |

| Yield |

| Medical Properties Trust |

| 15.0% |

| CareTrust REIT |

| 5.9% |

| Omega Healthcare Investors |

| 9.9% |

| Physicians Realty Trust |

| 6.3% |

| Sabra Health Care REIT |

| 11.2% |

| National Health Investors |

| 7.1% |

There's no strong evidence at this moment that Medical Properties Trust will need to cut its distribution in the near term. In fact, the company seems to be at a level of health that is not that far removed from similar firms. In addition, the stock seems to have significant upside potential. Performing a similar analysis to what I did in a prior article , shares do seem to have a great deal of upside relative to similar firms. Upside potential, based on my estimates, ranges between a very conservative 23.8% and a rather extreme, but not unrealistic, 214.9%.

| Valuation Scenario |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Low |

| 23.8% |

| 53.5% |

| Average - Highest |

| 71.4% |

| 214.9% |

Takeaway

Over the past several months, those who are bullish on Medical Properties Trust have taken a beating, while those who are bearish have done quite well. Based on the data provided, I believe the market is mistaken about this opportunity. Shares have been pushed down materially, but the business seems to be in better shape now than it was months ago. I don't want to make it sound like everything is perfect. It definitely isn't. I would like management to focus on debt reduction, whether that be through asset sales or through the cash the firm generates. But when you consider how the company stacks up compared to similar firms, its picture does not look measurably worse. And for those who want an attractive upside, the firm should actually look really appealing on a relative basis.

For further details see:

Medical Properties Trust: On Better Footing Than You Think