OHI - Medical Properties Trust Pops On Renewed Optimism

2023-05-01 13:03:43 ET

Summary

- The management team at Medical Properties Trust, Inc. came out with mixed but largely positive developments for the firm's most recent quarter.

- The firm continues to show dedication to deleveraging and shares of the enterprise look remarkably cheap.

- In all, Medical Properties Trust very likely deserves to trade materially higher than where it is at today.

If you were a shareholder of Medical Properties Trust, Inc. ( MPW ) on April 27th, odds are you were pretty happy. After the company announced , before the market opened, financial results covering the first quarter of its 2023 fiscal year, shares of MPW shot up, closing higher by 7.6% for the day. Although this in no way makes up for the significant decline in price the company experienced over the past year, it is a nice reprieve from the pain and suffering many investors in the firm have been subjected to.

For those digging deep into the numbers, it may seem peculiar that MPW stock rose at all. After all, management did slightly decrease guidance for FFO, or funds from operations, per share for 2023. In my opinion, the move higher was based on the market recognizing that management continues to deliver on their promises and has taken a bold stance when addressing its critics. When you add on top of this how cheap shares are, both on an absolute basis, and relative to similar firms, I do believe that the company still warrants a "strong buy" rating at this time.

Assessing matters

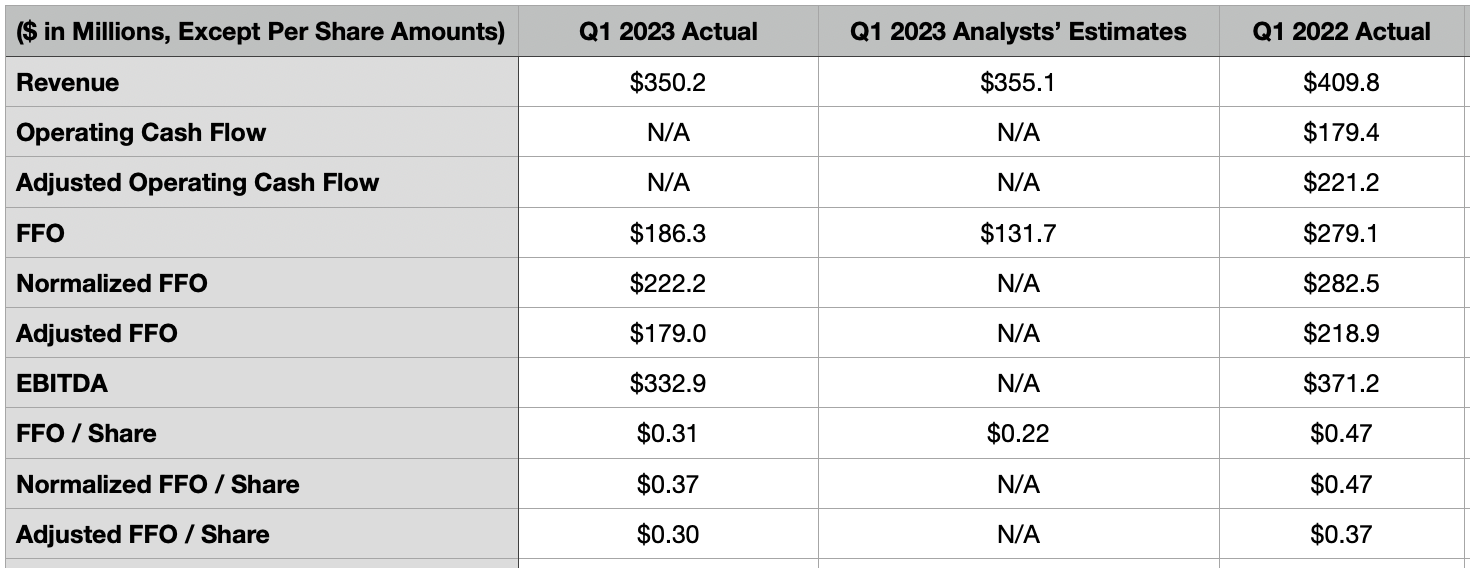

In some respects, I would argue that the quarterly data provided by management at Medical Properties Trust was rather lackluster. Consider, for instance, the revenue the enterprise generated. Sales for the quarter came in at $350.2 million. In addition to being lower than the $409.8 million reported one year earlier, MPW also managed to miss analysts’ expectations by $4.9 million. Asset divestitures, as well as other factors, played a role in the year-over-year revenue decline. Excluding straight line rent that the company received, rent billed by the company fell from $263.4 million to $248.2 million. But the most significant decline came from income associated with financing leases. This plunged from $51.8 million to $13.2 million.

{kind=link}

On the bottom line, the picture for Medical Properties Trust, Inc. did come in far better than anticipated, though. FFO per share came in at $0.31. Although this was substantially lower than the $0.47 per share reported the same quarter one year earlier, it did beat analysts’ expectations of $0.22 per share. This translated into FFO of $186.3 million, down from the $279.1 million reported one year earlier . By comparison, analysts were anticipating a reading of $131.7 million. As you can see in the table above, other cash flow metrics for the company also declined year over year. But the drops were not as significant as they likely would have been had analysts been correct about FFO and assuming that the other said profitability metrics would have declined at a similar rate to it year-over-year. Generally speaking, I do like to look at operating cash flow and adjusted operating cash flow. But given that the company did not report this in its earnings release and has not provided a 10-Q as of this writing, we don't know what that data looks like.

Those who follow Medical Properties Trust, Inc. closely will know that debt is a rather hot topic regarding this enterprise. At the end of the most recent quarter, net debt was $10.14 billion. This was actually up from the $10.03 billion that the company reported at the end of the 2022 fiscal year.

However, certain adjustments are warranted. When we factor in pending asset sales and other transactions that management has already planned, net debt actually drops to about $8.37 billion. If we annualize the $332.9 million in EBITDA that the company reported for the first quarter of its 2023 fiscal year, the net leverage ratio drops to roughly 6.5. This is great to see. For the 2023 fiscal year, management said that normalized FFO per share should be between $1.50 and $1.61. The upper end of this range is actually down from the $1.65 estimate previously provided. At the midpoint, this would translate to normalized FFO of $930.4 million. If we assume that other profitability metrics will change at a similar rate, that would imply FFO of $799.4 million, adjusted FFO of $727.2 million, and operating cash flow of $749.1 million.

{kind=link}

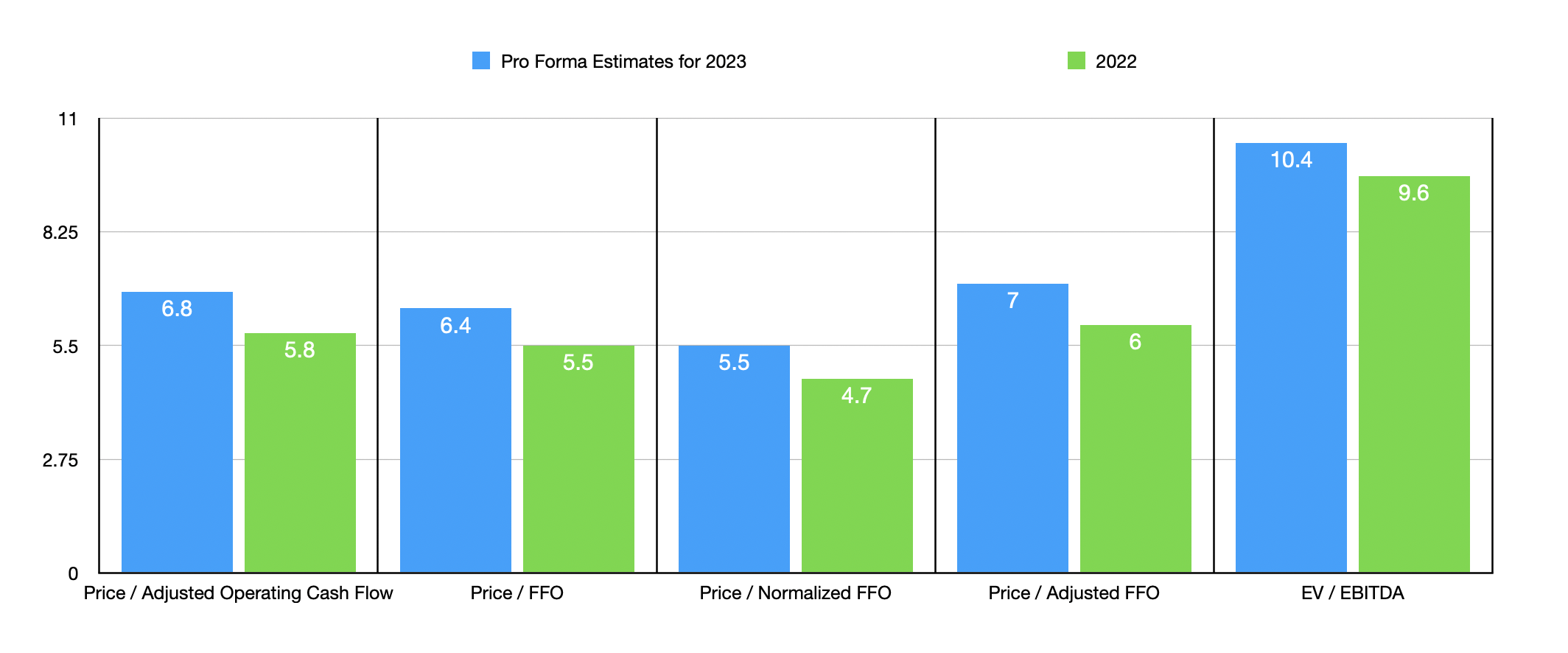

Based on these figures, shares of Medical Properties Trust, Inc. look quite affordable. As you can see in the chart above, the stock looks very cheap on a forward basis, even though it is a bit more expensive than if we were to use data from 2022. By considering the structural changes that are taking place at the enterprise, this difference is not surprising to see. In the table below, meanwhile, you can see how the company is priced against five similar firms. Using the 2023 estimates, I calculated that it was the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Medical Properties Trust |

| 6.8 |

| 10.4 |

| Healthcare Realty Trust ( HR ) |

| 20.0 |

| 24.7 |

| Omega Healthcare Investors ( OHI ) |

| 10.6 |

| 11.3 |

| Physicians Realty Trust ( DOC ) |

| 13.2 |

| 14.0 |

| Sabra Health Care REIT ( SBRA ) |

| 8.3 |

| 23.0 |

| National Health Investors ( NHI ) |

| 12.1 |

| 18.2 |

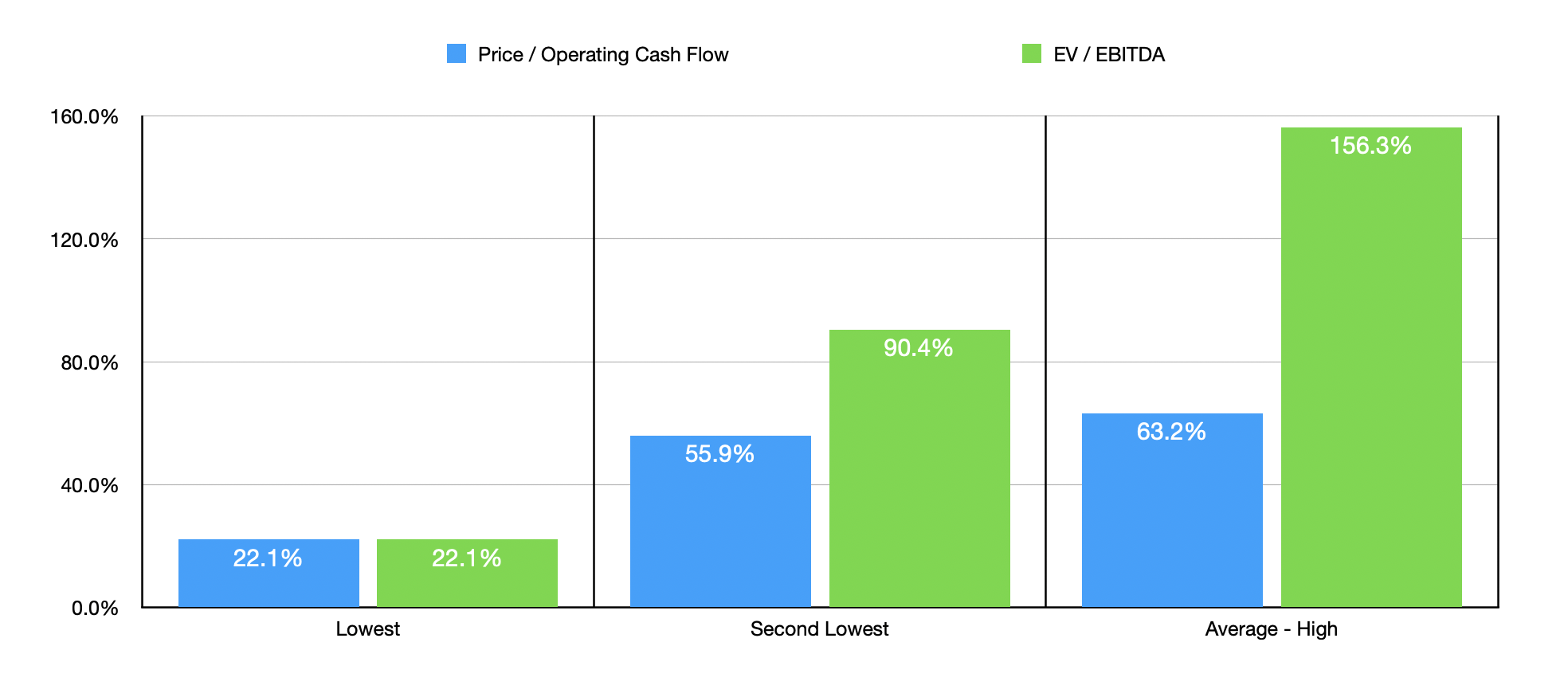

In order to see what kind of upside potential, if any, Medical Properties Trust, Inc. might offer, I decided to look at three different scenarios. The first scenario calculates what kind of upside potential the business were to offer investors if its price to operating cash flow multiple and its EV to EBITDA multiple were trading at the same multiple as the cheapest of the five peers that I put it up against. The second scenario looks at how much upside would exist if I compared it to the second cheapest of its peers. And the final scenario looks at what pricing would look like if I were to strip out the most expensive of its peers and average out the other four as a decent multiple for Medical Properties Trust to trade out.

As you can see, Medical Properties Trust, Inc. shares would have upside ranging from 22.1% to 156.3%. That's quite appealing in my book and, I would argue, that upside is probably closer to the higher end of that range.

{kind=link}

Other developments are encouraging as well

Outside of the fundamentals, there were some other interesting pieces of information for Medical Properties Trust, Inc. investors. For starters, the company does continue to make some interesting deals aimed at maximizing shareholder returns. Some of these I have already written about. For instance, last month, the company agreed to sell off its entire portfolio of assets in Australia in order to pay off all of the debt associated with those assets. But some of these I have not touched on. For instance, last month, the company received notice from Prime Healthcare indicating that Prime had decided to exercise its right to repurchase 3 hospitals split between Kansas and Texas that Medical Properties Trust currently owns. This should take place in the third quarter of the year and will bring in roughly $100 million in proceeds. And earlier this month, the company agreed to acquire five behavioral health facilities in the UK, as well as three post-acute facilities in Germany, for what will be around $150 million.

Perhaps more interesting than this, however, is Medical Properties Trust, Inc.'s update on a lawsuit that it filed against Viceroy Research, wherein the enterprise accused the defendant of essentially defaming the company and trying to levy a short assault against it. According to the update, Viceroy filed motions aimed at dismissing the claims, with multiple arguments made as to why this should occur. Intriguingly, the research firm argued that its reports were not matters of "fact," but were, instead, "opinion and "commentary… dominated by colorful, hyperbolic language." This kind of admission absolutely works in the favor of Medical Properties Trust if the company's goal is not necessarily to win money, but instead is aimed at ensuring investors that its overall financial health is robust and that concerns spouted by parties critical of it are unwarranted.

Takeaway

From all that I can tell, Medical Properties Trust, Inc. is in solid shape right now. The company continues to reduce debt and cash flows are looking strong. The firm is coming out of the gate swinging in response to hostile parties. And on top of this, Medical Properties Trust, Inc. shares look very cheap on both an absolute basis and relative to similar firms. Given all of these factors, I cannot help but to keep the "strong buy" rating I had on Medical Properties Trust, Inc. stock previously.

For further details see:

Medical Properties Trust Pops On Renewed Optimism