OHI - Medical Properties Trust Q4 2022 Earnings Preview: A Great Prospect Ahead Of Earnings

Summary

- The management team at Medical Properties Trust is due to report financial results for the final quarter of its 2022 fiscal year.

- Ahead of that time, analysts have rather bearish expectations, but the overall picture for the company looks healthy right now.

- The company is also incredibly cheap and should appreciate from here absent some major change in circumstances.

As those who follow me closely know, I run a very concentrated portfolio. Today, my portfolio consists of only 10 holdings. One of them, representing 9.2% of my holdings today, is a REIT called Medical Properties Trust ( MPW ). Although REITs are often appreciated because of their stable cash flows and overall stability, this particular player has been lacking in the latter. Concerns about the fundamental condition of its tenants, particularly its largest tenant, have resulted in shares of the company coming under pressure in recent months. But just around the corner is an opportunity for the company to update investors as to its overall health. This is because, on February 23rd, before the market opens, the management team at the firm is slated to report financial results covering the final quarter of the company's 2022 fiscal year. Leading up to that time, it's important to note that analysts don't have all that rosy an outlook for the company. But all the data that has been made available up to this point suggests that the company is in fine health and that shares remain meaningfully underpriced. All things considered, I do believe that MPW stock still represents a ‘strong buy’ opportunity for long-term, value-oriented investors.

Analysts have a negative outlook

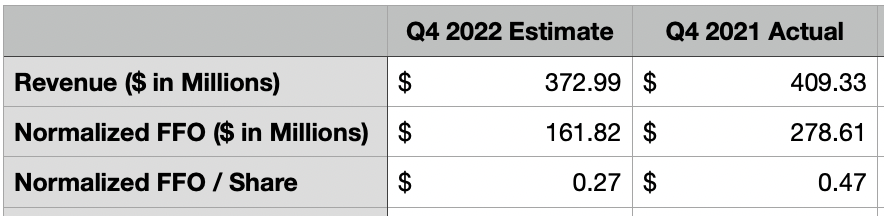

As I mentioned already, Medical Properties Trust is getting close to announcing financial results covering the final quarter of the company's 2022 fiscal year. Leading up to that time, analysts have a rather negative outlook for the company. For instance, the current expectation is that revenue will come in at $372.99 million. If this comes to fruition, it would translate to an 8.9% decline compared to the $409.33 million the company generated the same time one year earlier. At first glance, it may seem odd for a REIT to report declining sales. But this wouldn't be the first time the company reported a drop in revenue.

{kind=link}

In the third quarter of 2022, sales came in at $352.3 million. That compared to the $390.8 million reported in the third quarter of 2021. In addition to seeing sales drop, the company missed analysts' expectations by $36.7 million. This decrease in revenue was driven entirely by operating lease revenue charged by the company plunging $47.9 million year over year. The biggest portion of this came from straight-line rent, which dropped 58.9% from $64.6 million to $26.6 million. Management attributed this decline really to a $72.7 million decrease caused by asset disposals. It would not be surprising, then, to see this trend continue.

Although analysts may focus to some degree on earnings per share, that's a metric that's not all that important when it comes to REITs. More important will be the normalized FFO, or funds from operations, that management reports. The current forecast is for this to come in at $0.27 per share. That would mark a significant decline compared to the 47 sons per share reported the same time last year. Truth be told, I find this call by analysts to be peculiar. After all, during the third quarter earnings release, management forecasted normalized FFO per share for 2022 of between $1.80 and $1.82. At the midpoint, that would translate to a reading in the fourth quarter of $0.43 per share.

It is always possible that the company could come in below expectations. After all, when it reported for the third quarter, it did miss expectations by $0.03 per share when it came to normalized FFO. However, there's a big difference between a miss and a scenario where the company looks to be in bad shape. And I would like to think that there would be signs of trouble ahead of time. But this doesn't appear to be the case. The biggest concern that investors have had involves the company's exposure to Steward Health Care System. As of the end of the third quarter, about 29.5% of the company’s revenue is tied to Steward. There have been many who have expressed concern about the ability of Steward to survive in the current environment. Naturally, having its largest operator, which is responsible for such a large portion of revenue, go bankrupt could prove painful. But as I detailed in an article last year, the picture there looks nowhere near as bad as many suggest.

One really great development for Medical Properties Trust came about on February 15th when the company announced that it agreed to lease its Utah hospital portfolio to Catholic Health Initiatives Colorado. That enterprise is a wholly-owned subsidiary of CommonSpirit Health, which agreed to acquire the Utah hospital business that has been operated by Steward Health Care System. This is noteworthy because Medical Properties Trust’s exposure to Steward has long been a key contributor to the stock’s low trading multiple since the health of Steward has, multiple times, been called into question.

This move will reduce Medical Properties Trust’s gross asset exposure to Steward from 26% to about 20% based on data from Medical Properties Trust’s third-quarter filing. The move will bring with it a 15-year initial lease term, with payments equal to 7.8% of the firm’s gross investment in the properties. Each year moving forward, those payments are expected to rise by 3%. At the 5, 10, and 15 points from the date of closing, CommonSpirit Health will have the ability to acquire the properties from Medical Properties Trust at the greater of the asset’s fair market value or Medical Properties Trust’s gross investment in the properties. Further exposure reduction is also expected, with Steward electing to use at least some of the proceeds to prepay loans extended to it by Medical Properties Trust during the second quarter of the 2022 fiscal year. This should total $150 million in all. Hopefully, management can reallocate that capital to other, safer, and still-productive means.

In addition to the picture with Steward looking fine, there are other positive developments to take into consideration. For instance, on January 13th, n ews broke that the master lease of four area hospitals and two medical office buildings under Pipeline Health had been approved as part of Pipeline’s successful confirmation of its plan of reorganization after Pipeline entered into bankruptcy. All aspects of the lease are identical to what they were prior to that firm entering bankruptcy. In addition, as part of the agreement, Medical Properties Trust state that it will be paid all rent that accrued during the first half of January of this year but that it will defer $5.6 million of cash run into 2024 that would ultimately be collected with interest. And on top of all of that, the company also announced that the pre-bankruptcy plans for Pipeline involve Medical Properties Trust adding a behavioral facility within Coast Plaza Hospital that will ultimately bring it additional rent. Not only does this remove another pain from Medical Properties Trust, it's also a sign of what could happen in the event that a large operator ends up going under. Separate from this, but also on a positive note, is the fact that Medical Properties Trust announced a $500 million share buyback program late last year. From the start of the program through November 4th, the company repurchased 1.3 million shares for $14 million. It's highly irregular for a company that's troubled to start such an ambitious plan. Though I do think it would be a better idea for the company to use that capital to pay down debt.

{kind=link}

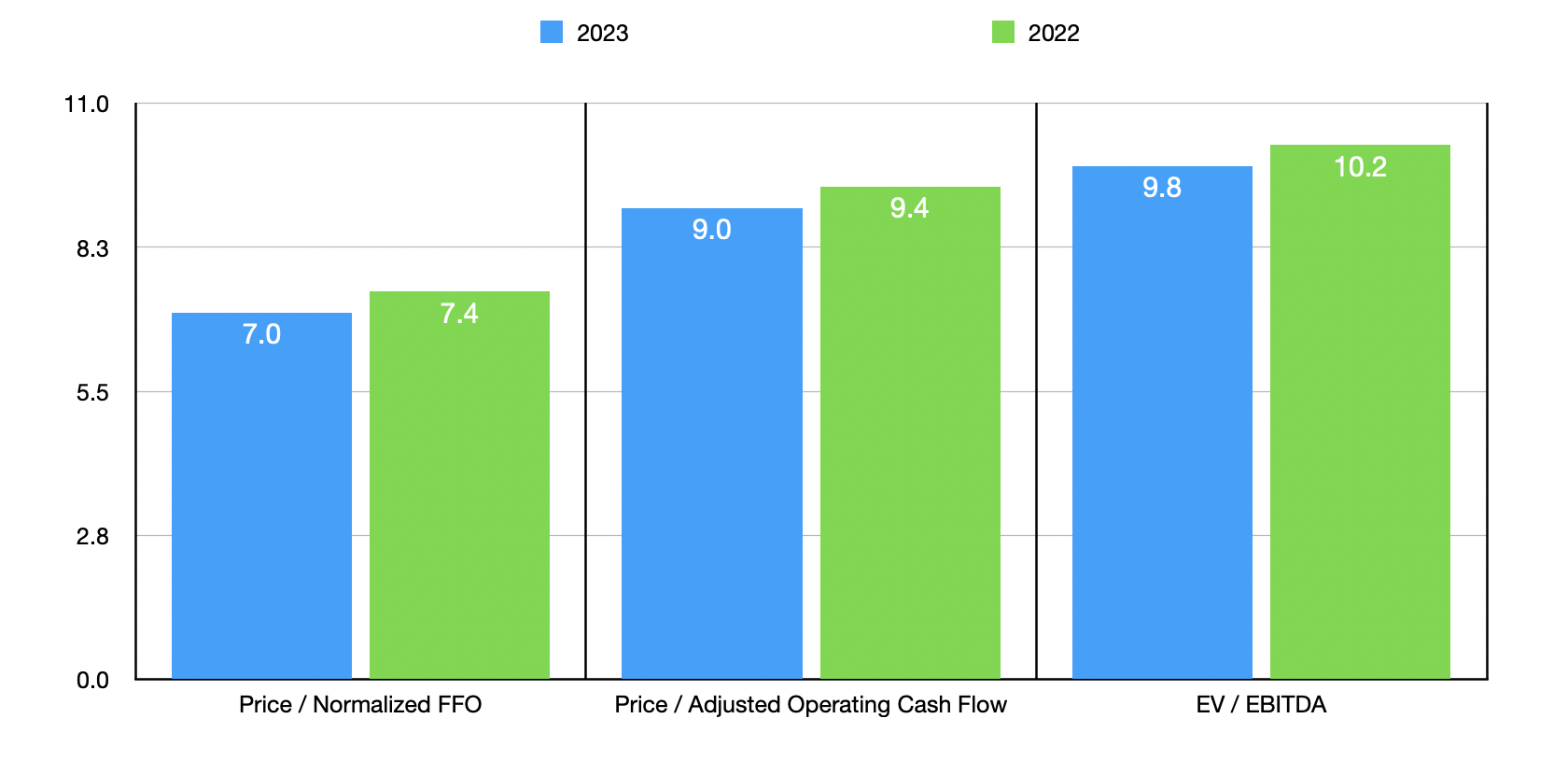

If we assume that management will come through on the guidance that they set in the third quarter, then total normalized FFO for the company should come in at around $1.09 billion for the year. No guidance was given when it came to other profitability metrics. But if we assume that they will increase at the same rate that normalized FFO should, then we should anticipate operating cash flow of $850.9 million and EBITDA of $1.72 billion. Based on these numbers, the company should be trading at a price to operating cash flow multiple of 9, at a price to normalized FFO multiple of 7, and at an EV to EBITDA multiple of 9.8. By comparison, if we were to use the data from 2021, these multiples would be 9.4, 7.4, and 10.2, respectively.

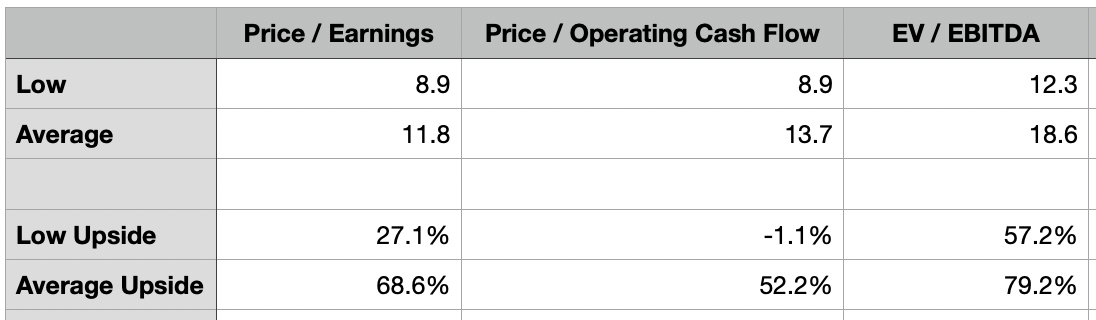

As part of my analysis, I decided to compare Medical Properties Trust to five similar firms. On a price to FFO approach, these companies ranged from a low of 8.9 to a high of 14.9. And when it comes to the EV to EBITDA approach, the range was from 12.3 to 26.5. In both of these cases, Medical Properties Trust was the cheapest of the group. Meanwhile, using the price to operating cash flow approach, the range was from 8.9 to 21.7. In this case, only one of the five firms was cheaper than our target. In order to see what kind of upside the company might offer, I decided to look at two different scenarios. The first scenario valued the company as though it were worth what the lowest of its five peers was worth using all three valuation approaches. The second scenario compared Medical Properties Trust to the average of the five from a valuation perspective.

| Company |

| Price / FFO |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Medical Properties Trust |

| 7.0 |

| 9.0 |

| 9.8 |

| Healthcare Realty Trust ( HR ) |

| 12.7 |

| 21.7 |

| 26.5 |

| Omega Healthcare Investors ( OHI ) |

| 9.6 |

| 11.4 |

| 12.3 |

| Physicians Realty Trust ( DOC ) |

| 14.9 |

| 13.0 |

| 14.6 |

| Sabra Health Care REIT ( SBRA ) |

| 8.9 |

| 8.9 |

| 20.4 |

| National Health Investors ( NHI ) |

| 12.9 |

| 13.6 |

| 19.4 |

In the first scenario, you can see that, when it comes to the price to FFO approach, implied upside for investors is 27.1%. If we use the price to operating cash flow approach, it might actually be overvalued by 1.1%. Though it's worth noting that if we ignore the cheapest competitor, upside would be 26.7%. And when it comes to the EV to EBITDA approach, upside would be 57.2%. Using, instead, the average approach, we would get upside of between 52.2% and 79.2%, depending on which valuation method we utilize.

{kind=link}

Takeaway

Since I created my new portfolio back in March of last year, the market has experienced a great deal of pain. Although the S&P 500 has shown a nice recovery in recent months, it's still down 8.4% since then. Fortunately, I'm still up, with returns of 14%. Sad as it is to admit, Medical Properties Trust is one of the two companies in my portfolio that's been giving me a hard time. At present, that particular holding is down 20.6%, making it my worst play to date. With all that said though, I have a tremendous amount of faith in the company and its ability to perform well moving forward. Naturally, that picture could change based on what ends up being reported by management. And because of that, investors should pay careful attention when the company does report its earnings later this month. But given how cheap the company is, both on an absolute basis and relative to similar firms, and given the other signs that we have seen that suggest management is at least bullish about the firm, I still maintain that it makes for an excellent ‘strong buy’ candidate moving forward.

For further details see:

Medical Properties Trust Q4 2022 Earnings Preview: A Great Prospect Ahead Of Earnings