SBRA - Medical Properties Trust: Still Drastically Undervalued

- Medical Properties Trust has been hit a bit in recent months, driven in part by management failing to keep up with analysts' expectations.

- Although this is a negative in and of itself, the company continues to demonstrate that it's a high-quality operator that's trading on the cheap.

- Investors would be wise to consider adding the firm to their portfolios given the upside potential it appears to offer.

Those who follow my work closely know by now that I run a very concentrated portfolio. At present, I have only six holdings in it. The fourth largest of these by portfolio percentage is Medical Properties Trust ( MPW ), a REIT that focuses on the ownership of medical real estate. Recently, share price performance for the company has not been all that great, but this comes at a time when fundamentals for the business remain robust. Although the company recently announced financial results for the second quarter of its 2022 fiscal year that did not really please the market, I do believe that the business still offers significant upside potential for investors moving forward.

Medical Properties Trust's good performance isn't appreciated

On May 30th of this year, I wrote an article that was extremely bullish on Medical Properties Trust. I called the company a stellar opportunity with strong fundamentals that offered a history of attractive growth when it came to both revenue and cash flows. I said that debt levels were reasonable and that the yield on the company was most certainly appealing. As of this writing, the yield on the firm is 7.1%. I also acknowledged that shares were cheap, both on an absolute basis and relative to similar firms. This all led me to rate the business a 'strong buy', but things have not gone exactly as planned. Since the publication of that article, shares have generated a loss for investors of 9%. This compares to the 1.9% increase experienced by the S&P 500 over the same timeframe.

{kind=link}

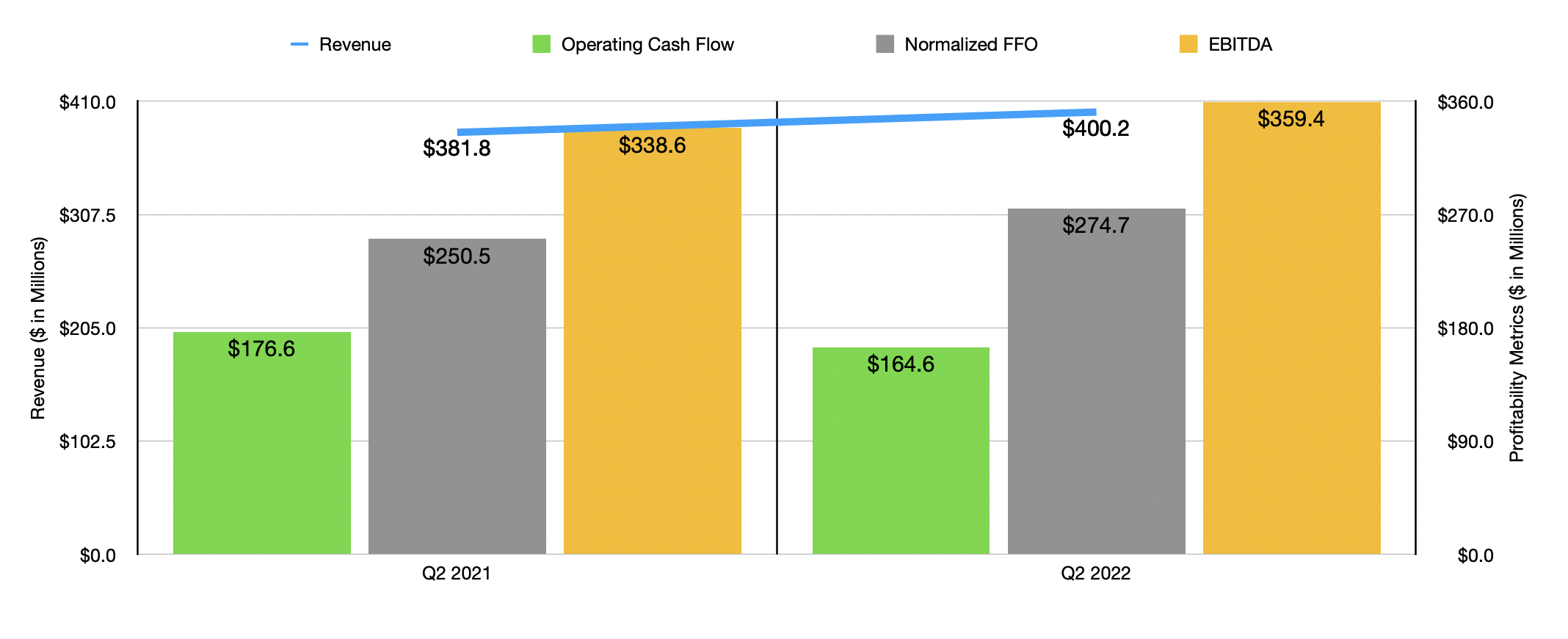

The tricky thing about the market is that even when financial performance comes in positive, if it doesn't come in positive enough, there could still be pain for the company and shareholders in question. This seems to have been the case regarding Medical Properties Trust and the financial performance figures it revealed for the second quarter of its 2022 fiscal year. Consider, for instance, the company's revenue. During the quarter, sales came in at $400.2 million. Although that's 4.8% higher than the $381.8 million generated one year earlier, it still missed analysts' expectations to the tune of nearly $0.7 million. FFO, or funds from operations, per share actually beat analysts' expectations by $0.01, coming in at $0.46 for the quarter. Despite these mixed but generally positive results, shares of the business fell 4.9% in response to the news.

Part of the problem seems to have been related to expectations that analysts had that were just out of touch with what management had previously forecasted. For the year as a whole, management said that normalized FFO should be between $1.78 and $1.82 per share. This guidance comes in spite of the fact that management recently engaged in multiple transactions that should add to the company's top and bottom lines over time. For instance, it agreed to develop one property here in the US for $35 million. It purchased a hospital in Colombia for $26 million. It purchased three radiotherapy facilities in Spain for 27 million euros. And it agreed to develop three other facilities in Spain for 121 million euros. This is not to say the company didn't sell off any assets. It did sell one property in Kansas for $63 million. Although this would beat out the $1.75 per share reported for the company's 2021 fiscal year, it seems to be coming in light compared to the $1.82 per share analysts have been expecting. But beyond that, there really is not much reason for the decline in share price the company experienced during the day.

{kind=link}

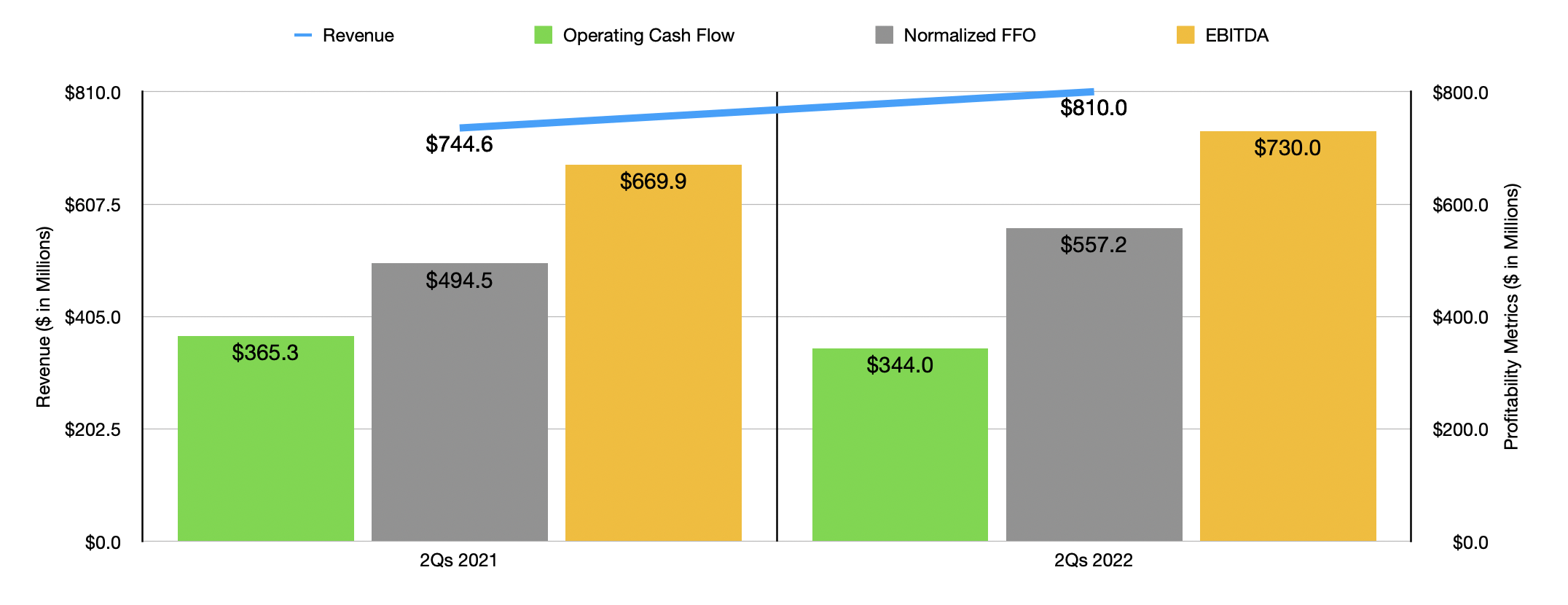

Across the board, fundamental performance came in quite strong. In addition to seeing revenue rise, taking sales for the first half of the year up to $810 million compared to the $744.6 million generated one year earlier, profitability also increased. We already covered normalized FFO per share. In absolute dollar terms, this metric came in at $274.7 million. That's 9.7% above the $250.5 million generated at the same time one year earlier. Thanks to this strong showing, the year-to-date results are also looking good, with the metric rising by 12.7% from $494.5 million in the first half of 2021 to $557.2 million in the first half of this year. This is not to say that everything has been great. Operating cash flow in the latest quarter came in at $164.6 million, which was down from the $176.6 million seen one year earlier. For the first half of the year as a whole, it declined from $365.3 million to $344 million. Even though there was pain on this front, EBITDA rose from $338.6 million to $359.4 million, while for the year-to-date period it increased from $669.9 million to $730 million.

{kind=link}

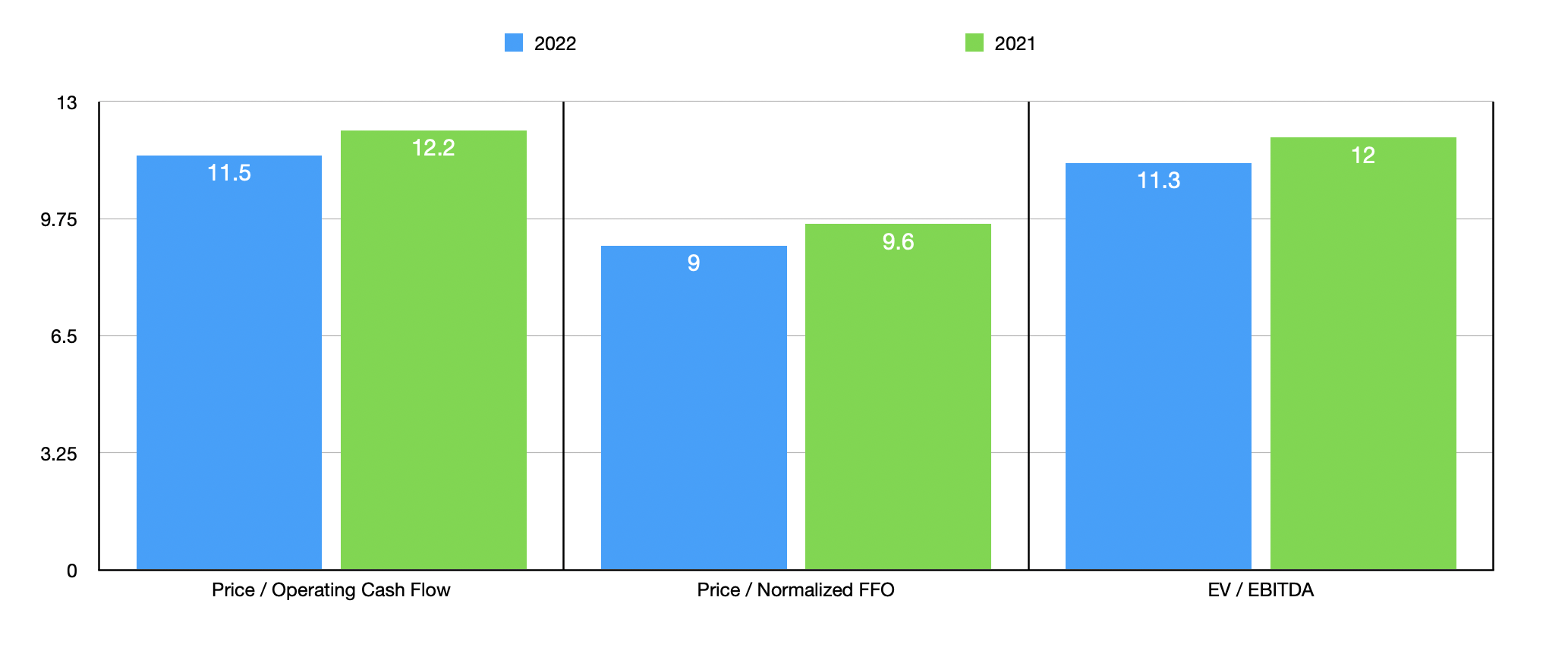

When it comes to the 2022 fiscal year as a whole, meeting midpoint expectations on normalized FFO per share implies normalized FFO of $1.10 billion. No guidance was given when it came to other profitability metrics. But if we assume that the year-over-year change for those will match what we should see with normalized FFO, then we should anticipate operating cash flow of $861.1 million and EBITDA of somewhere around $1.74 billion. Taking these figures, it's pretty easy to value the firm. On a forward basis, the company is trading at a price to operating cash flow multiple of 11.5. This is down from the 12.2 reading that we get if we rely on 2021 results. The price to FFO multiple is 9, which is down from the 9.6 reading we get using our 2021 figures. And the EV to EBITDA multiples should decline from 12 to 11.3. To put this all in perspective, I decided to compare the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 10.1 to a high of 41.9. Two of the five companies were cheaper than Medical Properties Trust. And using the EV to EBITDA approach, the range was between 14.8 and 40.6. In this scenario, our prospect is the cheapest of the group.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Medical Properties Trust |

| 11.5 |

| 11.3 |

| Sabra Health Care REIT ( SBRA ) |

| 10.1 |

| 25.1 |

| Omega Healthcare Investors ( OHI ) |

| 10.9 |

| 14.8 |

| Healthpeak Properties ( PEAK ) |

| 17.0 |

| 21.5 |

| Physicians Realty Trust ( DOC ) |

| 15.1 |

| 20.8 |

| Healthcare Realty Trust Incorporated ( HR ) |

| 41.9 |

| 40.6 |

Takeaway

Although the market was disappointed with the performance reported by Medical Properties Trust, I see the fundamental condition of the company in a favorable light. I think that shares are attractively underpriced, the yield is high, and the outlook for shareholders is positive. All things considered, I still do believe that it warrants a 'strong buy' rating at this time and, absent something changing, I intend to continue holding my stock in it for the foreseeable future.

For further details see:

Medical Properties Trust: Still Drastically Undervalued