MPW - Medical Properties Trust: The Reversal Might Have Begun

2023-06-09 11:10:22 ET

Summary

- Despite the recent nearly 30% bounce off the 2023 lows of MPW’s share price, short interest remains high.

- Management began addressing the attacks against the company as well as de-leveraging/de-risking transactions.

- Business conditions in the medical operators’ sector may be improving, which should benefit MPW.

- In terms of valuation, MPW is still considerably below its peers as well as its own historical multiples, presenting an opportunity.

Medical Properties Trust (MPW) has been one of the most discussed stocks on Seeking Alpha, due to its high dividend yield and the short attacks that have been targeting the company. While the share price has rebounded nearly 30% off its 2023 lows, short interest remains quite high, making the stock a potential short squeeze candidate, but also indicating that a lot of market participants maintain a negative outlook. At the same time, management began fighting back as it filed a lawsuit against the main source of the short attack and recently uploaded a special presentation, aimed towards restoring investors' confidence.

Looking at the broad picture, interest rate hikes - the main concern of investors seem to be over, and even some cuts are expected towards the end of the year. A positive sign could also be found in the performance of the medical operators sector, which was struggling during the pandemic years. In light of this and what appears to be a significant discount to peers, I think that the latest move in MPW's is a reversal, rather than a dead cat bounce.

Management takes the initiative

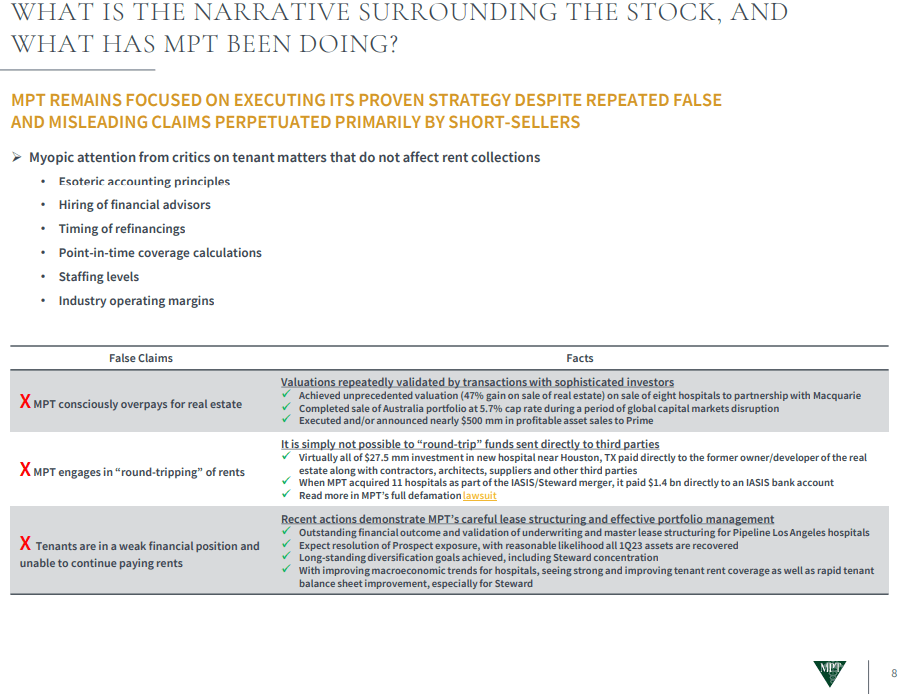

In the very beginning of the year, the short attack was in full force, but management seemed to be ignoring it. Instead, MPW was focusing on de-risking and de-leveraging transactions such as the CommonSpirit deal, which I covered here and the sale of its Australian assets, which I also wrote about. However, In the end of March, management has had enough and filed a lawsuit against the most active source of the short-attack - Viceroy Research, accompanied by a letter to MPW's shareholders, refuting some of the claims against the company.

MPW against the narative (MPW)

{kind=link}

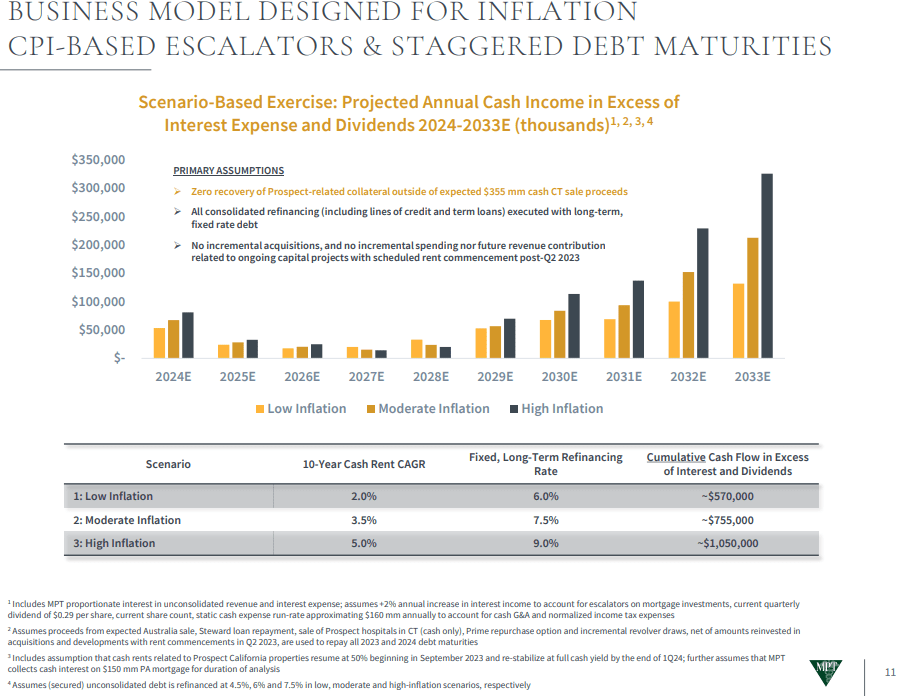

Resilient business model reconfirmed

Just days ago, a special presentation was uploaded by MPW, aiming to boost investors' confidence in the company. The document emphasizes the strength of MPW's business model as its leases poses inflation-adjustment characteristics, which could pretty much off-set higher financing costs in the future. The simulation done by the company indicates that MPW should be able to generate sufficient cash flow, which more than covers the dividends.

MPW's inflation resilient business model (MPW)

{kind=link}

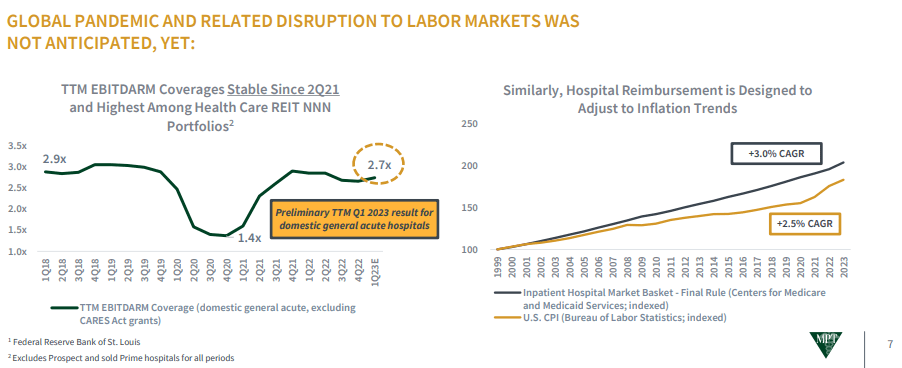

Medical operators' business conditions might be improving

Still, the resilience of MPW's business model could be boiled down to medical operators' business viability. After all, MPW's rent escalators are useless if the tenants are unable to pay their rent. Such is the case with Prospect Medical, which is in financial trouble and has halted payments to MPW, while working on a turnaround. Recently, Prospect obtained US$375M in third-party financing, which could be interpreted as a positive sign.

Medical operators EBITDARM coverage (MPW)

{kind=link}

Looking at the broad hospital operators market, the business conditions may be improving. Data, presented by MPW, indicates that the TTM EBITDARM coverage of the sector is at 2.7x, which is close to the pre-pandemic levels. An insight in the industry could also be obtained from the Q1'23 earnings call of one of the biggest public medical operators in the USA - HCA Healthcare (HCA):

The operational momentum we had at the end of the last year continued into the first quarter of 2023. The company produced solid earnings that reflected strong demand for our services and improvements in our operating costs in particular contract labor expenses.

- Sam Hazen, CEO of HCA

Our consolidated adjusted EBITDA margin was 20.3% in the quarter. Labor cost as a percentage of revenue improved both sequentially and when compared to the prior year and our supply costs continue to trend favorably as well.

- Bill Rutherford, CFO of HCA

While there's no guarantee that the positive cost developments, observed in HCA are also present in MPW's tenants, it gives us an educated guess of how things might be developing there.

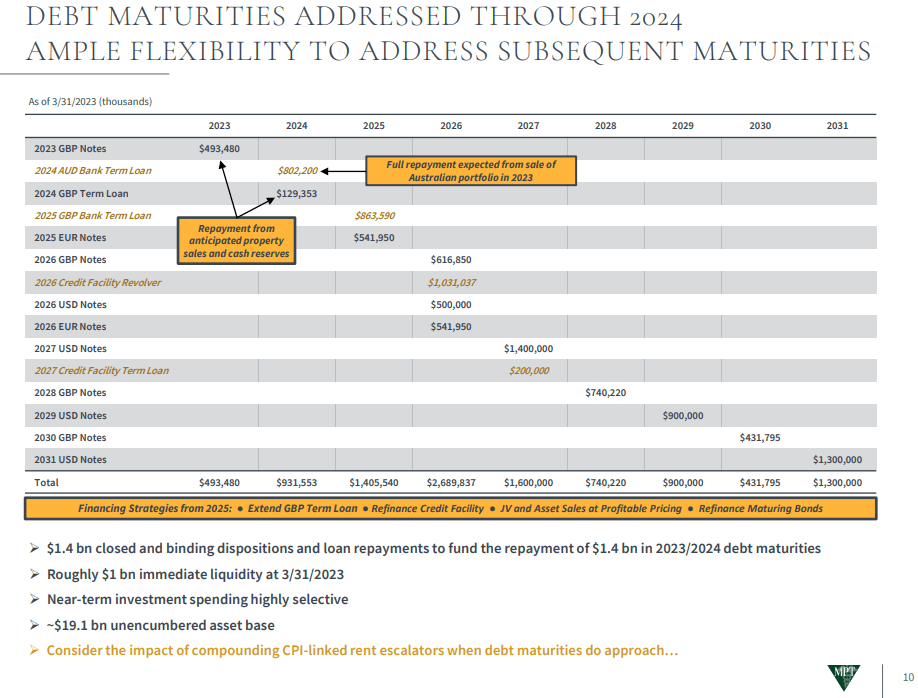

Debt should be manageable

Debt schedule (MPW)

{kind=link}

Following the sale of the Australian assets, MPW should be able to cover its debt maturities through 2024. This gives the company much needed time to take an adequate decision towards the larger maturities that come due in the 2025-2027 period. The three possible ways to approach this are to stop/reduce the dividend, sale some assets or roll the debt forward. Of course, a combination between these options is also possible. However, I see the first option - cutting the dividend more like a last resort, since management has elected to maintain it, despite the problems with Prospect. Asset sales is a reasonable option as long as the sale price stays around to even better above book value, as currently MPW is trading at a considerable discount to its book value. The third option - refinancing, seems the best, as this is in the lifeblood of REITs.

FED funds rate expectations (CME Group)

{kind=link}

While the current raising interest rates environment is not the best for raising debt, the course of monetary policy could soon change. The market even expects some rate cuts towards the end of this year, which should make it easier for MPW to refinance in 2024. Looking back at historic rate movements, the FED has generally cut rates much faster than they were raised.

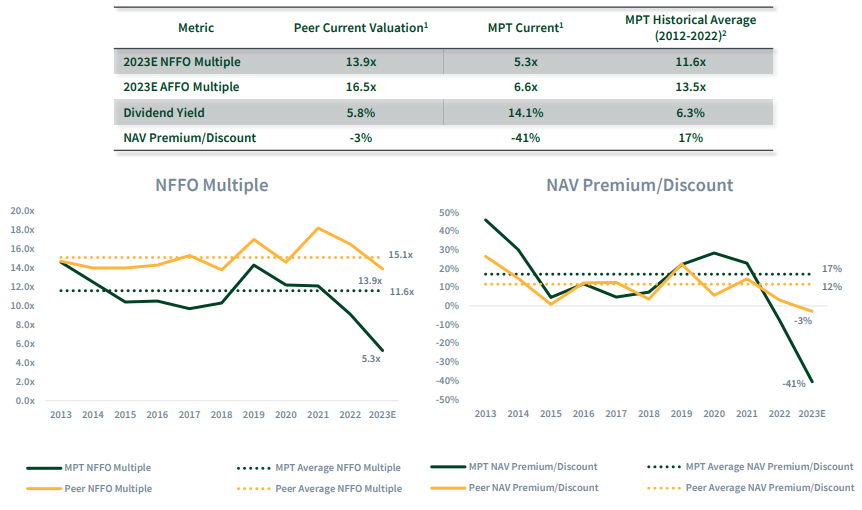

Valuation

MPW currently depressed share price results in deep discount to both the peers in the industry and to MPW's own historical multiples as well. I expect that the stock should return at least to its own average as time passes by and management is able to address the tenants issues, while the overall macro environment for the healthcare sector improves.

Multiples analysis (MPW)

{kind=link}

I see potential upside triggers in resolution of the issues with Prospect and/or diversifying away tenant exposure from Steward and Prospect, preferably towards publicly listed operators, which have timely and transparent financials.

Risks

Tenants risk

The biggest risk for MPW are related to its tenants' financial condition. If restructuring at Prospect doesn't yield the desired results and the company is unable to resume full payments in the anticipated timeline and or more tenants, for example Steward, begin having difficulties to pay their rent, MPW will suffer. In such a scenario, cut in the dividend is likely. However, the indications from public medical operators' Q1'23 results, suggest that the business environment is improving.

Monetary policy risk

Another significant risk is related to tight monetary policy. Raising interest rates and tight supply of credit could lead to higher cost of refinancing the existing debt of MPW. However, inflation is trending downwards, and the market expects that the rate hikes are pretty much over, with anticipations of monetary policy easing towards the end of the year.

Conclusion

MPW's share price has bounced-off the March 2023 lows and is nearly 30% higher. While short interest remains elevated, indicating that some investors think the move is a dead cat bounce, I disagree with that view. In my opinion, the move is likely a reversal as business conditions in the medical operators' sector are improving and MPW's management is addressing the short attack against the company. Despite the recent run-up, MPW remains at a considerable discount to its peers and its own historical multiples, which presents an opportunity to bet on mean-reversion.

For further details see:

Medical Properties Trust: The Reversal Might Have Begun