VNO - Medical Properties Trust: The Streets Flow With Blood

2023-08-23 10:34:23 ET

Summary

- The market is pricing MPW for a future where book value and funds from operations decline by half.

- The fundamental narrative for MPW is bleak with downgrades, negative press, and short interest abound.

- By cutting its dividend, MPW is finally getting serious about its debt problems.

- When the streets flow with blood, our contrarian nature takes notice.

Our investment thesis for Medical Properties Trust ( MPW ) is simple: the streets are flowing with blood. Lots of blood.

If anyone were to ask you what a "falling knife" is, just show them this chart:

That's what MPW is: a falling knife. And that knife has been cutting/slashing/hacking with surgical precision. A lot of hands have been gashed and the streets are inundated with the blood of woeful investors. Shares have become victim to a series of rating downgrades from analysts:

- August 21 - J.P. Morgan

- August 19 - Juxtaposed Ideas (Seeking Alpha)

- August 16 - On the Pulse (Seeking Alpha)

- August 11 - Raymond James

- August 11 - Bank of America

- August 10 - Samuel Smith (Seeking Alpha)

Seems as though things have really turned for the worse for this Hospital REIT.

Seasoned investors should know how difficult it is to buy low and sell high. By its nature, the market has a tendency to do what no one expects. Oddly enough, it is often when the fundamental narrative is most optimistic that a stock's price tops and when the narrative is most bleak the stock bottoms. Not always, but often. The narrative for MPW, by our assessment, is quite bleak at the moment.

John Maynard Keynes famously stated:

Markets can remain irrational longer than you can remain solvent.

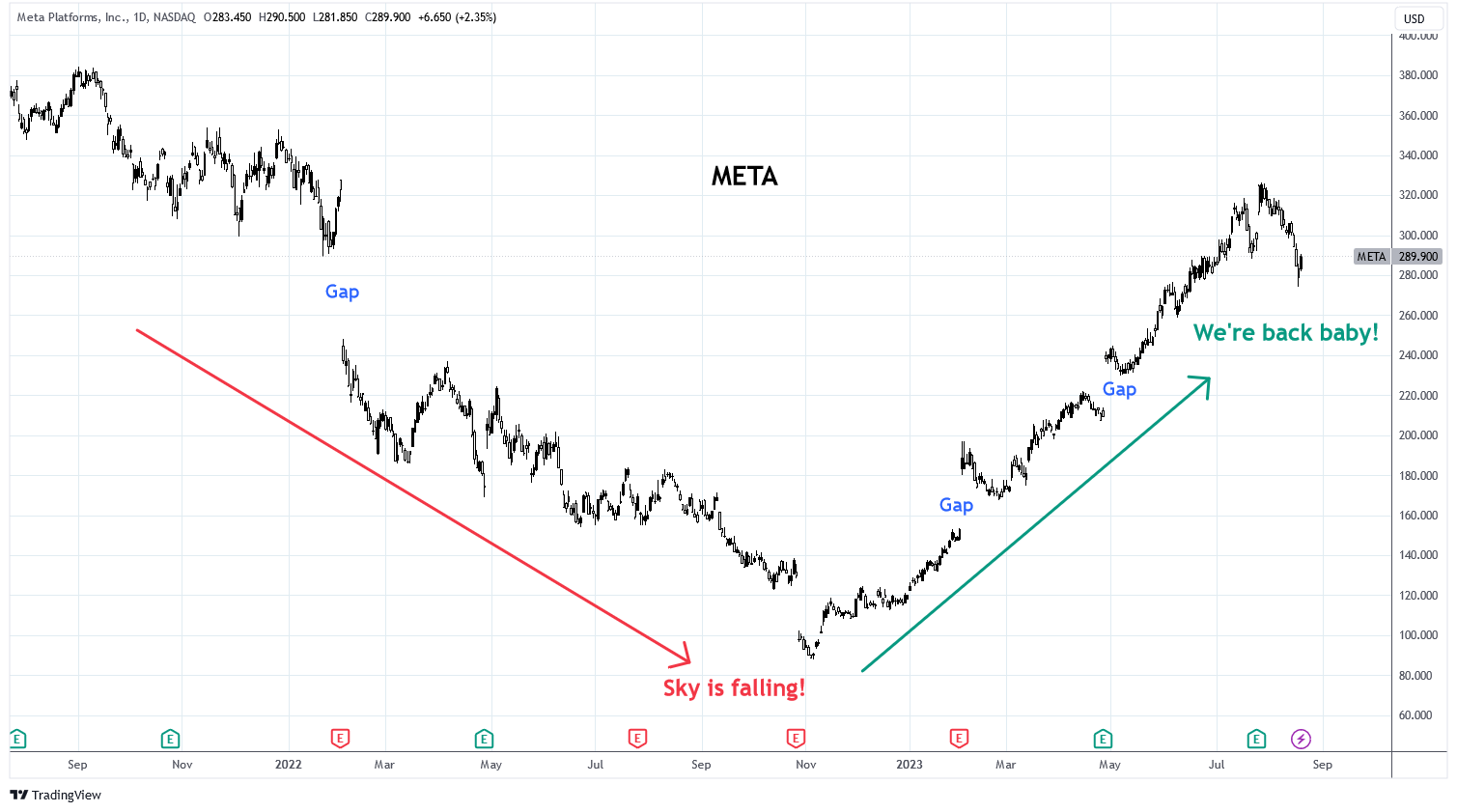

This is often referenced when criticizing the strategy of short selling a market believed to be overvalued. The idea is equally applicable to the opposite side of the spectrum. Momentum is important in markets. Human psychology leads to the tendency to move with the group. It derives from our instincts of survival. When momentum starts to move in a particular direction it easily feeds upon itself. The best recent example of this can be found in the price chart of META, observe:

{kind=link}

Charts by TradingView (adapted by author)

Notice that META shares plummeted 77% in 14 months only to rocket higher 262% in nine months. One can follow the trail of narratives that both justified and fueled each move. On the way down: Facebook was dying as user growth reached its limit, the Metaverse was turning out to be a money pit, competition was going to take market share, management was incompetent. On the way up: WhatsApp is going to be strong, buybacks were bullish, management was genius, subscriptions are improving, TikTok might get banned. But did the fundamentals really change that much? We would argue, no.

But bearish narratives don't become irrational over nothing. They start with actual, serious problems. MPW has problems . Hospitals are still struggling to be profitable in this post-COVID environment. MPW continues to have issues with tenants paying rent and managing its debt service.

This isn't to say that MPW is the next META, it's not.

The situation reminds us of another REIT debate that involved one of Brad Thomas ' controversial picks: Tanger Factory Outlet Centers, Inc. ( SKT ). Brad famously took heat for remaining bullish on SKT through a nasty bear market. His articles are numerous throughout 2017-present with bullish takes on the mall REIT.

{kind=link}

Seeking Alpha

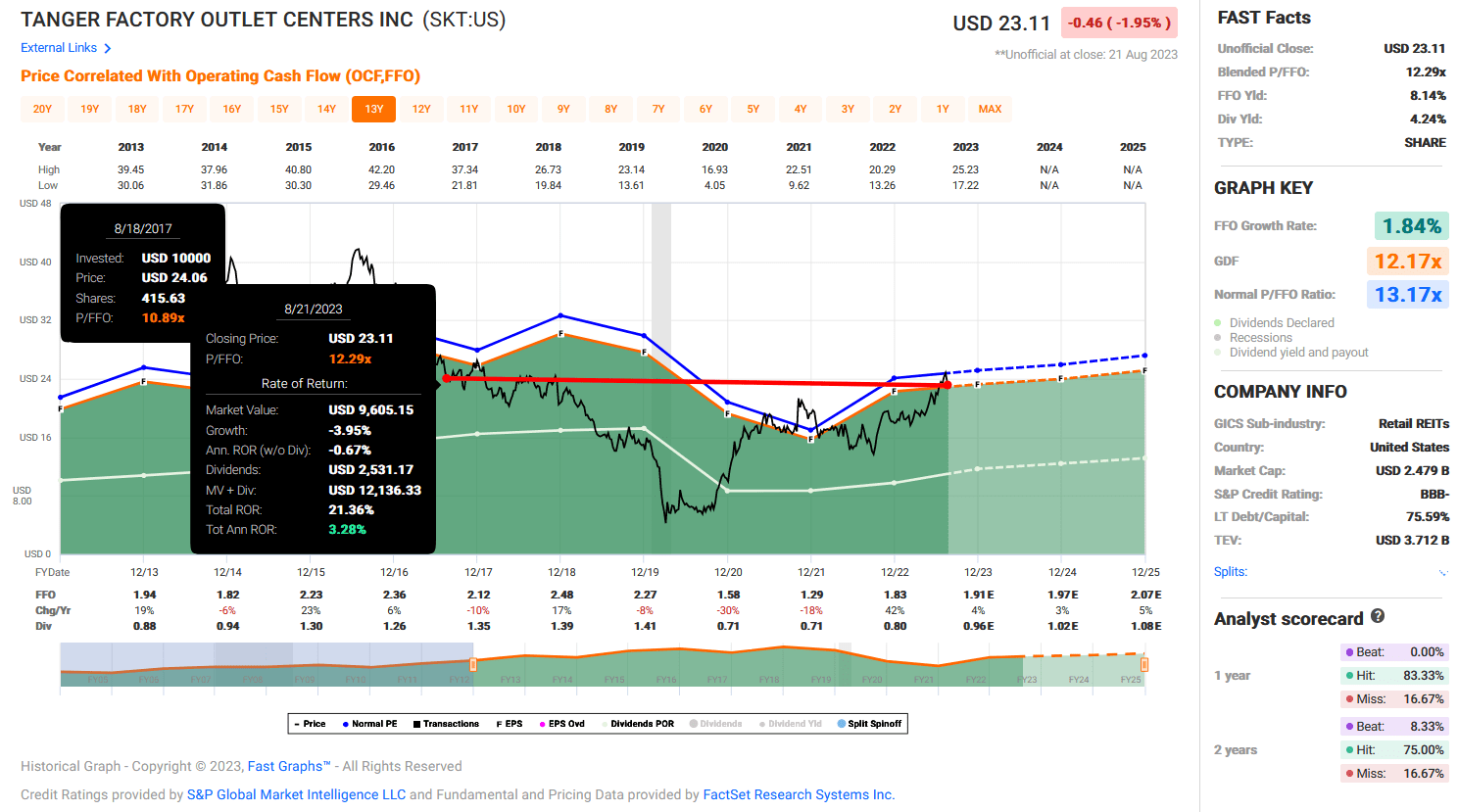

By our assessment, Brad was right. Shares of SKT have recovered to the $23 level. This may not seem like a victory, given that shares traded above $30 in 2016, but there's more to the picture. COVID caused SKT to take a huge hit to operating cash flow, a truly black swan event. What's more important is that shares have traded up to a higher valuation during this span, upgrading from 10.89x FFO in 2017 to 12.29x FFO today. If it were not for COVID contributing to a 43% decline in FFO its possible that shares could already be trading at $30+.

{kind=link}

FAST Graphs

The point is this: sometimes, the market can be irrational for a long, long time. This is where we see the similarities. Brad is now taking similar heat for bullish calls on MPW. His latest piece, Medical Properties Trust: Let Me Tell You About The Lonesome Loser , acknowledges this. SKT cut its dividend in May 2020, 40 days after shares bottomed. MPW cut its dividend last Monday. Sometimes, analysts get bullied for their view because it doesn't fit with the market. Sometimes, it's the darkest before the dawn. Sometimes the streets flow with blood .

Fundamental Overview

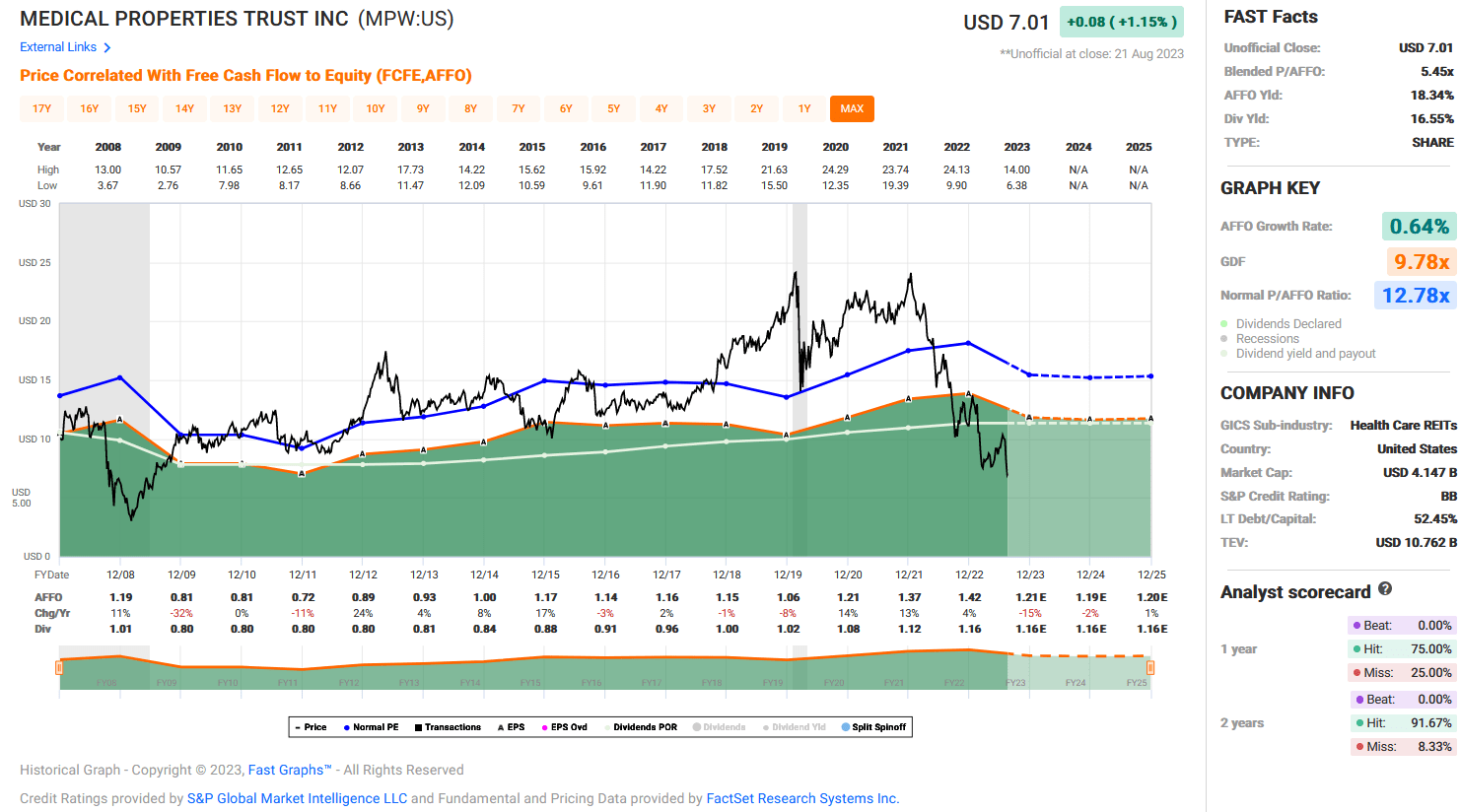

A brief fundamental examination of MPW is where we begin. Shares of MPW trade at a blended AFFO yield of 18.3%. Management has guided for NFFO in $1.53-$1.57 per share. This puts the guided NFFO yield around 22%. Analysts are expecting little change in AFFO in 2024 and 2025 with forecasts of -2% and 1%, respectively.

{kind=link}

FAST Graphs

The last time that MPW traded at price multiples this low was in 2008-09 during the GFC. As a reference, shares traded as low as 2.7x AFFO compared to the current multiple of 5.45x. The REIT has a price to tangible book value of 0.5. Tangible book value has been declining in recent quarters, but share the price has declined much faster resulting in a valuation that is close to the lowest in company history.

This fundamental overview is a brief but insightful examination of the company's current position. By these appearances, shares look attractively priced. The market appears to be pricing in shares of MPW for a future where book value declines by half and funds from operations decline by half. But there's more.

Dividends and Debt

For many investors, the recent dividend cut was just one more stab by this falling knife. We, on the other hand, are surprised at how long it took. The company cut its quarterly dividend from $0.29 to $0.15 a share. At current prices this represents a yield of 8.5%. We do not need a yield higher than 8.5% and we especially do not need a yield higher than this when the capital can be used to improve the balance sheet. This is the objective of the dividend cut.

The company will use this cash to reduce debt and its cost of capital. The company has $500 million of debt maturing at the end of 2023 and $315 million in May of 2024. At the end of last quarter MPW had about $324 million in cash. The dividend cut will free up about $83.7 million in cash per quarter. MPW has been selling properties to reduce the debt on its balance sheet as it grapples with higher interest rates and the cost of refinancing their debts. Here is a partial description of this plan from the Q2 10-Q report :

On March 30, 2023, we entered into a definitive agreement to sell our 11 general acute care facilities located in Australia and operated by Healthscope Ltd. ("Healthscope") (the "Australia Transaction") to affiliates of HMC Capital for cash proceeds of approximately A$1.2 billion. As a result, we designated the Australian portfolio as held for sale in the first quarter of 2023 and recorded an approximate $79 million net impairment charge, which included $37.4 million of straight-line rent receivables, an estimated $8 million in fees to sell the hospitals, and $13 million of accumulated other comprehensive loss related to foreign currency translation. This impairment charge was partially offset by approximately $29 million of deferred gains from our interest rate swap in accumulated other comprehensive income that was reclassified to earnings as part of this expected transaction. This transaction was set to close in two phases. The first phase closed on May 18, 2023, in which we sold seven of the 11 facilities for A$730 million, with the final phase currently expected to be complete by early fourth quarter of 2023. We used the A$730 million proceeds from the first phase of the sale to pay down the Australian term loan.

In addition, the company is considering the following asset sales:

... strategic property sales or joint ventures, including current binding commitments to sell four remaining Australian properties that will generate proceeds of approximately $315 million and three Connecticut facilities that is expected to generate $355 million.

The issue with selling properties to pay down debt is that it can be dilutive to AFFO. Management referenced this fact in the dividend cut announcement. Using cash flows, from the dividend cut, can accomplish the same purpose of deleveraging without this dilution. This dividend cut may actually be one of many steps that MPW needs to do to right the ship. The company's cost of capital is rapidly on the rise and its access to capital is drying up as the company suffers from downgrades. This was especially exacerbated when the company's credit rating was downgraded by S&P Global to BB, causing the company to lose its investment grade rating. It was cited that the primary reasons for the downgrade was overly concentrated exposure to hospital operations who they themselves were struggling with profitability and credit quality and the ongoing financial support from MPW to its tenants via credit facilities. The use of company cash flows to shore up its balance sheet in an effort to earn back an investment grade credit rating is more valuable to shareholders than the dividend itself, we conclude.

Short Interest

By now, investors should be well familiar with the short interest community for MPW. We must all admit that, at least up until now, the bears have been right. MPW is now the third most shorted REIT, according to Seeking Alpha, at 21% of open interest. That is not insignificant. Only Pebblebrook Hotel Trust ( PEB ) and SL Green Realty ( SLG ) are more shorted. Even the second largest Office REIT, Vornado ( VNO ), has a lower short interest with FFO declining at a CAGR of -11% since 2019.

Seeking Alpha

It might seem like there's enough short interest to say that the bears have sniffed this one out. We frequently see claims by bears that MPW is doomed to fall to $5, $3, or even $0. We're not saying that isn't possible, it certainly is. Although it is yet another sign of feverish despair. But look at the short interest on SKT near its bottom in 2020. Short interest briefly topped 100%. This coincided with the most bearish of fundamental narrative for the company. Short sellers aren't always right and they aren't always wrong. In this case, there were a lot of wrong ones. Many companies that are heavily shorted head for bankruptcy. But feverish bearishness, represented by short interest among other factors, is a sign of narrative despair.

Something Wicked This Way Comes

Clearly, the bear case is about more than just struggling tenants, shrinking margins, a dividend cut, and tightening credit. The discount placed by the market on both the equity and bonds suggests something much more serious. The market implies that the numbers are wrong . It implies that the book value is overestimated and reported cash flows are manufactured or fleeting. Some prominent bears have gone so far as to claim that the company is actually bankrupt.

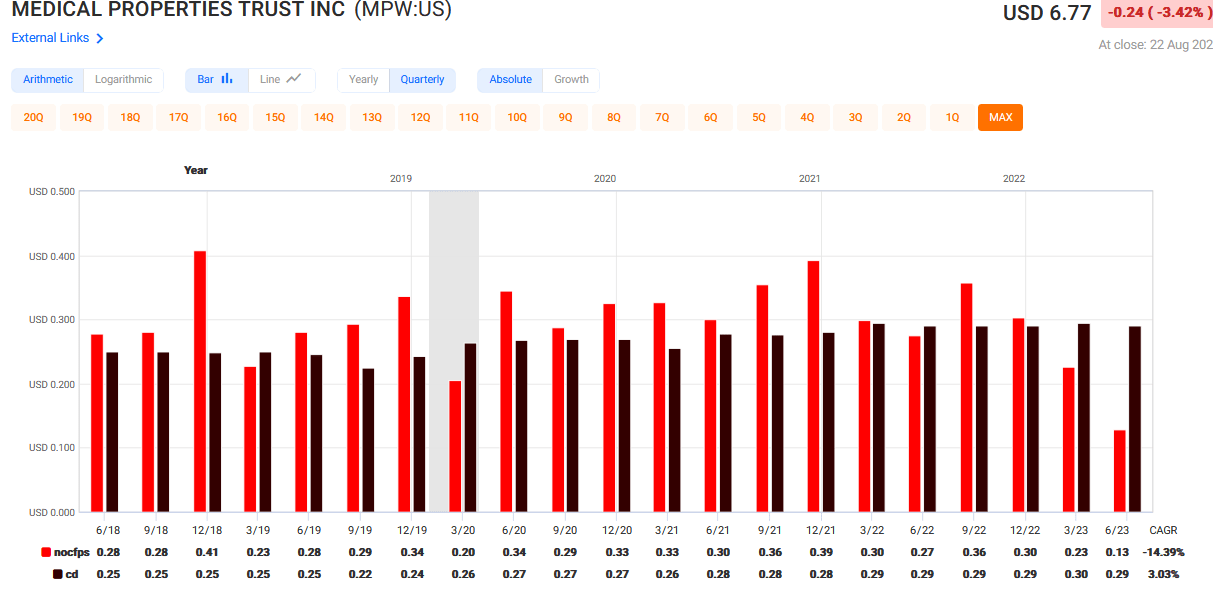

Last week the Wall Street Journal published an article about MPW analyzing the company's financial position. The article pointed out that California regulators have put a hold on the company's transaction with Prospect Medical Holdings and that the company failed to report the development in its latest SEC filing. The article also pointed out that MPW's net operating cash flow has not been covering the dividend over the past two quarters. This is what its net operating cash flow in red and dividend payout per share in dark red looks like since 2018. In Q1 2023, MPW had $0.23 per share of net operating cash flow and $0.30 per share of dividends. In Q2 2023, NOCF per share was $0.13 with a $0.29 dividend. These declines in net operating cash flow are primarily due to declines in FFO and accounts receivable. Even after the dividend cut, last quarter's cash flows do not cover the new dividend. Bears have pointed out that MPW has been covering these dividend payments with more debt. This is misleading. During this span, the company has reduced its total debt by $174 million. It funded the dividend, effectively, through the sale of assets.

{kind=link}

FAST Graphs

The company released a statement in response to the WSJ article. They argued that the hold by California's regulators is not out of the ordinary and stood by the company's accounting methods that the WSJ criticized. On the one hand, we can understand their point. On the other hand, management should know that investors are on edge and that extra transparency is prudent. It does make us wonder, even if not required why not disclose this information willingly?

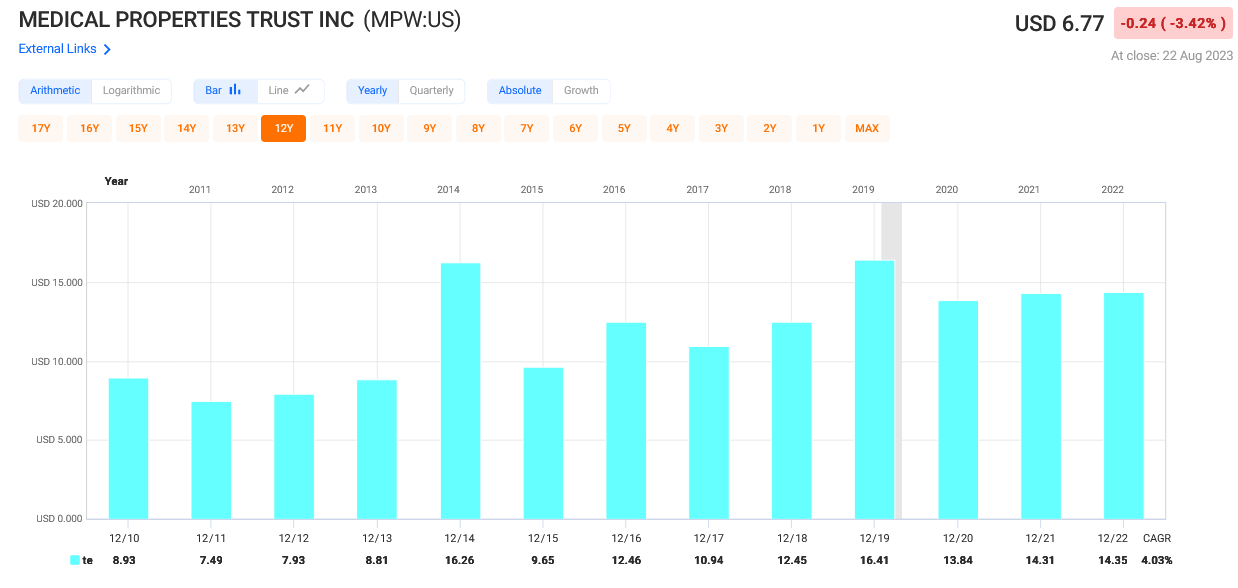

While we have no knowledge of what is accurate or inaccurate about the company's financial reports, we are keen to point to a key fact: for over a decade the company has increased its equity per share (chart below). This is difficult to do without positive cash flow and a persistent business model. The current estimated equity per share is $13.90. Bears will say this figure is overstated. They could be right. But they have to be right for the bear narrative to make sense.

{kind=link}

FAST Graphs

Conclusion

MPW is in a tough place. The fundamentals are bleak, very bleak. Cash flows are taking a dive at precisely the wrong time when the company is facing cost of capital pressures. For the time being, growth is out of the picture. Right now the company should focus on survival.

The inundation of downgrades, bad news events, bad press, and negative online commentary on social media and the like is an indication of the situation. Naturally, markets do not take an optimistic stance in the face of such despair. This is an investment thesis predicated on the idea that being contrarian matters. Let us be clear, being contrarian is not easy. At this time we remain on the sidelines with MPW. We need to see more positive steps toward financial stability. We need to see that cash flows are temporarily impaired and returning to trend. We don't care about the dividend.

But one thing has certainly got our attention: the Streets are flowing. Flowing with blood .

For further details see:

Medical Properties Trust: The Streets Flow With Blood