HOWL - Medicenna: Multiple Catalysts Ahead In 2023

Summary

- Medicenna is testing MDNA11, an IL-2 superkine, with potential in various cancer types, in a phase 1/2 trial called ABILITY.

- A February 2023 update tells us MDNA stock has been able to increase the dose of MDNA11 without issues so far.

- The ABILITY trial is set to produce more data in Q1'23, but also in Q3'23 and Q4'23.

Medicenna Therapeutics ( MDNA ) is a biotech that develops modified cytokines, called superkines, that may have benefit across a range of cancers and inflammatory conditions. This article focuses on MDNA11, an interleukin-2 (IL-2) superkine with potential in various cancers, as we should see additional clinical data from the drug during Q1'23 and throughout 2023.

MDNA11: Developing a better Proleukin

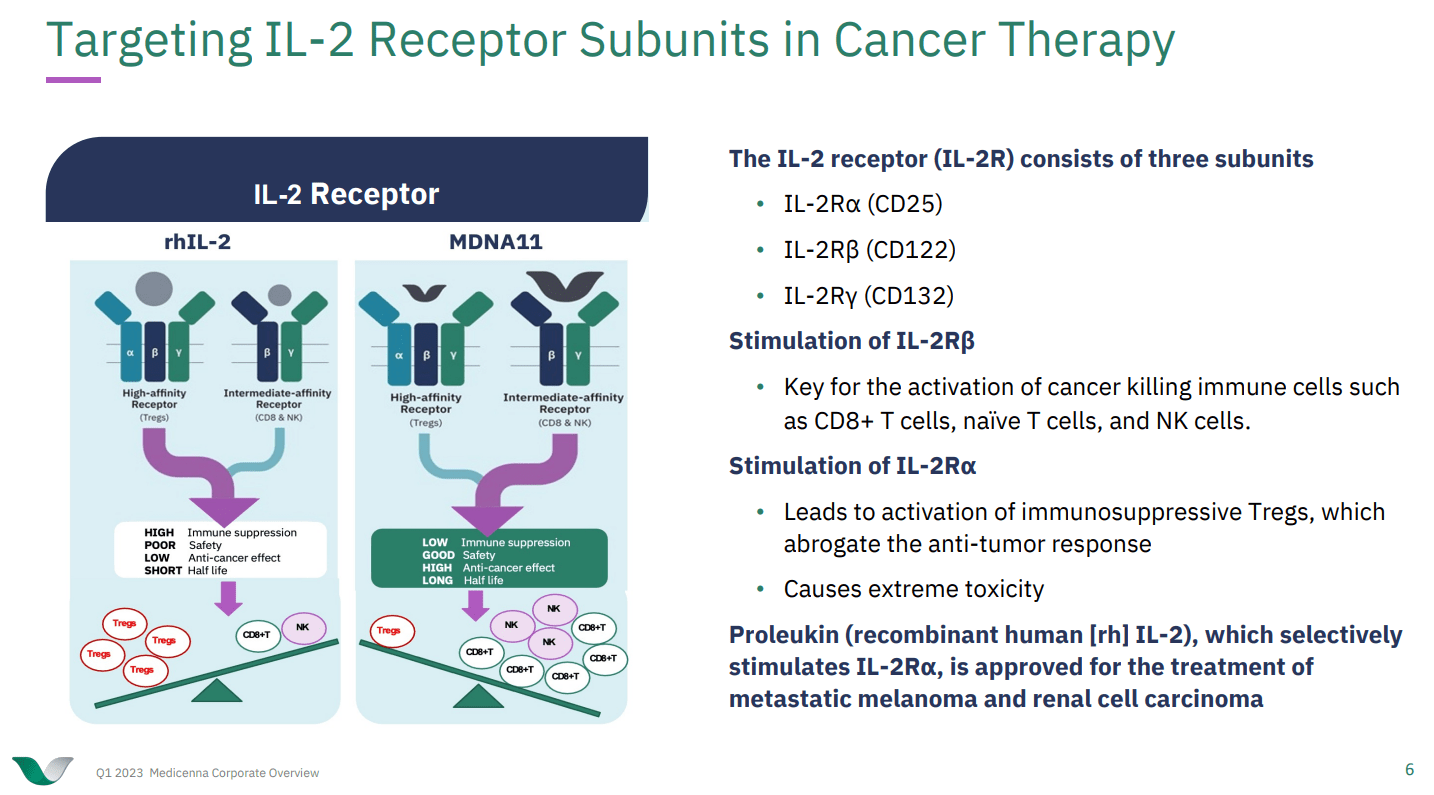

Proleukin (aldesleukin) is a recombinant interleukin-2 (IL-2) product that has been on the market for many years for the treatment of metastatic melanoma and metastatic renal cell carcinoma. The toxicity of Proleukin is notable with the drug having boxed warnings concerning cardiac and pulmonary function and capillary leak syndrome. Since IL-2 produced endogenously, or administered via Proleukin, binds to multiple types of IL-2 receptors, the possibility exists to attempt to hold onto, or improve on the efficacy of Proleukin in cancer, while reducing its toxicity.

MDNA is one of many players trying to improve on IL-2/Proleukin and many of these players in the space have a similar theory on how to do that. IL-2 can bind to alpha subunit-containing IL-2 receptors, found on regulatory T-cells (T-regs), and non-alpha subunit-containing IL-2 receptors, found on CD8+ T-cells and NK cells. If we think of T-regs as anti-inflammatory, or at least as mediating immune tolerance, whereas we think of NK cells and CD8+ T-cells as being involved in doing the killing, in this case of tumor cells, then the idea of targeting activation of CD8+ T-cells and NK cells by activating non-alpha containing IL-2 receptors arises. MDNA11, a superkine developed by MDNA, does exactly that.

Figure 1: MDNA11 targets IL-2 receptors containing the beta and gamma subunit, but not the alpha subunit, thus avoiding activation of T-regs, and favoring the activation of CD8+ T-cells and NK cells. (MDNA Corporate Presentation Q1 2023.)

{kind=link}

MDNA11: Data from the first four cohorts

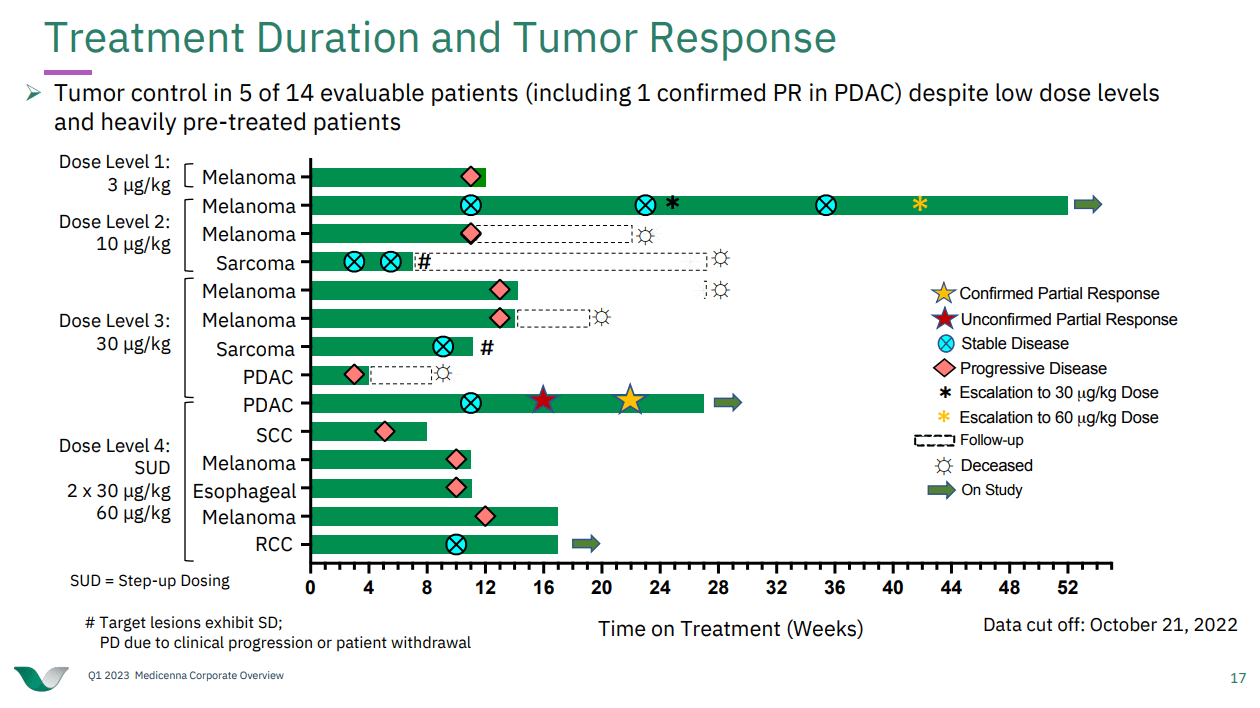

In data from MDNA's phase 1/2 ABILITY trial of MDNA11 in select tumor types, the company has thus far released anti-tumor activity data with a cutoff of October 21, 2022. That data showed that in 14 evaluable patients, there was tumor control in five of them, including a partial response in one pancreatic cancer patient. The data are encouraging in one regard because many of the patients only received lower doses of MDNA11 (ABILITY includes dose-escalation work so that MDNA can select a dose for phase 2). In another regard, we see that at the 60 ?g/kg dose tested so far, there were still examples of progressive disease following treatment initiation.

Figure 2: Response data from MDNA's ABILITY trial of MDNA11. Note that one patient initially dosed at 10 ?g/kg underwent dose-escalation to 30 and then 60 ?g/kg. (MDNA Corporate Presentation Q1 2023.)

{kind=link}

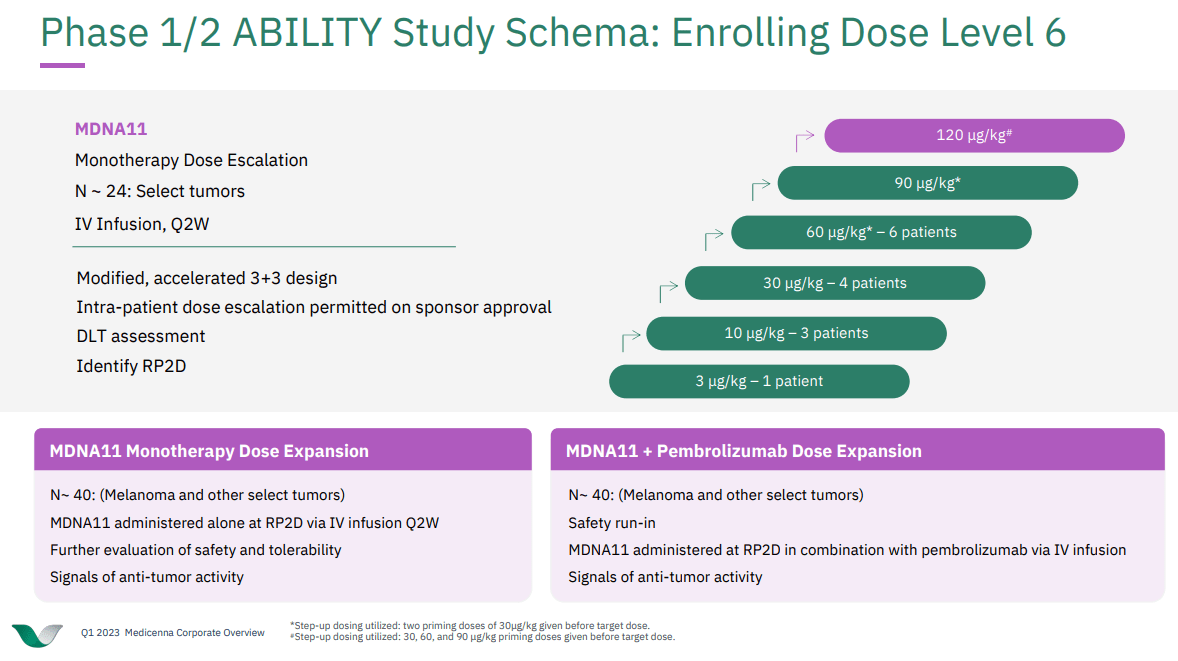

Moving forward with future updates on patient responses to MDNA11, the market will want to see more partial and hopefully complete responses, especially as MDNA is planning to dose about 40 patients with MDNA11 monotherapy at the recommended phase 2 dose, but also another 40 patients with MDNA11 and the approved cancer therapeutic pembrolizumab.

Figure 3: Schematic of the Phase 1/2 ABILITY study of MDNA11 in select tumors. (MDNA Corporate Presentation Q1 2023.)

{kind=link}

The February 2023 update

On February 7 , MDNA announced earnings for the quarter ending December 31, 2022, and provided an update on the ABILITY trial. MDNA noted that the ABILITY study had advanced to the sixth dose escalation cohort, meaning patients are set to be dosed with 120 ?g/kg. More importantly, in those dosed in the fifth cohort (90 ?g/kg) there were no dose-limiting toxicities, de-escalations or discontinuations due to safety seen to date. While MDNA notes there was also more expansion of lymphocytes than with previous cohorts that received lower doses, we didn't see data on anti-tumor activity. The February 7 press release notes that updated anti-tumor activity data from the first four cohorts are still expected in Q1'23, meaning there is a catalyst this quarter for MDNA. Further MDNA expects to report anti-tumor activity data from the sixth dose-cohort and the expansion cohort in Q3'23 with data from the pembrolizumab combination in Q4'23. That means MDNA has lined up three catalyst readouts in the remaining ten months of 2023.

The rest of the pipeline

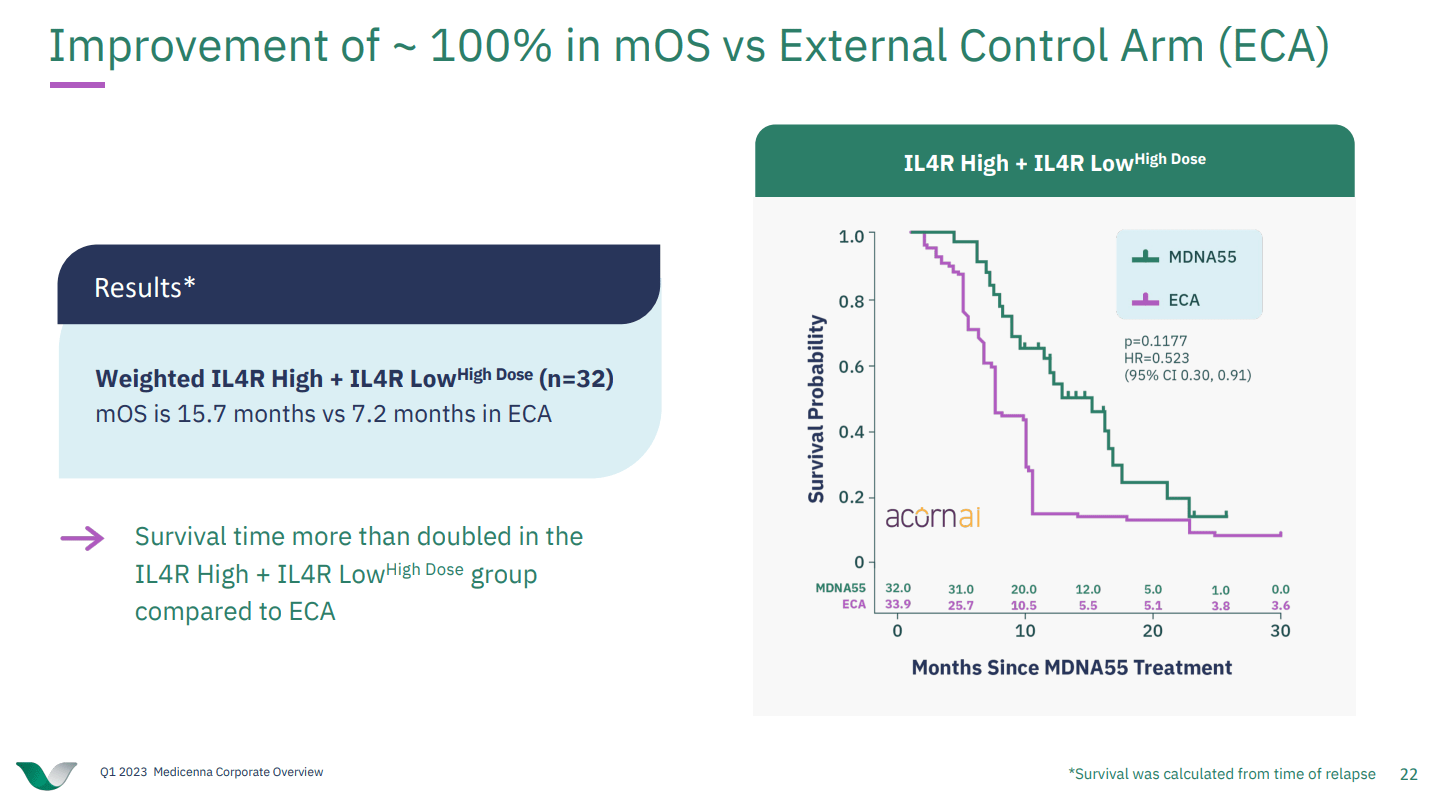

MDNA has also produced data with MDNA55, and IL-4 superkine, in recurrent glioblastoma multiforme but is waiting for a partner to progress that drug. I don't know if MDNA will be able to find that partner quickly, or if the company might end up having to raise cash one day should it want to run a phase 3 trial on that drug itself. Right now the company notes that the existing efficacy data looks good compared to an external control arm, but I tend to put only a little weight into external comparisons like that. I have seen examples where companies noted that based on appropriately matched controls from a database, that their drug looks promising, only to go on and fail in phase 3 when the drug was compared to a control arm within the phase 3 study.

Figure 4: Comparison of the MDNA55 data to that of an external control arm calculated using Acorn AI. (MDNA Corporate Presentation Q1 2023.)

{kind=link}

An example that comes to mind from the glioblastoma space is Celldex Therapeutics' ( CLDX ) rindopepimut. A March 2016 press release from the company announced that the Data Safety and Monitoring Board had recommended discontinuation of CLDX's ACT IV study of rindopepimut in newly diagnosed glioblastoma as the drug arm and the control arm were performing on par with each other. This was despite results from the ACTIVATE, ACT II and ACT III studies, which ACT IV had a very similar patient population to, apparently looking promising when compared to matched historical controls. Indeed there was also a controlled phase 2 study of rindopepimut in recurrent glioblastoma, that had produced some promising data. Nonetheless, newly diagnosed glioblastoma was the indication in the larger phase 3 study and the comparison of the phase 2 data to historical controls looked good, but didn't pan out in phase 3.

Figure 5: Pooled data from ACTIVATE, ACT-II and ACT-III trials of rindopepimut in newly diagnosed glioblastoma. (Celldex Presentation slide from SmithOnStocks article, December 2013.)

One enticing factor for a potential collaborator might be the fact that the FDA was supportive of an innovative study of MDNA55 using a hybrid control arm (two-thirds matched external controls, one-third randomized patients). Patients might be more likely to enroll in a design where the odds of being randomized to the control arm (where you would only receive standard of care and not MDNA55 as well) are reduced. A hybrid design does exactly that, if you enroll 133 patients, and 100 get the drug, whereas 33 go into the control arm (the remaining 67 control patients coming from external matched controls) then you have a three out of four (75%) chance of getting the drug. As such MDNA might find a collaborator likes the idea of a trial that would be smaller than a regular phase 3 study, and potentially enrolls faster too due to patient demand.

Outside of MDNA55 and MDNA11, MDNA has preclinical programs such as the Bifunctional Superkines for immunotherapy (BiSKIT) program, but the program hasn't entered the clinic as of yet, so isn't currently a big part of the near-term story for MDNA.

Financial Overview

At December 31, 2022, MDNA had cash and cash equivalents of $36.2M CAD (about $26.7M USD at the time of writing), which the company expects to last until Q2'24. This certainly seems feasible with R&D expenses thus far of $2.9M CAD and G&A of $2M CAD for the quarter ending December 31, 2022. With 69,637,469 shares outstanding as of February 7, 2023, MDNA has a market cap of approximately $42.5M USD ($0.61 per share on the Nasdaq).

MD&A for the three and nine months ended December 31, 2022, filed as part of a 6-K, February 7, 2023.

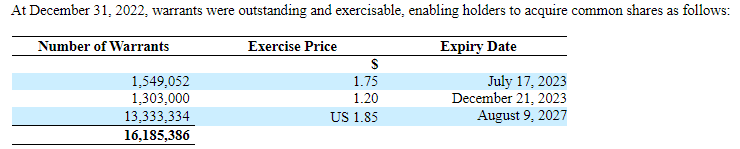

Considering the outstanding warrants and stock options, we see that about 2.85M of these warrants will expire in 2023, but the majority don't expire until 2027. A fully diluted market cap including all of these warrants and stock options is $55.9M USD.

MDNA's Interim condensed consolidated financial statements for the three and nine months ending December 31, 2022.

{kind=link}

MDNA is trading at about 1.6 times cash, in a biotech market where many names trade below cash or at cash. One such example is Werewolf Therapeutics ( HOWL ) which Bret Jensen's Busted IPO Forum recently wrote about . HOWL is also developing an improved form of IL-2, designed to be activated within tumors to avoid peripheral side effects, although it isn't targeted to non-alpha containing IL-2 receptors, so has its differences to MDNA11. HOWL currently has a market cap of $90M with cash of $140M an debt of $15M, meaning the name has an enterprise value of -$35M. Apparently HOWL's pipeline essentially represents a sinkhole rather a treasure trove, at least the market seems to think. I actually like HOWL, but the point is that the market seems a little bit more excited about MDNA's pipeline than HOWL's.

Conclusions

There are some signs of efficacy so far with MDNA11, and with the company now dosing a sixth cohort, patients will be receiving twice the dose (120 ?g/kg vs 60 ?g/kg) from what we've seen previously. With the 90 ?g/kg dose having no toxicity issues to date as of the February 7 press release, even if the 90 ?g/kg dose ends up being used for expansion, the possibility exists of some more tumor responses to stimulate the market's interest in MDNA11. I think that the market is already aware that MDNA might have something with MDNA11 given that I can find peers trading at or below cash in this tough biotech market. Further with multiple readouts with MDNA11 on tap in 2023, there are plenty of opportunities for MDNA to garner further attention and perhaps run up into some of these readouts. I consider MDNA a strong buy given the prospect for a run up into catalysts, especially in Q3'23 and Q4'23.

The risks of any long in MDNA are several fold, a few of which I'll discuss here. Firstly, the company could report adverse events with MDNA11 which create concerns over how high the drug could be dosed, thus limiting its potential efficacy. Secondly, any delays in reporting data from ABILITY could lead to investors or traders moving on to other companies in the IL-2 space that are ahead, leading the stock to sell off. Lastly, MDNA might produce efficacy data from the ABILITY trial that underwhelms relative to competitors offerings, or even without regard to competitors drugs. Disappointing results in the IL-2 space have been seen previously, such as with Nektar Therapeutics ( NKTR ) bempegaldesleukin.

For further details see:

Medicenna: Multiple Catalysts Ahead In 2023