ACRDF - Medicine Man Technologies: Why I Am Buying This Stock

Summary

- Medicine Man Technologies is currently trading at an extremely low valuation and has the potential for a 200% appreciation compared to its peers.

- The company is in an optimal position to benefit from the fast-growing cannabis industry.

- Despite the challenging conditions of the economy and industry, Medicine Man is continuously deleveraging its balance sheet and expanding its margins.

- The seasoned management team continues to expand the company's profit margins while benefiting from strategic acquisitions.

Editor's note: Seeking Alpha is proud to welcome Adrian Nunez as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Summary

Medicine Man Technologies (SHWZ) - which I would give the nickname Med-Man - is an undervalued company in the cannabis industry, trading at an EV/Sales of 1.2x, EV/EBITDA of 6.4x, and P/E of 3.4x. The low EV/Sales, EV/EBITDA, and P/E indicate an attractive valuation compared to its peers, making Med-Man an excellent investment opportunity. The cannabis industry has suffered from strict FDA regulations leading to valuations and stock prices falling, but Med-Man's low valuation comes from significant financial performance in recent years. With a talented and experienced management team, the company's revenue grew at a 171.6% CAGR from 2015 to 2022, and they generated $105 million in cash in 2021.

Med-Man's growth strategy focuses on its retail, market share, and brand development. With 25 stores outperforming the core market by 12% in revenue, the company is poised for future growth. The cannabis industry has an expected total addressable market ((TAM)) of $28 billion this year, growing to $46 billion by 2026 and $100 billion by 2030, providing ample opportunities for Med-Man to increase sales and profitability. As the demand for cannabis products continues to grow, Med-Man's sales and profitability will expand, leading to higher margin expansion thereby attracting more investors.

In brief, Med-Man is an undervalued company in a seemingly recession-resilient industry, poised for future growth, with a talented management team, strong financial performance, and a differentiated growth strategy. I believe the company's low valuation makes it an attractive investment opportunity, and its potential for growth in the cannabis industry makes it a valuable asset for any investor looking for long-term returns.

Quick Company Overview

Med-Man operates in the cannabis business. It provides consulting and technology to help cannabis businesses grow and succeed. The company does this through regulatory compliance, cultivation and dispensary management, and tech solutions.

In brief, a cannabis business goes to a firm like Med-Man to get help with running its business. Med-Man then makes money from charging its clients a fee (depending on the type and scope of the services). The company aims to help cannabis businesses increase profitability and growth while keeping everything safe and legal.

My Investment Approach

I look for undervalued companies with significant potential for the coming years. With that, I also love riskier investments as they provide greater rewards in the long term. Therefore, I aim to hold an investment for anywhere from 3-10 years. There are five main points I look at when analyzing a healthcare company and Med-Man ticks all the boxes I outline below, hence I am bullish on the name.

1) Undervalued

The first thing I ask myself when looking at a healthcare company is: are they cheap? Med-Man company is trading at a total EV of $179 million, LTM sales of $146 million, EBITDA of $28 million, Net income of $21 million, and a market cap of $70.6 million. This means their EV/Sales is 1.2x, EV/EBITDA is 6.4x, and P/E is 3.4x. This, to me, screams undervalued/cheap.

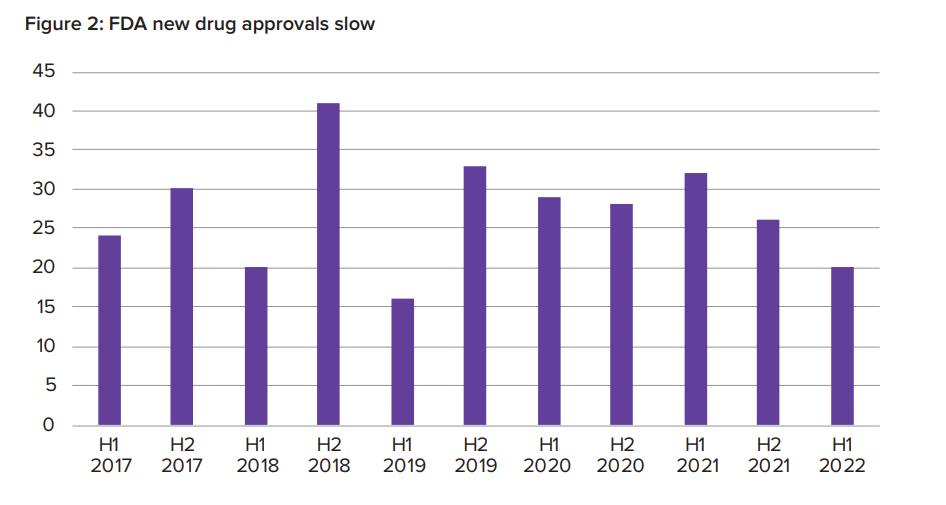

Why is it so cheap? Well, the whole cannabis industry has dropped well over 50% because current legal conditions in the industry have been worse than investors have seen. For example, on January 26 this year, the FDA gave a negative sentiment on CBD , which led to a significant drop in the prices of Cannabis stocks. The FDA has also become stricter over time, and new approvals have slowed significantly. The number of new drug approvals by the FDA was at nearly 60 in 2020 and 49 in 2021, and this number reduced further to 39 in 2022. You can read the whole report here .

{kind=link}

These factors have led the cannabis industry to drop, and valuations drop when stock prices drop. When valuations and stock prices fall, this means stocks trade at a discount. However, this does not imply all cannabis stocks are cheap; in fact, most cannabis stocks still lack an attractive valuation. Med-Man has an attractive valuation because of its low EV/Sales, EV/EBITDA, and P/E (and any other valuation multiple). A quick rule of thumb to identify a good EV/EBITDA or P/E is anything below 10. This rule depends on the industry but is always a good measure to determine if a company has an attractive valuation. With SHWZ trading at a 3.2x P/E, this means that their stock price is only 3.2 times higher than the earnings they generated in the last twelve months.

In essence, all cannabis stocks have suffered from the strict FDA, and their valuations have dropped. Companies that have a lower valuation are those that have shown significant financial performance in the past years. This said, not all companies that have fallen have an attractive valuation, but SHWZ has an attractive valuation in comparison to its peers.

I have compared Med-Man's valuation to that of its peers (see below) and further explained why the company is trading at an attractive valuation. I've also dived into the cannabis industry and explained why, I believe, things are looking brighter for the sector in the coming years.

2) Management Team

The second thing that I look at when investing in a healthcare company is the management team. Med-Man’s leadership team is well-seasoned and has a track record in competitive low-margin sectors. Looking at their team, they all seem to have over 20 years of industry experience and have all taken part in very successful projects. This is a very talented management team, and I am thrilled to see where they can continue to take this company in the coming years.

3) Financial Performance and Profitability

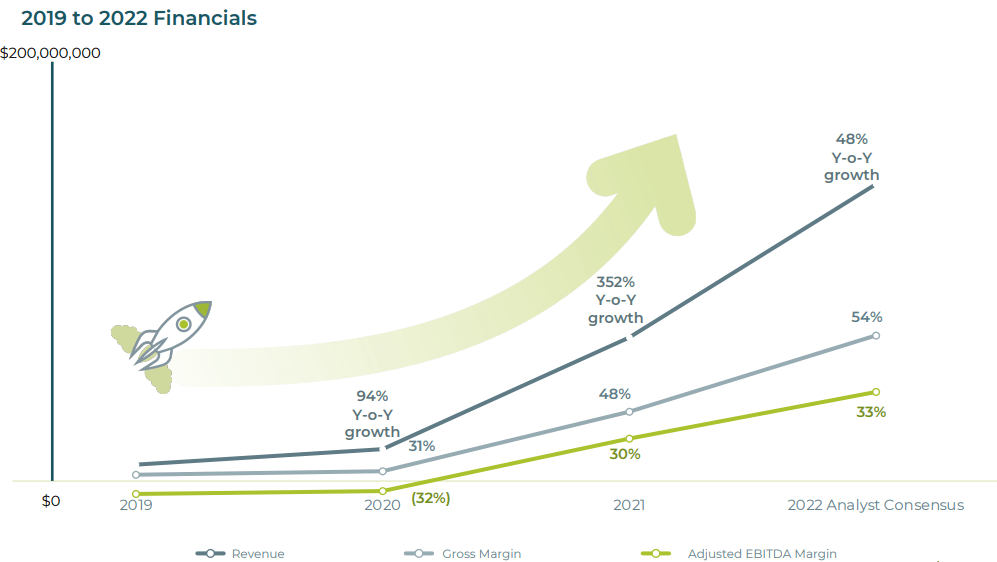

The next thing I'd analyze is financial performance. Is the company consistently growing revenue and generating cash flow? From 2015 to 2022, Med-Man’s revenue grew at a 171.6% CAGR; In 2020, they had $24 million in sales; in 2021, they accounted for $108 million in sales; and in the LTM, they accounted for another significant increase with $146 million in sales. Med-Man’s cash flows in 2019 were at $13 million; in 2020, they lost $12 million in cash; in 2021, they generated $105 million in cash; and they have $18 million in the last 12 months. This company is growing at a radical pace which is leading to significant margin expansion. As it continues to grow its sales and profitability, I think the company will be able to keep re-investing, all of which is a great sign that will attract investors.

{kind=link}

4) Industry Outlook

So, what is the state of the cannabis industry? The Cannabis Industry is recession resilient, which is an important thing to note as we head into a period of slower economic growth.

Additionally, there are 20 US states where Cannabis is legal recreationally, and 45% of the U.S. population lives in these states. The numbers have grown significantly in the past, and they still have a long way to go. I believe this is an excellent sign for the industry and for this company.

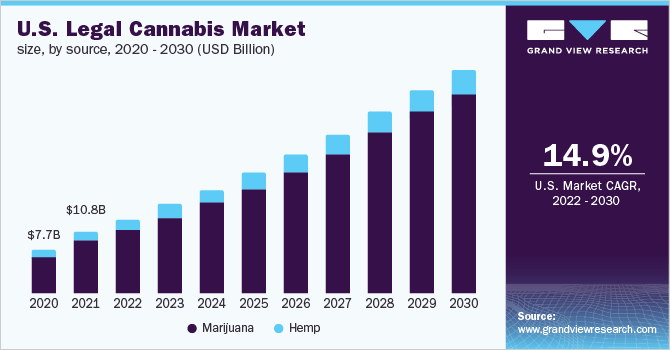

According to a report from Grand View Research , U.S. legal cannabis TAM is expected to be $28 billion this year and growing to $46 billion by 2026 (expanding at a 13% CAGR). Total U.S. Cannabis TAM is expected to reach $100 billion in 2030.

{kind=link}

In other words, the demand for cannabis products is expected to continue to grow, providing opportunities for Med-Man to increase its sales and profitability, thus leading to higher margin expansion which will continue to attract investors.

5) Growth Strategy

The last important factor that I ask is whether the company has a differentiated strategy and how have they applied it? Med-Man focuses on its retail, market share, and brand development. They have 25 stores outperforming the core market by 12% in revenue in the latest quarter and the past seven quarters, with 16 stores in New Mexico and the rest in Colorado. According to BDSA, Legal Cannabis Markets in New Mexico are estimated to grow nearly 200% by 2026. I never said this is a great company, but it sure is a good business with great ambitions and has much potential to benefit from the growing cannabis industry.

Med-Man - Inorganic Growth

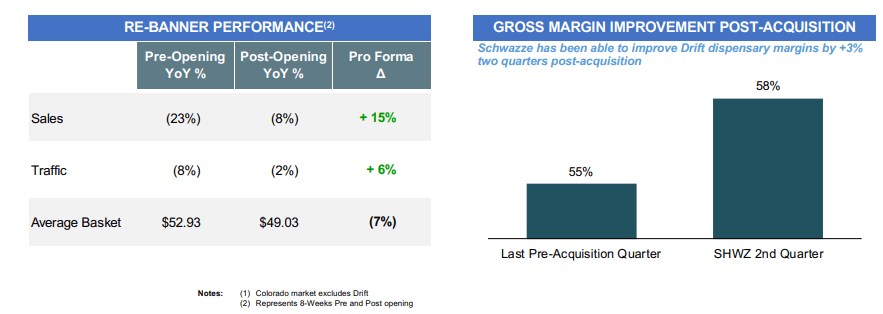

M&A is an optional consideration when looking to invest in a company. Med-Man has had significant growth due to its two acquisitions, supporting this business and my investment thesis. In December 2021, it acquired Smoking Gun and its assets in Denver:

{kind=link}

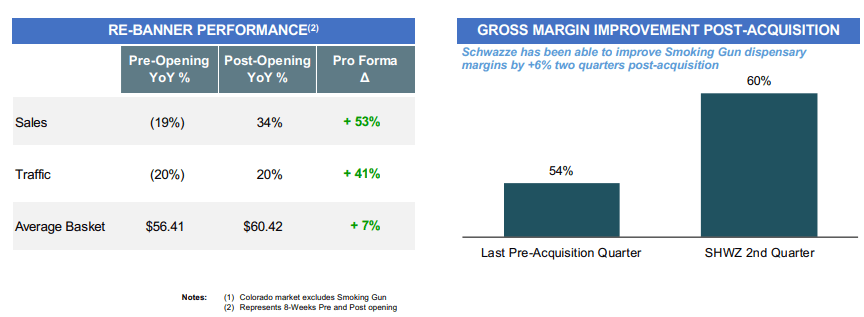

In just one quarter, they grew Smoking Gun into a significantly profitable business (they were not profitable before). This led the gross margin to increase by 6% QoQ. This is a testament that this company has a strong management team and has meaningful ambitions.

In January 2022, the company acquired Drift , consisting of two Cannabis dispensaries located in Boulder County, Colorado.

{kind=link}

Source: SHWZ Corporate Presentation

Here we can see another successful acquisition that Med-Man performed while still digesting the acquisition they made the month prior. Although this one was not as impactful as the last one, the fact that we are seeing a 3% margin expansion and a 15% sales increase QoQ still proves the company's potential as they continue to acquire new assets.

Another thing to note is that the bearish market has led to extremely low valuations, and many companies are trading significantly lower than they were one year ago. I believe this company will take advantage of the current state of the economy and, thus, continue to perform strategic acquisitions, which will dramatically benefit their business. Of course, this is my opinion and what I would do if I put myself in the shoes of their management team. Nonetheless, I think this company will continue to benefit from its current acquisitions, and we will likely see new investments in the coming years.

Peer Comparison: Med-Man A Rising Industry Leader Trading at a Discount

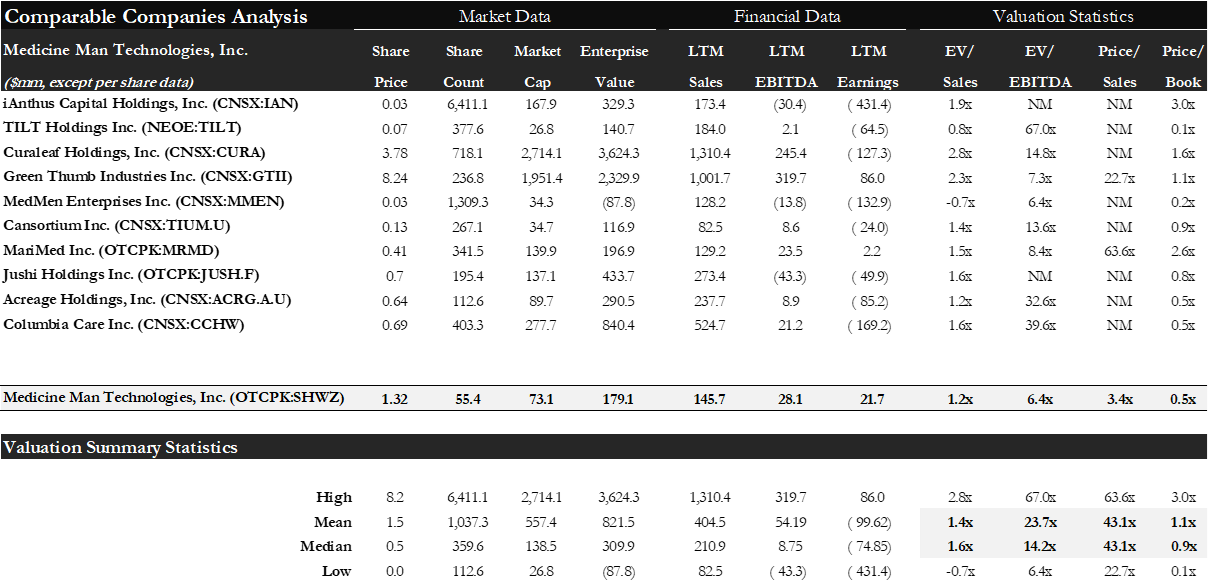

As mentioned above, Med-Man is highly undervalued in comparison to its peers. When a company is undervalued, it does not guarantee it will see a share price appreciation. It only means that the company has a significant potential for appreciation. In terms of Med-Man's potential, I chose the following companies for comparison: iAnthus Capital Holdings (ITHUF); TILT Holdings ( TLLTF ); Curaleaf Holdings (CURLF); Green Thumb Industries (GTBIF); MedMen Enterprises (MMNFF); Cansortium Inc. (CNTMF) (TIUM.U); MariMed Inc. ( MRMD ); Jushi Holdings (JUSHF) (JUSH.F); Acreage Holdings ( ACRHF ); and Columbia Care Inc. (CCHWF):

Comparable Companies Analysis (Author's Data)

{kind=link}

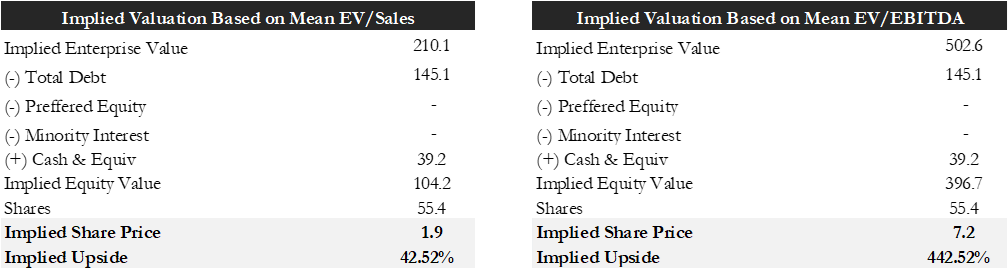

I made this comps analysis to paint a picture as to why I think SHWZ is undervalued. Then, to find the appropriate appreciation potential, I calculated SHWZ’s implied share price based on the mean or average EV/EBITDA and EV/Sales:

{kind=link}

With SHWZ trading at $1.32 per share, they have an average appreciation potential of 242.52% or a $4.5 share price. EV/EBITDA is arguably one of the most attractive valuation multiples when it comes to evaluating a company, and the fact that SHWZ has a 442.52% appreciation potential based on EV/EBITDA is extremely attractive.

Another very attractive multiple to consider would be the P/E. Using the mean P/E from the comps of 43.1x, SHWZ's share price implies an 1,180% upside appreciation potential. However, the mean P/E is exceptionally high because many of these companies are still small and new, so I do not think this is an accurate measurement. We could also compare the P/B where SHWZ is trading at (0.5x) and the mean for its peers (1.1x). But the point is that this company has a significant appreciation potential, and that also suggests that the stock is cheap. All of these I think dramatically reduce the risks of buying this company at today's prices. Regardless of the multiple that you use, there is one thing they all suggest: SHWZ is extremely undervalued.

As the cannabis industry continues to grow at a faster pace and Med-Man continues to make a name for itself in this industry, I believe investors will catch on to the company's low valuation; and that this stock will be valued at a much higher price with at least a 1.0x P/B. Nonetheless, I am extremely excited to see where the market values this undervalued and rapidly growing company in the coming years.

Downside Risks

It is essential to keep in mind that this is not a comprehensive compilation of all the potential risks that Med-Man faces. In general, Med-Man's most significant risk lies in its own industry. This is due to the strict FDA, as explained above. Every time the FDA announces a negative sentiment on the cannabis industry, this leads companies such as Med-Man to drop well over 5% in one trading day.

Dependence on the Cannabis Industry

Med-Man is entirely dependent on the cannabis industry, which is still in its early stages of development. If the industry does not grow as projected, the company’s share price will be harmed.

Limited Geographic Reach

The company primarily operates in the United States and has limited international exposure, which limits its potential for growth in other countries. This is not too big of a problem now, but this company has a limited growth capability when looking at a long-term investment.

Upside Risks

Expansion into New Markets

Med-Man has yet to announce this, but the company has the potential to leverage its expertise in consulting and technology solutions to expand into other industries and diversify its revenue streams.

Positive Sentiment From FDA

The legalization of cannabis in other countries could allow Med-Man to broaden its reach and offer its services in new markets. Just like the downside risks, if the FDA announces a positive sentiment on the cannabis industry, companies such as Med-Man will enjoy a nice high in one trading day.

My Final Thoughts

Med-Man has demonstrated attractive characteristics for an investment opportunity. With an undervalued stock price, an industry-leading management team, consistent growth in revenue and profitability, a well-positioned growth strategy in the growing cannabis industry, and successful inorganic growth through strategic acquisitions, the company presents a compelling investment opportunity.

It is also worth noting that the bearish market and strict FDA have led to low valuations, providing opportunities for Med-Man to continue performing strategic acquisitions to further benefit its business. It is important to keep in mind that investing in the cannabis industry can be riskier than other industries. Still, the growth potential and the company's strong fundamentals make it a worthwhile consideration for a long-term investment.

Overall, SHWZ is an attractive investment opportunity for those seeking undervalued companies with significant potential for growth. I am eager to see where this company will be valued in the next 3-5 years and where the state of the overall industry will be.

For further details see:

Medicine Man Technologies: Why I Am Buying This Stock