MED - Medifast: A Low Earnings Multiple Despite Strong Financial Performance

Summary

- Medifast has consistently grown its EPS by 20% annually for the past 20 years, has more cash than debt, and is a well-established health and wellness firm.

- The low earnings multiple assigned by the market is not justifiable in my opinion.

- Q3 2022 earnings were lower than expected, but the management attributes it to macroeconomic factors and sees improvement in customer retention. Still targeting double-digit growth going forward.

Introduction

Despite consistently growing its EPS by 20% annually over the past 20 years and maintaining a solid financial position with more cash on hand than total debt outstanding, the market still assigns Medifast (MED) a close to all-time low earnings multiple.

Known for its scientifically crafted meal plans and nutritional supplements, Medifast is a reputable health and wellness firm that supports customers' efforts to lose weight and improve their general health. For many years, Medifast has been assisting people in achieving their health goals with a dedication to quality and a staff of qualified experts. Protein bars, drinks, dinners, and snacks are just a few of the company's offerings.

In my opinion, the low valuation is not justifiable and will eventually rectify given time. Meanwhile, investors can reap the benefits of a highly attractive dividend yield of 5.89%. Share buybacks are currently also being done, further increasing intrinsic growth.

Q3 2022 Earnings

In contrast to the earlier expectation of $1.58 billion to $1.66 billion, the company has reduced its full-year 2022 revenue projection to fall between $1.51 billion and $1.59 billion. The anticipated non-GAAP diluted EPS for 2022 has also been reduced, from the previous range of $12.70 to $14.10 to a range of $11.61 to $13.05. The management attributes this change in outlook to the adverse effects of inflation and macroeconomic volatility on the acquisition of new customers.

The current low valuation of Medifast may be somewhat reasonable in the short term, as evidenced by the latest earnings release. The results showed that net income and revenue fell just short of expectations. Due to decreasing coach productivity, revenue for the third quarter of 2022 fell by 5.6% to $390.4 million. In the third quarter of the previous year, the average revenue per active earning OPTAVIA Coach was $6,773, while it was $5,897 in the current quarter.

Despite revenue forecasts not being met, signs of recovery are showing. Dan Chard, the Chairman and Chief Executive Officer, shared the following insights:

We've seen faster than anticipated improvement in customer retention rates back to quarterly historical norms, as we focus on delivering a high quality experience for all customers,"

Fundamentals

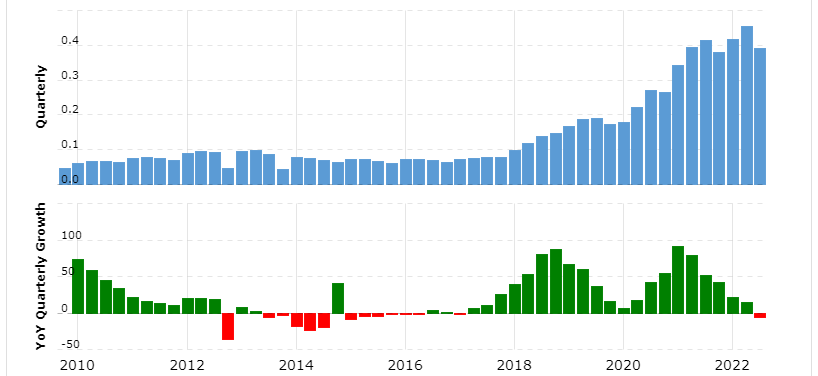

Under the leadership of CEO Daniel R. Chard, who joined the company in 2016, the firm experienced a rapid surge in revenue. OPTAVIA, the weight loss program , became the center of attention and its double-digit annual growth in revenue and profit was a testament to this focus. The number of coaches and their average earnings per coach also saw consistent yearly increases.

However, the company's growth has recently hit a snag due to a drop in consumer spending. Despite this setback, the management remains optimistic and aims for an average revenue growth rate of 15% per year.

{kind=link}

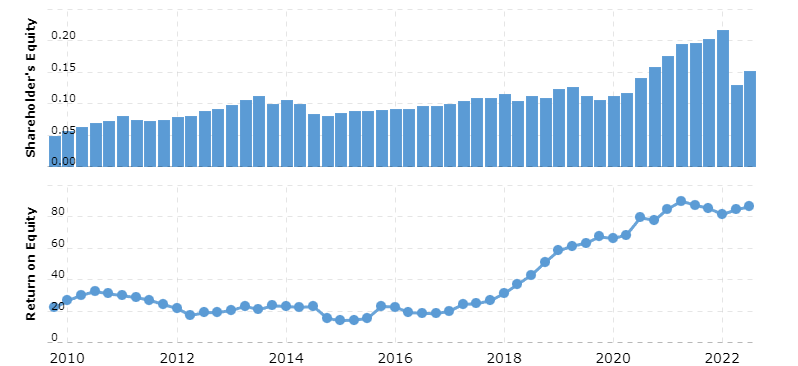

As seen in the figure below, the return on equity has significantly increased since the new CEO was hired in 2016. The strength of OPTAVIA is highlighted by the declining correlation between the required equity and earned profits.

Profits are being used on dividend payments and share buybacks rather than allocating cash to build equity. Sustaining the same return on profits while continuously growing equity is likely unrealistic, hence the generous dividend payout ratio of ~50%.

{kind=link}

Even if the company were to completely halt equity growth and thus net income growth as well, the current low valuation still provides a substantial margin of safety. The company distributes 50% of its earnings as dividends, while the remainder could be used for share buybacks.

At the current low valuation, share buybacks would generate an estimated annual return of ~5.8%. Coupled with the dividend, a conservative annual total return of 11.7% could be expected. On the other hand, if the company decides to continue building equity, a higher total return could be expected, as the company's historical ROE has consistently exceeded the returns that buybacks are offering at current valuations.

Stock Chart

Quick disclaimer: A technical analysis in itself is not a good enough reason to buy a stock, but combined with the company's fundamentals, it can greatly narrow your price target range when you buy.

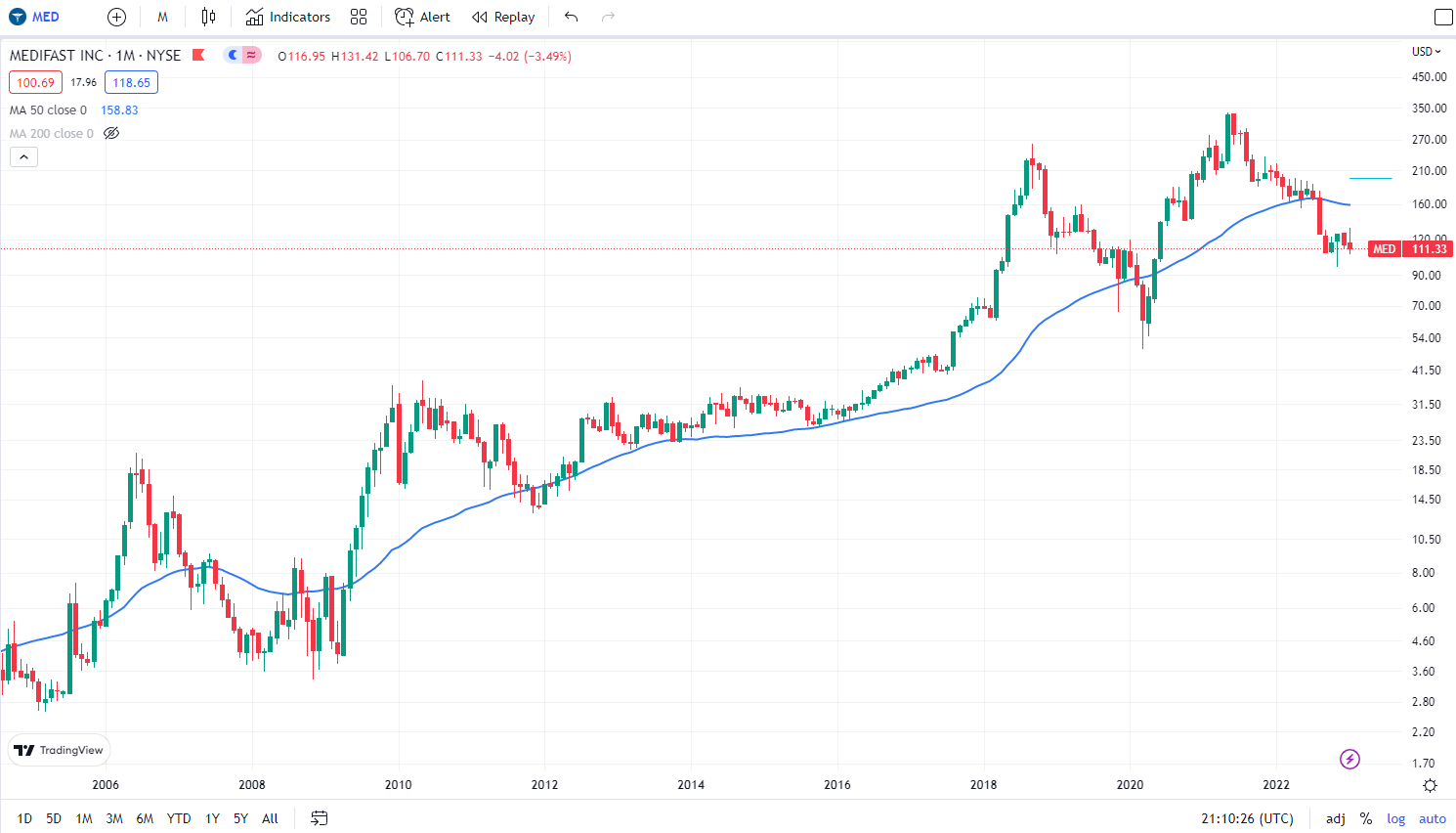

The 50-month moving average has been a dependable way of finding potential support levels for companies that have a history of steady growth, including Medifast. Historically, whenever the stock has fallen below this average, it has been significantly undervalued based on its earnings. With an impressive balance sheet, a profitable outlook, and an expectation of EPS growth fueled by share buybacks, there's no reason to believe this time will be any different.

Medifast's stock price has been known to oscillate from being overvalued to undervalued and vice versa. However, the company seems to be aware of this trend, as evidenced by its repurchasing of shares and insider buying activity .

A rise back to a level slightly above the moving average would place the stock around $185 per share.

{kind=link}

Valuation

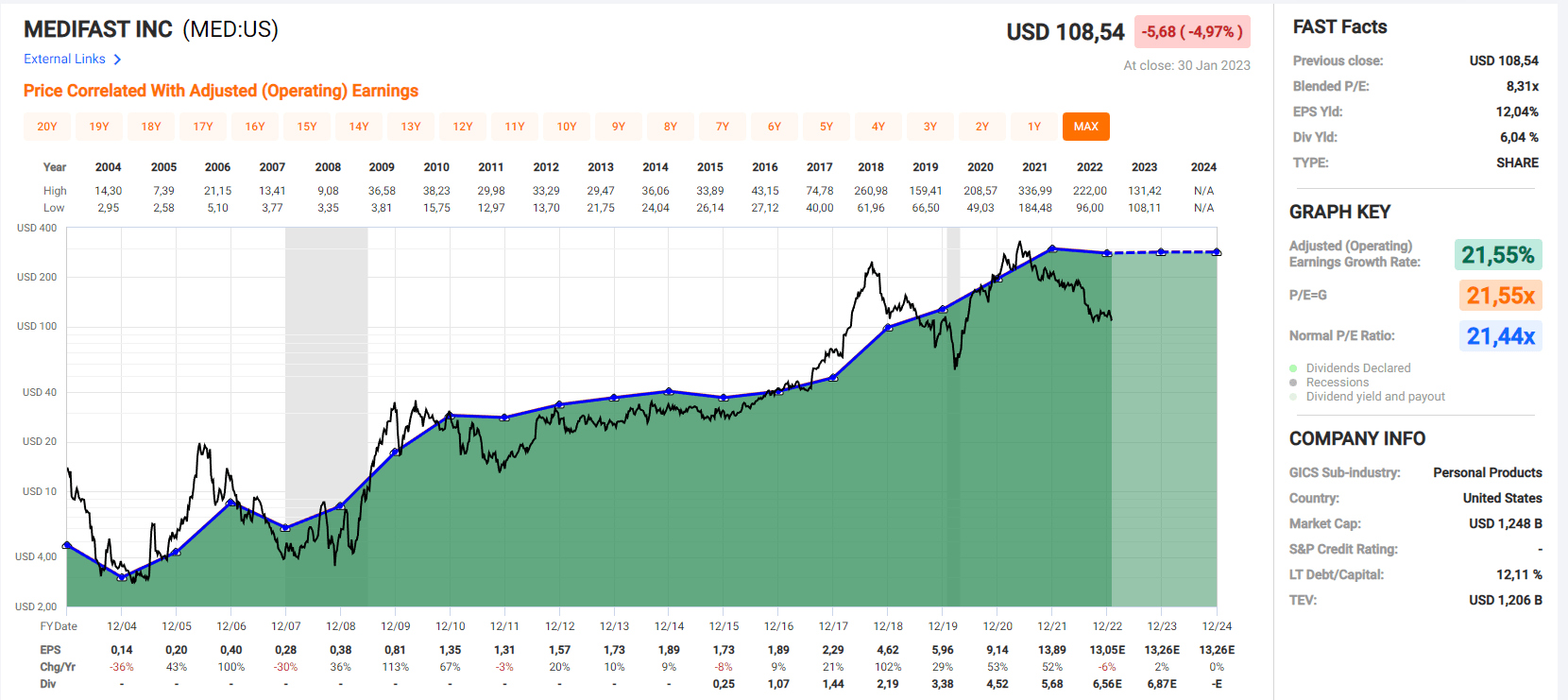

The past two decades have witnessed growth far above the average , as depicted in the picture below. It is not surprising that the average earnings multiple has been higher than the standard multiple of 15 however, its current multiple does seem too low.

Medifast has maintained an impressive average annual growth rate of ~22% in EPS since 2003, which was previously reflected in a proper average multiple of ~21.4. However, due to the recent stagnation in growth estimates by analysts, a significant decline in the multiple has occurred.

Medifast's stock is currently assigned a low multiple of 8.31, which is the lowest it has been in 20 years, despite having more cash than debt and actively repurchasing its own shares.

If the earnings multiple were to return to a conservative 15, it would indicate that the stock is undervalued by as much as 75%.

{kind=link}

Final Thoughts

The company has an impressive balance sheet, profitable outlook, and expected EPS growth driven by share buybacks. Despite its growth history and current financial strength, the market currently assigns the company a low multiple of 8.31, the lowest in 20 years.

The stock has oscillated in the past but the company seems aware of this trend through its share buybacks and insider buying. If the earnings multiple returns to a conservative 15, it would indicate the stock is undervalued by up to 75%.

With its combination of share buybacks, dividends, low valuation, and zero net debt, I think Medifast offers a compelling margin of safety, regardless of whether its ROE continues to grow or remains steady.

For further details see:

Medifast: A Low Earnings Multiple Despite Strong Financial Performance