MED - Medifast: Good On Paper But A Slowdown In Sales Is Very Worrisome

2023-11-24 05:46:27 ET

Summary

- Medifast has strong financials with a healthy cash position and no debt, but its sales have plummeted, and its business model is questionable.

- MED's efficiency and profitability metrics are impressive, but its high-priced products may deter customers.

- The decline in sales can be attributed to tough macroeconomic conditions and competition from weight loss drugs, and the future outlook is uncertain.

Investment Thesis

I wanted to take a look at Medifast ( MED ), which has been on my watchlist for many years but only recently attracted my attention due to its low (supposedly) PE ratio. I wanted to dive deeper into the company and its financials to see if I should commit some capital. On paper, the company looks fantastic and healthy, however, the plummet in sales may not be the fluke of one year and the questionable business model keeps me away from investing, therefore, I assign the company a hold rating.

Financials

As of Q3 '23, MED had around $157m in cash and marketable securities against 0 debt. This is a great position to be in. The company is not burdened by annual interest expenses on debt, which allows for flexibility on how the company decides to utilize its cash flow, whether that is through dividend increases (already at 10% yield, so I wouldn't be a fan of that because of tax implications), inorganic growth (looks like it is needed given the revenue slumps), or share buybacks (if the share price is cheap). It is safe to say the company is at no risk of insolvency right now.

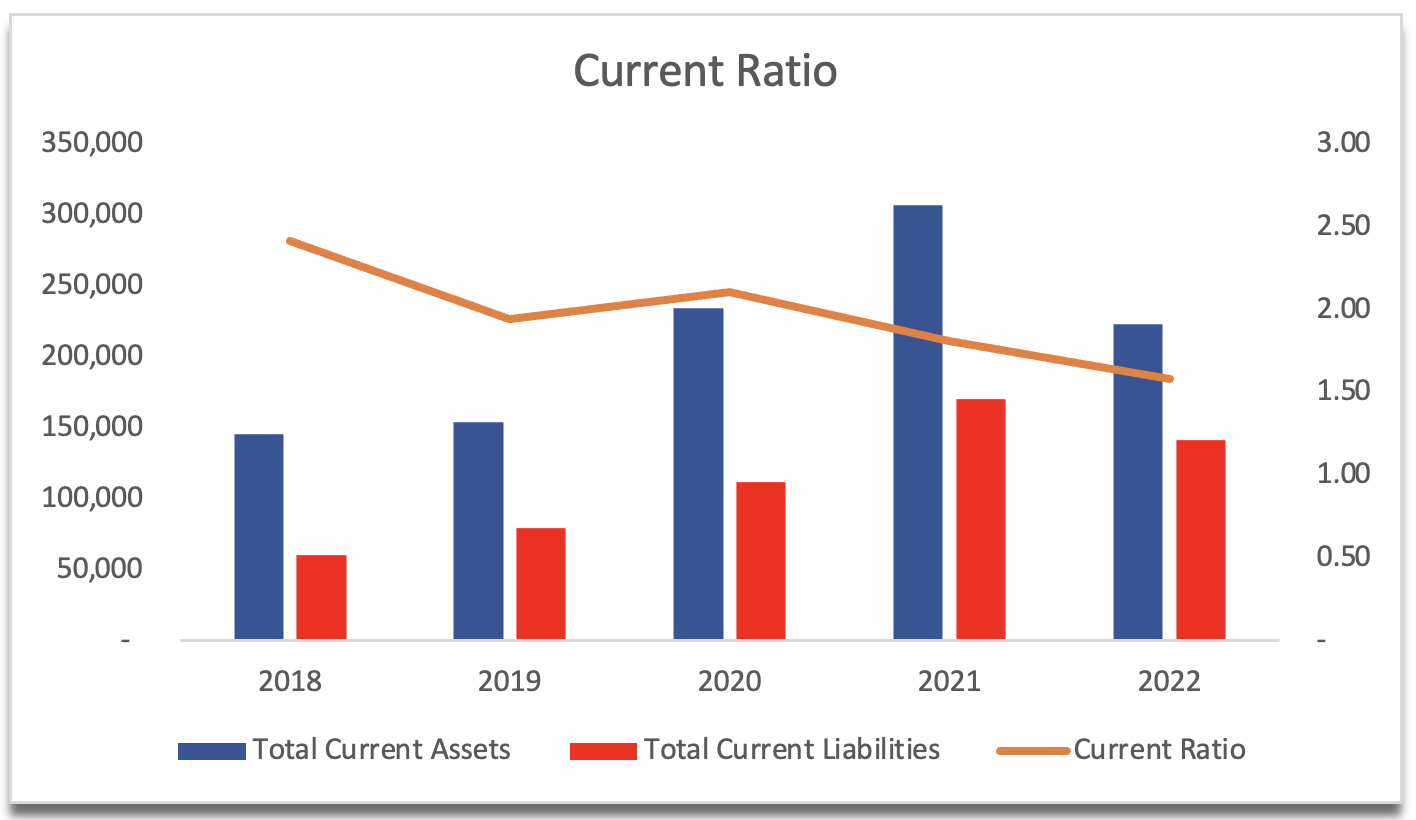

The company's current ratio has been decent over the years; however, it has come down considerably in FY22. As of the latest quarter, it has moved up to around 2, so it is still in that range that I consider to be an efficient current ratio, which is the range of 1.5-2.0. I think that this range is a good balance between having the ability to pay off short-term obligations with ease and still having enough capital for the future growth of the company. So, it is also safe to say that the company has no liquidity issues.

{kind=link}

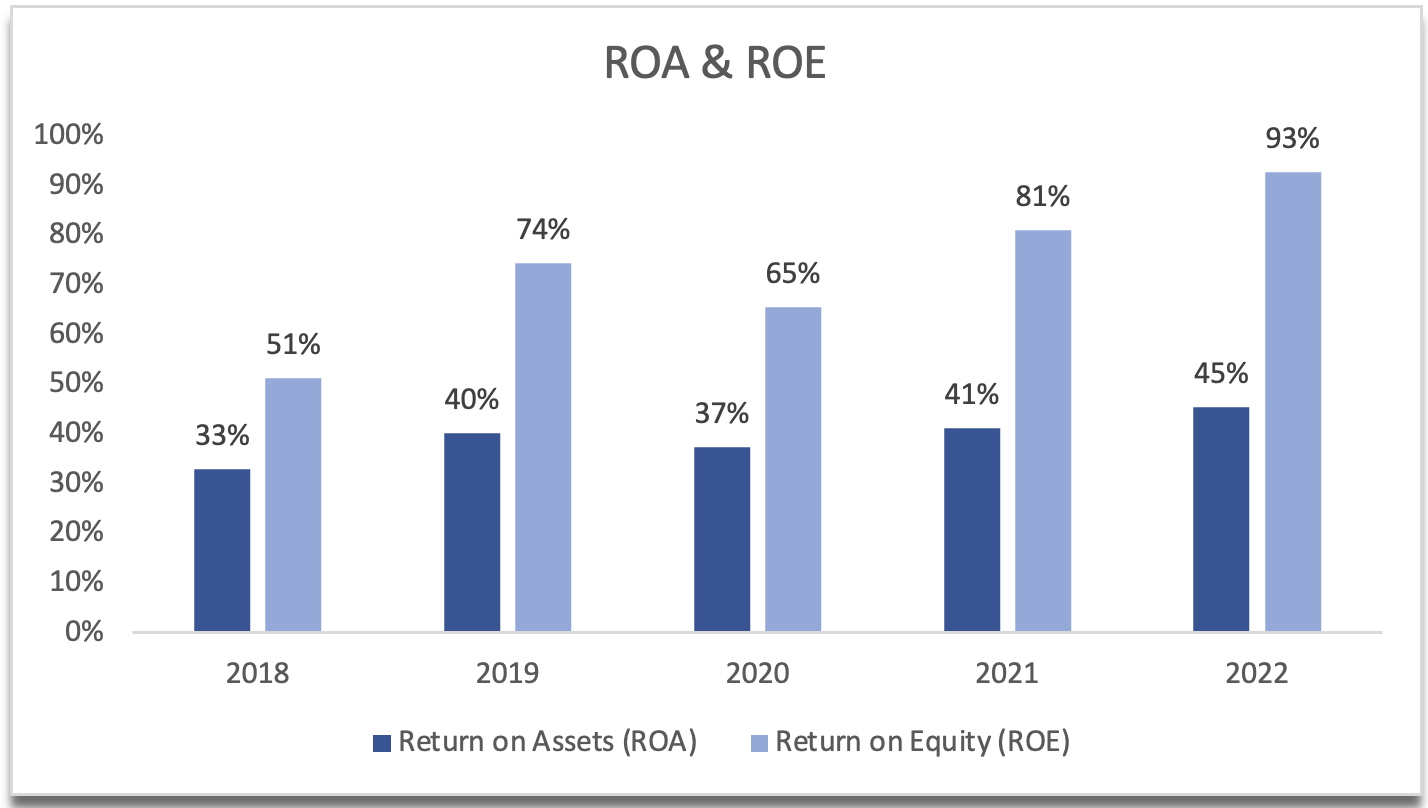

I was blown away by the company's efficiency and profitability metrics. ROA and ROE have been consistently very high. I don't think I have covered a company with such consistently high numbers before (or at least I don't remember). How is the company achieving such efficiency? The company has been enjoying quite decent margins (I will cover later), which contributed massively to the efficiency of the company.

{kind=link}

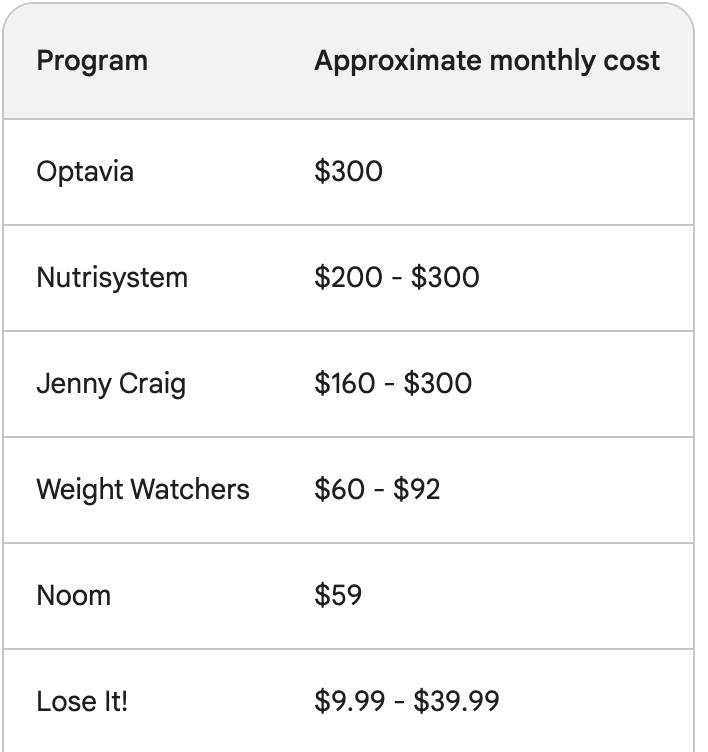

Their products are usually priced higher than other weight loss competitors, so given the popularity of the program, we can see that the company is utilizing its assets and shareholder capital very efficiently. Just a quick Google search of different plans will show that Optavia is at the top range of products available to people.

Price points of competitors (Author)

{kind=link}

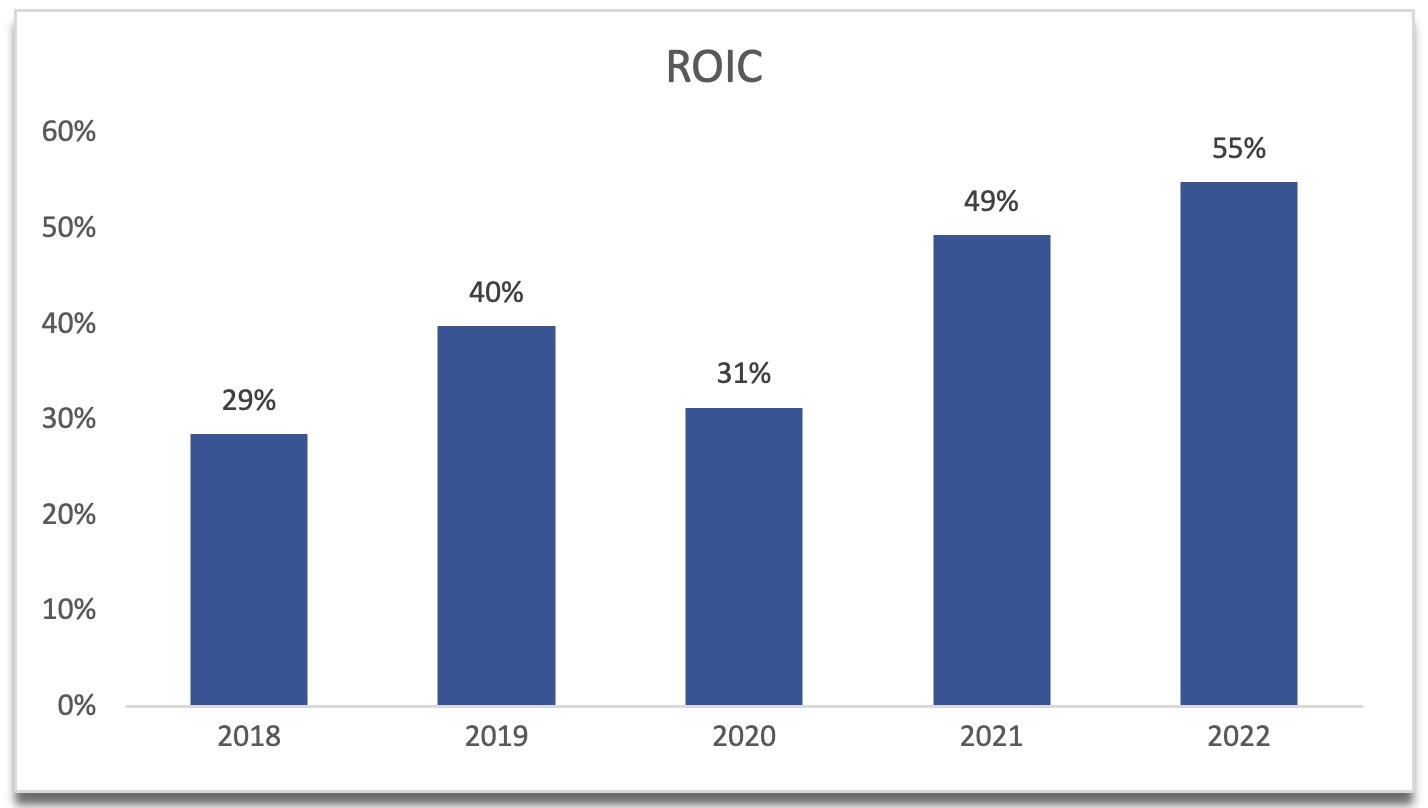

This means the company is enjoying a strong competitive advantage and has a decent moat. This can be seen from the company's ridiculously high ROIC. This tells me that the company can invest capital into very profitable ventures that create significant value.

{kind=link}

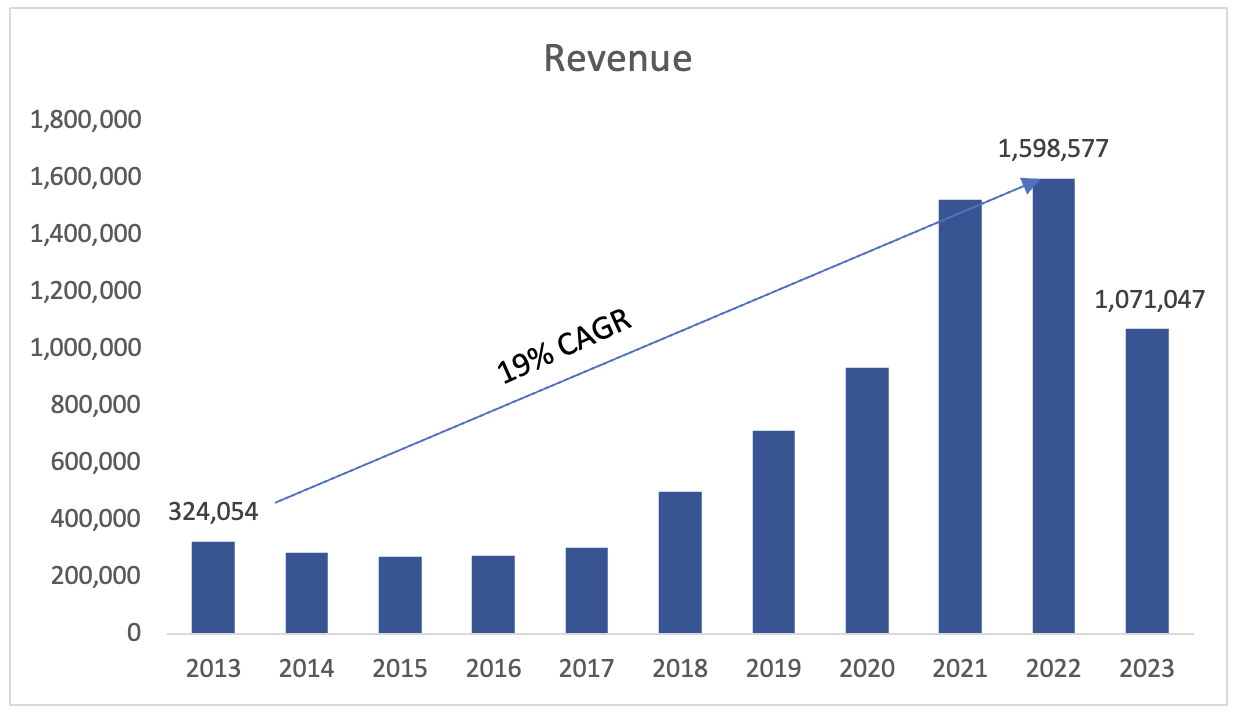

In terms of revenues, the company saw a significant jump around the pandemic time, which I believe will not come back again unless we see another one popping out of nowhere, so people are stuck at home and have nothing to do. This year has not been very easy for the company as it has reported a massive reduction in sales due to the tough macroeconomic conditions and expects to see around a 33% decrease in sales y/y. Up until the disastrous FY23, the company managed to achieve 19% CAGR, but if we factor in the estimate, CAGR goes down to 13%.

Revenue Growth and plummet (Author)

{kind=link}

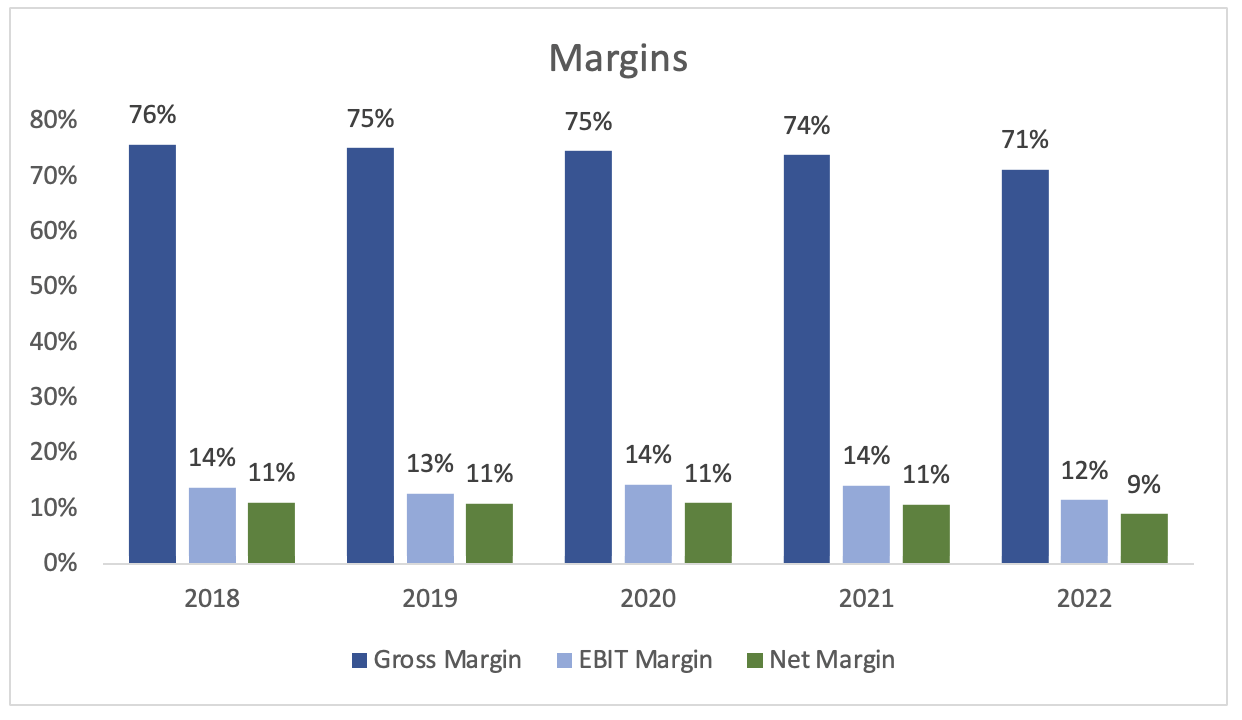

In terms of margins, these have been very consistent and high, especially gross margins. I am a little disappointed that the company isn't able to grow operating and net margins at all.

{kind=link}

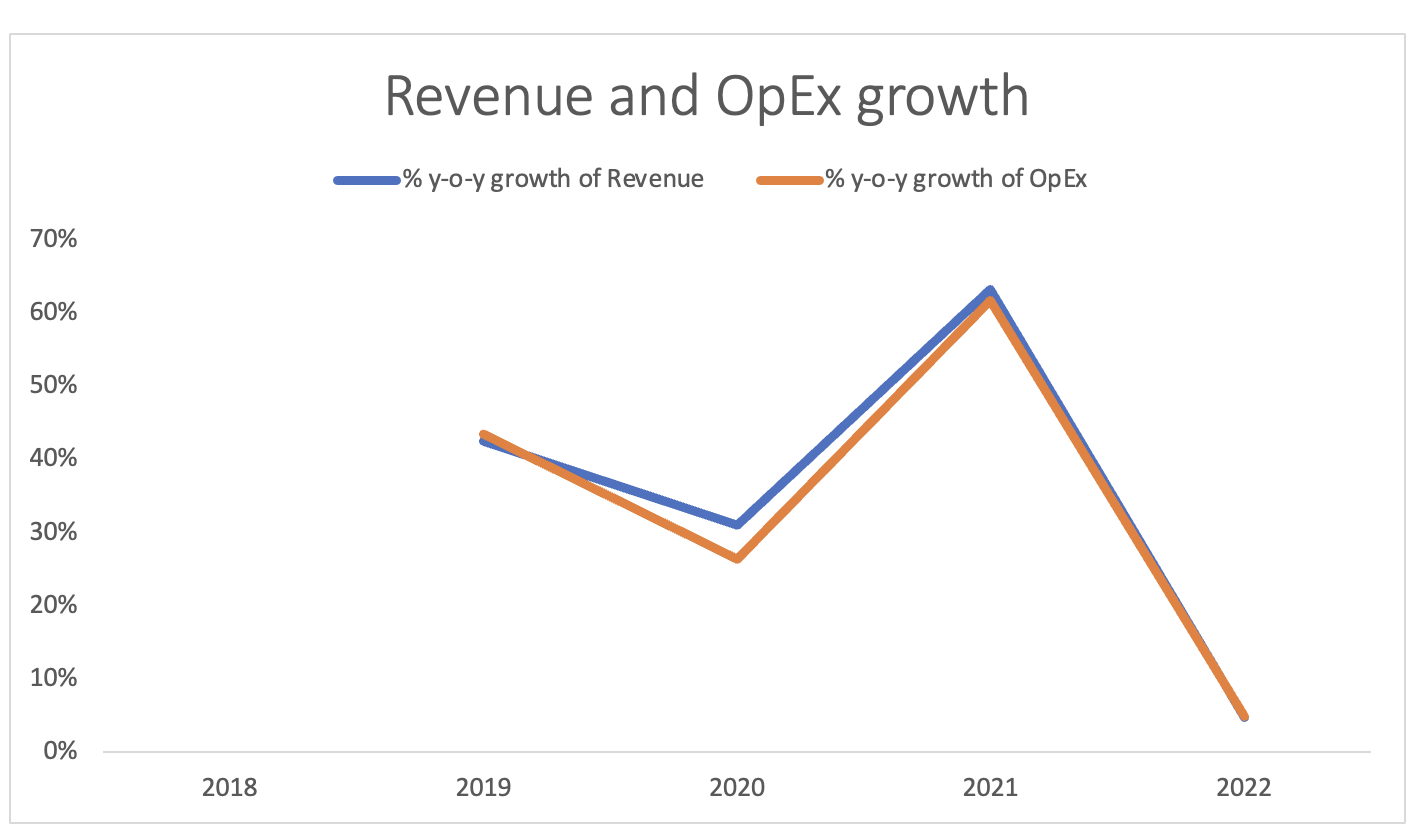

A scalable business can increase its top line considerably and profits, which the company has not been able to achieve in the last 5 years. It may not be a very scalable business if the company cannot manage to keep the costs lower than the increase in revenues.

OpEx growth keeping up with Revenue growth, which may mean the company is not as efficient and scalable (Author)

{kind=link}

So, it looks like the company has been doing significantly well over the last few years, however, if we take into consideration the massive drop off in sales for FY23, I would expect the efficiency and profitability metrics above to follow suit, so, I wouldn't base my assumptions on historical performance as it is not as easy anymore because we don't know whether the sales numbers will recover and FY23 is just a fluke because of the tough macroeconomic conditions.

Comments on the Outlook

I mentioned a couple of times that the macroeconomic conditions have not been particularly easy for MED. High interest rates and sticky inflation have killed the demand for the company's products and services as we can see in the guidance numbers of around 33% decline. That is a serious number. Is it a one-time freak accident and the company will recover? It is hard to tell because of the recent past. The company saw an explosion post-pandemic era. People were out of shape and stuck in their homes so now that they were able to leave again, they wanted to get back into shape and lose those kilos that had been put on over that short period of isolation. MED and its product Optavia have been benefiting from the resurgence in healthy habits, however, now that with higher prices and interest rates, the company's rather expensive diet plan is the one to be cut first when tightening the strings of the wallet. 33% decline is understandable and certain now; however, can we assume the sales next year will bounce back strong or continue to decrease?

The Product

In my opinion, the sales may continue to dwindle for a while mainly because of that high price and I've read many people's reviews of the product, which is not very appetizing and is very restrictive. People are on 800-1000 calorie diets and that is not very healthy in the long-term. I guess it is okay for that quick loss of weight but is not sustainable in the long run, hopefully, by then, people have changed their eating habits and will be eating proper diets and exercising. $300 a month for the product is very high I think, so I am not surprised that people opt not to use it this year when inflation is so high. The company's initiatives for expansion may be promising. Optavia Active is their new entry into the essential amino acids, whey protein powders, and digital exercise programs, however, will these turn out to be catalysts to reignite the company's decline in sales? It is too early to tell for now but will keep an eye out for future earnings calls.

The Coaches

The company may not market itself like an MLM, however, the resemblance is uncanny. The supposed coaches are just people who have been recruited by other "coaches" who have used the product earlier. I guess they are going for more personal connection with people by saying that they have been through the same journey and got fit and healthy, however, with no actual qualifications to be an actual coach, I wouldn't want to be trained by a person who may not be very well versed in training people like an actual coach.

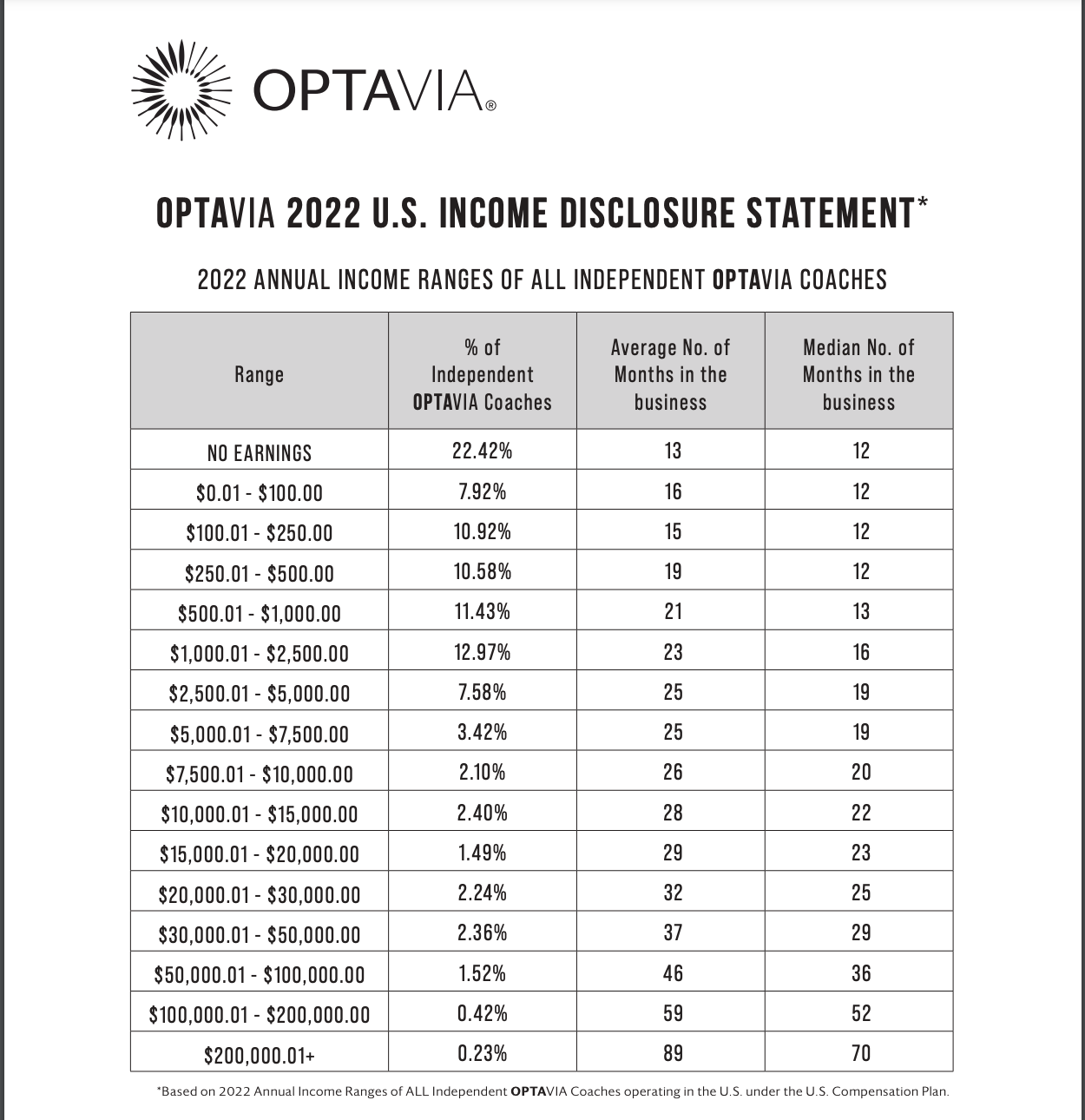

The company's main revenue source is the coaches and a lot of the decline in revenues can be attributed to a decline in active Optavia coaches that are earning money. Many coaches do not even earn a single dime, which of course makes no sense to continue with the program if you're not making money. Sure, you can make money if you really are exceptional at marketing yourself and the product, however, most make very little, which sounds a lot like an MLM.

Coaching Annual income (Medifast Income disclosure)

{kind=link}

Miracle Weight loss drugs

Many miracle drugs for weight loss have recently taken the front stage and many people are saying that companies like Medifast will be obsolete with these drugs doing the rounds across the globe. Sure, there is some merit to it, however, I don't think these drugs are going to take all the market share from MED and other similar companies. It may have contributed to the company's decrease in revenues, however, I believe there will be people who are not going to rely on a drug that may have some long-term negative effects and also the very common side effects of GLP-1 class of drugs, which include nausea, vomiting, and diarrhea. I know for a fact I wouldn't want those side effects in my weight loss journey. At least what Medifast does during the client's weight loss journey is trying to rewire the brain to make better food decisions, whereas with a drug, sure you will lose weight but once you're off it how can they be sure to stick to a better diet and before.

Valuation

So, let's take a look at some assumptions, which are not going to be easy to estimate because of the uncertainty of the company's outlook. These are just my estimates so take them at face value. Your growth assumptions will differ from mine. It is impossible to predict how the company is going to perform in the future, with many different alternatives standing in the way that can take sales and potentially cripple the company's performance going forward. We already know that the company will see around 33% decrease for FY23. The company isn't very well covered on the Street, so only 2 analysts are covering the stock according to Seeking Alpha. I coincidentally ended up going with very similar estimates for the next two years. Below are my assumptions for the base, conservative, and optimistic and their respective CAGRs.

{kind=link}

In terms of margins and EPS, I went with stable margins as the company managed to achieve in the prior years, so most of the EPS fluctuations come from top-line changes. Below are those assumptions.

Margins and EPS assumptions (Author)

{kind=link}

I also went with the company's WACC of around 10% as my discount rate and 2.5% terminal growth rate. On top of these assumptions, I decided to add a 40% margin of safety to the intrinsic value calculation. With that said, MED's intrinsic value is around $100 a share, meaning there is a 50% upside from current valuations.

{kind=link}

Closing Comments

So, it looks like the company is very sound financially. The biggest concern for me is how the company's future ventures in other health segments will pan out and whether these will revitalize the company's top-line growth. I don't think the company saw the worst of the declines for now, so for that reason, I will give the company a hold rating until we get some clarity.

Financially speaking, the company looks like a steal, however, when you look at the company itself, the business model is not appealing to me, the product is not good in my opinion and many people can achieve results without the need to fork over such money and not enjoy your life for a while until you reach your desired weight. There are better ways of doing it, that involve a healthy, balanced, and not deprived diet. The company may have to fall a lot more before I put aside my dislike for the product.

For further details see:

Medifast: Good On Paper, But A Slowdown In Sales Is Very Worrisome