MED - Medifast: The Race To Weight-Loss Drugs Not Lost Yet

2023-10-09 12:17:34 ET

Summary

- Medifast is a provider of weight management solutions with a diverse product line.

- The company has shown strong revenue growth and consistent positive free cash flow but faced sustainable disruptions due to the FDA's approval of weight-loss drugs two years ago.

- The stock is undervalued and has a potential upside of 48%, but the next few quarters are expected to be tough for the company.

Investment thesis

Medifast's (MED) stock hit an all-time high in late May 2021 because the company has been delivering stellar financial performance. But in June 2021, the FDA started approving weight-loss drugs, a big disruption to Medifast. Since then, the stock price declined by more than four times, and the forward dividend yield is now as high as almost 9%. My valuation analysis suggests that the stock is indeed very cheap. On the other hand, the competition from weight-loss drugs, together with the current weak environment, continues to weigh on the top line significantly and the upcoming quarter's earnings do not add optimism as revenue is expected to nosedive again. While I believe that Medifast has not yet lost its battle against GLP-1 drugs, I prefer to wait on the sidelines and assign the stock a neutral "Hold" rating.

Company information

Medifast provides comprehensive weight management solutions that empower individuals to live healthier lives. MED’s product line includes more than 65 consumable options, including, but not limited to, bars, bites, pretzels, puffs, cereal crunch, drinks, hearty choices, oatmeal, pancakes, pudding, soft serve, shakes, smoothies, soft bakes, and soups.

The company's fiscal year ends on December 31. The U.S. is the principal market for the company, according to the latest 10-K report .

Financials

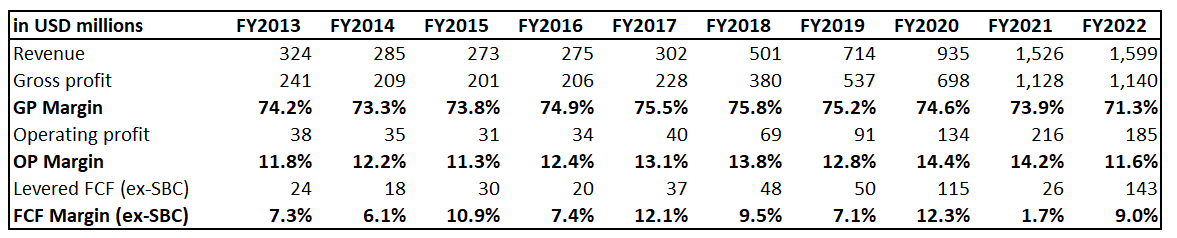

The company's revenue growth has been stellar for the past decade, with a 19.4% CAGR. The gross margin has also been impressive, consistently demonstrating the above 70% level. Despite revenue increasing by about five times over the past ten years, the operating margin did not improve much. The free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been very volatile but consistently positive.

{kind=link}

Having a consistently positive FCF margin enables the company to keep the balance between fueling growth, keeping shareholders happy, and maintaining a sound financial position. MED pays dividends and conducts stock buybacks. The company is in a solid net cash position, and its leverage ratio is insignificant. Liquidity ratios are also in excellent shape.

Seeking Alpha

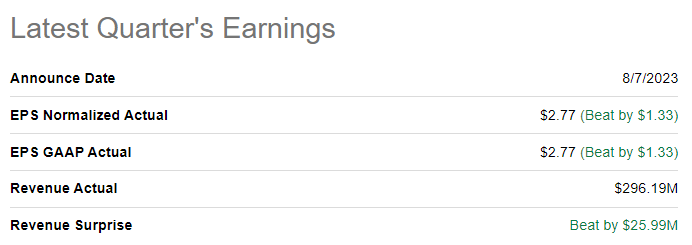

The latest quarterly earnings were released on August 7, when the company topped consensus estimates. Revenue decreased by almost 35% YoY due to a decline in the number of active earning OPTAVIA Coaches and lower productivity per active earning coach. Despite a substantial decline in revenue, profitability metrics demonstrated firm resilience. While the gross margin expanded subtly, the operating margin demonstrated a notable YoY expansion by more than two percentage points.

{kind=link}

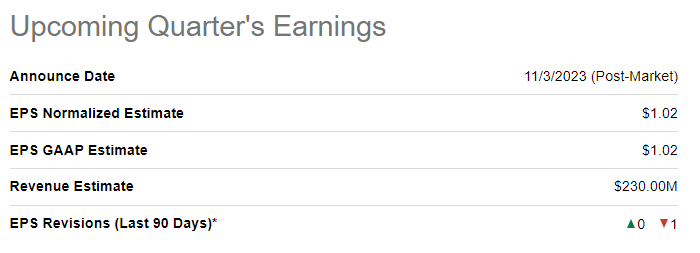

The upcoming quarter's earnings are scheduled for release on November 3. Consensus estimates project quarterly revenue at $230 million, which means a 41% YoY decrease. The adjusted EPS is expected to follow the top line and shrink by about three times.

{kind=link}

The company experiences substantial headwinds due to the current weak macro environment, changes in social media algorithms, and rapidly increasing competition from GLP-1 drugs, which started getting FDA approvals in recent years. The macro environment is a cyclical issue, and I have a high conviction that MED will be able to adapt to changes in social media algorithms. But competition from weight-loss drugs looks like a big challenge. Despite the fact that Medifast's more comprehensive approach to tackling obesity is apparently a healthier option for obese people, the pills might win the race. Taking weight-loss drugs is likely to be a preferable option since it looks like an easier and faster shortcut to achieving the desired weight.

On the other hand, almost 70% of adults in the U.S. are considered obese, meaning that there is a massive target audience, and the pie is big enough to share between drugs and Medifast's offerings. It is also important to underline that Medifast has the potential to expand internationally because obesity is not only an American phenomenon. According to the World Health Organization, obesity is a global problem, and in 2016, about 40% of the global population was overweight.

Valuation

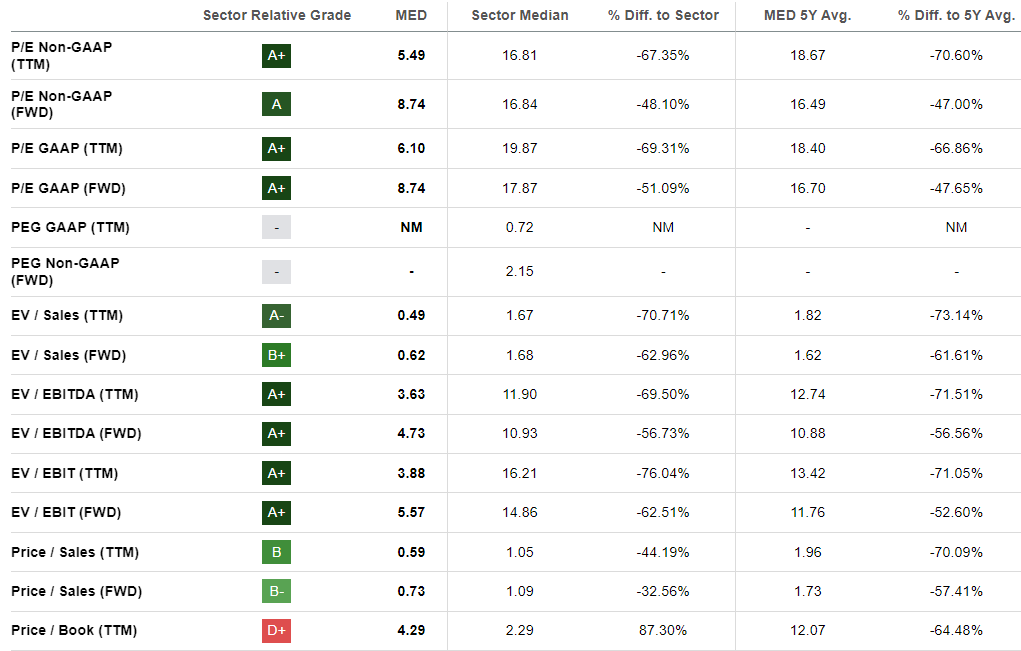

The stock massively underperforms the broader U.S. market this year, with a 36% year-to-date price decline. Seeking Alpha Quant assigns the stock a very high "A" valuation grade because current multiples are substantially lower than the sector median and historical averages. Based on the ratios analysis, I can conclude that the stock is very attractively valued.

{kind=link}

MED is a dividend stock with good ratings, so I think that the dividend discount model [DDM] is a good choice to expand my valuation analysis. Dividend consensus estimates are unavailable, so I refer to history and take the FY 2022 full-year payout of $6.56. I use an 11% required rate of return and expect a 5% dividend growth, which is very conservative compared to the last five-year CAGR of above 20%.

Author's calculations

According to my DDM calculations, the stock's fair price is close to $110. It indicates that the stock is massively undervalued, with a 48% upside potential. The valuation looks very attractive, especially given MED's clean balance sheet.

Risks to consider

I consider regulatory scrutiny as the most significant risk for the company. Changes in regulations, labeling requirements, or health claims can adversely affect Medifast's operations, including product offerings and marketing strategies. Failing to comply with regulatory requirements might lead to significant reputational damage and costly litigations.

The company's financial performance is subject to macroeconomic conditions and consumer spending sentiment. Economic downturns usually lead to reduced consumer spending on discretionary products like weight loss programs. This will ultimately undermine the company's revenue and profitability.

The health and wellness industry is highly competitive and subject to constantly shifting consumer preferences and trends. MED faces the risk of market saturation and increased competition from digital wellness platforms. Any failure to recognize new trends and adapt to them could adversely impact Medifast's market share and profitability.

Bottom line

To conclude, MED is a "Hold". The company faces severe headwinds, both temporary and secular. While I believe that MED has enough resources to weather a temporary storm, the competition from weight-loss drugs looks like a big secular challenge. Side effects of weight-loss drugs and the company's strong track record of success give me a moderate level of optimism that the competition against GLP-1 is still not lost by Medifast. The massive undervaluation of the stock suggests that a very high level of pessimism is already priced in. Despite the attractiveness of the valuation, I prefer to watch at how the company will handle the next few quarters of revenue decline.

For further details see:

Medifast: The Race To Weight-Loss Drugs Not Lost Yet