GEOS - Medium-Term Drivers To Win Over Geospace Technologies' Inventory Concerns

2023-10-17 00:57:04 ET

Summary

- GEOS expects its Oil and Gas and Adjacent Markets segments to perform well in late 2023 and 2024 as the offshore industry outlook improves.

- The company has received a contract for its new shallow water Mariner nodal system and is making initiatives to enter energy transition projects.

- While some product lines have seen diminishing demand, GEOS' balance sheet remains robust with no debt. The stock is undervalued compared to its past average multiple.

GEOS Sits Close To A Ramp Up

I have been discussing Geospace Technologies ( GEOS ) in the past, and you can read my latest article here . I expect GEOS’s Oil and Gas and Adjacent Markets segments to continue performing well in late 2023 and 2024 as the offshore industry outlook improves. Plus, it has received a contract related to its new shallow water Mariner nodal system. The company is also making initiatives to foray into energy transition projects, including carbon storage, geothermal, and mining.

However, some of its product lines have seen demand diminishing, resulting in the company discontinuing certain low-margin and low-revenue products. Cash flows improved but are still wobbly. The balance sheet with no debt, however, remains robust. The stock is undervalued compared to its past average multiple. But the stock price rally over the past six months may have removed the juice from any significant potential upside and validates my “hold” call.

Strategy And New Contracts

GEOS's Q3 2023 Presentation

Strategy And New Contracts

GEOS has favorable conditions for its Oil and Gas and Adjacent Markets segments, leading to improved 2H 2023 and 2024 performance. After the first half of 2023, the company primarily focuses on key developments. One is meeting the demand for smart water products, including the HydroConn series of AMI water meter connectors. The other is to meet the demand for deep and shallow water nodes. Ocean Bottom Nodes products drove 86% growth in revenue for the adjacent market. In specialized manufacturing, it has introduced a blend of vibrating sensors with real-time analytics to capture market share. Due to higher volume, product delivery lead time in the water mater connector product category has reduced in 2023.

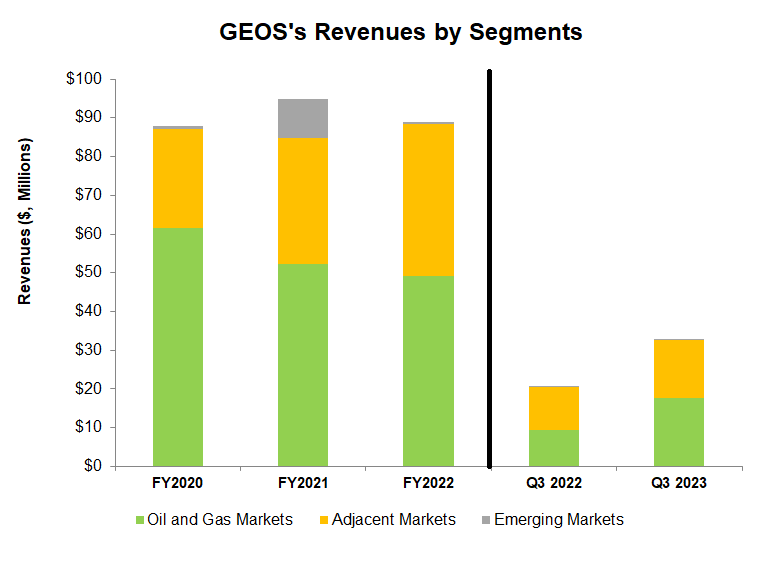

In August, the company received a couple of contracts. It received a $5.7 million contract with an international seismic contractor for an advanced marine sensing application. In another contract valued at a minimum of $3.2 million, it will rent out its Mariner products. Investors may consider investing in this company because of the diversified revenue stream, with 59% coming from oil & gas and 40% from adjacent activities.

Segment Business Outlook

{kind=link}

In the Oil and Gas segment, the company’s rental fleet of OBX ocean bottom nodes, which provides high-resolution seismic data, is near full utilization. These products have been deployed in the North Sea, the Middle East, the Far East, West Africa, and the Gulf of Mexico. Recently, it received a $20 million contract to rent its new shallow water Mariner nodal system. However, investors may note that the seismic sensor portion of the business is difficult to foresee and can disrupt the planning process.

In Industrial Products, the company focuses on smart meter connectors, water utility IoT control, monitoring, and data management. The smart meters see increased demand following the smart city initiatives within municipalities. The smart city initiative will likely grow in the future, and so will the demand. Its Aquana subsidiary has recently announced the release of its Actuator Valve Serial. This was a remote shut-off valve designed to reduce the cost of operations and enhance safety. Among other products, we see an increased demand for electronic prepress products. The long-term demand growth in the adjacent market products will persist based on cyclicality.

The Emerging Markets segment significantly depends on the government and defense industry contracts. The company aims to secure contracts for perimeter security and new energy transition applications. In 2023, it received a contract for marine solutions from the Defense Advanced Research Projects Agency (or DARPA). Its new energy transition initiatives include carbon storage, geothermal, and mining.

Challenges

{kind=link}

Crude oil prices have strengthened in the past few months, which is a positive for the energy industry. However, a lag occurs between rising oil prices and rising demand for the company’s Oil and Gas Markets segment products. As the lag persists in the short term, I expect onshore energy and wireless products will see low demand. In the medium term, I also expect the company’s customers will consume their excess levels of underutilized equipment. On the other hand, demand for the marine wireless rental fleet has increased, leading to near-full utilization.

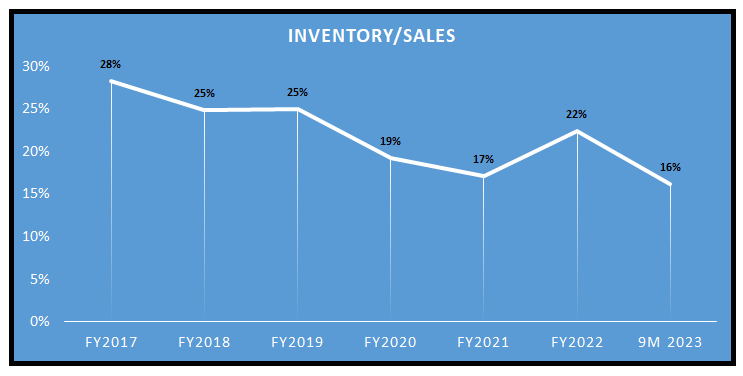

The company has discontinued manufacturing certain low-margin and low-revenue products in this scenario. It has also reconfigured its production facilities to lower our costs. Despite that, the inventory balances have increased compared to the demand for Oil and Gas Markets products. Plus, it has added new inventories for new wireless products. So, it may continue to record obsolescence expense as it experiences reduced demand.

Q3 Performance Analysis

{kind=link}

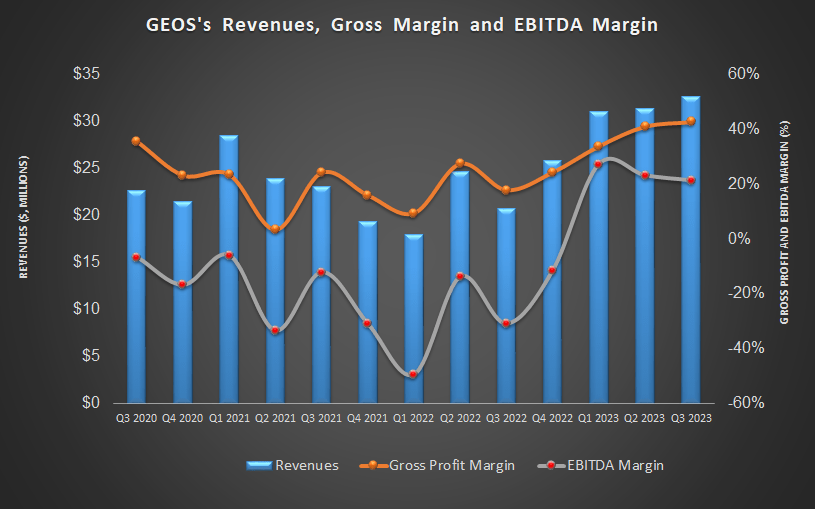

In Q3 2023, GEO’s year-over-year revenues from the Oil and Gas Markets segment increased by 86%. Increased utilization of its marine OBX rental fleet and higher demand for seismic sensors caused a sharp rise. During Q3, the sale of marine streamer products allowed profitable growth in the traditional seismic exploration product suite.

The Adjacent Markets segment saw 36% year-over-year growth in Q3. The company’s recent decision to increase manufacturing capacity to meet the demand for connector cables and water meters resulted in the topline growth. Also, the imaging product line introduced affordable pricing to garner market share in a multi-billion-dollar screen print industry. On the other hand, GEOS’s revenues decreased by 19% in Q3 in the Emerging Markets segment.

Cash Flows And Liquidity

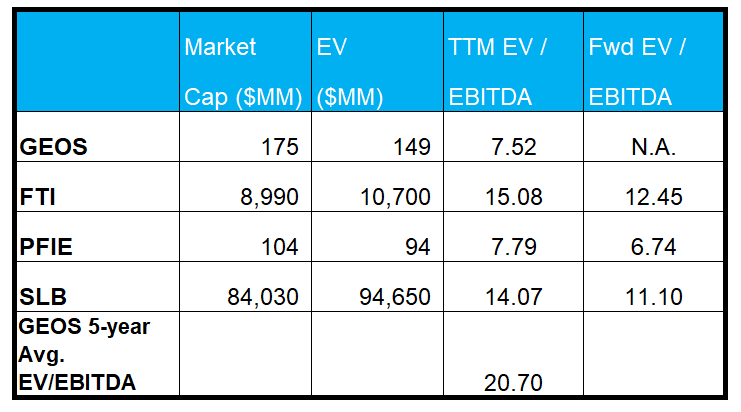

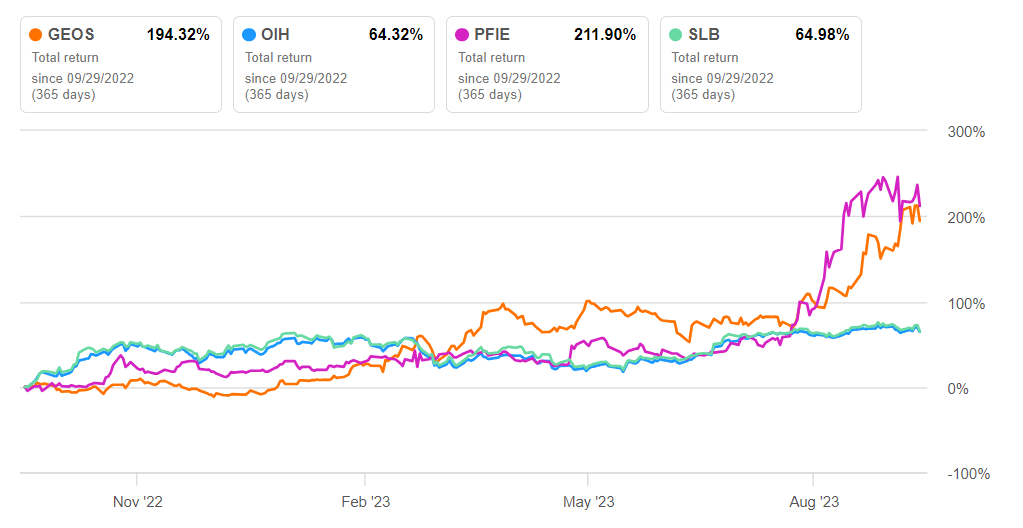

In 9M 2023, GEOS's cash flow from operations improved and turned mildly positive compared to the previous year. Higher revenues mainly accounted for the improvement in cash flow. Free cash flow also recovered in 9M 2023. GEOS has no debt. This offers an advantage over some of its peers (FTI and SLB). Its liquidity (cash & short-term investment plus working capital) was $88 million on June 30.

What Does The Relative Valuation Imply?

Author Created and Seeking Alpha

{kind=link}

GEOS's current EV/EBITDA multiple (7.5x) is much lower than its five-year average (20.7x). So, it appears to be undervalued versus its past. If the stock trades at its five-year average, it would provide a 147% upside potential. However, given the uncertainty over the energy industry, the stock cannot return to its past status (i.e., relative valuation). The stock price has also increased considerably (58% up) over the past six months. So, I think, investors should not expect more than 10% returns in the short term.

Why Do I Keep My Rating Unchanged?

I did several iterations of my analysis about GEOS in the past. The common themes that cut across the analysis are GEOS's plans to consolidate OBX rental operations and reduce costs. The sale of water meter cables and related products started to increase. However, its financials suffered from continued net losses over the past several years. In the previous article, I noted that the offshore market improved in the US. However, it became cautious over the oil and gas seismic equipment fleet addition plans. I wrote :

demand for its water meter cable and connector products will stay robust following domestic municipalities' smart meter infrastructure update process. Plus, there can potentially be a few undisclosed major defense contracts in the future.

Since I last published, the company has focused on smart water products and deep and shallow water nodes. However, demand for onshore energy and wireless products can remain low in the near term. Excess inventory can also be an issue. Cash flows, on the other hand, improved. Considering various value drivers, I keep its rating unchanged at "hold" versus the previous call.

What's The Take On GEOS?

{kind=link}

While a robust offshore energy industry has led to higher demand for deep and shallow water nodes, increased adoption of smart meters from various municipalities has shored up demand for its HydroConn series of AMI water meter connectors. This connection will increase demand for associated products like utility IoT control, monitoring, and data management.

However, the demand for seismic sensor products is difficult to foresee and can disrupt the planning process. I see a lack of demand for onshore energy and wireless products. Although the company’s cash flows have improved, they are unsubstantial at the current level. The stock price rallied rapidly in the past six months. Nonetheless, given the relative valuation, I think investors should continue to “hold” it for steady medium-term returns.

For further details see:

Medium-Term Drivers To Win Over Geospace Technologies' Inventory Concerns