MEDP - Medpace: Building Stronger Foundations Each Quarter

2023-10-24 16:58:20 ET

Summary

- Medpace operates as a Contract Research Organization, providing clinical development services to the biotech, pharma, and medical device industries.

- Despite challenging macroeconomic conditions, Medpace's Q3 results demonstrate revenue growth, stable profitability, and excellent cost control.

- If the price returned to $230 or $240 levels, it would be a more than compelling opportunity, since the company continues to demonstrate an improvement in its fundamentals.

Investment Thesis

In my last article about Medpace ( MEDP ), I commented that the company had very solid fundamentals. However, the price seemed a bit expensive to me. Well, the shares had fallen 16% since I wrote that article to around $227, but that was before the latest report for Q3 2023 that shows us that the underlying business continues to improve. Moreover, the management decided to raise the guidance provided.

However, the stock price rose 18% after the report was released, so I will maintain my 'hold' rating until the stock returns to prices close to $230 USD.

Business Model

Recapping about the business model: The company is a Contract Research Organization, so its business model is focused on providing outsourced clinical development services to the biotechnology, pharmaceutical, and medical device industries.

Before a new drug can be brought to market, it often must undergo extensive preclinical and clinical testing, as well as regulatory review, to verify safety and efficacy. As you can guess, this is not cheap; in fact, it is estimated that the cost of getting a new drug approved is around $2.5 billion, and it takes about an average of 10 years.

Phases of a New Drug (Cancer NSW Gov)

This why small and medium-sized companies often face challenges when developing their medicines and drugs independently. This is where companies like Medpace come into play, as they can efficiently handle these tasks and guide the successful progression through the development process, from Phase I to Phase IV.

This is primarily attributed to two key factors:

- Medpace's established professional infrastructure.

- Their know-how in conducting these therapeutic trials.

Revenue is generated through fees outlined in the contracts for services provided. The contract duration and pricing are generally based on a fixed fee, which takes into account activities performed by third parties and the associated ancillary costs necessary to fulfill the contract's scope (which are reimbursable). These contracts can vary in duration, spanning from a few months to several years, and are negotiated based on the projected project scope, including complexity and inherent performance risks. They are structured with an initial fee due at contract signing, with the remaining fee paid over the contract's duration, either according to an agreed-upon billing schedule or upon achieving specific performance milestones.

As a result, it becomes evident that income tends to be stable and predictable, thanks to the structure of contracts and the manner in which income is received. Additionally, the importance of these services to Medpace's clients makes it challenging for them to abruptly halt their orders, regardless of the prevailing macroeconomic conditions.

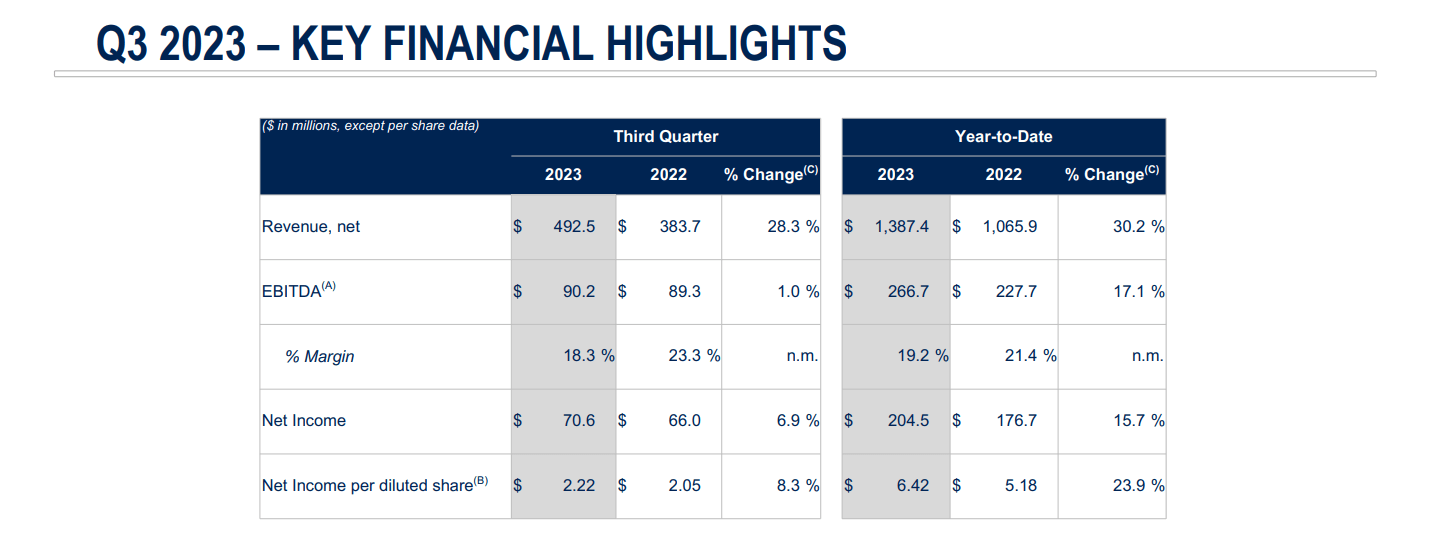

Q3 Results

On October 23, the company released its quarterly results for the third quarter of 2023. These results demonstrated that, despite the challenging macroeconomic situation, revenues continue to grow, and profitability remains stable. The results were as follows:

- Revenue for the first 9 months of FY2023 reached $1.39 billion, representing a growth of 30% compared to the same period of the previous year.

- The EBITDA margin remained at FY2021 levels, falling from 20.6% achieved in FY2022 to the current 19.4%.

Despite this margin compression, the change is not very significant. It indicates a business that is resilient in the face of inflationary environments and recession fears. This is in contrast to companies in other sectors that have already begun to experience the effects of rising interest rates and the long-awaited recession.

- Net Income margin went from 16.8% to 14.7%.

- Shares outstanding reached 31.8M, meaning the company has repurchased 5.4% so far this fiscal year.

This excellent cost control also had a positive impact on the bottom line, despite expectations of worse results. Much of this can be attributed to the aforementioned practice of receiving payment for contracts before the services are performed.

Some other data to highlight are the following:

- Accounts Receivable grew 17% YoY (vs the 30% growth in revenues). This is positive because it implies that the company is collecting cash from its customers more efficiently and quickly relative to the sales it is making.

- Accounts Payable increased by only 2.75% year over year. This indicates that Medpace is not indiscriminately increasing its outstanding obligations to suppliers and creditors. In other words, the company is reducing some of the amounts it owes to its vendors, which will lead to an enhancement of working capital and, consequently, better cash conversion.

- Advanced Billings grew by 24% year over year. It's worth noting that the company charges in advance for some of its services, and these advance payments are reflected on the balance sheet until the services are performed. This provides a strong indication of the growth potential that the company may continue to experience in the coming months.

{kind=link}

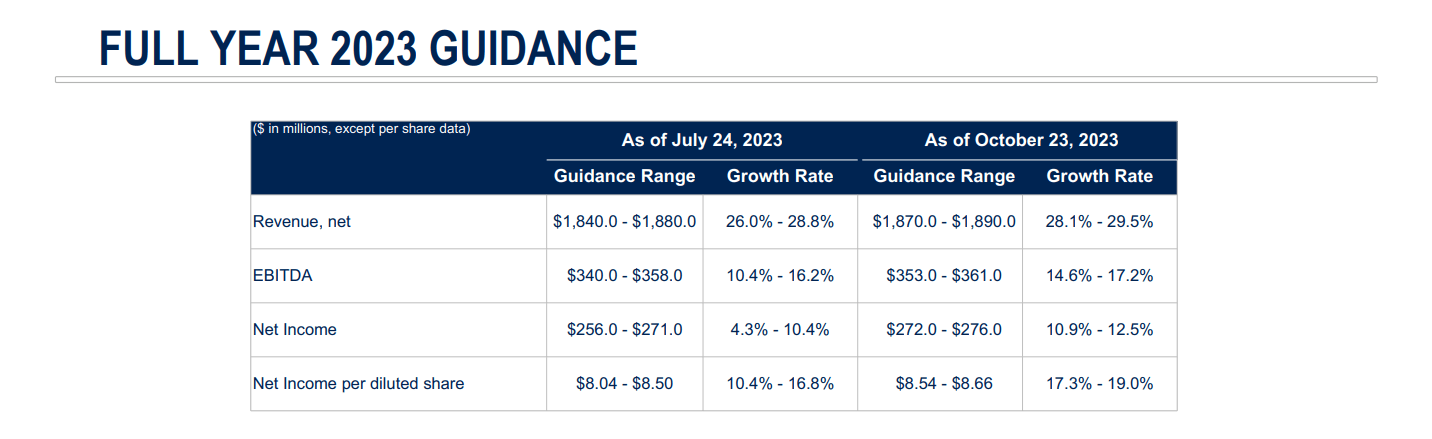

New Guidance

In Q2 2023 , the company had announced guidance that indicated year-over-year (YoY) revenue growth ranging between 26% and 28.8%. This represented a substantial increase compared to the guidance provided in Q1 2023 , which indicated growth between 19.5% and 23.6%.

Now, in Q3, the company anticipates YoY growth between 28.1% and 29.5%, aiming for $1.80 billion in revenue. It's evident that the company tends to be conservative, often resulting in better-than-expected results.

Similar trends can be observed in other metrics. For instance, in Q1, the estimated net income for the year ranged from the lower end of $250 million. In Q3, the company now anticipates a net income of $272 million, again in the lower end, resulting in a margin of 14.5% and earnings per share around $8.6. In other words, the company would be trading at a forward price-to-earnings ratio (P/E) of 26x.

{kind=link}

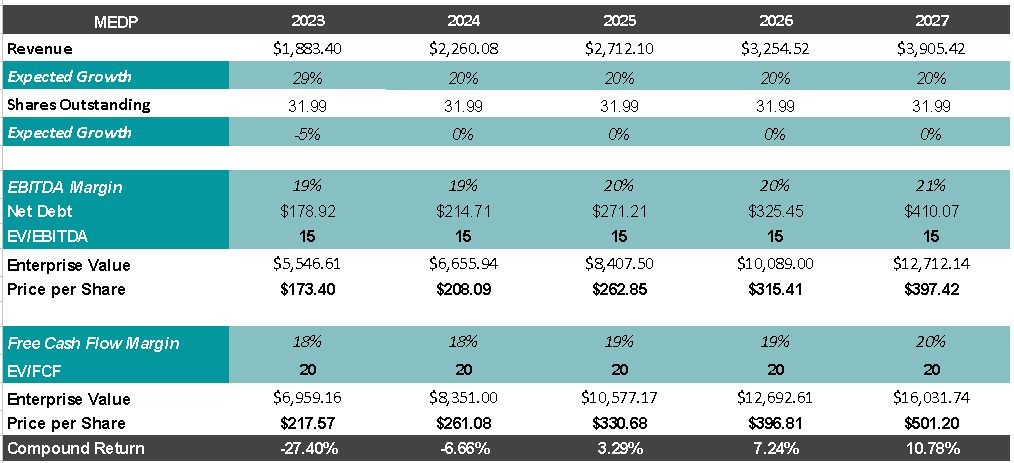

Valuation

In my valuation, I will consider the new guidance and take a midpoint for both Revenue and Margins. This implies revenues of $1.88 billion for FY2023 and EBITDA of $357 million, resulting in a margin of 19%. This is in line with the guidance range of $1.87 billion to $1.89 billion in revenue and $353 million to $361 million in EBITDA.

This already translates to an annual return of 10% from the current share price of $270 at the time of writing this article. However, if we consider only the Free Cash Flow valuation, the annual return would be nearly 13%.

{kind=link}

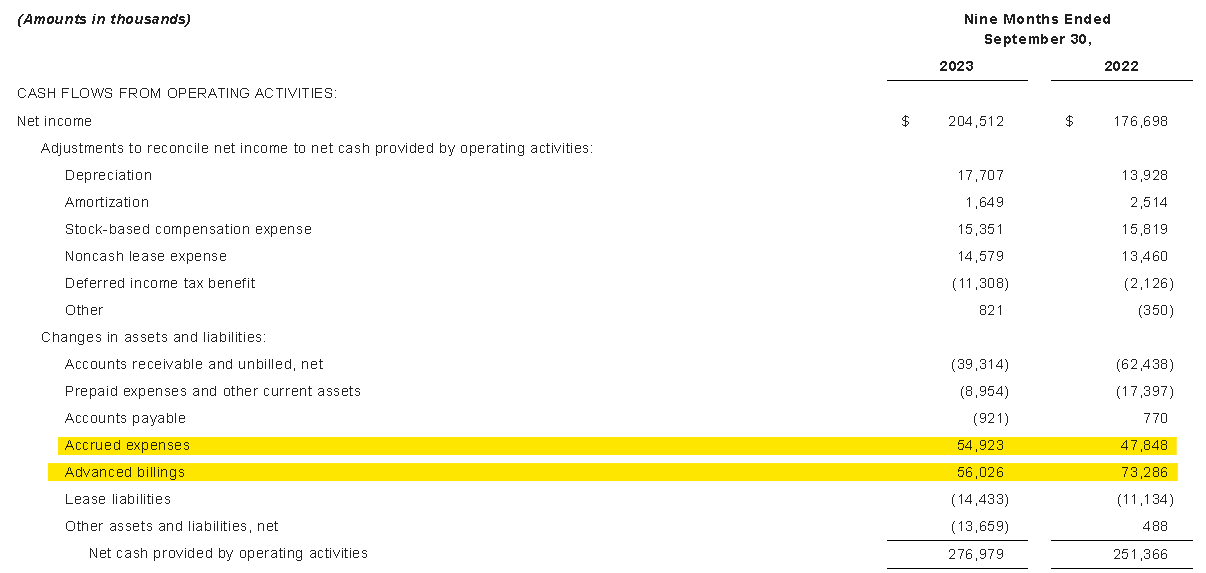

It's worth noting the significance of valuing Medpace using Free Cash Flow, as the company is typically affected in the Income Statement due to Accrual Accounting. This accounting method requires them not to account for the cash collected for services that have not yet been provided. For example, when we examine the Cash Flow Statement, we can identify $110 million in Accrued Expenses and Advanced Billings. While these amounts are subtracted from the Income Statement, they are considered when calculating Free Cash Flow, making it a reliable method since it shows us the actual cash available to the company for various purposes, including reinvestment in the business, debt repayment and acquisitions.

{kind=link}

Final Thoughts

The new quarterly report reaffirms the company's robust financial position and the quality of the business. An analysis of the balance sheet reveals a healthy company that should weather a recession without difficulties. Additionally, the company has demonstrated efficiency in collecting payments from its customers and managing its supplier relationships to enhance working capital.

It is worth mentioning that the risks remain the same as those mentioned in my previous analysis . Sadly, after the share price rose post-quarterly report, I have decided to keep the rating on hold until the price returns to the previous levels around $227.

For further details see:

Medpace: Building Stronger Foundations Each Quarter