ANFGF - Meet The Bright Future Of Copper With Antofagasta

2023-10-04 09:50:26 ET

Summary

- Antofagasta plc receives a Hold rating due to its medium-/long-term growth prospects and plans to expand copper production in Chile.

- S&P Global Market Intelligence predicts a robust copper price environment over the next five years, including a potential copper shortage.

- Antofagasta plc aims to increase annual copper production through expansion projects at its mines in Chile.

A Hold Rating for Antofagasta plc

This analysis assigns the stock in Antofagasta plc (ANFGF) a recommendation rating of Hold as shares of this British producer of copper and by-products such as molybdenum and precious metals in Chile are subject to the following outlook.

The Medium-/Long-Term Outlook

The rating is motivated by an interesting medium/long-term outlook, influenced by the company's plan to expand copper production in Chile, the largest producer in the world while benefiting from the enormous growth potential that this metal offers as a key component of the global energy transition program.

S&P Global Market Intelligence forecasts a robust copper price environment over the next five years, with the price per pound expected to reach $3.902 in 2024, up from $3.6040 currently, and expected to reach $4.368 in 2027. S&P Global Market Intelligence forecasts the copper price per metric ton. However, since 1 metric ton is approximately 2,204.62 pounds, the projections as presented in this analysis are per pound.

Higher copper prices will be fueled by robust copper demand as the world will need more of this base metal for the construction of clean energy generation technologies. On the supply side, a number of issues affecting supply will be resolved going forward, such as declining ore grades, supply disruptions, and bureaucratic inertia in obtaining permits for mining projects. However, given S&P Global Market Intelligence forecasts, a copper shortage appears inevitable, which would boost the metal's price in a couple of years.

The company produces copper cathodes and copper concentrates, which is its primary source of income, from:

- its 60% interest in the Los Pelambres mine, whose production represented ? 44% of the company's total copper production of 295,500 tons in the first half of 2023 . Cash costs before by-product credits were $2.04 per pound of copper versus the company's $2.48/lb. Net cash costs were $1.17/lb versus the company's $1.75/lb in the first half of 2023.

The aim of the Los Pelambres mine is to increase annual production in the medium term by implementing an expansion of the mineral asset's capacity for copper production in two phases.

The $2.3 billion Phase 1 expansion project aims to increase annual copper production by an average of 60,000 tonnes per year over 15 years, to be achieved by increasing throughput. This goal is expected to be achieved through the commissioning of the seawater desalination plant and the expansion of the concentrator by the end of 2023. The ongoing production ramp-up is expected to continue in the second half of 2023.

The Phase 2 expansion project aims to double the seawater desalination plant's capacity to 800 liters per second by 2026 and extend Los Pelambres' current mine life of approximately 12 years by at least 15 years. Annual copper production is expected to increase by 35,000 tonnes as expanded tailings storage and concentrator capacity will provide the opportunity to develop a larger mineral resource base of approximately 6 billion tonnes.

- its 70% interest in the Centinela mine, whose production represented ? 37% of the company's total copper production in the first half of 2023. Cash costs before by-product credits were $2.82 versus the company's $2.48/lb. Net cash costs were $1.88/lb versus the company's $1.75/lb in the first half of 2023.

The company has a $3.7 billion expansion project aimed at producing 170,000 tonnes of copper equivalent annually in the first ten years through the construction of a second concentrator and a tailings storage facility both near the existing concentrator.

At the end of the year, the company will present a phase 2 project to the consideration of the board to further develop the second concentrator so that the facility can process 150,000 tons of ore per day from 95,000 tons of ore per day in phase 1, thereby accommodating more ore from mining operations conducted at the Centinela mine.

- its 70% interest in the Antucoya mine, whose production represented ? 13% of the company's total copper production in the first half of 2023. Cash costs were $2.72 per pound of copper versus the company's $2.48/lb.

- its 50% interest in the Zaldívar mine located in Chile, whose production represented ? 6.7% of the company's total copper production in the first half of 2023. Cash costs were $2.96 per pound of copper versus the company's $2.48/lb.

Antofagasta plc expects that through these projects it can achieve an annual production of 900,000 tonnes of copper in the long term, which will represent an increase of 34.3% to 40.6% from 640,000 tonnes to 670,000 tonnes that the company predicted for the full year 2023.

A strong positive contribution to Antofagasta plc's growth prospects comes from the People's Republic of China.

The government of the People's Republic of China's stimulus measures to enable the economy, which is the second largest in the world , to recover from three years of restrictions against COVID-19 and overcome the headwinds of the severe crisis in the real estate sector will contribute significantly to Antofagasta's growth, as China consumes the most refined copper in the world .

The Chinese gross domestic product already showed encouraging signs of recovery in the second quarter of 2023.

What Can Happen in the Short Term?

However, against this backdrop, the rating cannot currently be higher than a Hold, as shares are on the way to form a more comfortable entry point and become a better opportunity to gain exposure to the mentioned medium/long outlook for copper.

In the short term, shares face the likely headwinds of an expected deterioration in the economic cycle of the US, as certain indicators suggest.

There is a good chance that the US economy will enter a recession with a significant devaluation of copper, as such a sharp economic downturn has a strong dampening effect on copper demand.

The need to keep interest rates higher for longer following another hike, likely around the end of 2023, increases the likelihood of a serious slowdown in the U.S. economy as higher borrowing costs continue to impact consumption, which accounts for nearly 70% of U.S. GDP , and investments.

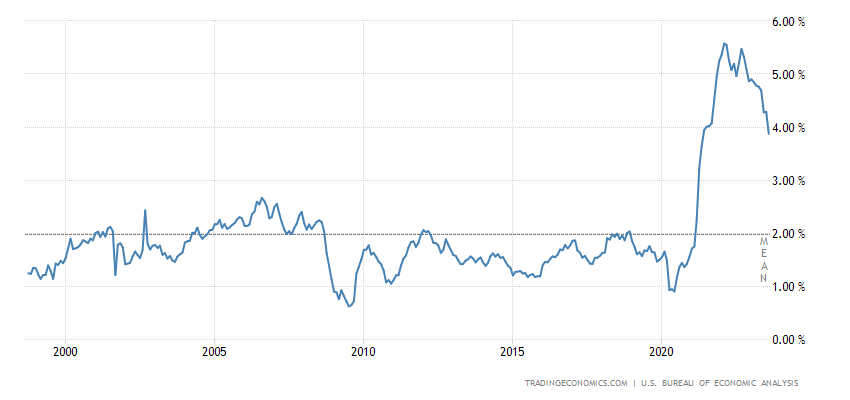

Inflation will continue to weigh on US household purchasing power as, despite the Federal Reserve's monetary policy, the US core PCE price increase of 3.9% year-on-year in August remains a long way off the median target rate of 2%.

{kind=link}

BofA card spending has fallen sharply for weeks , and this reluctance by US households to spend, which is proving more persistent than many economists probably expected, is now raising concerns of an impending slowdown.

Not only could it be the loss of thousands of jobs, with the current dispute between automakers and the United Auto Workers being a warning sign, but two other major headwinds are likely to impact household spending and subsequently weigh on consumption:

These are as follows:

- the impact of expensive energy purchases on inflation as fossil fuel prices are pushed up by OPEC+ crude oil cuts, including Russian retaliation in response to the West's continued support for the Kyiv government in its conflict with Russia.

- the resumption of student loan payments after a three-year moratorium granted during the COVID-19 pandemic. About $1 trillion in student loans is such a huge sum for students to pay back to lenders that many of their families will likely be forced to hold on to multiple categories, and not just furniture.

Looking at the near-term outlook for their incomes, businesses and labor market conditions, consumers assigned a score of 70, which has historically been associated with a recession within a year of the survey.

How a Recession Can Affect Copper and Antofagasta plc Shares

The red metal is used in the manufacture of a variety of products that a technologically powerful society uses every day. Therefore, a recession that dampens demand for this base metal will put strong downward pressure on the pound. Since Antofagasta plc gets almost 90% of its total revenue from copper sales, a weaker metal price will correlate with a lower share price as the market downgrades the company's profitability.

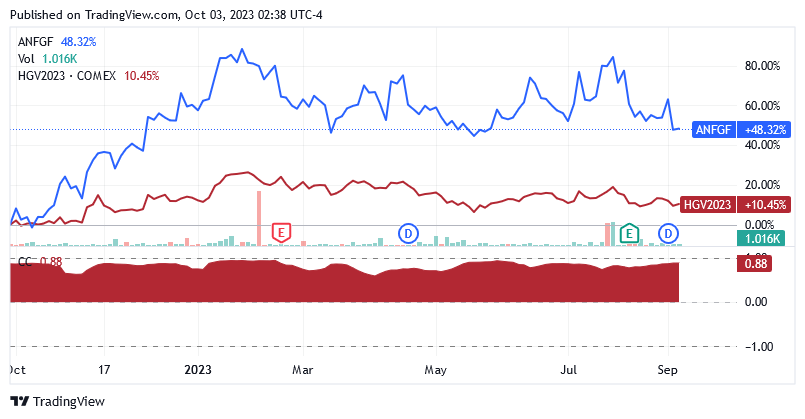

Seeking Alpha's chart shows that the correlation between Antofagasta plc share price and copper price is positive and also very strong, as the red area, which is a graphical representation of the correlation coefficient, has always been well above zero over the past year.

{kind=link}

This analysis assumes that the recession, expected as early as 2024, will create a new negative catalyst that, under the same dynamics as in the first half of 2023, will have a noticeable impact on the share price of Antofagasta plc.

In the first half of 2023 , despite higher copper and byproduct sales volumes, EBITDA margin declined 290 basis points year-over-year to 46.1%, as a lower realized price for copper sales caused EBITDA growth to lose ground relative to revenue growth. EBITDA increased 7.5% year over year to $1,331 million, while revenue increased 14.3% to $2,890 million.

In the futures market, the copper price per pound fell 10.5% from an average of $4.423/pound in the first half of 2022 to an average of $3.957/pound in the first half of 2023.

The company reported results for the first half of 2023 on August 10, but these were not welcomed by the market as the share price has since fallen 16.4%.

However, a renewed negative trend in Antofagasta plc share price as a result of the expected recession should not be viewed by investors as a problem, as this analysis would otherwise have suggested a Sell rating, but rather as an opportunity to increase their position in this stock. A lower price therefore allows investors to benefit more from the medium to long-term growth prospects of the copper market.

The Stock Valuation

Shares of Antofagasta plc have fallen sharply in the past two months amid growing fears about copper demand following the Fed's 25 basis point interest rate hike on July 26 and China's housing crisis.

{kind=link}

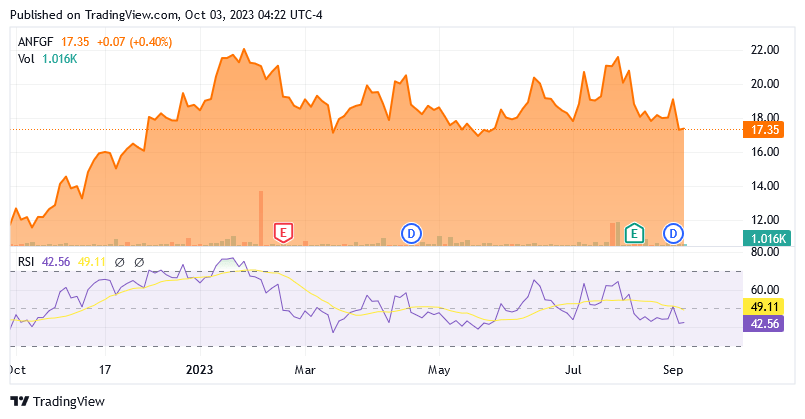

The shares are trading at $17.35 each at the time of writing, giving a market cap of $17.19 billion. They are trading well below the 75-day moving average line of $18.58 but are still slightly above the longer-term trend of the 175-day moving average line of $16.84.

Shares are also trading slightly above the $17.24 midpoint of the 52-week range of $11.53 to $22.95.

In terms of the enterprise value to EBITDA ratio, Antofagasta plc shares are more attractively valued than most of its peers.

In fact, Antofagasta plc has a forward EV/EBITDA ratio of 7.07x versus First Quantum Minerals Ltd. ( OTCPK:FQVLF )'s 8.24x, Lundin Mining Corporation ( OTCPK:LUNMF )'s 5.39x, Metals Acquisition Limited ( MTAL )'s 3.75x, and Taseko Mines Limited ( TGB )'s 7.21x.

Also, Antofagasta plc has a 12-month EV/EBITDA ratio of 7.23x versus First Quantum Minerals Ltd.'s 10.47x, Lundin Mining Corporation's 8.74x, and Taseko Mines Limited's 11.15.

A stock comparison based on the EV/EBITDA ratio makes a lot of sense according to this analysis because investors heavily consider EBITDA when assessing the profitability of a capital-intensive industry like a copper mining company.

Under the negative pressure from another Fed rate hike and the expected recession, the United States Antofagasta plc's shares could fall from current levels and may form an incredibly attractive market valuation in relation to medium and long-term growth prospects.

It will take a while as Duke professor and Canadian economist Campbell Harvey, who developed the recession indicator, which consists of comparing the yield on three-month U.S. Treasury bonds with the yield on 10-year U.S. Treasury bonds, points to a high probability of a recession as early as 2024 . So just stick to a Hold rating for the time being.

{kind=link}

The 14-day RSI of 42.56 suggests shares are at oversold levels, but despite the sharp decline over the past two months, there is still plenty of room for the downside to reach lower levels.

About the Dividend

The shareholder of Antofagasta PLC receives the payment of a dividend, the amount of which depends on the price and sales volumes of the metals, in particular copper, as the red metal represents 90% of the profit. Antofagasta's dividend policy aims for the semi-annual dividend to be approximately 35% of net profit.

The dividend is paid out twice, so here the shareholders receive a semi-annual dividend. For the 2023 calendar year, they received $0.505 per share, paid on May 12, 2023, and $0.117 per share paid on September 29, 2023.

The price of copper, Antofagasta's main source of income, has been in a downward trend since July 2023, losing 4.5%. S&P Global Market Intelligence predicts a weaker pound in 2023 and a slightly lower price in 2024 (one metric ton is approximately 2,204.62 pounds), both compared to the calendar year 2022 when the annual payout hit a record $1,281 per share. The board's next 12-month dividend could be lower than in 2022.

Adjusted for share price fluctuations due to various market headwinds from macroeconomics and the company's interim financial reports, a lower 12-month dividend than in 2022 resulted in a downward trend in Antofagasta's share price so far.

Source: Seeking Alpha

As continued pressure on the price per pound is likely to result in the next interim dividend being lower compared to 2022 and the market adjusting the valuation of Antofagasta PLC shares accordingly, this is yet another reason to Hold on to the stock for the time being.

As of today, the annualized dividend yield is 3.58%.

The Risk

Given the volatility of the copper market, neither the company nor the investor has control over the commodity. A position in Antofagasta plc stock carries some risk that the company will not be able to successfully develop its projects to increase future annual copper production to 900,000 tons. But this is a low risk.

From a geopolitical perspective, this analysis assumes that operating in Chile is low risk. As the Sprott Mining Risk Heat Map 2023 shows, Chile offers a friendly environment for companies looking to install or expand mining operations in the Latin American country.

From a financial perspective, Antofagasta plc's balance sheet appears to be reasonably strong to support the expansion projects and development of Mine of Life.

As of June 29, 2023, the financial condition of Antofagasta plc was characterized by a net debt position of $820 million , but an interest coverage ratio of 18.42x coupled with an Altman Z Score of 3.04 (scroll down this web page to the "Risk" section) points to a situation in which the company can afford debt capital, and that is almost the case, there is no risk of bankruptcy.

The interest coverage ratio is calculated by dividing the trailing 12-month operating income of $1.75 billion by the trailing 12-month interest expense of $95 million.

The Altman Z-Score measures the likelihood that a company will face bankruptcy problems. If the value is less than or equal to 1.8, the balance sheet is in distress zones, which means a high probability of bankruptcy within a few years. When the ratio is between 1.8 and 3, the balance sheet is in a gray area, which still implies a risk of bankruptcy, albeit moderate. While a score of 3 or higher means that the risk of financial insolvency is extremely low or non-existent.

Conclusion

Under the influence of an expected recession as early as 2024, Antofagasta plc's EBITDA margin is likely to deteriorate somewhat. In response, the share price will create more attractive entry points, but expansion and mine development projects are not at risk.

This stock has a Hold rating as Antofagasta plc's medium- to long-term growth prospects make this copper producer in Chile an interesting vehicle to participate in the metal's bright future as an important part of the energy transition.

For further details see:

Meet The Bright Future Of Copper With Antofagasta