MEGEF - MEG Energy: Buyback Bonanza Likely Coming

2023-12-07 20:25:32 ET

Summary

- MEG Energy is a top Canadian oil sand producer with capital appreciation potential and leverage to rising oil prices.

- The company has had a good first 9 months of 2023, with solid production growth and a reduction in debt levels.

- Once debt reaches $600m US, MEG will see a large increase in share buybacks, acting as a strong taillwind in 2024.

MEG Energy ( MEG:CA , [[MEGEF]]) is a top Canadian oil sand producer, with the right combination of production growth and leverage to a rising oil price. The company is in the neighborhood of $6.85 Billion CAD today, as it has pulled back with wider oil price concerns. The market cap is the perfect level for institutional investors as they can build sizable positions due to its strong liquidity and the underlying fundamentals. The company is prolific in the Christina Lake area of Alberta, with a heavy oil focus meaning big benefits from a strong oil price. As a result of these things I am holding and currently adding to positions of MEG, as the best capital appreciation potential in oil and gas today. Once debt gets down to its target of $600 million US, 100% of free cash will be going back to shareholders. This should increase the returns in 2024 for MEG as share buybacks will be able to increase significantly. As with any oil and gas producer I would suggest those buying to have a bullish view on oil before investing. The demand market is shaky with China not providing the rebound many hoped in consumption in 2023. However, American companies continue to be prudent with drilling new wells and OPEC is continuing to cut production to stabilize prices. This means a floor in the region of $65 is likely, especially with the US government slowly beginning to refill the SPR (Strategic Petroleum Reserve).

Q3 - Free cash machine

MEG has had a strong 2023, with solid production growth and continued reduction of debt load. Production for Q3 was strong 103,726 barrels per day , with the year to date averaging 8000 more barrels than 2022 at 98835 per day. This led to adjusted fund flow of $492 million of which $402 was free cash flow after capital expenditures. Operating netback per barrel was $58.64 dollars, showing strong leverage to the favorable oil price in Q3. The company projected that for 2024 to an average bpd of 105,000 , which would be another 4% growth in production. This is bullish as oil companies continue to focus on generating cash more than outright production growth. Keep in mind with turnaround and maintenance activities the average production will be lower than the maximum, which is 110,000 per day. Only $100 million is being allocated per year the next 3 years for production ramp - the remainder to maintenance and cash return. The market has responded positively to the update as the company focused more on cash generation than significant growth of production.

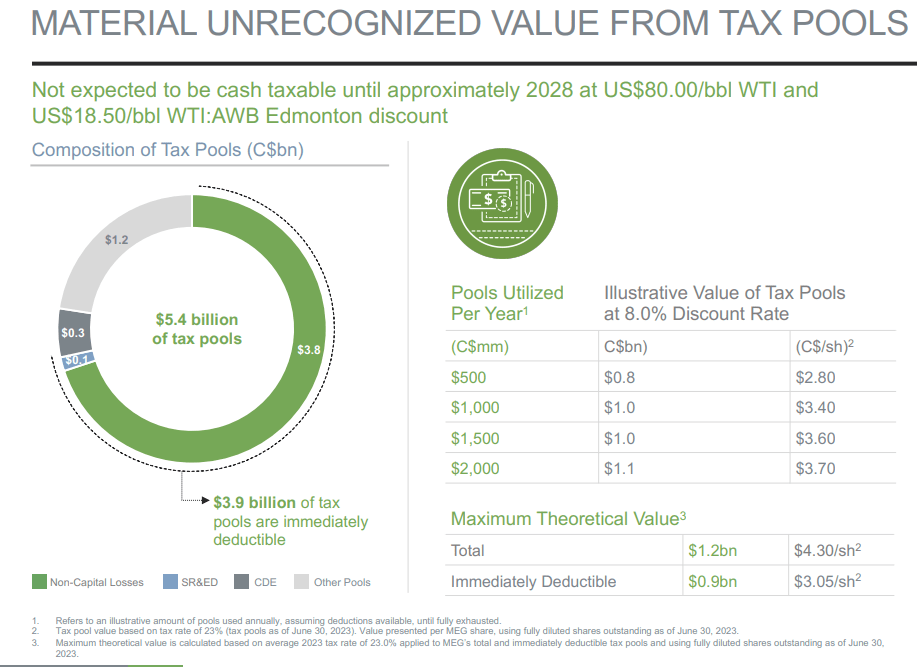

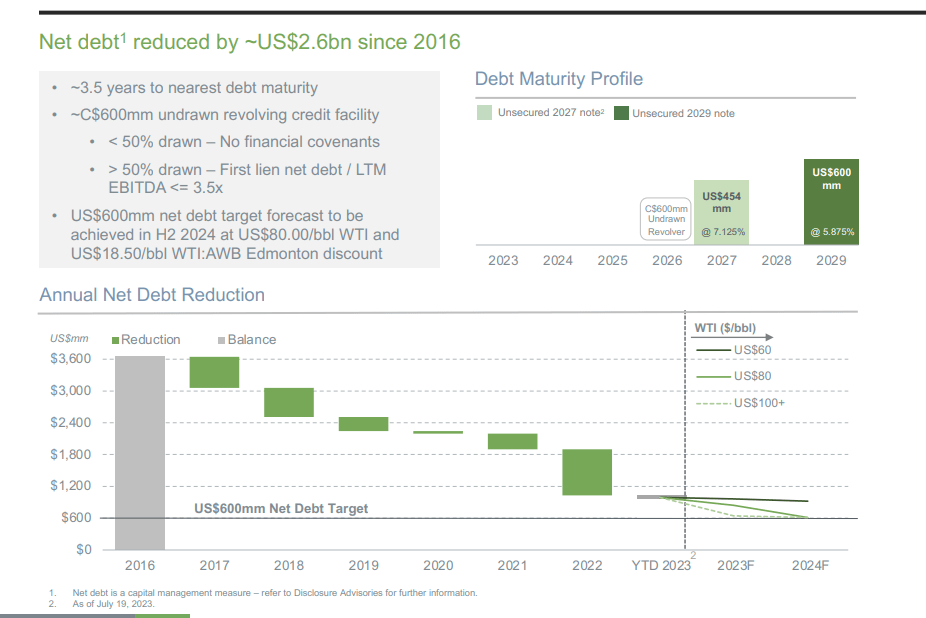

The company is paying back debt at a good clip, with $194 million US of debt reduced year to date. This puts debt at a reasonable level of $885 million US, only $285 million away from its goal of $600m. Once it reaches that level the company will see a large bump in share buybacks to 100% of free cash. At current prices this will be a late 2024 or early 2025 event, if WTI can rebound to the $80 level with the stock likely moving up before this occurs. Keep in mind that MEG has 20,000 bpm of production marked for the TMX pipeline coming online in Q1 2024, which should help the price MEG gets. The stock has shown resilience in 2023, with it outperforming peers during the weakness in the first half with lower oil prices weighing on the sector. The company has already bought back $227 million in shares year to date, cancelling 10.3 million shares in the process. This will continue to support a strong increase in the share price over time, as the company has chosen not to pay a dividend. While many solid dividend options exist in the Canadian oil patch, MEG is the best option for those looking for capital appreciation in a tax free account for example. Tax pools for MEG at WTI will have the company paying no cash tax until mid 2027, making the next few years extremely strong for cash generation even with a moderate WTI price. While others in the oil patch have similar losses to utilize, MEG has the best leverage if WTI ends up higher.

{kind=link}

MEG currently trades at just 7.8x trailing cash flow. As you can see that has barely increased over the past year and a half even as the stock has performed well, moving from $12 in January 2022 to $23.77 today. Valuations continue to stay low in the energy space, making it an ideal value play for those that see oil as important to energy security. Shares outstanding have been coming down steadily since the middle of 2022 with buybacks ready to ramp up in the coming year if oil prices remain at these high levels. This provides a solid floor under the share price as long as Oil remains above the important $70 WTI level it has flirted with recently.

MEG was previously one of the more indebted names in the Canadian oil patch during the last cycle, so to see them nearly debt free in 2024 is remarkable. Net debt is decreasing quickly with continued solid execution and the below chart demonstrates how far the company has come since 2016. Now the multiple can expand without significant costs for interest expense as it was a big issue in past periods.

{kind=link}

Conclusion: Top E&P to own

MEG energy is one of the top companies to own in the oil space due to its benefit from shrinking WCS differentials in 2024. The company has a reasonable debt level with 100% of free cash going to buybacks in the near future and the market pricing that in beforehand. While it pays no dividend at the moment the capital appreciation potential is quite impressive for MEG over a 3-4 year horizon with no cash taxes. Valuation is reasonable with strong netbacks on each barrel and moderate production growth into 2024. The recent pullback in the oil sector from demand concerns gives a great entry point into the shares for long term investors. As long as you believe that oil demand will continue to slowly grow over the next 30 years, the long lived assets MEG has will be instrumental and pay handsomely over time. As such I put a speculative buy rating on MEG with the stock ideal for those looking for torque to oil prices in Canada.

For further details see:

MEG Energy: Buyback Bonanza Likely Coming