MEGI - MEGI: A Hold For Capital Growth Income Seekers Might Seriously Consider

2023-11-24 08:15:00 ET

Summary

- Infrastructure is a resilient overlay to portfolios in times of market volatility and inflation.

- Infrastructure investments offer durable, cash-producing assets with low sensitivity to business cycle extremes.

- The MainStay CBRE Global Infrastructure Megatrends Term Fund offers a high dividend yield and can be a competent income vehicle.

- For those seeking capital appreciation, alternative instruments are recommended to meet investment objectives.

Investment outlook

The case for a strategic allocation to infrastructure is growing as a resilient overlay to portfolios at a time when markets are contending with multiple shock factors.

As markets digest these factors, dominated by inflation and central bank tightening, the 'resiliency' premium found in the infrastructure class is a potent measure to (i) protect investor capital (hence resiliency), and (ii) compound investor wealth over a long-term horizon (5-20 years).

Companies (and funds comprised of these companies) under the infrastructure banner often present with the following economic features:

- Durable, cash-producing assets (cyclical to the upside),

- Margin resilience, with the majority of the rate on cost fixed,

- Low sensitivity to business cycle extremes,

- Steady investment income/distributions backed by FCF etc. in (1),

- Little reinvestment or growth opportunities beyond fixed assets, so capital appreciation is cyclical.

Investors can strategically allocate to infrastructure through a number of ways.

One might consider owning real assets, private equity infrastructure, and individual rights.

As a powerful complement to owning these assets, one may also buy selective, individual equities (higher risk budget), or acquire a basket of securities, and monitoring this (moderate), to owning a diversified portfolio of assets in one instrument, through ETFs and MLPs and so forth (moderate). It depends on one's investment goals.

Infrastructure-backed ETFs are a liquid portfolio diversifier, typically owning sensible businesses with resilient cash flow/investment income. The MainStay CBRE Global Infrastructure Megatrends Term Fund ( MEGI) could offer value to investors (1) not necessarily concerned with capital appreciation, and (2) selectively after investment income.

Figure 1.

{kind=link}

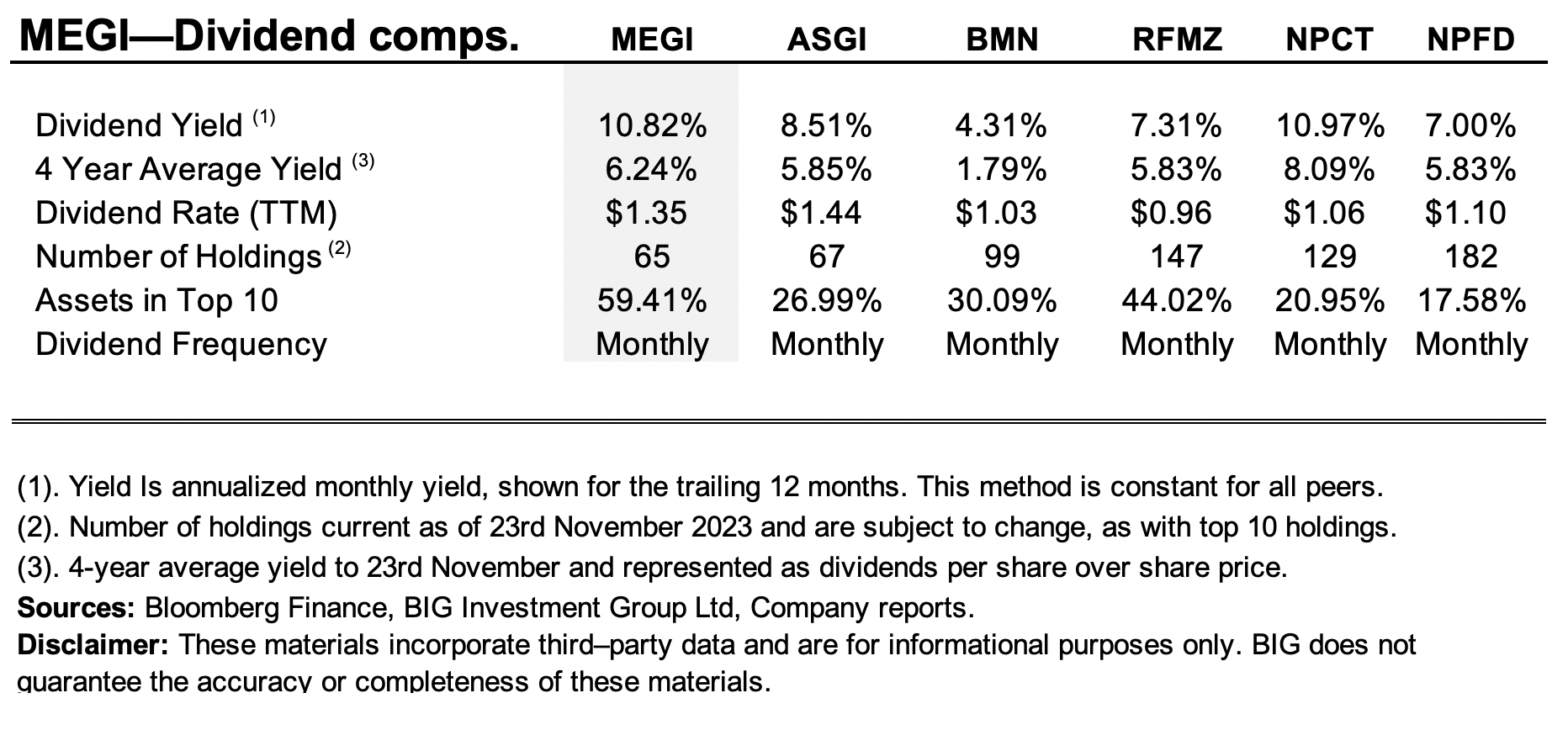

Here are the critical facts for MEGI:

- The fund was listed in 2021 at a market value of ~$1Bn and has traded lower to ~$750mm in AUM at the time of writing.

- Dividends are paid at the yield of 10.8% as I write, distributions are paid monthly on a $1.35 trailing payout.

- Highly concentrated fund with 60% portfolio weighted to top 10 holdings. The top position is 11% as I write, 65 positions in general.

- Sector bias to utilities (66.8%) followed by energy (11%) then real estate (7.8%), etc. Mostly US-weighted, reducing geopolitical infrastructure risk.

- High expense fee-1.92% of AUM, placing it in the upper bound of the fund universe.

- MEGI is structured with a 12-year limited term. It intends to liquidate on December 15th, 2033.

- According to the fund manager, the fund's investment objective " is to seek a high level of total return with an emphasis on current income ".

The fund's key dividend information relative to peers is seen in Figure 1. It is a reasonably fair playing field across names that commit to monthly distributions.

Figure 2.

{kind=link}

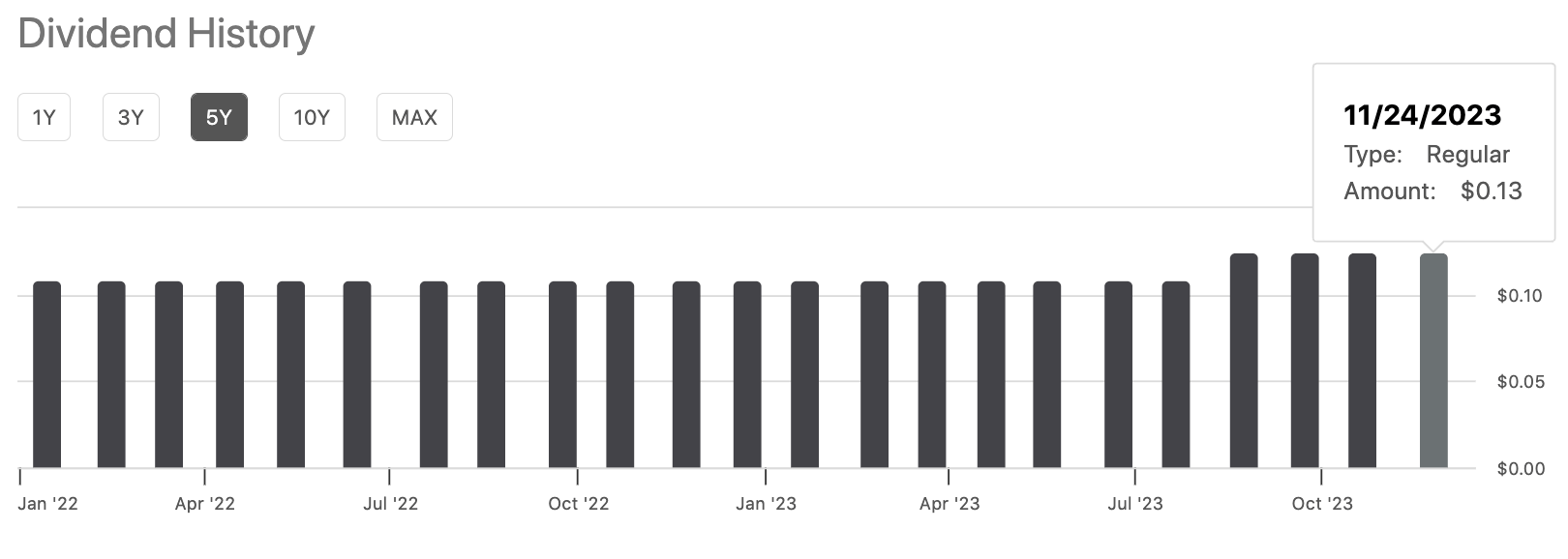

Figure 2a. MEGI Dividend history

{kind=link}

The opinion on a fund like MEGI depends entirely on the investor's critical preferences are (horizon, risk, size, and so forth). There is a clear investment case for buying the fund's 10% investment yield, distributed across a monthly horizon. The fund's market value was punished in '23 but found a bottom in October. Net-net, I rate MEGI a hold for those seeking capital appreciation. However, for those seeking investment income, MEGI may be worth serious consideration, as a competent income vehicle and tactical diversifier. This report will run through the logic.

Talking points

(1). All about the income

- The comparative benchmarks on yield stocks have risen sharply in the last 12 months. Cash + long-dated bonds now provide 4-5% starting yields with fewer risk parameters. Funds sporting anything above this level are worth the thoughtful analysis.

- Turn to MEGI's current dividend, constituting monthly income at 10-11% annualized yield as I write. This can be reinvested into more equity (automatically via DRIP) or taken as solid cash, and allocated elsewhere. MEGI is not the fund to own for tremendous capital appreciation in my opinion. This is one to own for the 'equity coupon' and sell near or at par at a future date.

- Companies underlying MEGI's monthly distribution stream are also of high credit and income quality. Most of the fund's assets are concentrated in utilities businesses, fitting the bill of a long compounder with low variance. As mentioned earlier, these are cash-producing assets, with tangible value.

- For example, when others might be concerned about the beta of their tech stocks in a volatile market, most of these companies are sitting with tremendous fundamentals, spinning off buckets of cash. The funding window opens up when the market values them lower, by lifting the yields on these companies (great for MEGI). The point is they throw off mountains of cash flow for the right shareholders. These assets are also embedded into societal fabric ensuring consistency and predictability in cash yield. In my opinion, this is a critical feature in the market of the coming decade.

- Finally, the monthly distribution, which is true capitalism by the way-efficiently recycling cash flow produced by private and public infrastructure into effective ways to benefit society-is one to consider under time value of money principles with higher rates.

This is an interesting value proposition - receive capital at 10% annualized via MEGI's distribution (for the time being), to potentially reinvest the capital elsewhere at rates above 10%. Keep in mind that distributions of such don't have to be reinvested in the same stock or spent on lifestyle. They can be allocated to other investments. This should only be done if $1 of investment produces more value than buying more of MEGI (or a risk-free rate) would.

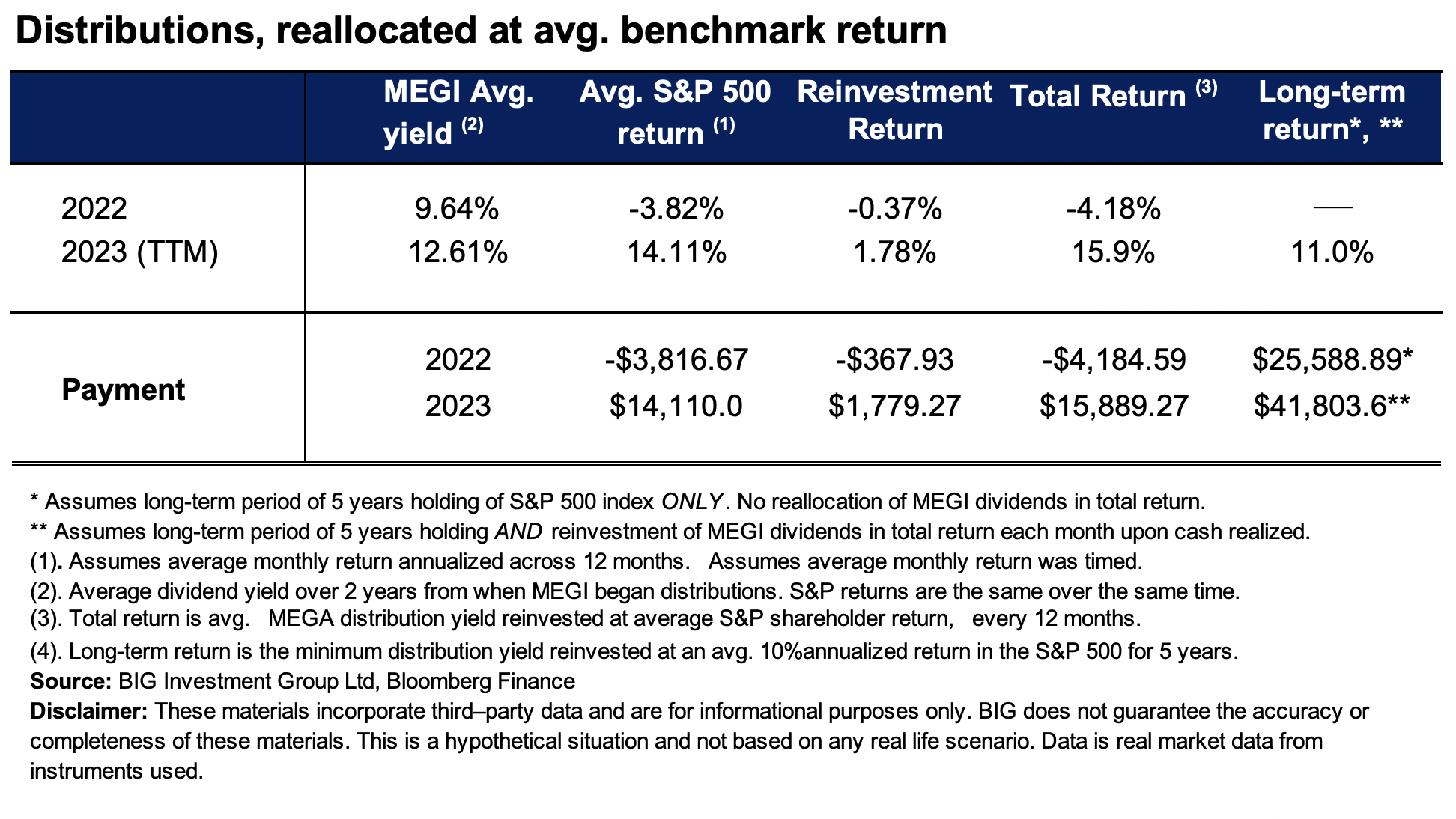

A simple thought experiment on this is shown in Figure 3. MEGI's min, max, and average dividend yield in 2022 and 2023 is shown, along with S&P 500 average monthly returns. The returns on two $100,000 long positions are noted: (i) dividend yield of owning MEGI, and (ii) capital appreciation of an S&P 500 index fund. It then tabulates the total return of reinvesting all MEGI dividends received each month at the average yield into the S&P 500 index fund at the average monthly return in 2022 and 2023.

- In a perfect world, investors might have reallocated an average of $1,779 of income per $100,000 owning MEGI in the last 12 months, buying at the average yield.

- This could have been recycled into an index fund such as the SPY and lifted a 14% outcome in 2023 to a 16% one. Because MEGI's distributions are paid monthly, this is a relevant exercise.

- Over the long term (5 years+), this has a considerable compounding effect in this hypothetical scenario.

Note these are very broad assumptions. They represent the notion of capital reallocation from dividends. Investors won't realize the full total shareholder return due to frictional costs associated with trading + brokerage, etc. Perfect timing is also highly unlikely.

Figure 3. Reinvestment scenario recycling max yield off MEGI into S&P 500 average return.

{kind=link}

(2). Infrastructure remains well positioned in current climate

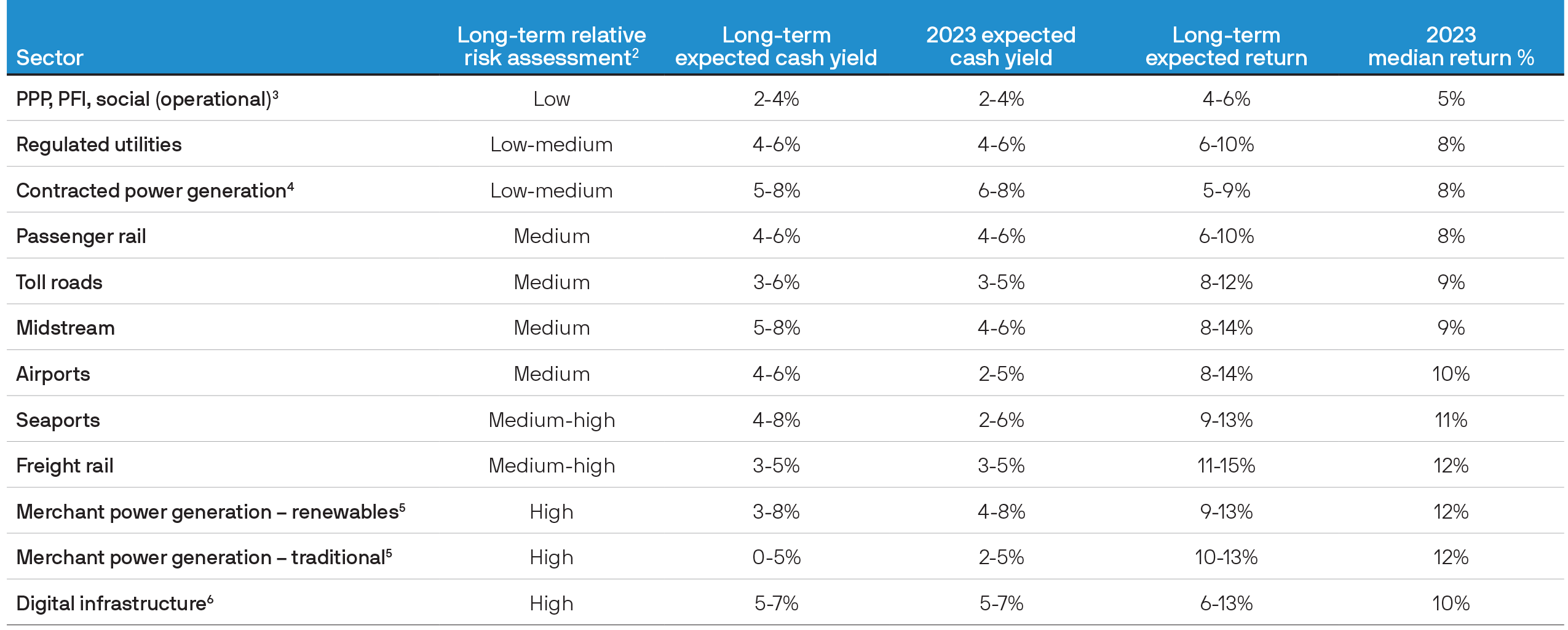

Investors were reminded of the importance of diversification in the 2022 rates-driven down market. Tangible assets arguably stand out in a new regime of higher rates and tighter growth. The crowd at JP Morgan outlined the "resilience and cycle agnostic nature" of infrastructure in a recent note . The firm says that volatility in the sector-especially in private infrastructure-is set to remain stable.

" The essential nature of infrastructure as an asset class has reduced the impact from recent macro-shocks, which has been illustrated by listed utilities performing strongly on a relative basis in 2022 ", it added. The firm's outlook across sub-sectors is seen below.

Most notably, its outlook on utilities is constructive, given the sector's essential services to society. The ability to pass through a higher cost of capital and commodity inputs is equally comforting. Further, as most core power generation assets have long-term offtakes in place, business returns have been stable, which helps investors in equity selection and portfolio positioning. A fund such as MEGI does this heavy lifting for you.

Figure 4.

{kind=link}

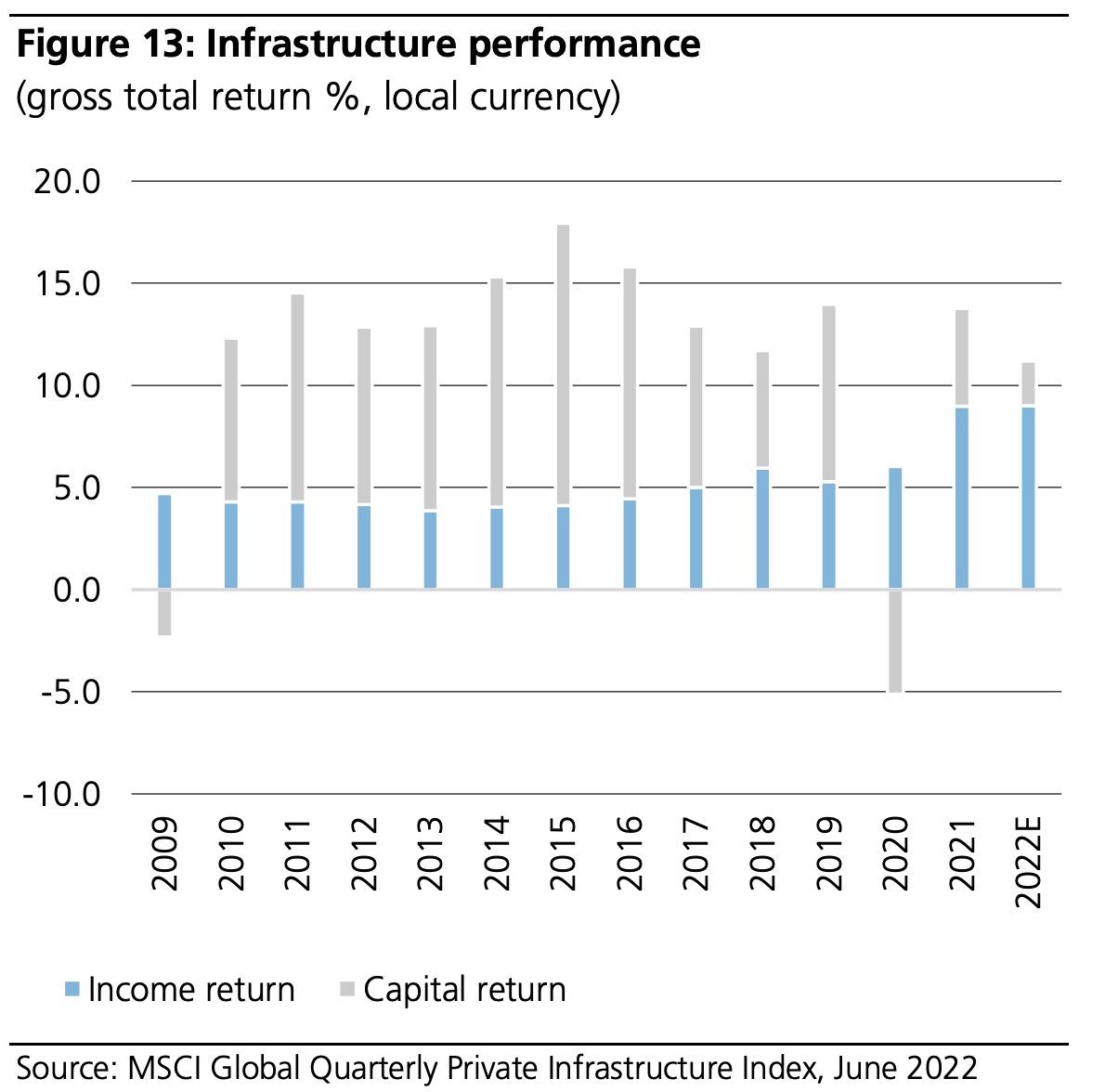

Those at UBS share the same palate in a note from earlier this year. In it, the bank explains that " judging by listed infrastructure revenues, the outlook is still relatively strong across the board, with previously underperforming industries such as toll roads and airports finally seeing strong recovery ".

The firm also notes that infrastructure performed well in periods of high inflation from 2005-2021. The spread widened when inflation occurred with low growth. The 2024 outlook of a similar macro climate provides a solid foundation for infrastructure to perform, therefore.

Figure 4a.

{kind=link}

The fact is that infrastructure assets possess desirable economic characteristics, especially in turbulent markets. These are cash-producing assets that have roots firmly established-hard to knock off, deep networks, high switching costs, regulation, and so forth. For example, it is nice to sit back at night and think that, whilst the Fed just pushed us up another 25bps, you're 5% weighted in real assets for instance that continue throwing off cash regardless.

Technical points for consideration

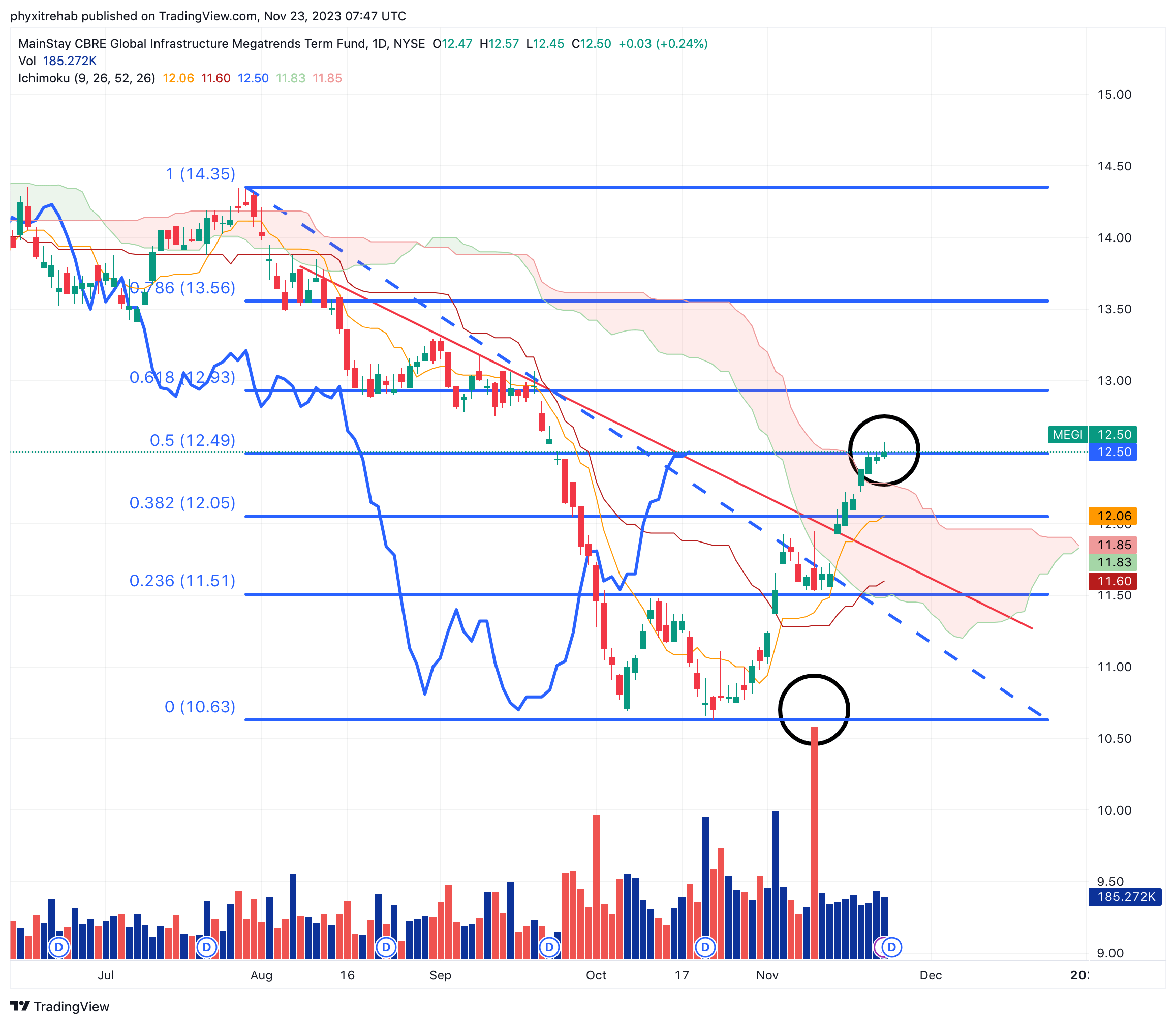

We have just reached a set of key technical milestones that need closer inspection.

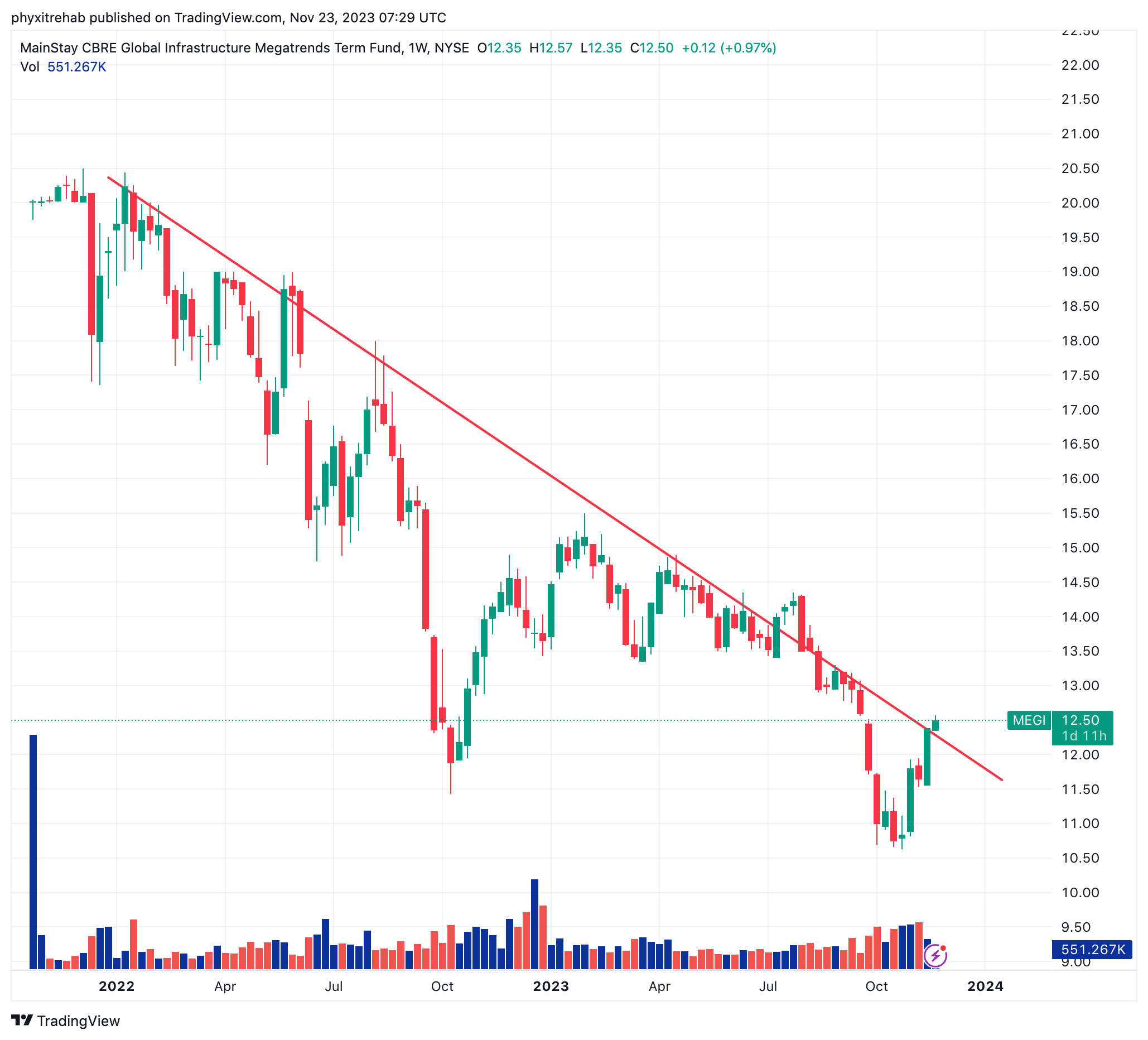

On the daily chart, looking to the coming weeks-

- We looked to have bottomed in October, and have just retraced 50% of the August to October selloff.

- This is a critical level and sees us cross above the cloud on the price line (top black circle). The lagging line has yet to nudge above but anything above $12.50 gets us there.

- The conversion and turning lines have crossed and are upward-facing.

- The first pullback is a classic cup and handle continuation, and the signal was the enormous selling day that didn't extend the price below the gap higher into November (bottom black circle).

- This is a constructive chart on the medium-term in my opinion. The next level on the upside is $12.95 then $13.50, $12.05 then $11.50 on the downside.

Figure 5.

{kind=link}

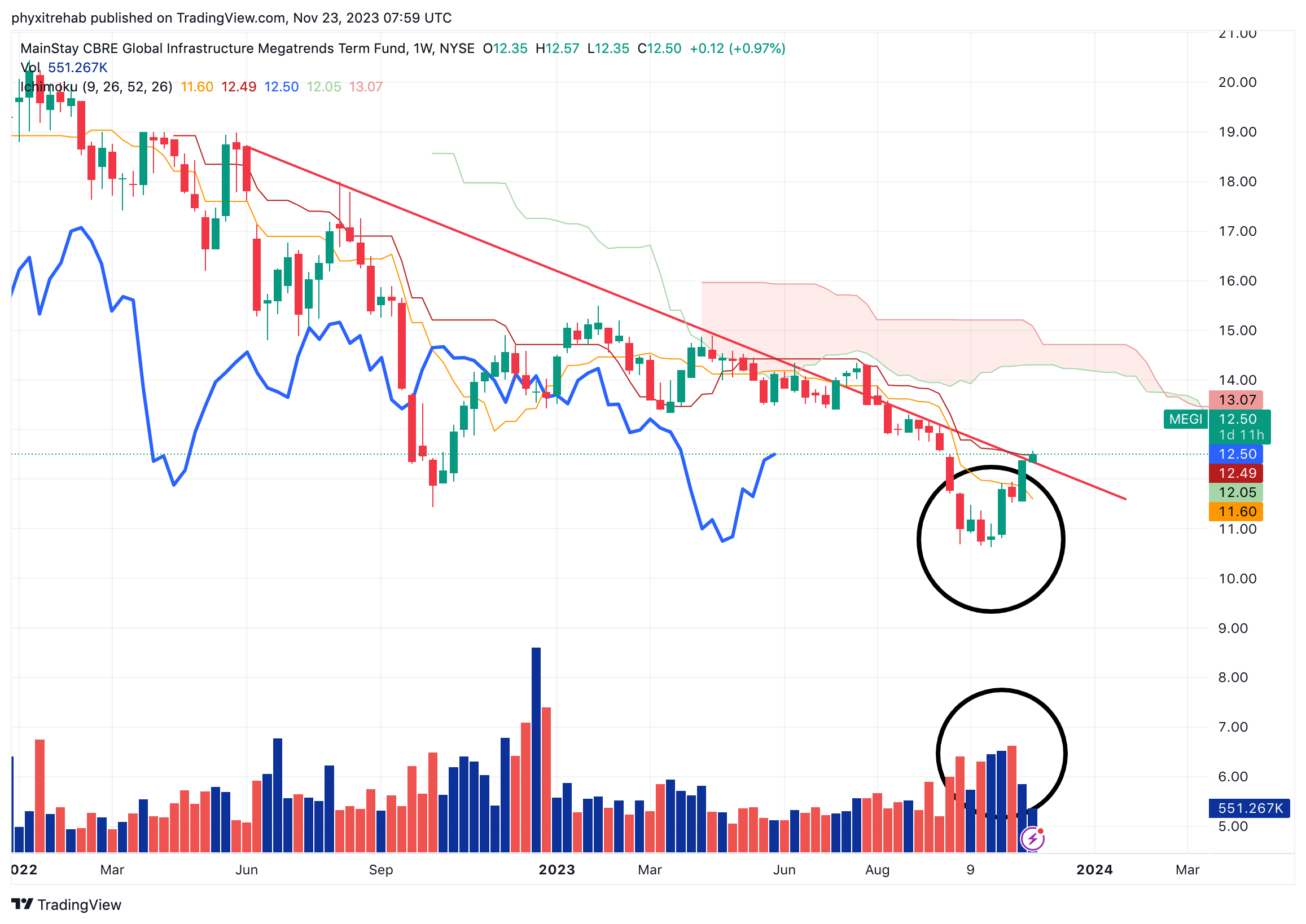

On the weekly chart, that looks to the coming months, there are the following observations:

- Ascending volume for the last 4 weeks before the pullback, preceding the reversal + price action.

- We are still neutral below the cloud and have a ways to go before turning bullish. Price and lagging lines are travelling with compressed cloud sideways.

- This chart is neutral in my view and indicates the potential for further sideways price action.

Figure 6.

{kind=link}

Discussion summary

Those investors seeking diversification of investment income may be drawn to asset classes such as infrastructure. Products such as MEGI provide this level of exposure to investors with a portfolio of securities in one liquid instrument. The fund's current distribution yield of >10% might be attractive to income-oriented investors who can stomach short-term volatility. Being an infrastructure holding, one might hope for more smooth returns from here. Readers will know that our core investment tenets focus on owning long-term capital compounders-a combination of yield and capital appreciation. We haven't the latter in the case of MEGI, so I rate the fund a hold.

For further details see:

MEGI: A Hold For Capital Growth, Income Seekers Might Seriously Consider